Life vs Health Insurance: Key Differences & Benefits

People confuse these two constantly. It’s understandable they both have "insurance" in the name, and you pay premiums for both. But they do opposite things. Life insurance is a check cut to your family when you die. Health insurance is the card in your wallet that keeps a hospital visit from bankrupting you while you're still breathing.

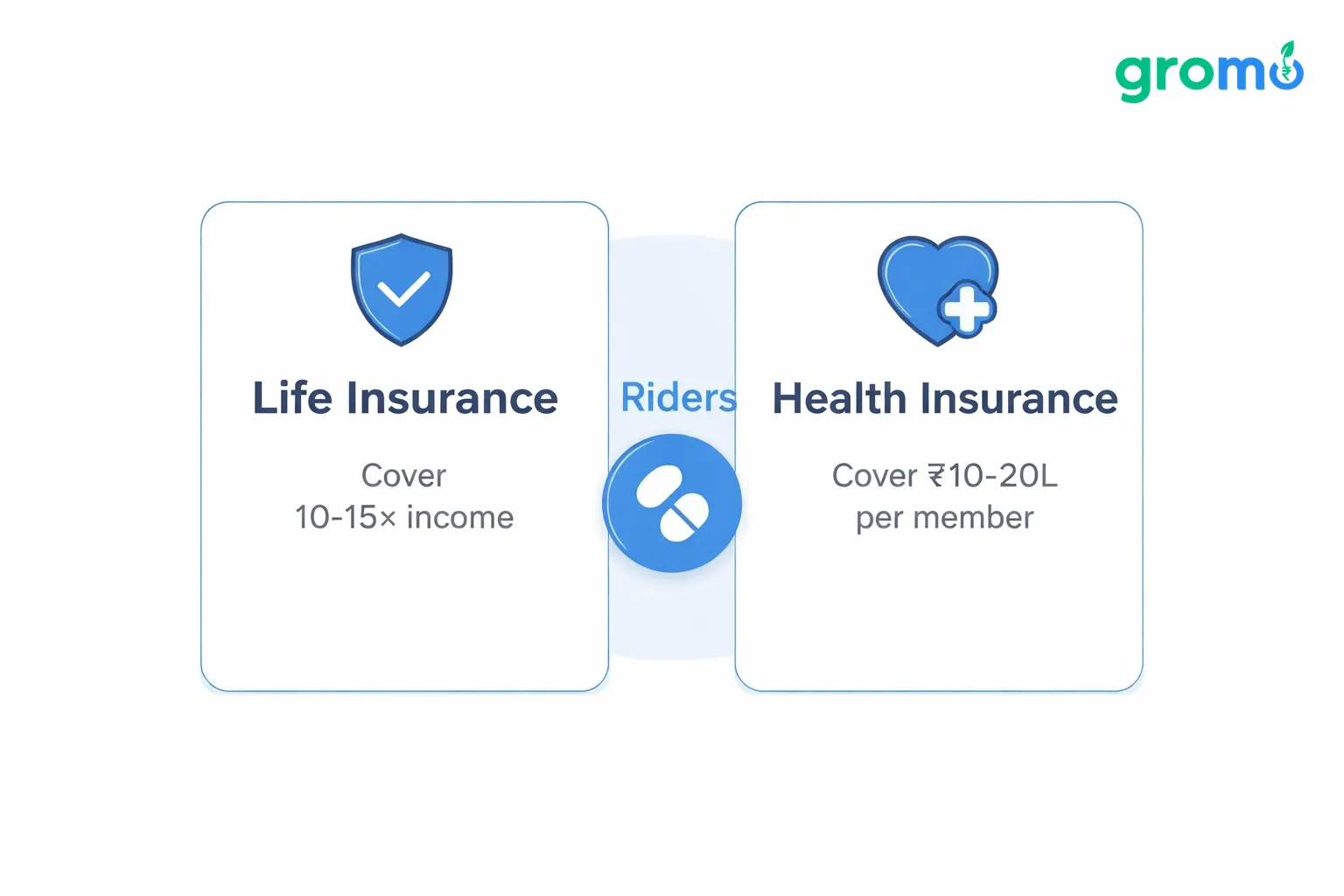

One protects your family's future; the other protects your current savings. One is a long-term safety net; the other is an active shield against medical expenses. You usually need both, but they play completely different positions.

What Life Insurance Actually Does

Life insurance pays out a set amount the "death benefit" to the person you name as your nominee. It doesn't pay you anything while you're alive (unless you have a specific endowment or ULIP plan, which is a different beast). Pure term life insurance, which is what most people should buy, only pays if you die during the policy term. If you outlive it, the policy just ends. There's no cash back.

For context, a ₹1 crore term cover for a healthy 30-year-old costs roughly ₹10,000–₹15,000 a year. If that person dies during the term, the family gets the full crore.

The whole point is income replacement. If you earn ₹8 lakh a year and support a spouse and two kids, your death erases that income. A ₹1 crore payout, invested safely at 7%, generates ₹7 lakh in annual interest almost replacing your salary. It also clears debts. Home loans, car loans, and personal debts get settled from the death benefit so your family doesn't have to deal with repossession or legal harassment.

Many employers offer group life insurance worth two or three times your salary. That sounds nice, but it vanishes the day you resign or retire. A personal term plan is non-negotiable if anyone relies on your income spouse, kids, parents, or siblings. If you're single with no dependents, you can probably skip it. But premiums are cheapest when you're young and healthy, so locking in a rate in your twenties or thirties is smart even if you aren't married yet.

Explore Life & Health Insurance Options Zero Investment

What Health Insurance Actually Does

Health insurance pays for your hospital stay room rent, surgeon fees, diagnostics, pharmacy bills, ICU charges, and pre/post-hospitalization costs up to your sum insured. It either pays the hospital directly (cashless) via network hospitals or reimburses you later if you go to a non-network provider. Unlike life insurance, this kicks in while you're alive. It covers planned surgeries like gallbladder removal or knee replacement, as well as emergencies like heart attacks or accidents.

Modern policies also cover day-care procedures like cataract surgery or chemotherapy that don't require a 24-hour stay. Pre-existing diseases get covered after a waiting period of two to four years. Comprehensive plans now include maternity, newborn care, and mental health treatment. Critical illness riders pay a lump sum if you're diagnosed with cancer, stroke, or kidney failure, independent of your actual hospital bills. You can use that money for treatment abroad or just to pay your rent while you recover.

Every adult needs this. Medical inflation in India runs about 14% a year double general inflation. A cardiac bypass in a metro hospital costs ₹5–₹8 lakh. Without insurance, families sell property or empty retirement accounts. Even employer-provided group health insurance is usually inadequate it ends when you leave the job, rarely exceeds ₹5 lakh, and often doesn't cover parents. A personal floater policy covering spouse, kids, and parents with ₹10–₹25 lakh cover ensures you aren't scrambling when you actually need it.

You can learn more about related financial products through Loan Partner Apps in India and explore how digital platforms simplify access.

Premiums: What You Pay and When

Life insurance premiums depend on your age and health when you buy the policy, but they stay fixed for the whole term. A healthy 30-year-old male pays about ₹12,000 a year for ₹1 crore of cover over 30 years. That ₹12,000 never changes, even when he's 55. But if you wait until you're 45 to buy that same cover, it costs ₹35,000 a year. Smokers pay 30–50% more. Avoid whole life or endowment plans they cost three to ten times more than term insurance because they mix in investment components, and the returns are usually mediocre.

Health insurance premiums reset every year. They go up as you age, as medical inflation rises, and sometimes if you make claims. A ₹5 lakh individual policy for a 30-year-old costs ₹6,000–₹8,000; for a 50-year-old, it's ₹20,000–₹25,000. A family floater covering two adults and two kids with ₹10 lakh cover costs ₹15,000–₹20,000 annually when the parents are in their thirties, but jumps to ₹40,000+ in their fifties.

Budgeting rule of thumb: Spend 1–2% of your annual income on life insurance and 2–4% on health insurance. If you earn ₹10 lakh a year, that means ₹10,000–₹20,000 on term life and ₹20,000–₹40,000 on health cover. Also, couples should buy separate term policies, not joint ones. Joint plans pay once on the first death, leaving the survivor with no coverage.

For those interested in zero-investment business models that complement insurance earnings, visit Zero Investment Business Ideas in India 2026.

The Tax Angle: Section 80C and 80D

Life insurance: Premiums qualify for a Section 80C deduction up to ₹1.5 lakh annually. If you pay ₹12,000 for a term premium and fall in the 30% tax bracket, you save ₹3,600 in tax. The death benefit paid to your family is entirely tax-free under Section 10(10D).

Health insurance: Premiums qualify for Section 80D. You get ₹25,000 for yourself, spouse, and kids; another ₹25,000 for parents under 60; or ₹50,000 for parents over 60. If you pay ₹20,000 for your own health insurance and ₹30,000 for your senior-citizen parents, you claim ₹50,000 total, saving ₹15,000 at the 30% bracket. Preventive health checkups of up to ₹5,000 per year also fall within the ₹25,000 limit.

Combined: A salaried individual can claim ₹1.5 lakh under 80C (life premium, ELSS, PPF, EPF) and ₹75,000 under 80D (₹25,000 self + ₹50,000 senior parents). That reduces taxable income by ₹2.25 lakh. At 30% tax plus cess, that's over ₹70,000 saved enough to cover most of your insurance costs.

Understanding compliance and documentation is crucial; refer to Self-Attestation Guide 2026 for KYC processes.

Where They Overlap (and Where They Don't)

Some life insurance policies ULIPs, endowments, money-back plans include accident or critical-illness riders. These pay a lump sum on disability or diagnosis, but they don't replace real health insurance. Riders have lower limits (₹10–₹25 lakh), only cover specific listed illnesses, and don't pay for room rent or outpatient care. If a rider pays you ₹10 lakh for a cancer diagnosis, you still need health insurance to pay for the chemotherapy.

On the flip side, health insurance never replaces life insurance. Even with ₹50 lakh health cover, your family gets nothing if you die of a heart attack in your sleep. Health insurance is a reimbursement contract; life insurance is a benefit contract. Don't confuse hospital cash policies (daily allowance plans) with life insurance they're supplementary, not income replacement.

The danger is over-insuring one and under-insuring the other. A ₹2 crore term plan is useless if a single illness drains your savings because you skipped health insurance. And ₹1 crore health cover won't help your family if you die suddenly without life insurance.

Balance: Life cover should equal 10–15 times your annual income. Health cover should be ₹10–20 lakh per family member, increasing with age.

Explore related earning opportunities through GroMo Earnings to supplement your insurance budget.

How Claims Actually Work

Life insurance claims happen after death. The nominee submits the death certificate, policy document, claim form, and (for accidental death) the FIR or post-mortem report. Insurers investigate claims made within the first two years the "contestability period" to check for fraud or hidden health conditions. After two years, claims are usually settled without investigation unless foul play is suspected. The money lands in the nominee's bank account in 7–30 days.

Health insurance claims kick in when you're hospitalized for 24 hours or more (or less for day-care). For cashless claims, you notify the insurer before planned surgery. They approve a limit, and the hospital bills them directly. You only pay for non-covered items. For reimbursement, you pay the hospital first, then submit the discharge summary, bills, and reports within 15–30 days.

Why claims get rejected: Life insurers deny claims if you hid diabetes, hypertension, or smoking on the application and died of related issues within two years. Health insurers reject claims for pre-existing diseases within waiting periods, cosmetic surgery, or hospitalization under 24 hours without a day-care code. Read the fine print and disclose everything upfront.

For insights into financial product distribution and compliance, visit Financial Product Distribution in India.

Portability: Can You Switch?

Life insurance: No. You can't transfer a policy to another insurer mid-term. If you're unhappy with your insurer, you have to surrender the policy losing any bonuses or paid premiums and buy a new one at your current, older age. Term policies are renewable until age 65 or 75, and premiums stay fixed if you locked them in at the start.

Health insurance: Yes. IRDAI rules let you switch insurers after holding a policy for 12 months. You keep your no-claim bonus and don't have to re-serve waiting periods for pre-existing diseases, provided you apply 45 days before renewal. But portability doesn't guarantee lower premiums just continuity.

Health policies are guaranteed renewable until age 65 (some offer lifelong renewability). Insurers can't refuse renewal based on claims, but premiums will rise. Floater policies get expensive once the main insured person crosses 55; splitting seniors onto individual plans while keeping younger family members on a floater often saves money.

Understanding how digital lending complements insurance purchases is explained in RBI-Approved Loan Apps India 2026.

Do You Really Need Both?

Yes unless you have ₹5+ crore in liquid assets generating enough passive income to replace your salary and cover any medical crisis. For almost everyone else, both are mandatory.

Priority for young singles: Get health insurance first (₹5–₹10 lakh). Buy term life after marriage or when you have dependents.

Priority for young couples: Term life for the primary earner (₹1 crore), family floater health insurance (₹10 lakh), then add coverage for the secondary earner.

Priority for mid-career: Increase term life to 15x income, upgrade health to ₹25 lakh with a super top-up, add a critical illness rider, and buy separate senior-citizen health policies for your parents.

Common mistakes:

Relying only on employer insurance (it ends when you leave).

Mixing investment and insurance (ULIPs and endowments usually have poor returns).

Under-insuring (₹5 lakh health or ₹25 lakh life is not enough).

Waiting too long (premiums roughly double every decade you delay).

Automate your premiums so you don't lapse. A lapsed policy means you lose benefits and have to pay penalties to revive it.

For strategies to balance insurance and income generation, see Passive Income Ideas India 2026.

Specific Examples: What Covers What?

Gallbladder stone surgery: Covered by health insurance if the hospitalization is over 24 hours or it's a day-care laparoscopic procedure. Costs run ₹50,000–₹1.5 lakh. Life insurance pays nothing unless you die during surgery, which is rare.

Parkinson's disease: Health insurance covers hospitalization for complications like pneumonia or falls, and deep brain stimulation surgery. It doesn't usually cover ongoing OPD consults unless you have that rider. Life insurance pays the death benefit if Parkinson's contributes to your death, but you must disclose it when you buy the policy. If you hide it and die within two years, the claim can be denied.

Heart attack: Health insurance covers angioplasty, bypass, ICU, and rehab. A critical illness rider on your life insurance pays a lump sum (₹5–₹25 lakh) on first diagnosis, regardless of hospital bills. That money can cover lost income or alternative treatment.

Accidental death: Life insurance with an accidental death benefit rider pays double the sum assured ₹2 crore if your base cover is ₹1 crore. Health insurance covers the hospital bills from the accident, but pays nothing on death. Personal accident insurance is a separate product that covers death and disability, often with lower limits.

Learn about credit products that complement insurance planning through How to Improve Your Credit Score India 2026.

How to Choose

For life insurance: Look at the Claim Settlement Ratio (CSR). Insurers with 98%+ CSR (LIC, HDFC Life, Max Life) are safer bets. Compare the cost per lakh of cover; for a 30-year-old, term insurance should cost about ₹10–₹15 per lakh annually. Don't mix insurance with investment buy pure term and invest the difference in mutual funds or PPF.

For health insurance: Check the network hospital count in your city (aim for 500+), cashless approval rate (95%+ is good), and avoid policies with co-payment clauses (where you pay a % of the bill). Look for policies without room-rent caps. Use aggregator sites to compare premiums, but try to buy directly or through a trusted advisor for better claim support.

Worthwhile riders: Critical illness (lump sum), waiver of premium (keeps policy active if you're disabled), and hospital daily cash (for attendant costs). Skip accidental death riders if your term cover is already high enough.

For referral-based income models that work alongside advisory roles, explore Legit Refer and Earn Apps 2026.

Frequently Asked Questions

Q: What is the difference between health insurance and life insurance?

A: Life insurance pays your family a lump sum when you die. Health insurance pays your hospital bills while you're alive. One replaces income; the other protects savings.

Q: Is a gallbladder stone covered in health insurance?

A: Yes. Removal surgery is covered if you're hospitalized for over 24 hours or it's a laparoscopic day-care procedure. Cashless claims need pre-authorization. Costs are usually ₹50,000–₹1.5 lakh.

Q: Is life or health insurance better?

A: You need both. Life protects your family if you die; health protects your savings if you get sick. Skipping either leaves a gap.

Q: Does life insurance cover Parkinson's?

A: It pays the death benefit if Parkinson's contributes to your death, provided you disclosed it when buying the policy (or it was diagnosed after the two-year contestability period). It doesn't pay for treatment health insurance does that. Some critical illness riders may pay a lump sum on diagnosis if listed in the policy.