How to Improve Your Credit Score in India (2026 Guide)

Discover 12 proven strategies to boost your credit score in India. Learn expert tips, timelines, and avoid common mistakes. Complete 2026 guide.

Your credit score in India affects loan rates, credit card approvals, rental applications, and sometimes even job prospects. If you're trying to improve yours in 2026, good that's actually worth doing.

Here's what works.

The Basics

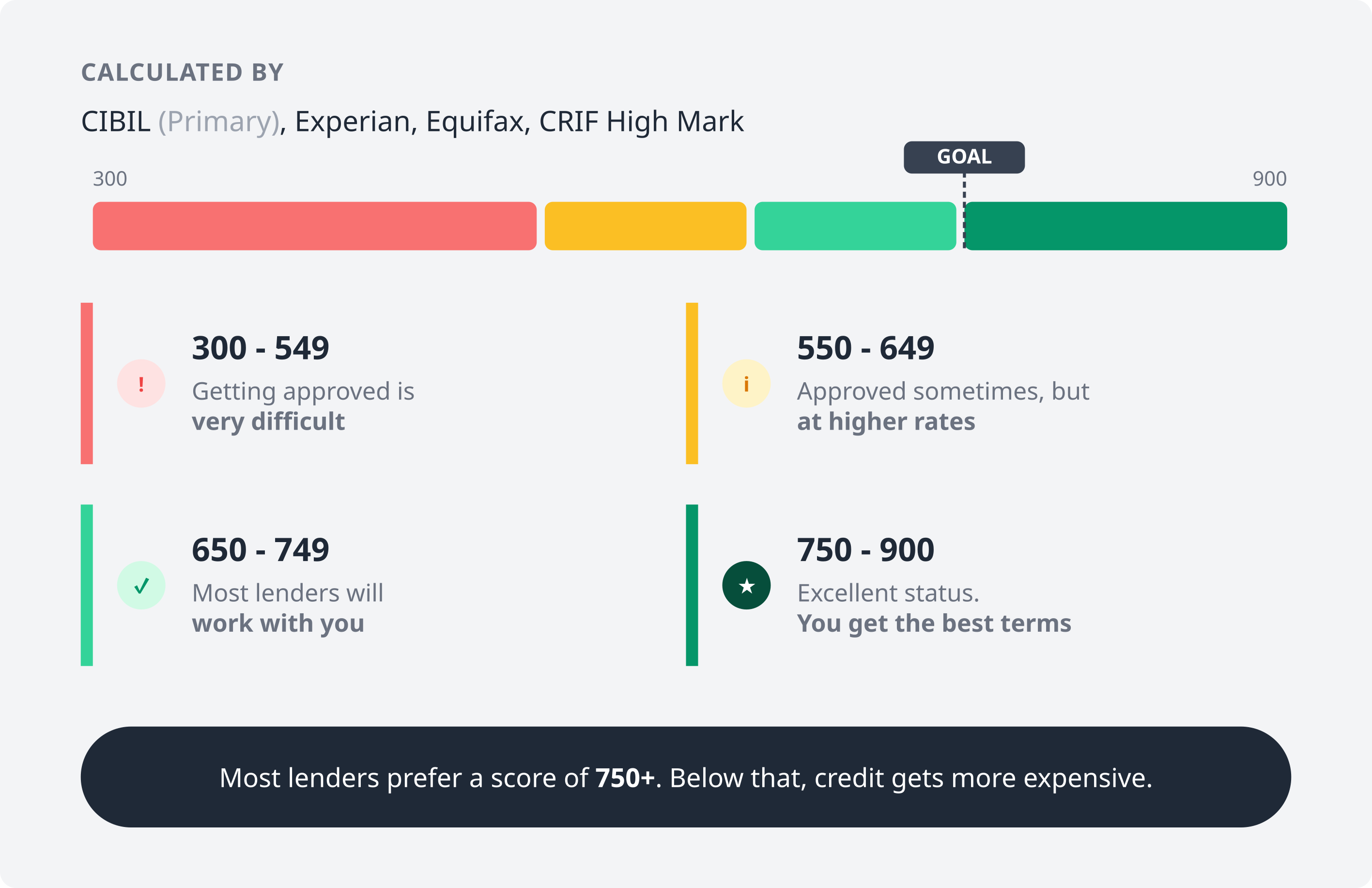

Credit scores in India run from 300 to 900. Four bureaus calculate them: CIBIL (the one most lenders check), Experian, Equifax, and CRIF High Mark.

The rough breakdown:

| Score Range | What it Means |

| 300-549 | Getting approved is very difficult |

| 550-649 | You'll get credit sometimes, but at higher rates |

| 650-749 | Most lenders will work with you |

| 750-900 | You get the best terms |

Most lenders want 750+. Below that, credit gets more expensive.

What Moves Your Score

Payment history (~35%) – Do you pay on time? This is the biggest factor.

Credit utilization (~30%) – How much of your available credit are you using? Under 30% is the goal.

Account age (~15%) – Older accounts help.

Credit mix (~10%) – A combination of secured loans (home, car) and unsecured (cards, personal loans) looks good.

Recent applications (~10%) – Lots of applications in a short window looks risky.

What Actually Works

Pay on time. Every time.

One missed payment can drop your score 50-100 points and stay on your report for years. Set up autopay for at least the minimum on everything. Add calendar reminders a few days before due dates. If you've missed payments, the only fix is to get current and stay current.

Juggling multiple due dates? Call your lenders. Many will let you shift your payment date.

Keep utilization under 30%

If your limit is ₹1 lakh, don't carry more than ₹30,000. High utilization looks like you're stretched thin.

Ways to manage this: pay your card multiple times a month (don't wait for the statement), request a limit increase and then don't use it, spread charges across multiple cards, use UPI or debit for daily stuff.

Don't close old cards

Account age matters. That card from years ago? Keep it open. Put something small on it a subscription maybe and set up autopay. If there's an annual fee, ask the bank to waive it or switch to a no-fee version.

Check for errors

Reports in India have mistakes more often than you'd expect. Wrong payment statuses, accounts that aren't yours, incorrect limits.

Get your free report from CIBIL, Experian, or Equifax once a year. Look through everything. Dispute anything wrong through the bureau's site. Follow up. Corrections usually take about 30 days.

Become an authorized user

A family member with excellent credit and a long-standing card can add you as an authorized user. Their history on that card gets credited to you. You don't need to use the card just confirm the issuer reports authorized users to bureaus.

Space out applications

Each loan or card application creates a "hard inquiry." Several in a short period makes you look desperate.

Apply only when you're fairly confident. Space things out by 3-6 months. Use pre-qualification tools when available they do "soft inquiries" that don't affect your score.

Exception: if you're rate-shopping for a home or car loan, multiple inquiries within 14-30 days usually count as one.

Diversify but don't force it

A mix of credit types helps, but don't take on debt just for this.

Only credit cards? A small personal loan or secured card could add variety. Only loans? Using a credit card responsibly helps. Credit builder loans and secured cards exist specifically for people building or rebuilding credit.

Handle collections and settlements

Accounts in collections or marked "settled" hurt your score badly.

Contact the lender. Negotiate if needed. Get any agreement in writing before paying. Confirm the lender updates the bureaus afterward. Some will agree to remove the negative entry after payment worth asking.

If you're using credit for business

Earning through platforms like GroMo? You might use cards for business expenses. Works fine if you're disciplined.

Charge only what you can pay off monthly. Track business expenses separately. Business credit cards sometimes don't report to personal files. Pay yourself from earnings rather than mixing everything together.

See how others are earning ₹50K+ monthly with zero investment if you want to build extra income.

Automate everything

Missed payments in 2026 are usually a systems problem, not a money problem.

Bank autopay for EMIs. Credit card autopay for at least the minimum. UPI autopay for subscriptions. Banking app notifications. Calendar reminders as backup. Redundancy helps one fails, the other catches it.

Increase your income

Income isn't directly in your score calculation. But more money makes everything easier paying debt, absorbing emergencies, avoiding late payments.

Freelance work, side business, monetizing a skill, negotiating a raise. Plenty of people are earning ₹1 lakh per month alongside full-time jobs. That changes how you manage credit.

Consider a credit builder product

Starting from scratch or recovering? These products exist for this situation:

Secured Credit Card – You deposit ₹10,000-50,000 as collateral. The bank issues a card with that limit. Use it responsibly, build history.

Credit Builder Loan – You make monthly payments into an account. At the end, you get the money. Forced savings that reports to bureaus.

Timeline

| Start | Target | Time | What helps |

| 550 | 650 | 6-12 months | On-time payments, lower utilizatio |

| 650 | 750 | 12-18 months | All that plus disputing errors |

| 750_ | 800_ | 18-24+ months | Consistent habits, aging accounts |

Negative marks last. Late payments: 3 years. Defaults and settlements: up to 7 years.

Mistakes That Set You Back

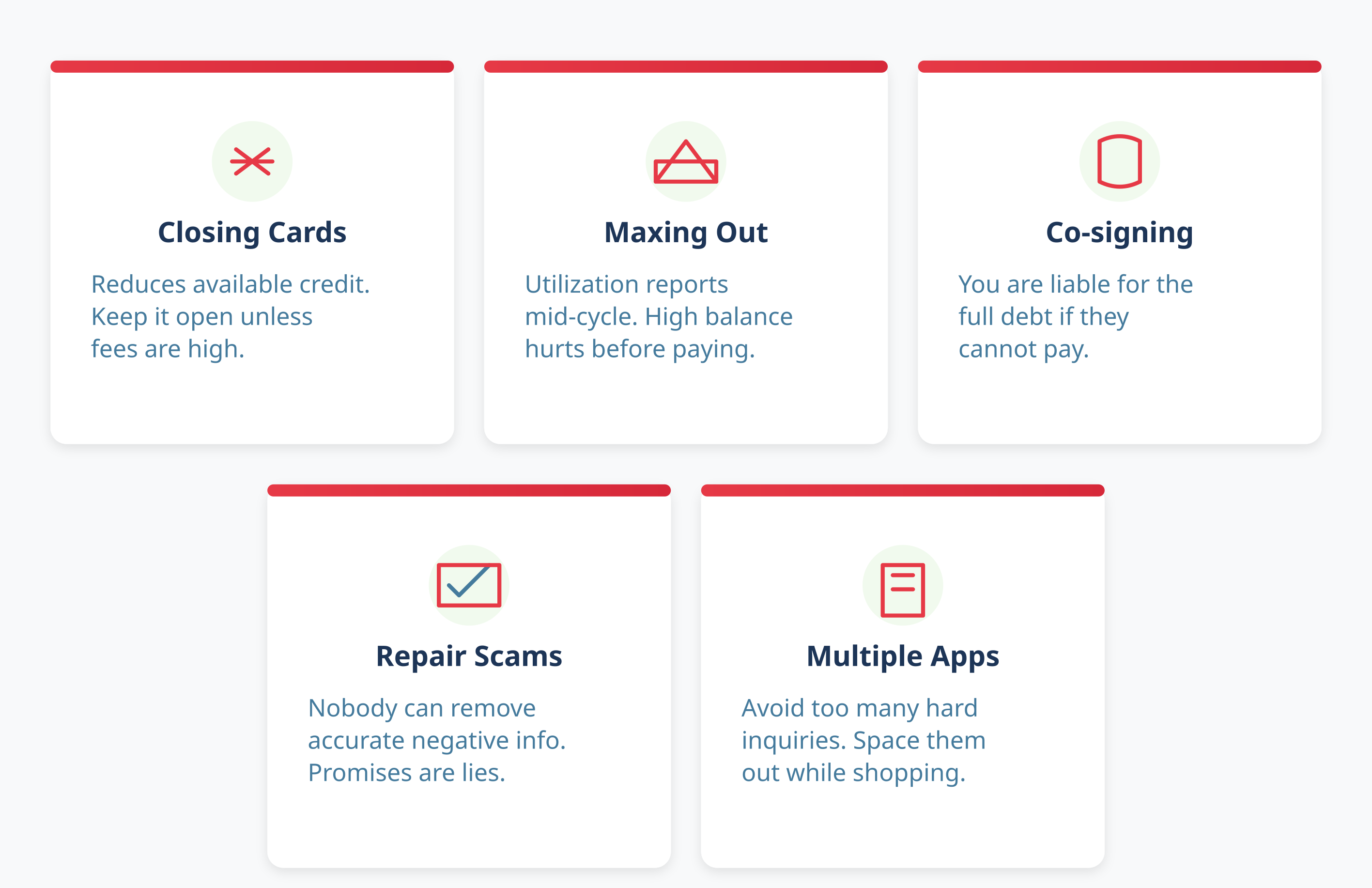

Closing cards after paying them off – Reduces available credit, increases utilization. Keep it open unless the fees are high.

Maxing out cards even temporarily – Utilization often gets reported mid-cycle. Paying in full doesn't help if the high balance gets reported first.

Co-signing without thinking – You're responsible for the full debt if the primary borrower can't pay.

Credit repair scams – Nobody can remove accurate negative information. Anyone promising that is lying.

Multiple applications while shopping around – Space them out unless you're getting a mortgage or car loan.

Ignoring your report – Check twice a year at minimum.

Credit counseling without research – Some help; some make things worse.

Special Situations

New to credit ("thin file")

No history means no score. Start with a secured card from your bank. Become an authorized user on family's account. Consider a small loan with a co-signer. Check if rent and utility payments can be reported.

Recovering from defaults/settlements

Clear everything outstanding. Get written confirmation. Start fresh with a secured card. Make every payment on time for at least a year. Add new credit gradually after 18+ months of clean history.

Too many loans/cards

Even with perfect payments, overextension hurts. Balance transfer to one low-interest card. Debt consolidation loan. Close newer accounts, keep the old ones. Attack highest-interest debt first.

Monitoring

Free reports (2026)

-

CIBIL: www.cibil.com (once yearly)

-

Experian: www.experian.in

-

Equifax: www.equifax.co.in

-

CRIF High Mark: www.crifhighmark.com

Apps

Paytm, PhonePe, Google Pay offer free checks. OneScore and CreditMantri go deeper. Most bank apps include it now.

Checking your own score is a soft inquiry zero impact. Check as often as you want.

Income Makes It Easier

Multiple income streams change the math. Extra money means faster debt payoff, emergency buffers, fewer maxed-out cards during unexpected expenses.

That's why people pursue side income flexible work bringing in ₹20,000-50,000 monthly. It helps.

See zero-investment business opportunities.

90-Day Plan

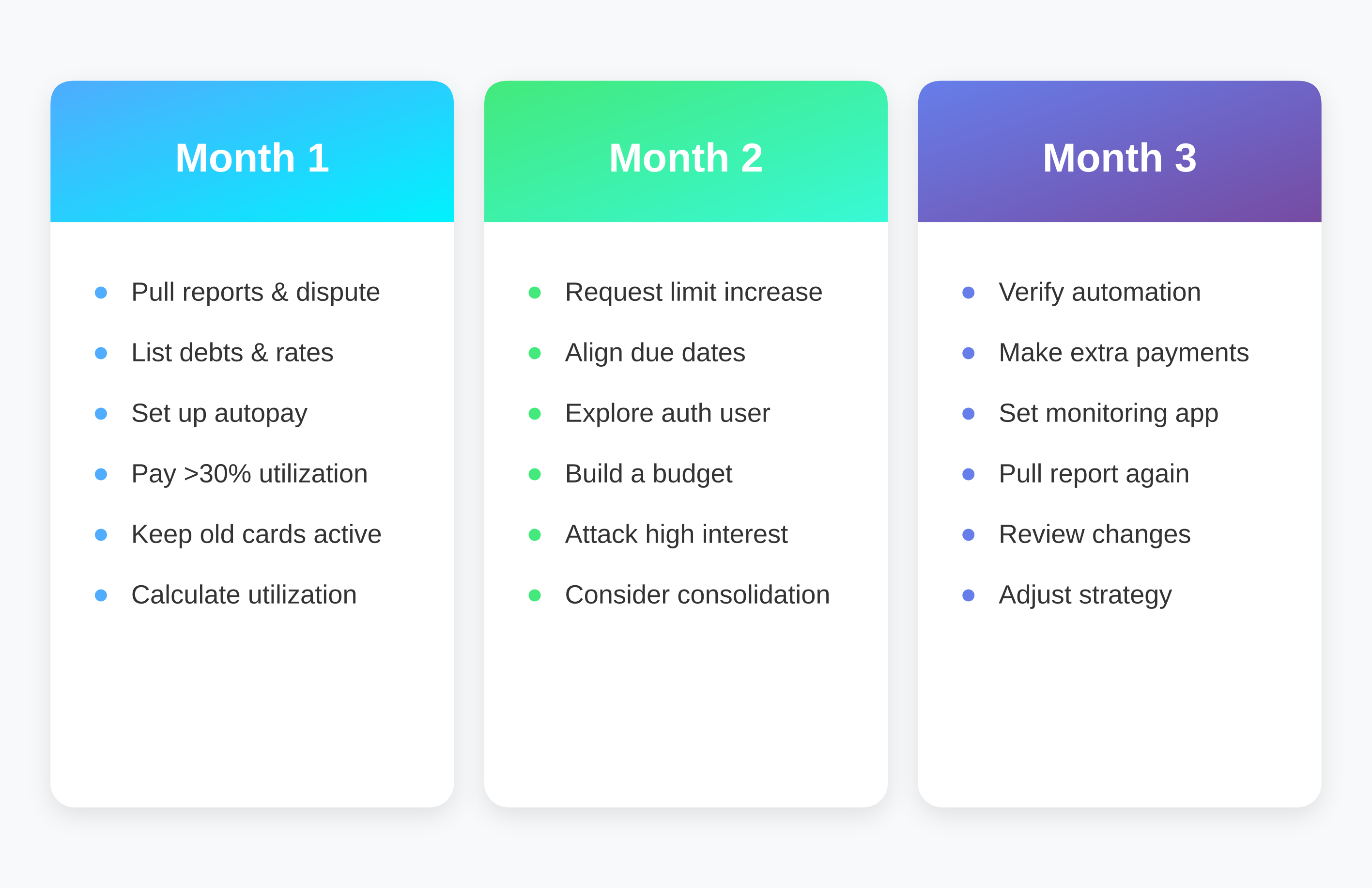

Month 1

Pull reports from all bureaus. Check for errors, dispute if needed. List all debts with balances, rates, due dates. Set up autopay. Calculate utilization. Pay down anything above 30%. Keep old cards active with small purchases.

Month 2

Request limit increases on cards with good history. Ask lenders about aligning due dates. Look into authorized user options. Build a budget. Attack highest-interest debt. Consider consolidation if helpful.

Month 3

Check that automation works. Make extra payments if possible. Set up a monitoring app. Pull your report again. Adjust based on what's changed. Plan the next 90 days.

Examples

Priya, 28, Mumbai – Started at 620. Autopay, paid down two cards from 80% to 20% utilization, disputed an error. Eight months later: 745. Got a premium card with ₹50,000 welcome bonus.

Rajesh, 35, Bangalore – Started at 580 with a settlement from 2023. Secured card with ₹25,000 deposit, 14 months of perfect payments, picked up side income. Result: 710. Approved for car loan at reasonable rate.

Anjali, 24, Delhi – No score (thin file). Authorized user on parent's card, got secured card, took small loan for laptop. Year later: 735. Foundation built for future home loan.

Quick Answers

Can I improve in 30 days?

Maybe 5-20 points if you pay down high balances or dispute an error. Real improvement takes months.

Does checking my score hurt it?

No. That's a soft inquiry. Only applications for new credit create hard inquiries.

Pay for monitoring?

Probably not. Free options are good enough now. Use the money for debt instead.

Closing a card helps?

Rarely. It reduces available credit and can shorten history.

Higher income helps directly?

No income isn't in the formula. But it makes good habits easier to maintain.

Start Somewhere

This isn't complicated, but it takes patience. Every on-time payment helps. Every point of utilization reduced helps. Every error corrected helps.

Pick one thing today. Check your report. Set up autopay. Commit to paying down one card. Then keep going.

If you want to strengthen your overall position, building extra income makes everything easier. See how people are doing it with zero investment.