Self-Attestation Guide 2026: How to Do It Right

If you've ever applied for a credit card, loan, or even a savings account in India, you've seen the demand: "Please submit self-attested copies." It sounds formal. Maybe even a little intimidating if it's your first time. Do you need a notary? A gazetted officer?

Actually, no. You just need a pen.

Here is the reality of self-attestation in 2026: it is a simple way to certify that a photocopy matches your original document. Instead of hunting down a government official to sign your papers, you do it yourself. You are essentially saying, "I promise this copy is real."

Financial institutions need this for KYC norms, fraud prevention, and audit trails. It saves them time and saves you the hassle of finding a notary for every single application.

How to actually do it

The process is simple, but banks and NBFCs are picky. If you mess it up, your application stalls.

Physical copies:

Take a clear photocopy of the original. Sign across the copy your signature should touch both the document text and the white border. Add the date. Some people write "True Copy" or "Self-Attested" for extra clarity, though just the signature is usually enough. Make sure the signature looks like the one on your PAN card or Aadhaar.

Digital copies:

Scan the document or take a photo. You can add your signature using a stylus, or sign the physical copy before scanning. Most financial apps now have built-in tools for this. When you upload a document to Axis Bank or Unity SFB's app, it often adds the attestation overlay automatically.

Start Your Financial Product Journey Today

Where people mess up

It's usually the small things that get an application rejected.

Signature placement: Don't just sign the white margin. The signature has to overlap the document. This proves you didn't just paste a new photo or text over an old copy.

Consistency: If your PAN signature is a chaotic scribble, don't suddenly write a neat, full name on your self-attestation. It looks suspicious. Try to match your registered signature.

The pen color: Use blue or black ink. Red or green ink is often rejected or flagged as unprofessional.

The date: Always date it. Some banks won't accept undated documents, especially for things like bank statements or salary slips.

Scan quality: A blurry photo of a document is a guaranteed rejection. Make sure the text is readable.

What actually needs attestation?

When applying for products through platforms like GroMo or directly with banks, these are the usual suspects:

Identity: PAN (mandatory), Aadhaar, Passport, Voter ID, Driving License.

Address: Aadhaar, Passport, recent utility bills (under 3 months), rent agreement, or bank passbook.

Income (Salaried): Last 3 months' salary slips, Form 16, 6-month bank statement showing salary credits.

Income (Self-Employed): Last 2 years' ITR, bank statements (6-12 months), GST certificate, Udyam registration.

Other stuff: Cancelled cheques for loan disbursal, photos, educational certs for student cards.

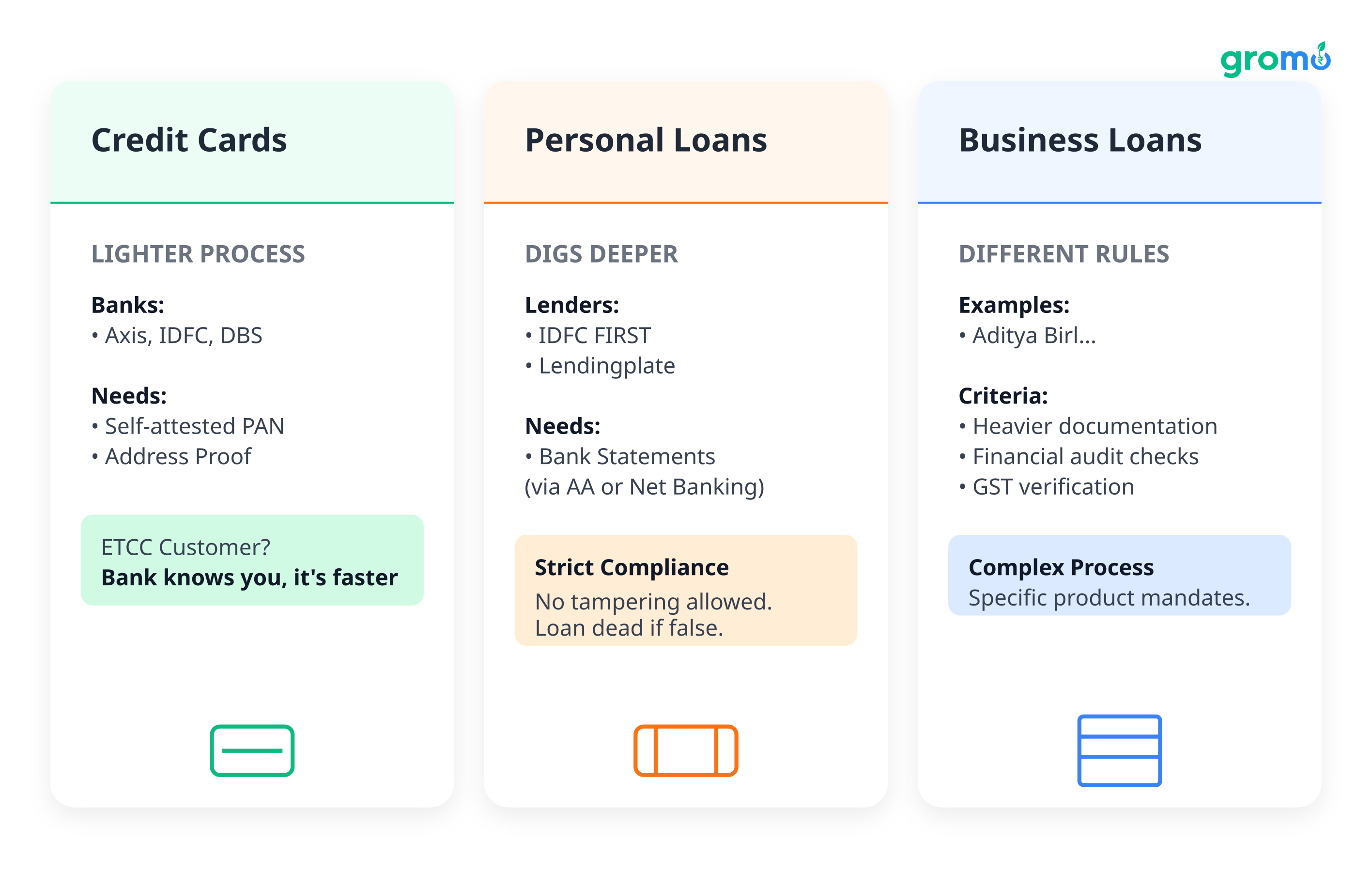

Does the product type change the rules?

Yes. A credit card application is lighter on paperwork than a business loan.

Credit Cards

Axis, IDFC, DBS they mostly want self-attested PAN and address proof. If you're applying for a card like the Axis MyZone, the process is quick. ETCC (Existing to Credit Card) customers often have it easiest since the bank already has their data.

Personal Loans

Lenders like IDFC FIRST, Lendingplate, or Unity SFB dig deeper. They want the PAN and Aadhaar, sure, but also bank statements uploaded via Account Aggregator or net banking.

A specific warning on IDFC FIRST loans: they run tight compliance. If you tamper with a bank statement or let a third party "handle" the attestation, you will get caught and rejected.

Business Loans

Products like Aditya Birla Udyog Plus need more business-side proof. PAN (individual or company), GST, Udyam registration, ownership proof. If the loan is over ₹10 lakhs, expect co-applicant paperwork, too.

Savings & Demat Accounts

Digital accounts (DBS, Kotak 811) rely heavily on Video KYC (VKYC). You show the original card to the camera. That act serves as the attestation.

Is this legally actually valid?

Yes. The government has pushed self-attestation to cut red tape. The Department of Personnel and Training (DoPT) allowed it for government apps, and RBI extended it to financial services.

It carries the same weight as a notarized document for most uses. But there is a catch: if you attest a fake document, you are liable. You cannot claim a "clerical error." Banks verify originals during VKYC or in-person checks, so lying is a fast way to get blacklisted.

The tech shift: AI, DigiLocker, and VKYC

In 2026, the process is less about pens and more about pixels.

AI Checks: Lenders use AI to spot edited files or mismatched signatures. It flags inconsistencies a human might miss.

DigiLocker: Platforms like Lendingplate pull documents directly from DigiLocker. Since the issuer (the government) provides the file, it is pre-verified. You skip the attestation step entirely.

Video KYC: For Unity SFB or DBS accounts, the VKYC call is the attestation. You show the original PAN card to the agent. They screenshot it. You say "Yes, that's mine." Done. Unity SFB even has a "silent mode" for VKYC where you just show the docs without speaking.

Join 60L+ Partners Earning with GroMo

If you're a GroMo Partner

If you distribute products via GroMo, documentation issues kill your conversions. You can fix that.

Pre-qualify the lead. Ask if they have the docs ready before you send the link. Do they have the original PAN handy? Is their address proof under 3 months old?

Match the customer to the product.

No time for paperwork? Send them to Axis Flipkart Credit Card or Zype.

Self-employed with messy finances? They might struggle with strict lenders but fit Aditya Birla Udyog Plus if their GST is clean.

Student? Make sure they know they have to sign, not their parents.

Follow up. If a lead stalls, it is usually a document error. A 2-minute call to check the signature or scan quality can save the sale.

Troubleshooting rejections

"Signature Mismatch"

Your signature changed? It happens. If it's drastic, you might need a signature affidavit or an update to your official records. VKYC can sometimes bypass this because the agent sees you sign in real-time.

"Document Not Legible"

Rescan at 300 DPI. Use natural light. Don't photograph a document on a patterned rug the camera gets confused.

"Attestation Date Too Old"

Some lenders want the attestation dated within 30 days of the application. Don't reuse old scans. Re-sign and re-scan.

"Not Self-Attested"

Did you sign too lightly? Is the signature floating in the margin? Sign darker and overlap the text.

What's next?

Blockchain verification is slowly appearing. A few fintechs are testing systems where a document, once verified, creates a permanent digital record. You wouldn't need to re-attest it for every new bank.

But for now, the pen is still your main tool. Until Aadhaar OTP and face auth completely take over, keep a blue or black pen handy.

Different customers, different headaches

Working Professionals: They have the docs but no time. Guide them to digital-first products (DBS, Kotak 811).

Students: They usually don't have income proof. Remind them that they have to sign their own papers, even if a parent is a guarantor.

Self-Employed: They have the most paperwork. GST, ITR, Udyam. Create a checklist for them. If their business docs are a mess, their application will be too.

Q&A

Can I just notarize it instead?

You can, but it is a waste of money and time. Self-attestation is accepted almost everywhere in 2026.

What if I submit a fake?

Don't. You will get blacklisted by the bank, reported to CIBIL, and potentially face legal trouble. The verification tech is too good now.

Do I need to attest for VKYC?

Usually no. Showing the original on camera counts.

Can I attest for my parents?

No. "Self" means the applicant. If your dad is applying, your dad signs.

Are self-attested docs okay for big loans (₹10L+)?

Yes, but they will scrutinize everything. Expect a multi-stage verification process, including VKYC and database checks.

What makes the below so obviously AI generated?

The structure is still very rigid (headers followed by predictable lists).

Phrases like "Let's break down what you need to know" or "Here is the reality of…" are filler transitions.

Some sections still read like a brochure (e.g., the "What's next?" blockchain paragraph).

The Q&A section is a bit too neat and comprehensive.

Final rewrite

When you apply for a credit card or loan in India, you will hit a wall of jargon. "Self-attested" is the classic offender. It sounds technical like you need a lawyer or a trip to a government office.

You don't. You just need a pen.

Self-attestation is simply certifying that a photocopy matches your original document. Instead of finding a notary or gazetted officer, you sign the copy yourself. You are telling the bank, "I promise this is real."

Banks require it for KYC compliance and fraud checks. It saves them the headache of verifying every copy with an external authority and saves you from running around for stamps.

How to do it (without getting rejected)

The concept is easy, but banks are picky about execution.

Physical copies:

Photocopy the original. Sign across the copy so your signature touches both the text and the white border. Add the date. Writing "True Copy" is optional but doesn't hurt. Just make sure the signature matches what you have on your PAN or Aadhaar.

Digital copies:

Scan the doc or snap a photo. Add your signature via a stylus or sign the physical paper before scanning. Most banking apps like Axis or Unity SFB now have an overlay feature that handles this when you upload.

Start Your Financial Product Journey Today

Common mistakes

Most rejections happen because of small, annoying errors.

Signature placement: Don't just sign the white margin. If the signature doesn't overlap the text, it looks like you could have just pasted a new photo in. The overlap proves the document hasn't been swapped.

Consistency: If your official signature is a scribble, don't write your full name neatly on the copy. It flags a mismatch. Match your existing signature, even if it's ugly.

Pen color: Blue or black. Red or green ink often gets flagged as informal or "altered."

The date: Always date it. Many banks reject undated docs, especially for salary slips or bank statements.

Bad scans: If the text is blurry, they won't accept it. Light it well and hold the camera steady.

What actually needs it?

If you are using GroMo or applying directly, these are the usual suspects:

Identity: PAN is mandatory for everything. Aadhaar, Passport, Voter ID, or Driving License usually follow.

Address: Aadhaar is king here. Otherwise, utility bills (under 3 months old), rent agreements, or passbooks.

Income (Salaried): 3 months of salary slips, Form 16, or 6 months of bank statements showing salary credits.

Income (Self-Employed): 2 years of ITR, GST cert, Udyam registration, and business proof.

Other: Cancelled cheques for disbursals, photos, or education certs for student cards.

Different products, different rules

A credit card application is lighter work than a business loan.

Credit Cards

Axis, IDFC, DBS they primarily need self-attested PAN and address proof. If you're an ETCC (Existing to Credit Card) customer, it’s even faster because the bank already knows you.

Personal Loans

Lenders like IDFC FIRST or Lendingplate dig deeper. They want bank statements uploaded via Account Aggregator or net banking.

One thing to note on IDFC FIRST loans: they run strict compliance. If you or an agent tamper with a statement, the loan is dead. The attestation must be genuine.

Business Loans

Products like Aditya Birla Udyog Plus require business proof. GST, Udyam registration, ownership documents. Loans over ₹10 lakhs usually need co-applicant paperwork, each self-attested by the respective person.

Savings & Demat Accounts

Digital accounts (DBS, Kotak 811) lean on Video KYC (VKYC). Showing the original card on camera often replaces the need for a physical signature.

Is it legally binding?

Yes. The government pushed for self-attestation to cut red tape. The DoPT permitted it for government applications, and RBI extended it to banking.

It carries weight. But that weight falls on you. If you attest a fake document, you are liable. Banks verify originals during VKYC or in-person checks, so don't try to bluff the systems are built to catch it.

The tech shift

In 2026, you see less ink and more pixels.

AI Checks: Lenders use AI to detect if a file was edited or if a signature doesn't match the database. It spots things a human clerk would miss.

DigiLocker: Apps like Lendingplate pull documents directly from DigiLocker. Since the government issues the file, it’s pre-verified. You skip the attestation.

Video KYC: For Unity SFB or DBS, the video call is the attestation. You show the card. You say "Yes." Done. Unity SFB even has a silent mode where you just hold up the documents without speaking.

Join 60L+ Partners Earning with GroMo

For GroMo Partners

If you are selling these products, documentation errors are your enemy. They kill conversions.

Pre-qualify. Ask the customer if they have the docs ready before you send the link. Do they have the original PAN? Is the address proof recent?

Match the customer to the product.

Busy professional? Send them to Axis Flipkart Card or Zype minimal paperwork.

Self-employed? Check their GST status before aiming for a business loan.

Student? Make sure they sign their own papers. Parents can't do it for them.

Follow up. If a lead stalls, it’s usually a doc issue. A quick call to check the scan quality can save the commission.

When things go wrong

"Signature Mismatch"

If your signature evolved over time, you might need to update your official records or use VKYC to prove it's you in real-time.

"Document Not Legible"

Rescan at 300 DPI. Use good light. No shadows.

"Attestation Date Too Old"

Some lenders want the attestation dated within 30 days. Don't reuse old files. Re-sign and re-scan.

"Not Self-Attested"

Did you sign too lightly? Did you miss the border? Go darker and overlap the text.

What's next?

Blockchain verification is creeping in. Some fintechs are testing systems where a document, once verified, creates a permanent record. You wouldn't need to re-attest it for every new bank.

But for now, the pen is still the standard. Until Aadhaar OTP and face auth completely take over, keep a blue or black pen handy.

Different customers, different headaches

Working Professionals: They have the docs but zero time. Push them toward digital-first products like DBS or Kotak 811.

Students: They often lack income proof. Remind them that they must sign, even if a parent is a guarantor.

Self-Employed: They have the most paperwork. GST, ITR, Udyam. If their business docs are messy, their application will be too.

Q&A

Can I just notarize it?

You can, but it’s a waste of money. Self-attestation is accepted everywhere now.

What if I submit a fake?

Don't. You'll get blacklisted by the bank and potentially face legal trouble. The verification tech is too good to bluff.

Do I need to attest for VKYC?

Usually no. Showing the original on camera counts.

Can I attest for my parents?

No. "Self" means the applicant. If your dad is applying, he signs.

Are self-attested docs okay for big loans (₹10L+)?

Yes, but they will look closer. Expect strict checks and a VKYC session.