Top 10 Fastest-Growing Business Sectors in India 2026

India's business environment is changing. Digital infrastructure, a young population, and recent policy changes are driving it. The country has over 60 million MSMEs. Sectors like fintech, e-commerce, and direct-to-consumer brands are growing.

I want to cover the fastest-growing business sectors in India for 2026, explain what's driving them, and show how you can get involved. If you're looking for side income or thinking about entrepreneurship, these trends matter.

The State of India's Business Ecosystem in 2026

India is now the world's fifth-largest economy. GDP growth here beats most developed nations. The government's Digital India initiative, GST implementation, and startup policies have made starting ventures easier. Mobile internet has reached over 800 million users. That creates real opportunities for digital-first businesses.

Small and medium enterprises contribute about 30% to India's GDP. For years, though, traditional barriers kept millions of people from starting businesses. Capital requirements. Inventory costs. Real estate expenses. That's changed with zero-investment business models.

Platforms like GroMo have made it possible to access profitable business opportunities without upfront capital. The platform has 60 lakh+ partners earning commissions by distributing financial products. I think this shift represents something bigger happening across Indian commerce.

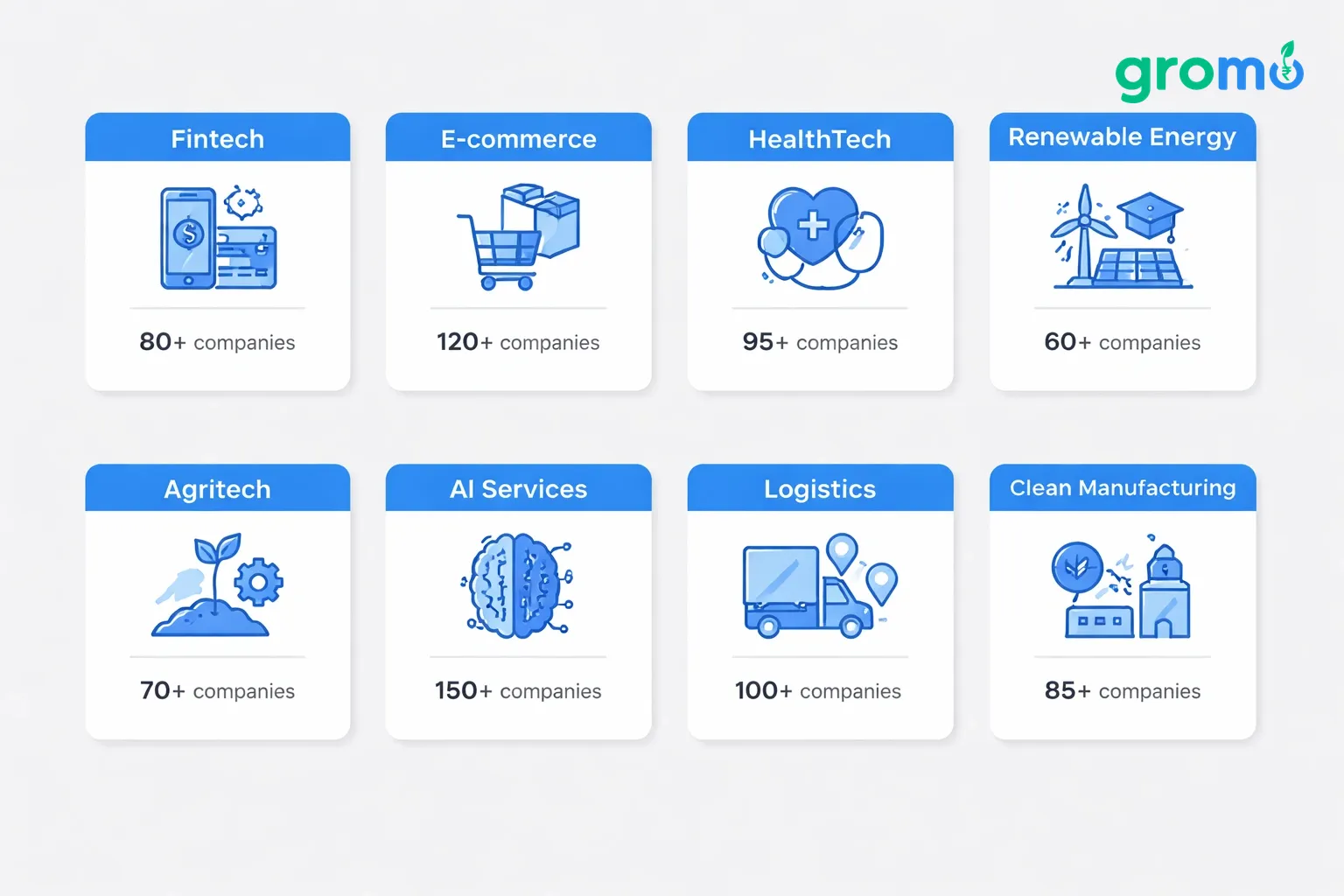

Top 10 Fastest-Growing Business Sectors in India (2026)

1. Fintech & Digital Financial Services

This is India's most explosive growth sector. The industry is valued at $150+ billion and growing at 22% annually. UPI transactions crossed 12 billion monthly. I find that number staggering it shows how quickly India has moved toward cashless payments. The sector includes digital payments, lending platforms, wealth management, neobanking, and insurance technology.

Why the growth? 190 million Indians remain unbanked or underbanked. That's a massive market. RBI's digital lending guidelines and account aggregator frameworks have legitimized the space. And consumer comfort with digital transactions has taken hold, especially in Tier 2 and Tier 3 cities.

Where I see opportunity: You can distribute financial products without inventory or technical infrastructure. Platforms offering commission-based models let anyone earn by connecting customers with credit cards, loans, savings accounts, and investment products. Top distributors earn ₹1 lakh+ monthly with just a smartphone and a network.

Here's what pays: Axis Bank savings accounts give ₹300-500 per activation. Credit card referrals generate ₹2,000-3,000 each. Business loans and credit lines offer 0.5% to 3% of sanctioned amounts. You can build real income without business loans or office space.

2. E-commerce & Quick Commerce

India's e-commerce market crossed $120 billion in 2026, growing at 18% year-over-year. Quick commerce 10-minute deliveries is the fastest sub-segment. Blinkit, Zepto, and Swiggy Instamart together process 5 million daily orders. The shift to direct-to-consumer brands has accelerated too. D2C brands collectively pull in ₹1 lakh crore in annual revenue.

Tier 2 and Tier 3 cities now contribute 60% of new e-commerce customers. That surprised me. Mobile commerce dominates at 78% of all online transactions. Social commerce through Instagram and WhatsApp has opened new distribution channels.

Where I see opportunity: Reselling or affiliate partnerships require no inventory. Many D2C brands offer 10-25% commissions on sales through referral links. If you create content product reviews, unboxing videos, curated recommendations you can generate passive income.

3. EdTech & Upskilling Platforms

The education technology sector reached $10.4 billion in 2026, growing 20% annually. K-12 online tutoring has matured. The real growth now comes from professional upskilling, vernacular education, test preparation, and corporate training. Platforms focusing on job-ready skills data science, digital marketing, coding are doing well.

Government initiatives like Skill India drive adoption. The gig economy's expansion creates ongoing demand for new competencies. Regional language content has unlocked audiences that English-only platforms couldn't reach.

Where I see opportunity: Educational platforms offer ₹500 to ₹5,000 per successful course enrollment through affiliate commissions. If you have expertise in high-demand skills, creating micro-courses on platforms like Teachmint or Unacademy lets you monetize directly.

4. Healthcare & Telemedicine

Digital healthcare crossed $11 billion in 2026, growing at 27% annually. That makes it India's fastest-expanding sector by growth rate. Telemedicine consultations increased 15x since 2020. Online pharmacy delivery captured 8% of India's pharmaceutical market. Health insurance penetration sits at 35% and rising among urban millennials.

Chronic disease management platforms, mental health services, and elderly care technology are emerging. Government digitization of health records through Ayushman Bharat Digital Mission has created interoperability. Preventive health and wellness now compete with reactive treatment.

Where I see opportunity: Health insurance distribution pays well typically 15-25% of first-year premiums. For a policy with ₹25,000 annual premium, you'd earn ₹3,750-6,250. Wellness product affiliate programs and nutrition consultation referrals offer additional streams.

5. Renewable Energy & Green Technology

India's renewable energy sector should reach $100 billion by 2028. Current growth rates exceed 30% annually. Solar installation, electric vehicle infrastructure, energy storage systems, and carbon credit trading are all expanding. Government mandates requiring 40% renewable energy by 2030 help.

Corporate ESG commitments create demand beyond government targets. Solar power is now cheaper than coal in most regions. Consumer awareness of climate issues affects purchasing preferences.

Where I see opportunity: Solar installation companies pay ₹5,000-15,000 per successful rooftop installation referral. EV manufacturers and charging network operators provide commissions for customer referrals. Green product aggregation curating and promoting sustainable brands creates content monetization opportunities.

6. Food & Beverage Innovation

India's food services industry reached ₹5.5 lakh crore in 2026. Cloud kitchens and delivery-first brands are taking share. Health-conscious consumers drive demand for organic, plant-based, and functional foods. Regional cuisine packaged for national distribution is growing. Brands like iD Fresh Food and millet-based startups are scaling.

Beverage innovation beyond chai and coffee cold brew, kombucha, protein shakes is finding urban traction. Food processing technology that extends shelf life without preservatives enables D2C models that weren't possible before.

Where I see opportunity: Delivery partnerships with Swiggy or Zomato provide immediate income. Transitioning to a cloud kitchen aggregator role offers higher margins. Food product affiliate marketing through Instagram and YouTube generates commissions from health food brands. Exploring side income opportunities here requires minimal capital.

7. Logistics & Supply Chain Technology

Logistics technology crossed $8 billion in 2026, growing at 16% annually. Third-party logistics, last-mile delivery optimization, warehouse automation, and freight marketplaces are expanding. E-commerce growth drives this directly. ONDC (Open Network for Digital Commerce) is creating new efficiency requirements.

Cold chain infrastructure for perishables, reverse logistics for returns, and hyperlocal delivery networks are high-growth sub-segments. Technology for real-time tracking and route optimization commands premium valuations.

Where I see opportunity: Becoming a delivery partner or micro-warehouse operator requires minimal investment. Logistics aggregation connecting businesses with optimal shipping solutions offers commissions. If you have a vehicle, partnering with freight platforms generates steady income.

8. Content Creation & Digital Media

India's digital advertising market reached ₹58,000 crore in 2026. Content creators are capturing growing shares. YouTube, Instagram, and regional platforms like ShareChat support millions of creators earning through ads, sponsorships, and affiliate sales. Vernacular content now dominates. Hindi, Tamil, Telugu, and Bengali creators often outearn English-language channels.

Micro and nano influencers (10,000-100,000 followers) get disproportionate brand interest because their engagement feels real. Educational content, entertainment, lifestyle vlogs, and financial advice channels all monetize successfully.

Where I see opportunity: Starting a YouTube channel or Instagram page requires just a smartphone. Monetization begins at 1,000 subscribers and 4,000 watch hours. Finance content creators earn ₹20,000-2,00,000 monthly promoting credit cards, demat accounts, and loans through platforms like GroMo's referral programs.

9. Real Estate Technology (PropTech)

Property technology reached $3.5 billion in 2026, growing at 19% annually. Online property search, virtual tours, fractional real estate investment, rental management platforms, and interior design marketplaces are disrupting traditional models. RERA compliance has increased consumer confidence in digital transactions.

Co-living and co-working spaces continue expanding in metros and Tier 1 cities. Smart home technology creates new value propositions. Property financing instant approvals, flexible tenures removes traditional friction.

Where I see opportunity: Real estate referral programs pay well typically 0.5-1% of property value. For a ₹50 lakh apartment, that's ₹25,000-50,000. Home loan distribution generates 0.25-0.5% of sanctioned amounts. Interior design aggregation connecting customers with vendors pays coordination fees.

10. Direct Selling & Social Commerce

Direct selling in India crossed ₹19,000 crore in 2026, growing at 14% annually. Social commerce selling through WhatsApp, Facebook, and Instagram has become mainstream, especially for fashion, beauty, and lifestyle. Live commerce, where hosts demonstrate products in real-time, is catching on.

Trust-based selling through existing networks works better than traditional advertising for certain categories. No middlemen means higher margins for sellers and lower prices for consumers.

Where I see opportunity: Joining direct selling companies requires minimal investment often just a starter kit. Social commerce needs zero capital. Curate products, share with your network, earn commissions. Zero-investment business models here are particularly accessible for housewives and students.

Why These Sectors Are Growing

Digital Infrastructure

India's digital infrastructure has reached a useful scale. 4G/5G coverage extends to 95%+ of the population. Data costs have fallen 95% since 2016. Even low-income segments can now use data regularly. This infrastructure powers everything I mentioned above.

Government initiatives like BharatNet are connecting 250,000 gram panchayats with high-speed internet. Digital payment infrastructure UPI, Aadhaar-enabled systems, account aggregators enables frictionless transactions. Businesses can now reach markets that were previously inaccessible.

Rising Middle Class

India's middle class expanded to 400 million people in 2026. By 2030, projections say 600 million. This drives consumption across categories from basic financial services to spending on education, health, and experiences. Per capita income crossed ₹2 lakh. Products once considered luxuries are now within reach.

Urbanization continues. 40% of Indians now live in cities. Tier 2 and Tier 3 cities are growing faster than metros, combining urban aspirations with lower living costs. This creates real markets for e-commerce, fintech, and services.

Policy Changes

India's World Bank Ease of Doing Business ranking improved from 142 in 2014 to 63 in 2026. GST simplified indirect taxation, eliminating cascading effects that hurt interstate commerce. Startup India initiatives provide tax exemptions, easier compliance, and access to government tenders.

Production Linked Incentive (PLI) schemes across 14 sectors encourage manufacturing. Digital regulatory frameworks for fintech, telemedicine, and education have provided legal clarity. FDI liberalization in insurance, aviation, and defense opens opportunities.

Technology Adoption

Indian businesses are adopting technology fast. Cloud computing adoption grew 40% year-over-year. AI and machine learning are now operational tools not experiments.

API-first architecture enables rapid integration. Open-source solutions reduce development costs. No-code and low-code platforms let non-technical founders launch products. Entry barriers are lower across sectors.

How to Participate: Zero-Investment Strategies

Financial Product Distribution with GroMo

This is the most accessible entry point. GroMo's platform lets anyone become a certified financial advisor and earn commissions without inventory, licenses, or capital. The model: share product links, guide customers through applications, earn payouts on completion.

What pays well:

Credit cards: Axis Flipkart Card pays ₹2,000-3,000. IDFC FIRST WOW offers similar. Ten successful applications monthly gets you ₹20,000-30,000.

Savings accounts: Axis Burgundy, Kotak 811, and IndusInd generate ₹300-500 per activation.

Demat accounts: Upstox and Indiabulls pay ₹250-400 per account opened with a minimum trade.

Loans: Business loans offer 1.5-3% of sanctioned amounts. A ₹3 lakh loan generates ₹4,500-9,000. Personal loans and credit lines provide 0.5-2%.

How I'd approach it: Build a referral system by sharing the opportunity with others. GroMo's referral program pays when people you recruit make sales. Focus on high-commission products first. Use proven strategies for earning ₹1 lakh monthly even with a full-time job.

The platform gives you training, marketing materials, customer management tools, and instant payouts.

Content Creation & Affiliate Marketing

Creating financial education content positions you as a trusted advisor while generating affiliate income. Start a YouTube channel, Instagram page, or blog. Focus on personal finance: credit scores, loan comparison, investments, credit card reviews.

Money comes from:

Ad revenue: YouTube and blogs generate ad income once you hit thresholds. Finance channels earn higher CPMs (₹80-200 per 1,000 views).

Affiliate commissions: Promote products through your content. Viewers apply through your links, you earn. Top creators earn ₹50,000-2,00,000 monthly.

Sponsored content: Brands pay for dedicated videos or posts. Rates range from ₹5,000 for micro-influencers to ₹50,000+ for established creators.

Start simple. "Best credit cards for salaried professionals" or "Fixed deposits vs mutual funds." Answer questions people actually search for. Link products in descriptions.

Referral & Network Marketing

Your existing network can become income. Identify products you already use and recommend credit cards, banking apps, investment platforms. Most have referral programs.

What works:

- Check your current financial products for referral programs

- Create simple messages for WhatsApp groups

- Offer to help friends with applications

- Track what converts

Expand beyond friends by creating communities. Facebook groups or WhatsApp communities focused on financial literacy naturally lead to product recommendations. Referral income strategies show people earning ₹30,000-1,00,000 monthly.

Freelancing

Skills don't require capital to monetize. High-demand areas:

Digital marketing: Content writing, SEO, social media, email marketing. Part-time rates start at ₹15,000-25,000 monthly.

Design: Graphics, UI/UX, video editing. Platforms like Fiverr and Upwork connect you with global clients.

Consulting: Accounting, HR, legal, business strategy. Premium rates: ₹1,000-5,000 per hour.

Virtual assistance: Admin support, calendar management, research. Good for flexible schedules.

Create profiles on Upwork, Fiverr, Toptal, or Freelancer.com. Price low initially to build reviews. Raise rates as reputation grows. Many freelancers go from side income to six figures monthly in 2-3 years.

Reselling

No inventory needed. The model: find quality products, create collections, market to audiences, earn commissions.

Platforms:

Amazon Associates: 1-10% on product sales. Create "best of" lists or comparison content.

Meesho: Resell fashion and lifestyle with 10-30% margins.

GlowRoad: Similar, focusing on women entrepreneurs in Tier 2/3 cities.

Industry marketplaces: Health supplements, books, electronics each have affiliate programs.

Know your audience. Parenting communities? Curate baby products. Fitness circles? Equipment and supplements. Only promote what you'd actually use.

Regional Differences

Metro Cities (Mumbai, Delhi, Bangalore, Hyderabad, Pune)

Premium services work well here. Wealth management, health insurance for high-income families, premium credit cards, international demat accounts. Corporate employees want tax-saving investments, home loans, education loans.

High-earning professionals create opportunities for specialized advisory services. Focus on higher commissions and longer-term relationships. Mumbai-specific strategies show how local dynamics matter.

Tier 2 Cities (Jaipur, Chandigarh, Lucknow, Coimbatore)

These cities balance affordability with aspiration. Focus on first-time users: first credit card, first demat account, first two-wheeler loan. Educational content works well here financial literacy gaps are bigger.

Business loan distribution does well as MSMEs digitize. Home loans are strong since real estate remains affordable. Bangalore's ecosystem shows how tier structure affects things.

Tier 3 Cities & Rural Areas

Basic banking services are growing fast here. Zero-balance savings accounts, small personal loans (₹10,000-50,000), micro-investment products. Government scheme awareness PM Mudra, Kisan credit cards creates advisory opportunities.

Use vernacular communication. WhatsApp outperforms other channels. Community trust matters more than digital advertising. Punjab approaches show regional customization.

What You Can Realistically Earn

Beginner (0-3 months): ₹10,000-25,000 monthly

New partners usually focus on one product category, learning the process. Income comes from your immediate network. Conversion rates are lower while you learn objection handling.

Focus on: mastering 2-3 high-commission products, completing training, setting daily targets (10 conversations, 5 applications), tracking what works.

Intermediate (3-6 months): ₹25,000-50,000 monthly

Experience improves conversion rates from 5-10% to 15-20%. You can match customers to products better. Referral systems start generating passive income.

Focus on: expanding to 5-7 products, developing sales scripts, implementing CRM for follow-ups, recruiting 2-3 sub-partners.

Advanced (6-12 months): ₹50,000-1,00,000 monthly

Reputation creates inbound referrals. Team-building generates override commissions. Specializing in high-value products (business loans, wealth management) increases average transaction size.

Focus on: building a team of 5-10 active sub-partners, creating content marketing, partnering with chartered accountants or consultants for referrals.

Expert (12+ months): ₹1,00,000-3,00,000+ monthly

Top performers run micro-enterprises with teams. Multiple streams direct commissions, overrides, content monetization, consulting create diversified income. Brand recognition drives organic customers.

Focus on: scaling to 20+ partners, developing training systems, expanding into adjacent services (tax filing, bookkeeping).

Challenges You'll Hit

Customer Acquisition

Problem: Every bank and fintech has multiple distribution channels. You need to stand out.

What works: Position as an advisor, not a salesperson. Show why specific products fit specific profiles. Use educational content to build authority. Target under-served niches first-time credit users, senior citizens, freelancers with irregular income.

Motivation During Slow Periods

Problem: Commission income fluctuates. Great months. Terrible months. This discourages beginners.

What works: Set non-negotiable daily activities. 10 conversations. 5 product shares. 2 follow-ups. Celebrate small wins applications submitted, not just completed sales. Join partner communities. Track leading indicators (conversations) not just lagging ones (income).

Product Rejections

Problem: Banks reject 30-50% of applications due to credit scores, income verification, or policy changes. Rejected customers might blame you.

What works: Set expectations early. "I'll help you apply, but approval depends on bank policies. If rejected, we'll figure out why and find alternatives." When rejections happen, offer credit score guidance or products for bad CIBIL scores. Being helpful builds loyalty.

Knowledge Gaps

Problem: Financial products have interest calculations, clauses, eligibility criteria. Misrepresenting features creates liability.

What works: Complete training. Never guess check documentation or support. Say "Let me confirm that with the bank" rather than speculating. Start with straightforward products (savings accounts, credit cards) before complex ones. Legitimate platforms emphasize training.

Tools That Help

CRM

GroMo has in-app CRM. But tracking in Google Sheets helps too:

- Lead source

- Product interest

- Application status

- Follow-up schedule

Tracking reveals patterns: best-converting products, most profitable lead sources, recurring objections.

WhatsApp Business

Automated greetings, product catalogs, quick replies. Create templates for common questions.

Broadcast lists let you send tips or updates without revealing recipients.

Content Tools

Canva for graphics. No design skills needed.

CapCut or InShot for mobile video editing. Short-form video outperforms text.

Grammarly for professional writing. Clear communication matters in finance.

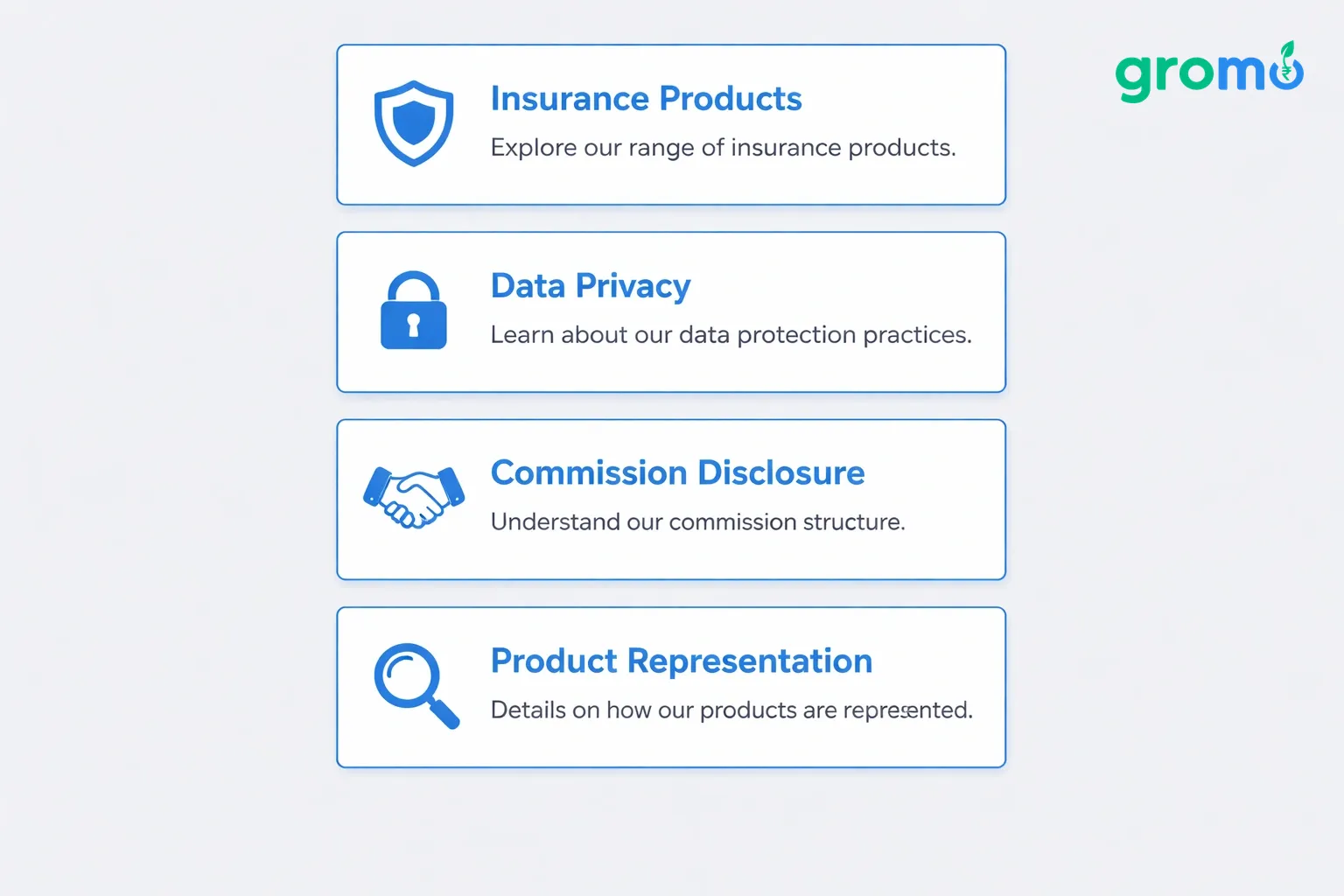

Legal Stuff

Insurance Products

If you distribute insurance independently, IRDAI registration is mandatory. 15-hour training course plus exam. PoSP certificates let you sell basic insurance. (GroMo no longer offers insurance products.)

Data Privacy

Never share customer data with unauthorized parties. Store securely. Use official channels.

Commission Disclosure

Ethics and regulations increasingly require disclosing commissions. Simple statement: "I earn a commission from the bank if you apply through my link. No cost to you."

Transparency builds trust.

Product Representation

Never misrepresent rates, fees, or eligibility. When uncertain, check official documentation. Over-promising destroys reputation permanently.

Real Results

Rajesh Kumar, Delhi (6 months)

Full-time accountant. Started sharing credit card offers with his client base small business owners asking about expenses. Six months in: ₹2.1 lakh total, averaging ₹35,000 monthly as side income. His approach: focus only on business credit cards and small business loans, using existing relationships.

Priya Sharma, Pune (10 months)

Homemaker. Started with savings and demat accounts through her residential society WhatsApp groups. Created simple educational posts about financial planning. After ten months: ₹48,000 monthly. Her edge: offering free help with applications, becoming a helpful neighbor rather than a pushy salesperson.

Mohammed Iqbal, Hyderabad (14 months)

Transitioned from offline insurance sales to digital distribution. Built a YouTube channel in Telugu explaining loan eligibility and credit card benefits. 15,000 subscribers. YouTube ad revenue: ₹12,000 monthly. Affiliate commissions: ₹95,000 monthly. Total: ₹1.07 lakh. Content plus distribution.

Going Full-Time

When to Transition

Consider it when:

- Side income consistently exceeds 75% of salary for 3+ months

- Customer pipeline extends 2-3 months

- Emergency fund covers 6 months

- Health insurance secured independently

- Family supports the decision

Too-early transitions create financial stress that hurts performance.

Building Systems

Full-time success needs systems that generate income without constant involvement:

Team: Recruit partners who handle conversations and applications. You train and acquire customers.

Content: Evergreen content (blogs, videos, posts) attracts customers organically.

Referral networks: Partner with chartered accountants, tax consultants, real estate agents. Exchange referrals or share fees.

Processes: Document standard procedures for delegation.

Diversifying

GroMo is comprehensive, but successful distributors diversify:

- Direct bank DSA arrangements for higher commissions

- Multiple fintech affiliate programs

- Financial planning consultation

- Tax filing and bookkeeping

- Business registration services

Diversification stabilizes income.

What's Coming Through 2030

India's GDP should reach $7 trillion by 2030. Third-largest economy globally. 1 billion+ Indians online. Financial inclusion aims to bring the remaining 100 million unbanked into formal systems.

Regulatory changes will continue. ONDC commoditizing e-commerce logistics. Account aggregator frameworks enabling new lending. Digital rupee creating payment ecosystems.

The sectors here will likely stay strong. New ones will emerge: space tech, synthetic biology, advanced manufacturing, climate tech.

For individuals, opportunity democratization will intensify. Zero-investment models create alternatives to traditional employment. Skills in customer acquisition, digital communication, and scaling will matter regardless of sector.

Starting Today

Reading creates awareness. Action creates results.

Today:

- Download GroMo and register

- Pick 2 high-commission products to learn first

- List 10 people who might need these

- Complete first training module

- Share your first product link with someone

Week one:

- Complete all training

- Talk to all 10 contacts

- Submit 3 applications

- Join partner communities

- Post about your new role

Month one:

- Process 15+ applications

- Earn first ₹10,000

- Recruit 2 sub-partners

- Establish daily routine

- Identify best-converting products

Growth compounds. First month might be modest. Systematic effort creates month-over-month improvement. Partners who persist 6-12 months hit ₹50,000-1,00,000 monthly that seemed impossible at first.

India's business growth isn't abstract data. It's opportunity. The question is whether you'll take it.

FAQ

Do I need sales experience? No. GroMo provides training on products, communication, objection handling, applications. Top earners came from teaching, engineering, homemaking. Willingness to learn and consistent effort matter more than background.

Time needed for ₹50,000 monthly? Most partners earning that invest 3-4 hours daily. Part-time (1-2 hours) typically yields ₹15,000-25,000. Efficiency improves with experience. Systems and teams reduce time as you scale.

What if customers default or don't use cards? For most products, once activation criteria are met (first transaction, minimum deposit, first trade), your commission is secure. Some business loans have clawback default on first 3 EMIs reverses commission. GroMo shows which products have this. Focus on quality customers, not just volume.

Conflict with full-time job? Most partners keep full-time jobs. Independent contractor arrangement means no conflict unless your contract prohibits outside activities (rare except senior positions). No fixed hours work when convenient. Many partners work during commutes, lunch, evenings.

How does this compare to traditional business? Traditional business: ₹2-10 lakh investment, 12-24 months to break-even, inventory risk, location dependence. Distribution: zero investment, positive cash flow from first sale, work from anywhere, no inventory. Trade-off: traditional businesses can scale higher long-term; distribution typically caps at ₹2-3 lakh monthly without large teams.

What makes GroMo different from task apps? Task apps pay ₹5-20 for ads or games. GroMo pays ₹250-3,000 per sale real business activity. Y Combinator-backed. ₹100+ crore paid to 60 lakh+ partners. Training, materials, CRM, instant payouts, support. Building skills and business, not micro-tasks. ₹1 lakh+ monthly achievable versus ₹5,000 max for task apps.