How to Earn ₹1 Lakh Daily with GroMo: Proven Strategies

Earning ₹1 lakh a day sounds like an Instagram ad scam. I get it. But on GroMo, the math actually works if you're moving high-volume products credit cards, loans, demat accounts or building a team that does it for you. Payouts range from ₹500 to ₹3,500 per referral. Scale that up, and ₹10,000 daily turns into ₹1 lakh in about 6 to 12 months.

It's not magic. It's just volume. Over 60 lakh partners on GroMo have collectively earned ₹100 crore. The ones making the big money aren't smarter than you; they just figured out three things: which products pay the best, how to build a team, and where to find customers who actually sign.

How the math works

₹1 lakh a day is ₹3.6 crore a year. You can't hit that with a "side hustle" mindset. You have to treat it like a business.

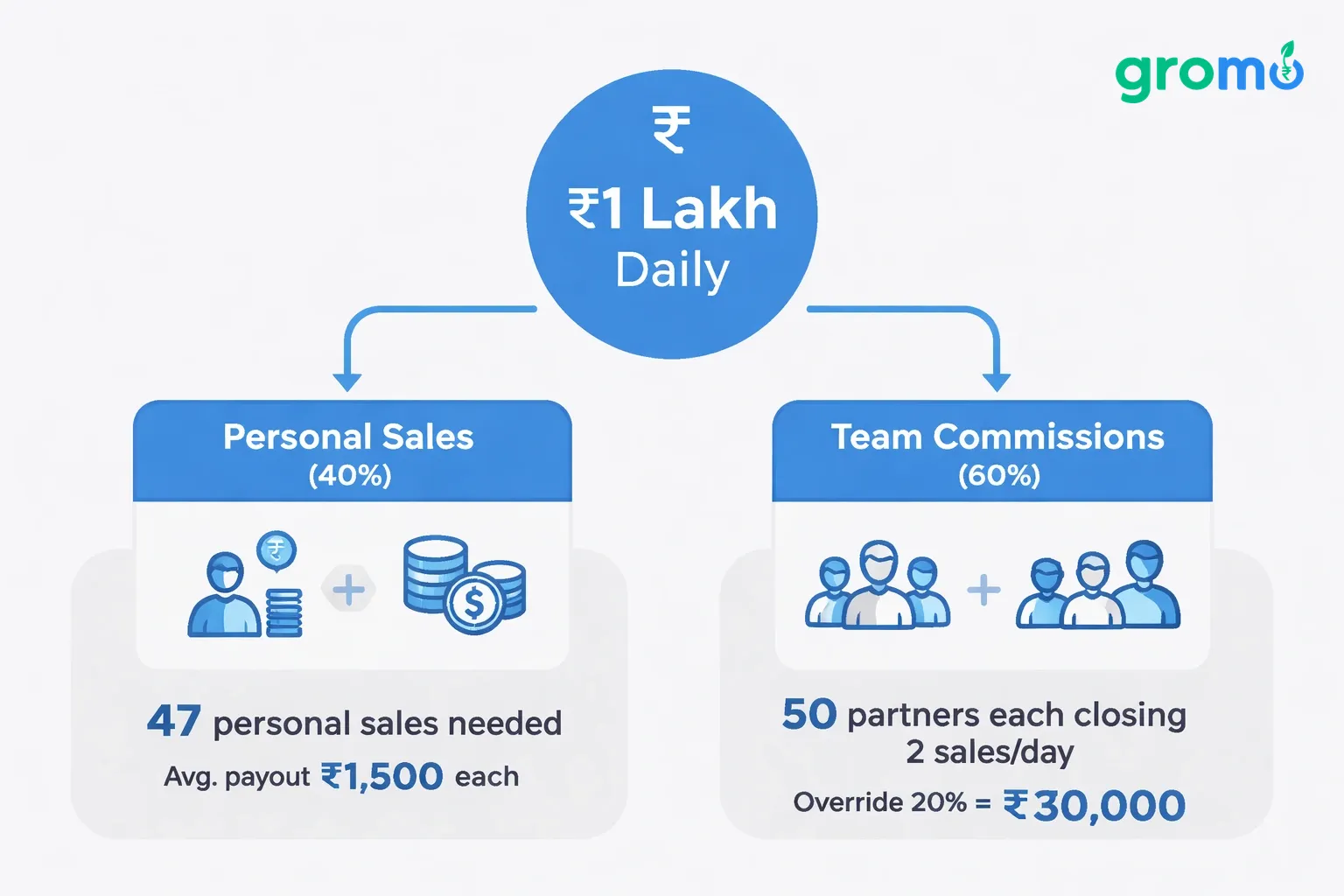

Here's the breakdown. GroMo pays anywhere from ₹180 for a demat account to ₹3,500 for a premium credit card. Let's say your average payout is ₹1,500. You need about 67 conversions a day. That sounds impossible alone. But if you have a team of 50 partners each closing 2 sales a day, and you take a 20% override, that's ₹30,000 from them. You just need 47 personal sales to hit ₹1 lakh.

Most top earners use a hybrid model: roughly 40% personal sales, 60% team commissions. This is how you build that system.

The products that pay

Credit cards are the bread and butter. Premium cards like HDFC Regalia, Axis Magnus, and ICICI Sapphiro pay ₹2,000 to ₹3,500 per approval. Your target is salaried professionals making ₹50,000+. In metros, these people are everywhere. Look for folks who already have a card and want an upgrade.

Personal loans are next. Moneyview, Hero Instant, and Poonawalla Fincorp pay 1.75% to 3.5% of the loan amount. On a ₹5 lakh loan, a 2.5% commission is ₹12,500. You only need 8 of those a day to hit ₹1 lakh no team required.

Business loans are the heavy hitters. ClickPe and Poonawalla Fincorp offer working capital up to ₹50 lakh for MSMEs. A ₹20 lakh loan at 2% pays ₹40,000. Target kirana stores, small manufacturers, anyone who needs cash flow.

| Product Type | Average Payout | Target Customer | Sales Cycle |

|---|---|---|---|

| Premium Credit Cards | ₹2,000–₹3,500 | Salaried ₹50K+ | 3–7 days |

| Personal Loans (₹5L) | ₹8,000–₹15,000 | Salaried ₹30K+ | 5–10 days |

| Business Loans (₹20L) | ₹30,000–₹60,000 | MSME owners | 10–20 days |

| Demat Accounts | ₹250–₹400 | First-time investors | 2–5 days |

Demat accounts (Upstox, Indiabulls) pay less ₹250 to ₹400 but they convert fast. Use them as a door opener. Once someone opens an account, they're 3x more likely to apply for a credit card later if you stay in touch.

Diversify. If credit card approvals dip during tax season, business loans often spike because shops need inventory. Understanding these cycles keeps you steady.

For more on earning ₹1 lakh monthly, check the playbooks from partners. Their zero-investment business models show the same logic applied to daily targets.

Building your team

You can't do this alone forever. You'll hit a wall at 20–30 sales a day. A team breaks that ceiling. GroMo lets you recruit partners and earn override commissions usually 15% to 25% on everything they sell. If your team does 100 sales a day at ₹1,500, you make ₹22,500 to ₹37,500 just from overrides.

Start close. Family, friends, colleagues. Train them with GroMo's free courses. Frame it as a zero-investment side income that just needs a phone. College students, housewives (proven earners), and retirees are solid bets.

Structure them. Junior Partners (0–10 sales), Senior Partners (11–30), Team Leaders (31+). Add your own incentives bonuses, trips, whatever drives them.

Daily huddles matter. A quick 15-minute call at 9 AM and 6 PM keeps everyone aligned. Use WhatsApp for real-time backup. If a partner is stuck on a question, the group jumps in.

Track the data. Use a sheet or CRM. Watch conversions, rejections, and payouts. If one partner kills it with credit cards but struggles with loans, pair them with someone who has the opposite profile.

For city-specific tactics, see the guides on Punjab and Mumbai.

Finding customers

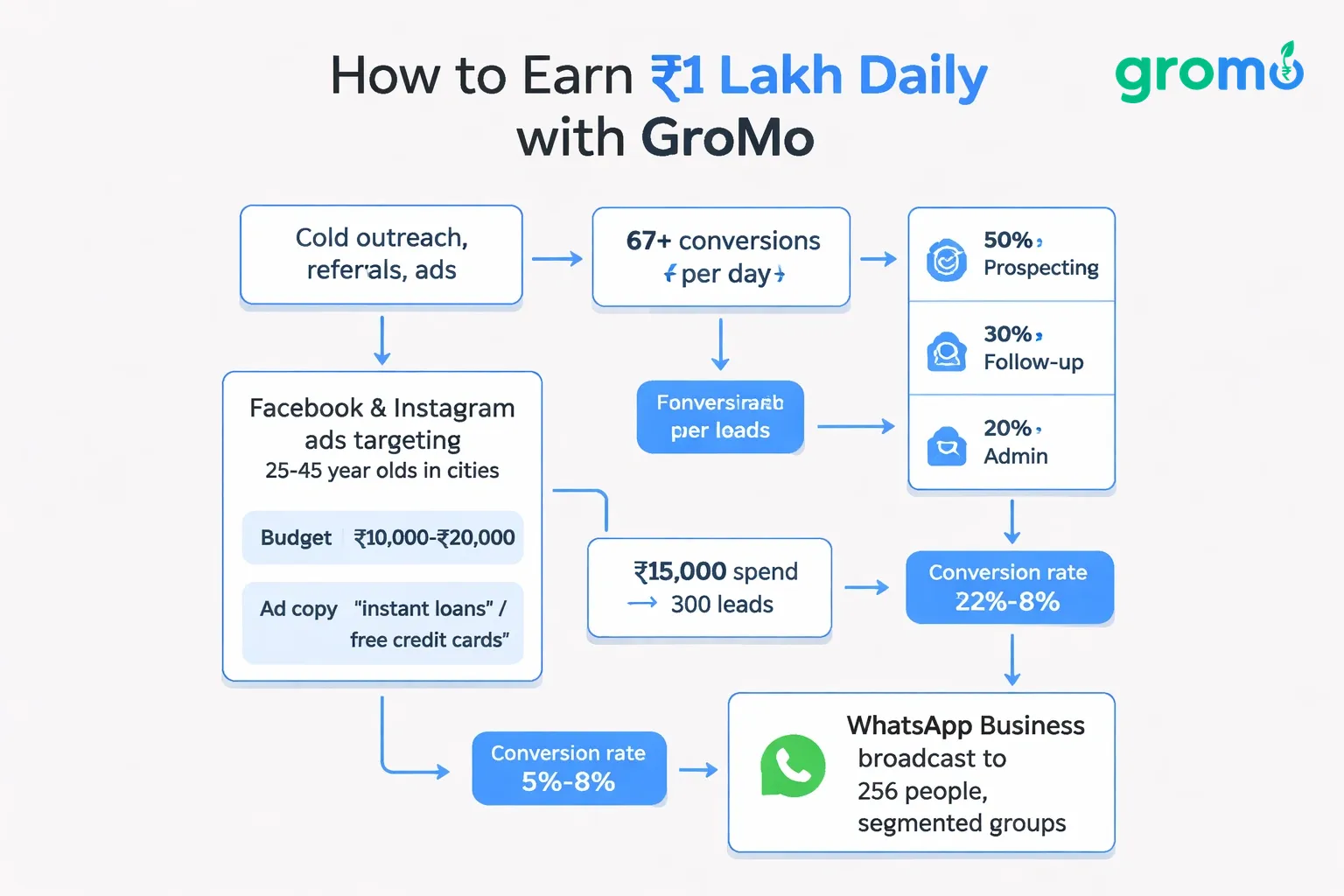

You need 67+ conversions a day. That doesn't happen by accident. You need a pipeline of cold outreach, referrals, and ads.

Split your time: 50% prospecting, 30% following up, 20% admin.

Facebook and Instagram ads work well for financial products. Target 25–45 year-olds in cities. Spend ₹10,000–₹20,000 a month on "instant loans" or "free credit cards." Send them to your GroMo link. A ₹15,000 spend can get you 300 leads. At a 5%–8% conversion rate, that's 15–24 deals and ₹22,500–₹36,000 in revenue.

WhatsApp Business is essential. You can broadcast to 256 people at once. Segment them: Group A for cards, Group B for loans. Send targeted offers. "HDFC Regalia approved in 48 hours." Use their name. Make it personal.

Offline still matters. Go to meetups, trade fairs. Hand out cards. Offer a free credit report analysis. That value-first approach builds trust.

Partner with professionals. CA firms and real estate brokers meet people who need loans. Offer them 10%–15% of your commission. One CA firm can send you 10–20 leads a month. That's ₹30,000–₹60,000 per deal.

Use GroMo's tools: your own website, brochures, templates. Share wins like "Got Mr. Sharma a ₹10 lakh loan in 2 days." Post on LinkedIn about financial literacy. Followers turn into customers.

Check out Bangalore ideas, Gujarat models, and Hyderabad tactics for region-specific advice.

Knowing your stuff

Top earners don't fumble. They know eligibility, documents, timelines, and payouts cold. If a customer asks about interest rates, answer instantly. Hesitation kills trust.

Take every free training GroMo offers. You'll learn objection handling and get certified, which shows up on your profile. Also, study your rejections. If 60% of card apps fail for low credit scores, start using the eligibility calculator first.

Segment your list. Tier 1: Salaried ₹1 lakh+, CIBIL 750+. Pitch premium cards and big loans. Tier 2: Salaried ₹30K–₹1L. Entry-level cards and smaller loans. Tier 3: Students, gig workers, thin credit files. Start with demat accounts. Build the relationship.

Match your pitch. Tier 1 wants rewards: "5% cashback on international spends." Tier 2 wants speed: "Approved in 2 hours." Tier 3 needs education: "Start building your score now."

Use a CRM to track notes. Income, pain points, past convos. Review before calling. If someone wanted a business loan 30 days ago but paused, check back. Timing matters.

Handle objections cleanly. "Too many cards?" -> "This one replaces your others with better rewards." "High interest?" -> "The difference on a ₹50k loan is ₹83/month. Less than your coffee habit." "Scared of rejection?" -> "Pre-qual says 92% approval. Let's try."

Read more on commission earnings and part-time jobs for extra tactics.

Systems and scale

Manual work will cap you. You need automation.

Use WhatsApp Business API for follow-ups: Day 1 benefits, Day 3 eligibility, Day 5 offer. It runs without you typing.

Track leads in a CRM Google Sheets is fine. Name, status, follow-up date. Set reminders. A missed follow-up is lost money.

Bulk tools like WATI let you send 10,000+ messages. Upload, segment, schedule. Always include an opt-out. Good broadcasts get 3%–5% replies.

Block your time. 6–8 AM prospecting. 8–12 meetings. 12–2 processing. 2–4 team calls. 4–7 follow-ups. 7–9 training. This rhythm keeps you moving.

Hire help. A VA costs ₹10k–₹15k/month. If you're earning ₹1 lakh a day, your hour is worth ₹12,500. Don't waste it on data entry.

Watch your dashboard. Conversions, payouts, rejections. If business loans slow down, shift to personal loans for quick cash.

See referral strategies and growth sectors for more ideas.

Playing by the rules

You can't earn ₹1 lakh a day if you get banned. GroMo has strict rules. No fake docs. No promises of jobs or loans. No direct payments. Always use the customer's phone for KYC.

Be transparent. Tell them about fees, rates, and charges upfront. A customer who finds out about hidden fees later will hurt your reputation.

Secure your data. Don't share customer info. Delete records when you're done (RBI rules). Use encrypted channels.

Watch for clawbacks. Some loans reverse commission if the customer defaults on the first 3 EMIs. Pre-qualify carefully. Check income and credit. A few rejections are better than a clawback.

Stay updated. RBI changes rules quarterly. Read announcements. Join webinars.

Sell what helps. Don't push a bad product for a high payout. A customer who gets a good deal refers five others. One bad deal kills ten future sales.

Check West Bengal, Delhi, and Tamil Nadu guides for local rules.

People actually doing this

Rajesh, Pune Started Jan 2024 making ₹15k/month on cards. By June, he had 20 partners. By Dec, 80. Today he clears ₹80k/day from team overrides plus ₹50k personal. Total: ₹1.3 lakh/day. He targets IT pros in Pune via LinkedIn and meetups.

Priya, Delhi NCR Solo operator. Focuses on big business loans. She works with 15 CA firms in Gurgaon, giving them 10% referral fees. They send 25–30 leads a month. Average loan: ₹20 lakh. Commission: ₹50,000. Two deals a day = ₹1 lakh. She acts like a consultant, not a salesperson.

Amit, Mumbai Runs a 30-person team plus personal sales. Team handles volume (loans, demat), earning him ₹35k/day in overrides. He does 10 high-ticket deals a day for ₹75k. Total: ₹1.1 lakh. He also runs a YouTube channel with 40k subscribers. Organic leads save him ad money.

Three different paths: team volume, high-ticket solo, or content-driven leads.

Mistakes to avoid

No follow-ups. 80% of sales need 5+ touches. Apply once and disappear? You lose. Set reminders for Days 1, 3, 7, 14, 30.

One product focus. If HDFC tightens rules and you only sell HDFC cards, you're dead. Mix it up: 40% cards, 30% personal loans, 20% business loans.

Ignoring training. 50 untrained partners make zero sales. Trained ones make 10–15. Hold weekly calls.

Bad math on ads. Spend ₹50k to make ₹40k? You lose. Track CAC. If a lead costs ₹75 and pays ₹1,500, that's a win. Referrals are free use them.

Compliance slips. One fake doc can end you. Verify on video. Check Digilocker.

Burnout. 67 deals a day solo is a burnout recipe. Build a team by month 6. You want a system, not a job.

See legit apps and best practices for more.

90-day plan

Month 1: Download GroMo. Finish courses. Close 30 deals (1/day). Learn. Use friends/family. Goal: ₹30k–₹50k.

Month 2: Hit 3 deals/day. Run ads, WhatsApp blasts. Build a 500-person list. Goal: ₹1L–₹1.5L.

Month 3: Recruit 10 partners. Train them. You keep selling. Goal: ₹2L–₹3L.

Month 4–6: Scale to 30 partners. Daily huddles. Goal: ₹5L–₹8L/month.

Month 7–9: Automate. Hire a VA. Start content. Team hits 50 deals/day. You handle big ones. Goal: ₹12L–₹18L/month.

Month 10–12: 50+ partners doing 2 deals each (₹30k override). You do 40 personal (₹60k). Total: ₹90k–₹1.2L daily.

Most people quit in 90 days. If you keep going, you hit the target in 12–18 months.

FAQs

Q: Is ₹1 lakh/day realistic for a beginner? A: Not immediately. You'll likely make ₹10k–₹30k/month for 3–6 months. ₹1 lakh/day takes a year or more of building a pipeline and team. It's a business.

Q: What pays the most? A: Premium credit cards (₹2k–₹3.5k), big personal loans (₹8k–₹15k), and business loans (₹30k–₹60k). Demat accounts pay less but convert fast.

Q: How big a team do I need? A: With ₹1,500 average commission and 20% override, 50 partners doing 2 deals each gets you ₹30k. You need about 45 personal sales to finish. Or get 80+ partners and do fewer yourself.

Q: What should I spend to get a customer? A: Keep CAC under 5% of payout. For ₹1,500 commission, don't spend more than ₹75/lead. Ads run ₹30–₹60/lead. Referrals are free.

Q: How fast do payouts happen? A: Usually 24–48 hours. Some loans hold payment for 90 days (clawback period). Check terms.

Q: Is this sustainable? A: Yes, if you adapt. Fintech distribution is growing 30% a year. You need to stay compliant, diversify, and maintain relationships.