Financial Product Distribution in India: Earn Online with GroMo

Financial product distribution in India is growing fast. The basic idea is simple: you connect people who need financial products credit cards, loans, demat accounts with the banks and institutions that offer them. You get paid a commission for every successful connection.

How distribution changed

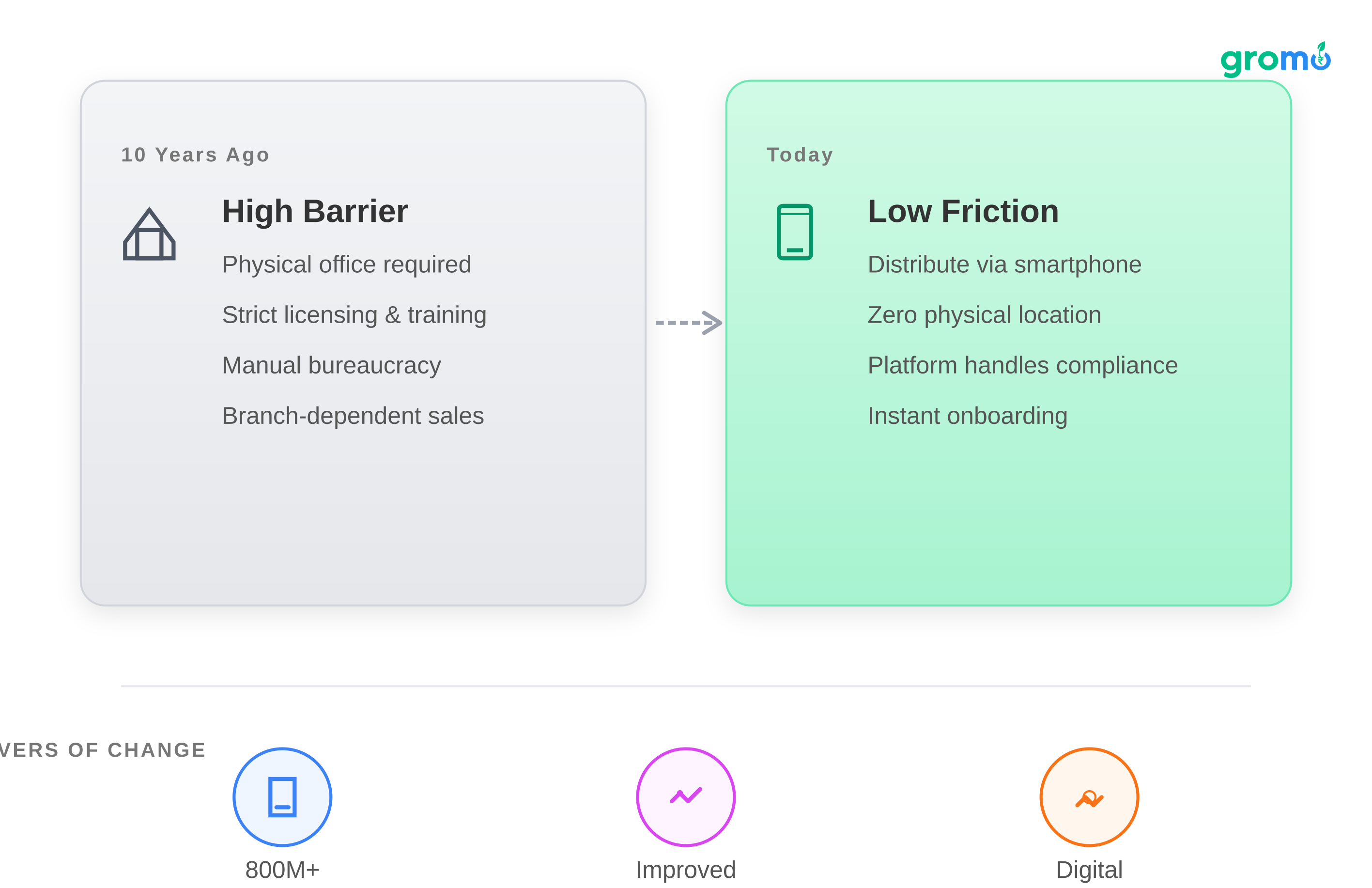

Ten years ago, you needed to be an insurance agent or work at a bank branch to sell financial products. The barrier to entry was high licensing, training, regulatory approvals, physical office space.

Now? You can become a distributor with a smartphone. Digital platforms have removed most of the friction. You don't need a physical location, and you don't need to navigate regulatory bureaucracy yourself. The platforms handle that.

Three things drove this shift: smartphone penetration in India crossed 800 million, digital literacy improved, and banks realized that acquiring customers through digital channels is cheaper than maintaining branches.

How the money works

The model is straightforward. You get access to products from multiple banks. Each product has a fixed commission. A successful credit card referral might pay ₹400-₹2,400 depending on the card and bank.

Everyone wins something:

Banks acquire customers without spending on advertising

Customers get recommendations from someone they know

You earn commissions without taking on risk

Start Your Distribution Journey - Download GroMo Now

What sells and what it pays

Credit cards are the easiest starting point. Commissions range from ₹500 to ₹2,400 per approval. Approval rates are decent, and the process is quick. Premium cards pay more but require customers with higher incomes. Entry-level cards pay less (₹400-₹800) but are easier to sell.

Personal loans and business loans pay the most ₹1,000 to ₹3,000 or more per disbursal but they're harder to close. Stricter eligibility, longer processing times, lower approval rates.

Savings accounts and demat accounts pay less per transaction (₹300-₹800) but convert easily. A digital savings account can be opened in 10 minutes through video KYC.

Credit lines (buy-now-pay-later, revolving credit) are growing. Investment products like mutual funds sometimes offer recurring commissions rather than one-time payouts.

Why platforms matter

You could try to build relationships with individual banks, but that's inefficient. Modern platforms like GroMo give you access to 80+ products in one app.

The better platforms also show you which products your customers are most likely to get approved for AI-powered matching that saves time and improves your success rate.

The other big change is payout speed. Traditional agents waited 30-90 days for commissions. Digital platforms credit your wallet within 24-48 hours of a confirmed sale, and you can withdraw once you hit ₹100.

Join 14 Lakh+ Partners Earning with GroMo

How to actually build this business

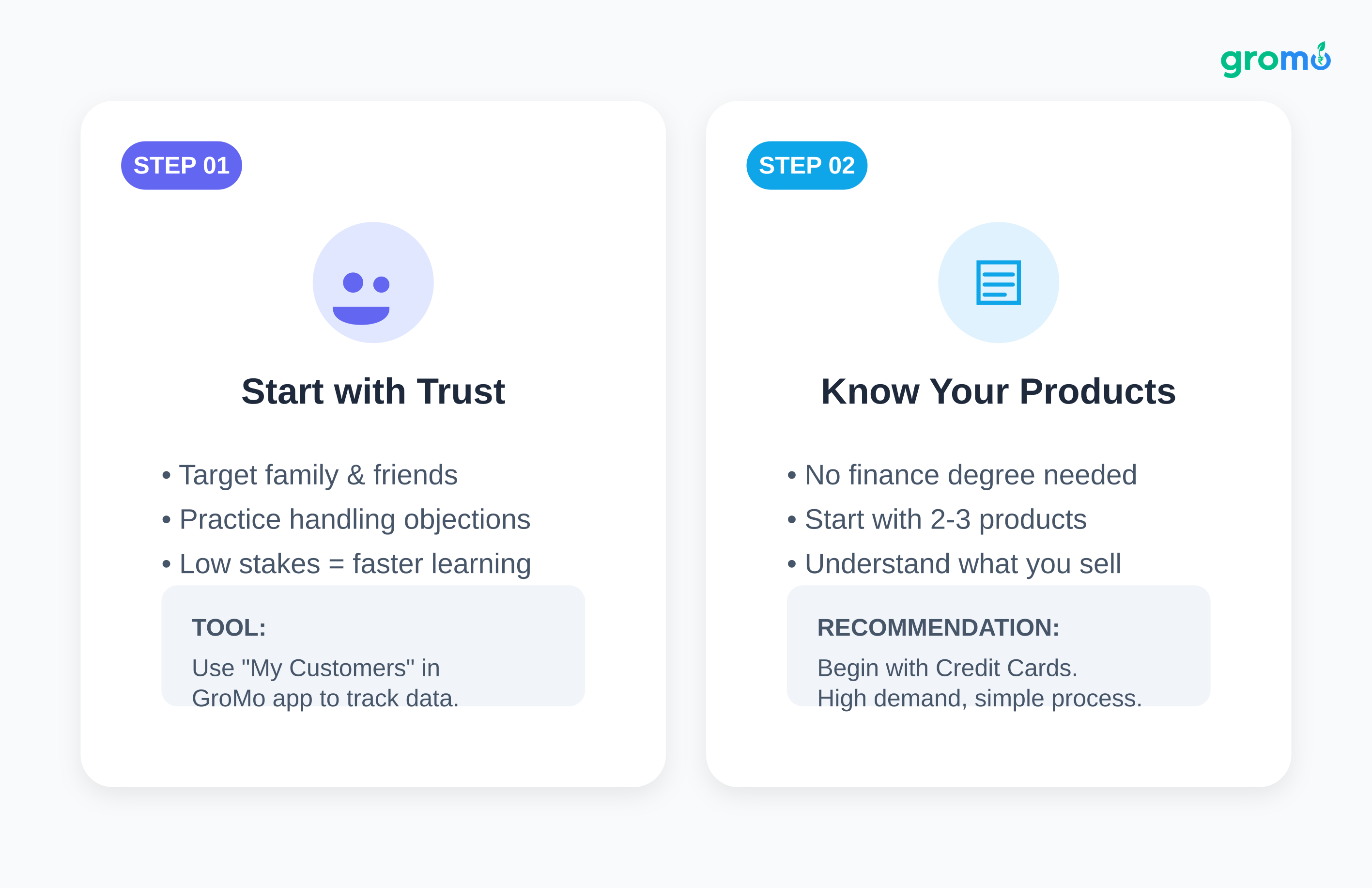

Start with people who trust you

Your first sales will come from family, friends, colleagues. These are lower-stakes interactions where you can learn your pitch and handle objections without freezing up.

Use the "My Customers" feature in the GroMo app to track basic information occupation, income range, existing banking relationships, immediate financial needs.

Know your products

You don't need a finance degree, but you need to understand what you're recommending. Start with 2-3 products in one category. Credit cards are good for beginners relatively simple, high demand, decent commissions.

Attend the training sessions most platforms offer. They're usually daily, usually live, and usually taught by product experts.

Check eligibility before you pitch

The biggest rookie mistake is pitching the wrong product to the wrong person. If someone has a credit score of 600, don't pitch them a premium card they'll get rejected for. It wastes their time and damages your credibility.

Use the eligibility checkers. Show people products they can actually get approved for.

Follow up

Most sales don't close on the first conversation. Set reminders. A customer who doesn't need a credit card today might need a personal loan in three months.

Gamification and rewards

Some platforms use coin systems alongside cash commissions. You might earn coins for creating leads, coins for successful sales. The coins can be converted to cash or used in app marketplaces.

There are also tier systems (Silver, Gold, Platinum) that unlock higher commission rates and better support as you hit milestones.

The referral multiplier

You can also earn by recruiting other distributors. When someone you refer makes their first sale, you might earn ₹100. As they hit milestones, you earn more sometimes ₹7,000-₹10,000 total per successful referral.

This is different from MLM because your earnings are tied to their actual performance, not to endless recruitment. You can also just sell directly and never recruit anyone.

Mistakes to avoid

Don't overpromise. Financial products are regulated. If you guarantee approvals that don't happen, or misrepresent terms, you'll get complaints and possibly deactivated.

Don't treat people as one-time transactions. A customer who trusts you might use 5-6 different products over several years. That's worth more than a single commission but only if you maintain the relationship.

Don't be careless with data. You'll handle PAN numbers, income details, contact information. Use the platform's secure tools, not a random spreadsheet.

Don't push high-commission products inappropriately. Just because something pays well doesn't mean it's right for every customer.

Don't quit in the first month. There's a learning curve. Your first weeks will be awkward and probably not very profitable. Push through it.

What you can realistically earn

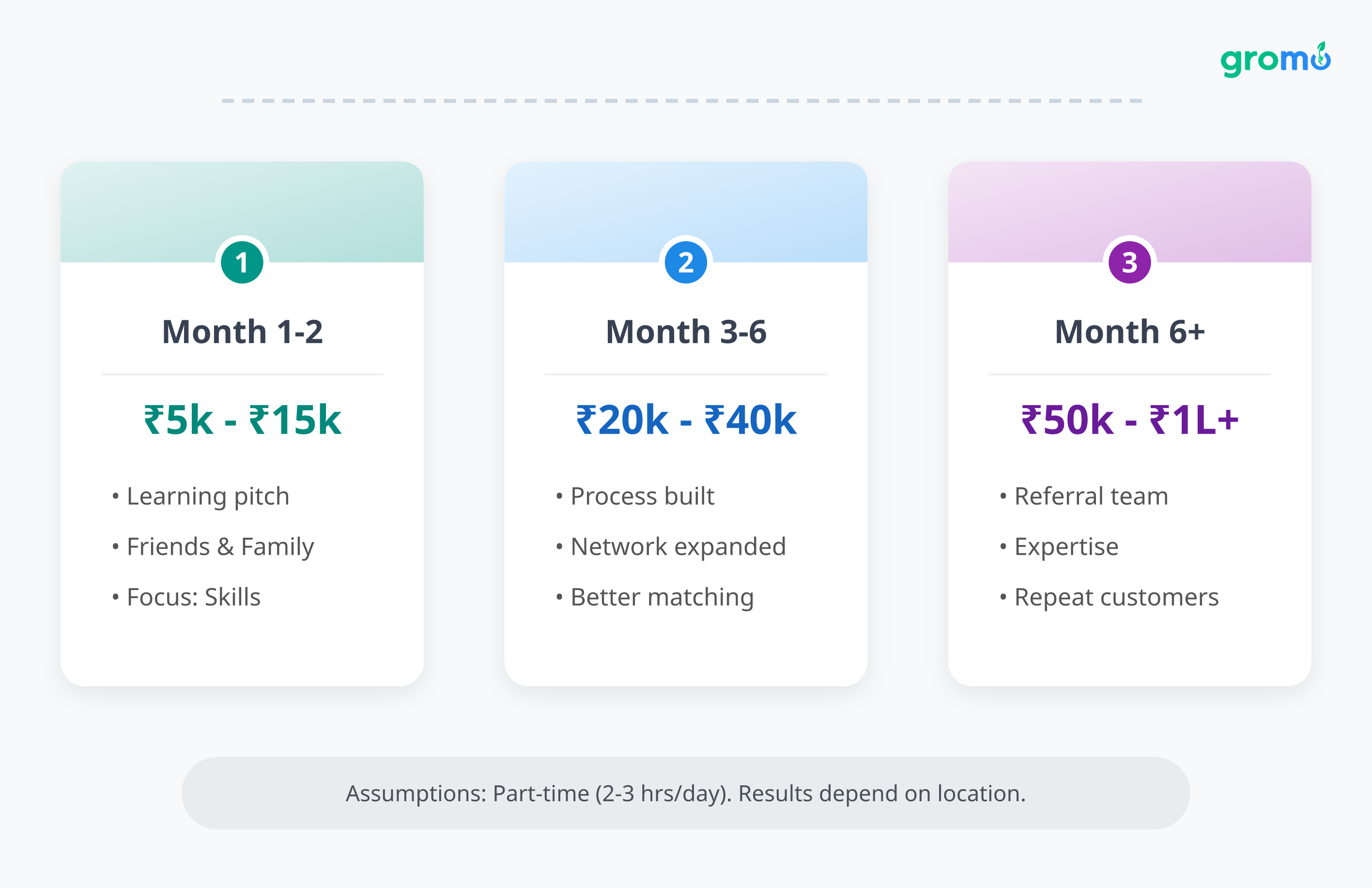

Month 1-2: ₹5,000-₹15,000. You're learning products, developing a pitch, selling to friends and family. Focus on skill-building, not income.

Month 3-6: ₹20,000-₹40,000. You've built a process, expanded beyond your immediate network, improved your matching.

Month 6+: ₹50,000-₹1,00,000+. You've built a referral team, developed expertise, accumulated repeat customers.

These numbers assume part-time effort (2-3 hours daily). Your results will also depend on location metro areas with higher-income customers typically produce higher earnings.

For more on realistic timelines, see this guide on earning ₹1 lakh monthly while working full-time.

Tools worth using

WhatsApp Business for customer communication. Use catalogs, quick replies, labels.

Content templates that platforms provide digital visiting cards, mini-websites. They look more professional than something you cobble together yourself.

CRM habits. Set specific times for follow-ups. Track birthdays and life events that might signal financial needs.

Communities. Join the WhatsApp groups and forums where successful distributors share strategies.

For those starting with zero capital, see this guide on starting earning with zero investment.

What's coming next

AI-powered matching is getting better. Platforms are using machine learning to predict which products fit which customers. Distributors who use these tools will outperform those who rely on gut instinct.

Video is becoming standard. Video KYC, video product explanations, video testimonials. If you're comfortable on camera, you'll have an advantage.

Financial products are being embedded into non-financial platforms e-commerce checkouts, gaming apps, educational platforms. New contexts for distribution.

Rural India is coming online. As smartphone adoption spreads to tier 3 and 4 towns, the potential customer base is expanding dramatically.

For more on legitimate online earning opportunities, see making money online in India.

Starting today

Day 1: Download a platform app, register, complete basic onboarding.

Day 2-3: Go deep on one product category (start with credit cards). Understand eligibility, benefits, application process, common objections.

Day 4-7: Build a list of 20-30 people in your network. Note their profiles and which products might suit them.

Week 2: Make 10 product recommendations to qualified prospects. Learn from the interactions.

Week 3-4: Attend daily training, refine your approach, aim for 2-3 successful conversions.

Month 2+: Systematize your routine, expand beyond warm contacts, consider building a referral team.

The industry is growing at 25%+ annually. There's real money here ₹100+ crore already paid out to distributors, 14 lakh+ active partners. The question is whether you'll take the first step.

FAQs

Do I need special qualifications?

No. Platforms provide training. You don't need a finance degree or prior sales experience.

How much do I need to invest?

Zero. You need a smartphone and internet. If a platform asks for upfront payment, it's probably a scam.

How long until I get paid?

Modern platforms credit your wallet within 24-48 hours of a confirmed sale. You can withdraw once you hit ₹100-₹500.

Can I do this part-time?

Yes. Most successful distributors start part-time 1-3 hours daily while keeping their day job.

Is this MLM?

No. The focus is selling actual products to end customers. Referral programs exist, but they're tied to actual performance. You can earn significant income purely from direct sales without ever recruiting anyone.

What if customers have problems?

The platform and the financial institution handle customer service. You make introductions and provide initial information. If problems arise, they work directly with the bank or platform support.