Zero-Invest Business for Housewives | Earn ₹50K/Month with GroMo

Zero-investment business ideas for housewives aren't really "business ideas" in the traditional sense. You don't need a shop, inventory, or capital. You can earn ₹15,000–₹50,000 monthly by selling financial products through GroMo using just your phone. You share a link, someone opens an account, you get a commission.

India has 153 million housewives. Most manage the household spending but don't have a formal income. Digital platforms are changing that, offering a way to earn from home without neglecting family duties. This guide covers which products sell best, how to find customers, and what you can realistically expect to earn.

Why Housewives Do Well at This

Housewives have three advantages here: people trust them, they have time for follow-ups, and they want to improve their family's finances. Traditional businesses need rent, stock, and fixed hours. This model cuts all that out.

GroMo pays you for recommendations you might already make. You know families through school groups, housing societies, and relatives. You aren't cold-calling strangers. You're telling people about useful products credit cards with cashback, savings accounts with better rates, loans to people who already trust you. GroMo handles the customer service and compliance; you just handle the referral.

According to GroMo, housewives actually stick with it longer and get more repeat business than other groups. Trust matters in this business.

Five High-Commission Products to Start With

Tide Business Account (₹800–₹1,200 Per Account)

Tide offers business accounts for self-employed people you know tuition teachers, boutique owners, caterers. They can open an account in three minutes on the app, do a video KYC with their PAN, and add ₹50. You get paid when they pay a utility bill and activate their expense card.

Look for small business owners in your building. The pitch is simple: "Want to keep business expenses separate from household? Free account with a cashback card."

Upstox Demat Account (₹250–₹400 Per Account)

This is for people who want to start investing maybe young parents saving for education, or salaried husbands looking at mutual funds. Upstox charges nothing to open an account or invest in mutual funds. Customers use Aadhaar and PAN to sign up, then make one trade.

You probably know people who are curious about investing but find it confusing. Tell them: "Investing in mutual funds and IPOs is free no commission, no paperwork."

IDFC FIRST Savings Account (₹350–₹550 Per Account)

This is a zero-balance account. It's a good option for domestic helpers, part-time workers, or relatives in smaller towns who struggle with minimum balance rules. They get a virtual debit card instantly and UPI access. They just need to verify their mobile number and do a video KYC.

You likely know 10–20 people who don't have a proper bank account or hate the fees they pay. Tell them: "Zero balance, instant debit card. No fees."

Kotak 811 Digital Account (₹300–₹500 Per Account)

Kotak 811 is a full bank account on a phone. It suits tech-savvy contacts neighborhood college kids, young professionals. They get a virtual debit card immediately and can set up FDs. They sign up with an Aadhaar-linked mobile number and PAN, do a video KYC, and add ₹1.

Your advantage here is helping them through the process. Some people get stuck on video KYC. If you help them, they are more likely to finish.

Personal Loans (3.5%–5.5% of Loan Amount)

This pays the most per sale. If someone needs ₹20,000–₹30,000 fast, platforms like My Money Bazaar can help. They upload a bank statement, verify ID, and get money the same day. You earn ₹700–₹1,650 for a ₹30,000 loan.

Target salaried families you know who have sudden expenses weddings, medical bills, school fees. Be careful: if they default on the first three EMIs, you lose the commission. Make sure they can actually afford the loan before you refer them.

For more on financial sectors, see India's top business opportunities in 2026.

Building Your Customer Pipeline in Four Weeks

Week 1: Map Your Network

Write down everyone you know who spends money: school parent groups, kitty party circles, apartment WhatsApp groups, relatives, tutors, shopkeepers, salon staff, domestic help. Categorize them by what they might need business owners for Tide, salaried people for demat accounts, people needing cash for loans.

You probably know more people than you think. Count them: immediate family (12), extended family (25), housing society (30), school connections (20), service providers (15). That's over 100 people. Pick 50 who trust you and might actually need these products.

Week 2: Do the Training

GroMo has free courses on product features, rules, and how to handle objections. Spend two hours a day on the videos. You'll learn what documents customers need and how KYC works.

The training also gives you ready-made content WhatsApp messages and scripts so you don't have to write everything from scratch.

Week 3: Start with People You Know

Start with five people who trust you a sister who needs a business account, a brother-in-law looking at investments, a friend's husband who needs a loan. Don't mass-message everyone. Personalize it. Help them sign up if they get stuck.

Your first ₹800 commission proves it works. The second builds momentum. These first customers also give you stories to tell others.

Week 4: Share Content

GroMo has content you can share on WhatsApp. Post a daily status about one product benefit: "Did you know you can get 1.5% cashback on business expenses with a free Tide card?" Share success stories (with permission).

Don't spam. Personal messages work better: "Hey Anjali, you mentioned needing a demat account? I found a zero-fee option."

See how Mumbai housewives do this: zero-investment business models proven in Mumbai.

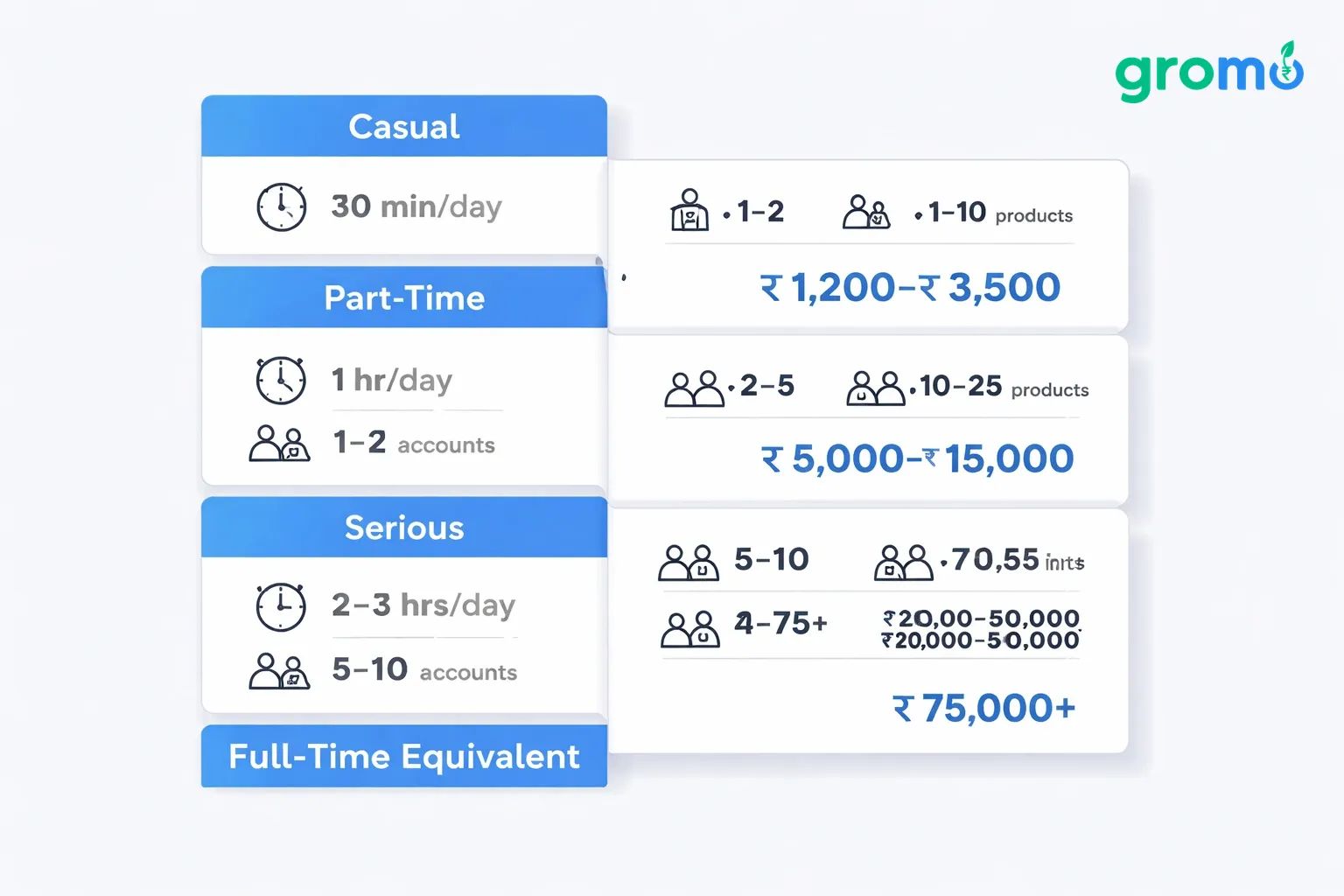

Realistic Monthly Earnings

| Activity Level | Daily Effort | Products Sold/Month | Monthly Income Range |

|---|---|---|---|

| Casual | 30–45 minutes | 2–4 accounts, 0–1 loan | ₹1,200–₹3,500 |

| Part-Time | 1.5–2 hours | 8–12 accounts, 1–2 loans | ₹6,000–₹15,000 |

| Serious | 3–4 hours | 20–30 accounts, 3–5 loans | ₹18,000–₹40,000 |

| Full-Time Equivalent | 5–6 hours | 40–60 accounts, 6–10 loans | ₹35,000–₹70,000 |

Casual: If you just want pocket money, spend 30 minutes a day. Message five people, follow up on two applications. Selling two Upstox accounts and one Kotak account gets you about ₹1,400 a month. No pressure.

Part-Time: If you spend 90 minutes a day 10 messages, three calls, daily updates you might earn ₹6,000–₹15,000. That covers tuition or household help.

Serious: If you treat this like a job (3–4 hours), you can earn ₹18,000–₹40,000. You attend webinars, join partner groups, and work through your network systematically.

Full-Time: Some earn ₹50,000+ by building a team. You refer other partners and earn a cut of their sales. See how: Bangalore's zero-investment income strategies.

Handling Common Problems

Problem 1: Family Doesn't Want You to Work

Some families resist the idea of a housewife "working." Don't call it a job. Call it learning about finance. "I'm taking a free course on financial products."

Once you bring in ₹5,000, the objections usually fade. If you deposit your earnings into the family budget, it speaks for itself.

Problem 2: Not Confident with Apps

If you use WhatsApp and banking apps, you can do this. GroMo works the same way tap buttons, read instructions, share links.

Watch the training videos. Open an account yourself first. If you get stuck, GroMo has chat support. You can also join WhatsApp groups with other women doing this.

Problem 3: Afraid of Looking "Salesy"

You don't have to be pushy. You are informing friends about products they might need. If a neighbor is paying ₹500 a month in bank fees, telling them about a zero-balance account is helpful, not salesy.

Try saying: "I found a business account with cashback thought of your shop. Want details?" instead of "You should open this."

See how West Bengal partners do this: West Bengal's zero-investment business models.

Taxes and Rules

GroMo commissions are business income. You need a PAN. If you earn over ₹2.5 lakh a year, you need to file taxes. Open a separate bank account for your GroMo income to keep it simple.

File ITR-4 if you earn under ₹50 lakh a year. It's a simplified form. A CA might charge ₹500–₹1,500, or you can use ClearTax.

Don't promise things you can't guarantee. Don't say "You'll definitely get the loan." Say "This account has no minimum balance." Keep customer details private.

More on rules here: financial product distribution compliance in India.

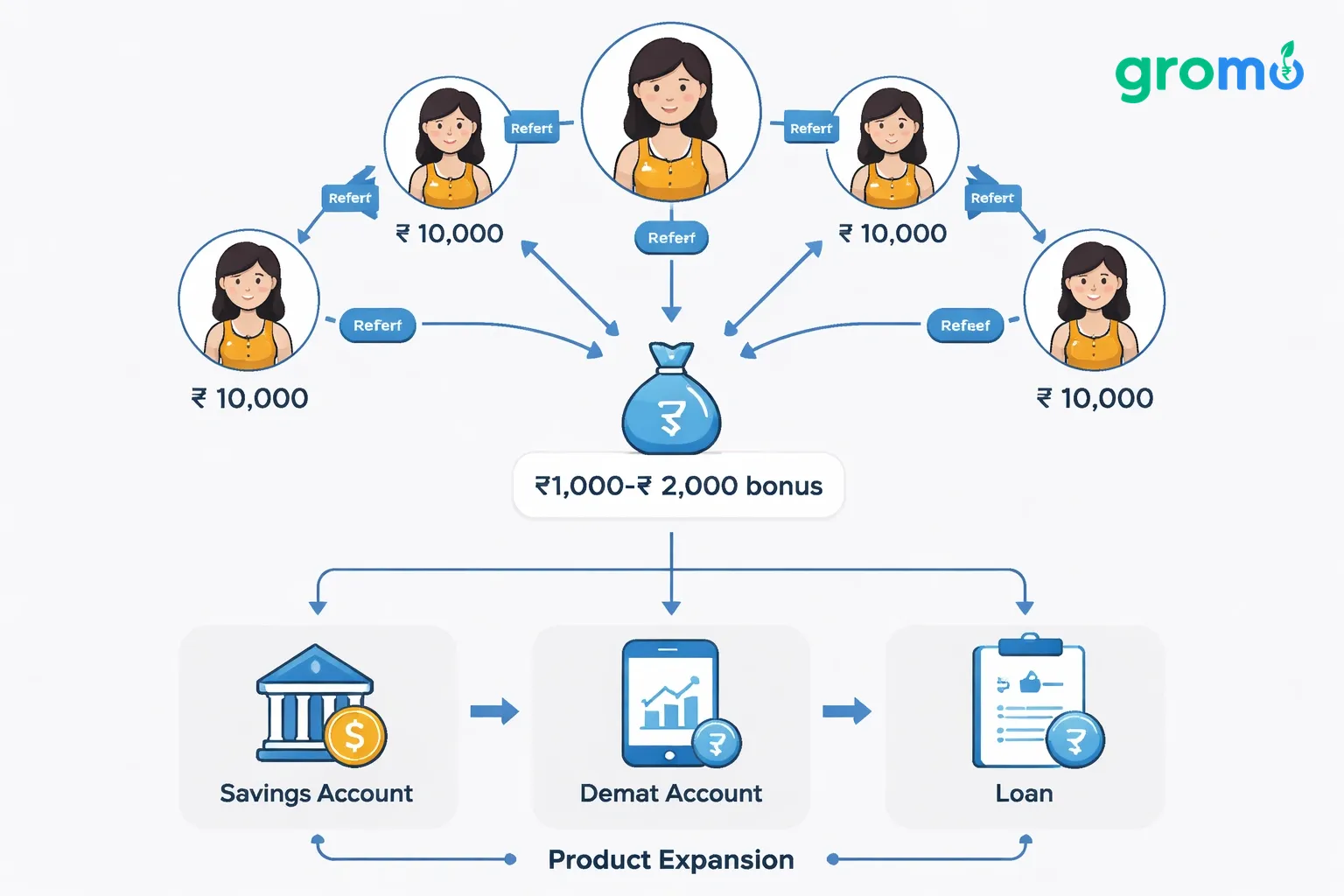

Scaling Up: Team Building

You can earn more by recruiting other partners. If you refer five housewives who each earn ₹10,000, you get an extra ₹1,000–₹2,000 on top of your own sales.

Recruit from your customers. After helping someone, say: "You could earn by referring others too. I can show you how."

Expand your products as you get comfortable. Start with savings accounts, add demat, then loans. Different products suit different people. See Pune strategies: Pune's financial product distribution strategies.

A Daily Routine That Works

Morning (30 mins): Check the app for updates. Send follow-up messages to three people. Post one status.

Afternoon (45 mins): Message five new people with specific product ideas. Look at GroMo's content library for new pitches.

Evening (30 mins): Watch a weekly webinar. Check your earnings. Plan tomorrow's contacts.

Consistency matters more than intensity. Thirty minutes every day for 90 days works better than a four-hour burst once a month. Fit it into your existing routine message people while waiting for the kids' bus, post a status while cooking.

See Tamil Nadu examples: Tamil Nadu's home business strategies.

Real Examples

Meera, Hyderabad: She earns about ₹32,000 a month focusing on personal loans for her family and neighbors. She checks bank statements before referring to make sure people can repay. Her honest approach "I'll only refer you if the EMI is comfortable" gets her more referrals.

Priya, Delhi: She earns ₹18,000 a month selling demat and savings accounts. She hosts weekend financial literacy sessions in her housing society's clubhouse. Twenty families opened accounts after her "Investment Basics" talk.

Anjali, Punjab: She went from ₹5,000 to ₹45,000 a month by building a team of five housewives. Each person focuses on one product. She runs Zoom trainings for them.

More stories: Punjab's zero-investment business achievements and Hyderabad's financial distribution results.

How GroMo Compares to Other Options

| Option | Investment Required | Monthly Potential | Time Flexibility | Scalability |

|---|---|---|---|---|

| GroMo Distribution | ₹0 | ₹15,000–₹50,000 | Complete | High (team-building) |

| Tiffin Service | ₹5,000–₹15,000 | ₹10,000–₹25,000 | Fixed cooking hours | Limited (capacity-bound) |

| Tuition Classes | ₹2,000–₹8,000 | ₹8,000–₹30,000 | Fixed class schedule | Moderate (room size) |

| Reselling (Meesho, etc.) | ₹0–₹3,000 | ₹5,000–₹20,000 | Moderate | Moderate (inventory) |

| Tailoring/Alterations | ₹8,000–₹20,000 | ₹6,000–₹18,000 | Order-dependent | Low (time-for-money) |

GroMo removes the money barrier. Tiffin services need gas and containers. Tailoring needs a machine. Here, you invest nothing.

Scalability is the other difference. A tiffin service maxes out at 30–40 customers because you can only cook so much. With GroMo, you can build a team. Five partners can reach 500 people you don't know.

See more: India's complete zero-investment business landscape.

Frequently Asked Questions

Q: How long before I earn my first commission? A: Usually 7–14 days. Opening a Kotak 811 account for a family member takes 10 minutes. Commission comes 48 hours after they fund it.

Q: What if my customer fails KYC? A: You don't get paid, but you lost nothing because you didn't pay anything. Help them fix the errors and try again, or suggest a different product.

Q: Can I do this anonymously? A: Yes. Just message people directly. You don't have to post on social media or your WhatsApp status. Your network already knows you.

Q: Do I need a business registration or GST? A: No. You operate as an individual. You just need a PAN. GST is only if you earn over ₹20 lakh a year.

Q: What if someone doesn't respond? A: Follow up once after 48 hours. If they don't reply in 3 days, move on. Focus on the people who are interested.

Q: Can I quit? A: Yes. There is no contract. Just stop sharing links. Pending commissions still get paid.