Zero-Investment Home Businesses in Tamil Nadu: Earn ₹15K-Monthly

Starting a business in Tamil Nadu used to mean finding capital. Rent. Inventory. Licenses. Each barrier weeded out people who had the skills but not the money.

That's changed. Your phone is now a business platform.

Across Chennai, Coimbatore, Madurai, and smaller towns, people are earning ₹15,000 to ₹1,00,000 monthly from home. Financial product distribution. Freelancing. Content creation. Online services. All without spending a rupee to start.

What Zero-Investment Actually Means

No physical infrastructure. No inventory. No licensing fees. You use what you already have smartphone, internet connection, personal network.

Tamil Nadu has an advantage here: the density of tier-2 and tier-3 cities. Tiruppur, Salem, Erode, Thanjavur. Lower living costs, growing digital literacy. A person in Dindigul can earn the same as someone in Chennai distributing financial products through apps. Geography stopped being a barrier.

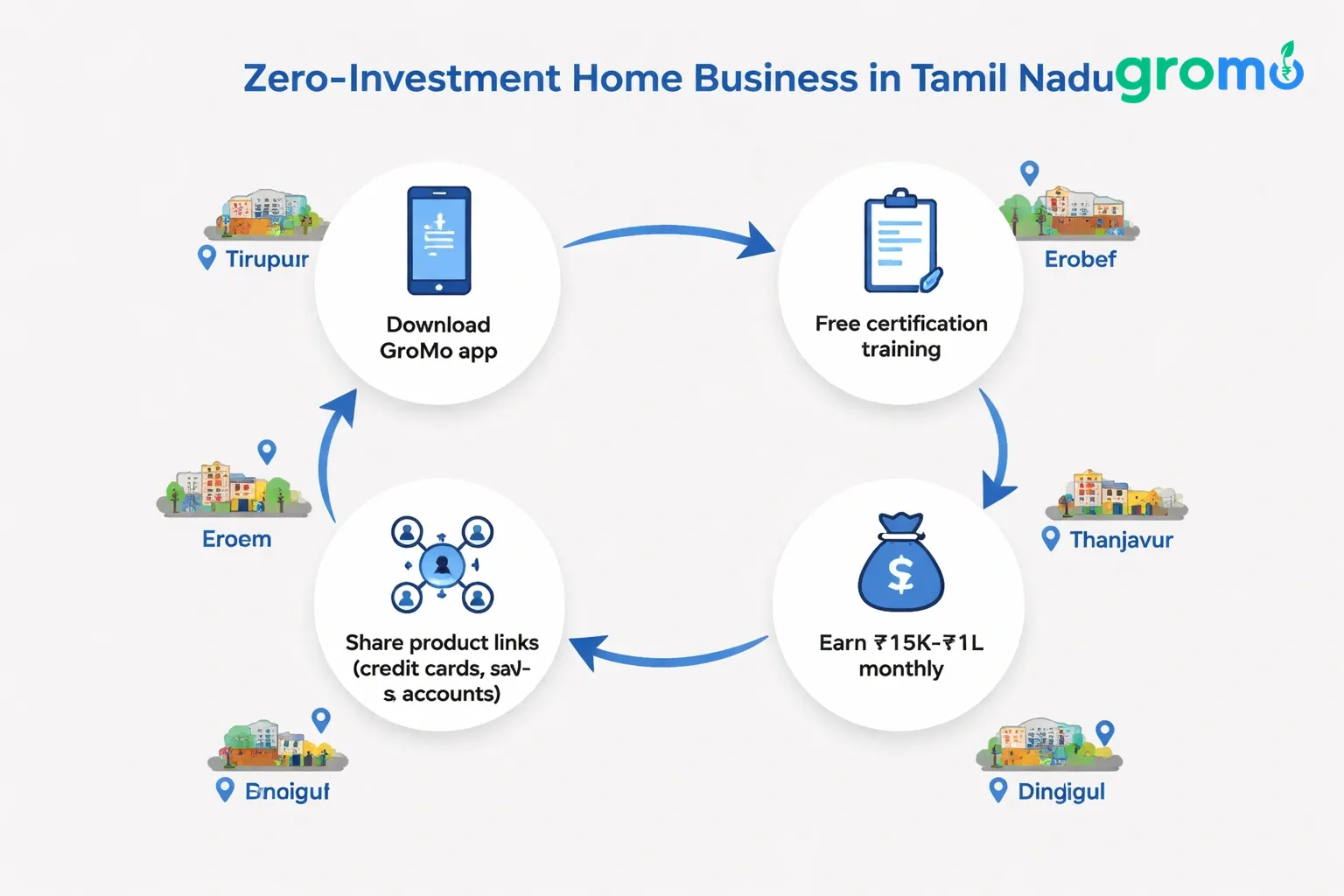

Platforms like GroMo show how this works. Download the free app, complete free certification training, share product links for credit cards, savings accounts, demat accounts, loans. Each successful application earns commissions ₹250 for demat accounts, up to ₹2,400 for premium credit cards. You don't handle money, don't provide customer support (banks do), don't stock inventory.

Home-Based Business Ideas That Work in Tamil Nadu

Financial Product Distribution

The old model: financial advisors needed certifications, office space, years to build credibility.

The current model: free online training, share links via WhatsApp or social media.

Tamil Nadu's banking penetration is 78% of households (RBI 2026). That's a large addressable market. Factory workers in Coimbatore applying for first credit cards. Students in Madurai opening demat accounts. Homemakers in Trichy helping neighbors with personal loans.

Platforms provide marketing materials, training videos, customer tracking, instant payouts. A home-based business with GroMo runs through your phone entirely.

Commissions: Upstox demat accounts pay ₹250-400. Tide business accounts can reach ₹2,000. Credit card referrals earn up to ₹2,400 for premium cards. Partners consistently hitting ₹50,000+ monthly process 25-40 applications across categories.

Tamil Content Creation

Tamil is the fifth most spoken language globally 80 million speakers. But quality Tamil content for finance, tech, lifestyle? Much less than Hindi or English. That gap is an opportunity.

Finance channels work. Explain UPI, CIBIL scores, loan comparisons. Build 50,000-200,000 subscribers in 12-18 months. YouTube's Partner Program pays ₹8-15 per thousand views for Tamil finance content (advertisers pay more). Channels with 2-5 million monthly views earn ₹30,000-80,000 monthly.

Equipment: phone, free editing apps (CapCut), natural light. First 20 videos will probably underperform consider it market research.

Localization runs parallel. International companies need website translations, app localization, cultural consulting for Tamil Nadu entry. Fiverr, Upwork, Freelancer.com list projects at ₹500-2,000 per 500 words. Technical and legal translations pay more.

Online Tutoring

Tamil Nadu's education culture creates demand. Chennai parents pay ₹300-800 per hour for quality tutoring. Competitive exam prep (NEET, JEE, TNPSC) commands ₹1,000-2,000 hourly for experts.

Platforms: Unacademy, Vedantu, Toppr, WhiteHat Jr. Teach from home via laptop, set your hours, earn ₹15,000-60,000 monthly. Math, science, English stay in highest demand.

Beyond school subjects: Spoken English for professionals, computer literacy for adults reentering workforce, digital marketing for small business owners. Weekend Excel classes in Coimbatore: ₹3,000-5,000 per student for eight-week courses. Ten to fifteen students per batch: ₹30,000-75,000.

Test prep for Tamil Nadu government exams (Group 1, 2, 4) and banking exams (IBPS, RRB) taps steady local demand. Create video courses on Teachable or Graphy students buy lifetime access, you earn recurring revenue from content you make once.

Freelancing and Consulting

Tamil Nadu produces 8.5% of India's engineering graduates (AICTE, 2026). Many are underemployed. Freelancing redirects talent to global markets paying international rates.

A Trichy developer earning ₹40,000 monthly at a local company can shift to freelance at $15-30/hour (₹1,200-2,400). Same hours, 3-6x income.

High-demand categories: web development, mobile apps, graphic design, content writing, virtual assistance, social media management, data entry. Platforms like Upwork, Fiverr, and Freelancer need only a profile no upfront fees.

First 5-10 projects build your profile. Charge competitively, over-deliver, collect five-star reviews. Most freelancers beat traditional employment income after 3-4 months.

Consulting leverages experience. Textile manufacturing background? Process optimization for Tiruppur exporters. HR experience? Recruitment for growing startups. Consulting bills ₹1,500-5,000 hourly.

How Financial Product Distribution Works

Getting Started

Download the app (Google Play or Apple App Store). Register with mobile number, PAN card, bank account for payouts. Ten to fifteen minutes.

Free training follows immediately: credit cards, loans, savings accounts, demat accounts, application processes, eligibility, compliance. Video lessons, quizzes, certification. Core training takes 2-3 hours.

Your dashboard provides personalized referral links. Send via WhatsApp, SMS, email, social media. Platform tracks clicks, applications, approvals no manual record-keeping.

Product selection strategy: Credit cards pay most (₹250-2,400) but need creditworthy customers. Savings accounts convert easily but pay less (₹50-300). Demat accounts target investors, moderate payouts (₹250-400). Loans pay percentage-based commissions (1.5%-5.5% of amount).

Finding Customers

Credit cards: salaried professionals 25-45, stable income, existing banking relationships. A Chennai IT professional earning ₹50,000+ monthly is ideal likely lacks cards (India's penetration is 3%) and meets criteria.

Savings accounts: tier-2/tier-3 residents, young adults opening first accounts, small business owners needing separate business banking. Tide business accounts help freelancers and micro-enterprises in Erode, Salem, Thanjavur who want digital features and business-focused tools.

Demat accounts: salaried professionals interested in stocks, SIPs, IPOs. Tamil Nadu's middle class in automotive, textile, IT sectors increasingly wants diversification beyond fixed deposits and gold. "Best SIP plans" or "how to buy stocks" questions signal opportunity.

Personal loans: medical emergencies, education fees, weddings, business working capital. Financial stress mentions, upcoming expenses, rejected bank applications suggest trying digital lenders.

Building Networks

Family and friends first. Tell your immediate circle. Explain benefits, offer help. Build confidence before wider outreach.

WhatsApp groups scale reach. Alumni, housing society, professional, hobby groups occasional relevant messages posted at the right time generate inquiries. Tax-saving fixed deposits in January. Credit card benefits before festival shopping.

Social media compounds. Regular Facebook and Instagram posts about financial tips, product benefits, customer wins position you as a resource. Tamil content attracts local audiences. Weekly tips on improving credit scores, UPI safety, loan comparisons 500-2,000 followers view you as trusted.

Local business partnerships generate leads. Chartered accountants, real estate agents, automobile dealers, retail shop owners partnering creates win-wins. CA referring tax clients needing loans. Car dealer suggesting credit card offers for down payments.

Maximizing Commissions

Multi-product expertise increases per-customer earnings. Credit card applicant might need demat account for investing rewards. Business loan applicant probably needs business banking account for disbursement. Cross-selling doubles or triples revenue.

Volume targeting ensures consistency. Daily goals: 5 link shares, 2 application assistance conversations, 1 follow-up call. Partners earning ₹50,000+ maintain 15-25 active conversations with 4-8 applications progressing weekly.

Timing matters. Tax season (January-March) drives tax-saving demand. Festivals (August-October, December-January) boost credit card applications. New financial year (April) prompts account openings. Academic starts (June) trigger education loan inquiries.

Follow-up separates high earners. Most applications face delays missing documents, customer hesitation. Checking status, reminding about uploads, addressing concerns ensures completion.

Why Tamil Nadu Has Specific Advantages

Tier-2 and Tier-3 Cities

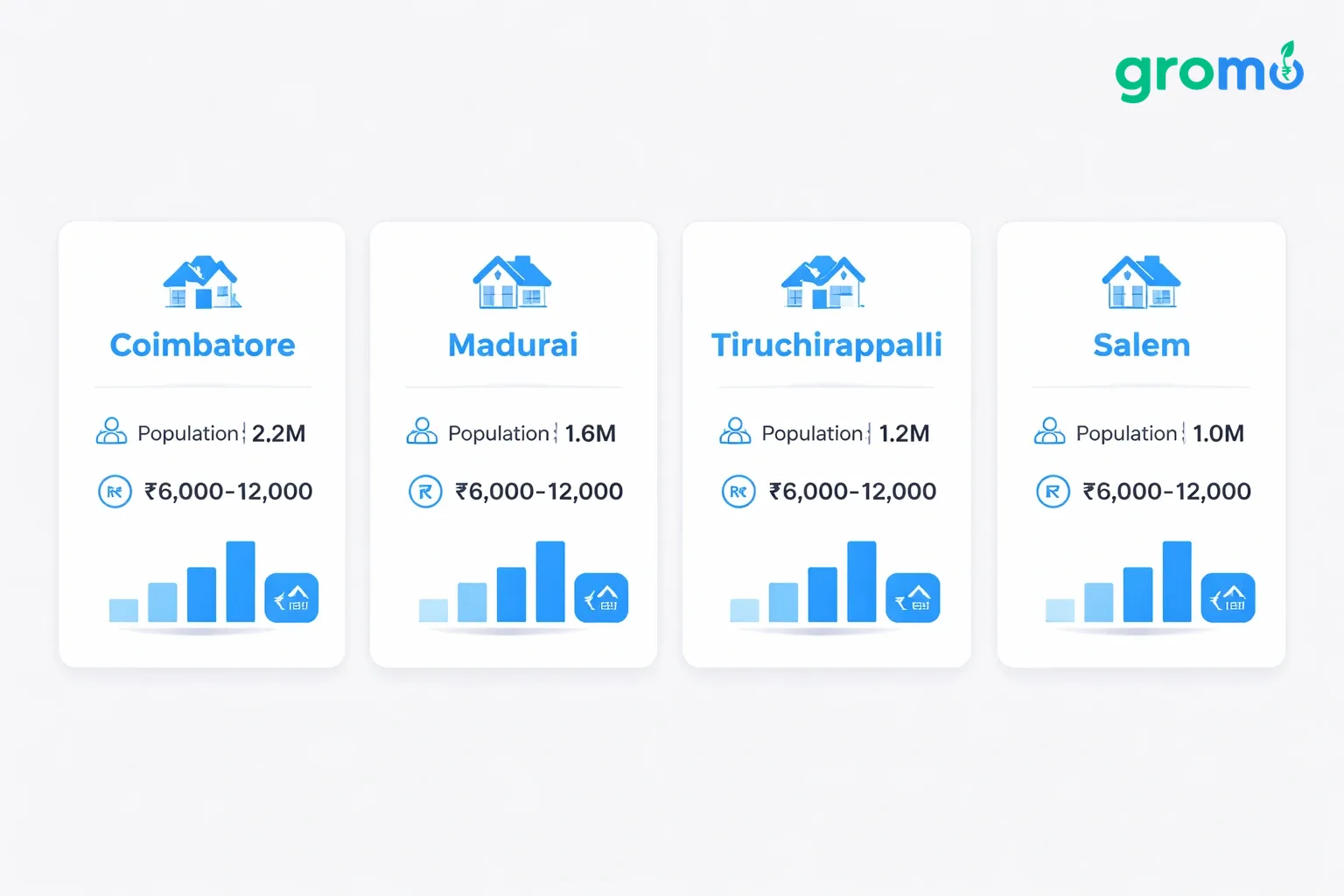

Chennai dominates conversations, but Coimbatore (2.2M), Madurai (1.6M), Tiruchirappalli (1.2M), Salem (1.0M) represent larger cumulative markets with less competition. Fewer active partners means more customer share for you.

Cost structures favor smaller cities dramatically. Chennai 2BHK rent: ₹15,000-30,000. Coimbatore or Madurai: ₹6,000-12,000. Your home-based business income goes further. ₹40,000 monthly means comfortable life in Salem. In Chennai, it barely covers expenses.

Banking growth in smaller cities creates opportunities. First-time credit card users, new demat holders, digital lending customers concentrate there as financial inclusion expands. Early trusted advisors capture long-term relationships.

Language advantage outside metros. Chennai residents often transact in English. Dindigul, Karur, Pudukkottai customers strongly prefer Tamil. Fluency removes barriers English materials create.

Cultural Factors

Tamil culture respects education and professional advice. Customers take certified advisors seriously. Platform training certification carries weight, especially with older demographics.

Family-oriented decisions create referral chains. Financial decisions involve multiple generations parents advising children, adult children managing parents' finances, extended family discussing purchases. One satisfied customer can trigger 3-5 referrals.

Festivals create natural engagement. Pongal, Diwali, Tamil New Year involve gifting, travel, spending. Proactive outreach before festivals with relevant products (credit cards for rewards, loans for expenses) aligns with needs.

Community networks caste associations, hometown groups, professional organizations facilitate trust. A community recommendation carries serious weight. Participating in WhatsApp groups, attending gatherings, building reputation creates sustainable pipelines.

Skills and Tools

Digital Literacy

Basic smartphone skills suffice. Downloading apps, sending WhatsApp links, making calls, navigating interfaces. Platforms design for non-technical users large buttons, clear instructions, vernacular support.

Learning happens through practice. Each interaction teaches nuances. Partners report significant confidence after 10-15 successful applications. Early struggles with eligibility explanations become routine.

WhatsApp Business (free) adds professionalism. Automated greetings, quick replies for common questions, product catalogs, broadcast lists. "What documents for credit card?" gets instant response from saved replies.

Canva (free) handles promotional graphics. Simple designs for product launches, benefits, testimonials. Visual content gets 3-5x more engagement than text posts.

Communication

Financial products need education-based selling. Customers must understand how products work, what benefits they provide, why they fit specific needs. You're an advisor explaining, clarifying, guiding.

Active listening reveals needs. Home renovation mention suggests loan need. Investment interest indicates demat prospect. Denied bank application suggests digital lenders.

Objection handling: "I already have a credit card" → explain specific benefits of new card. "My credit score is low" → suggest improvement strategies and products accepting lower scores. "I'll apply directly" → clarify that your link costs nothing while earning you commission, plus free assistance.

Follow-up balances persistence and respect. Checking status, reminding about documents, sharing launches maintains engagement without annoying. Weekly "touching base" to active prospects, immediate inquiry responses creates rhythm.

Time Management

Part-time works. Two to three hours daily morning, evening, or weekends generates meaningful income. Partners earning while working full-time invest 10-15 hours weekly.

Batch processing improves efficiency. Dedicated blocks: 30 minutes sending links, 45 minutes following up, 20 minutes posting content. Reduces context-switching.

Calendar scheduling ensures consistency. Blocking specific times creates routine, prevents procrastination. Monday evenings for link sharing, Wednesday mornings for follow-ups, Saturday afternoons for training updates.

Goal setting: Monthly income targets (₹15,000, then ₹30,000, then ₹50,000) backed by activity metrics (applications, shares, calls). Weekly tracking shows momentum.

Scaling Up

Building Teams

Referral programs pay for recruiting partners. Someone joins using your code, you earn 10-20% of their acquisitions passive income.

Recruit people seeking supplementary income students, homemakers, retirees, part-time workers. Pitch: zero investment, flexible hours, training provided.

Support your team. Weekly calls sharing practices, forwarding high-performing messages, celebrating wins. Engaged teams persist longer, earn more.

Ten partners each earning ₹20,000 monthly generates ₹2,000-4,000 monthly passive income for you minimal ongoing effort.

Diversifying

Financial distribution pairs with related services. Tax filing assistance. Investment advisory (with certification). Bookkeeping for small businesses.

Content creation monetizes expertise. Tamil finance YouTube, financial literacy blog, Instagram education monetize through platform payments (YouTube AdSense) plus product recommendations.

Affiliate marketing expands beyond finance. Insurance comparison sites, course platforms, business services recommend what you use. Amazon Associates pays 3-8% on purchases through your links.

Local consulting leverages success. Teaching others zero-investment business startup, social media marketing for local businesses, digital literacy training.

Long-Term

Customer retention increases lifetime value. Someone you help get a credit card in 2026 might need a loan in 2027, demat account in 2028, business loan in 2030. Periodic check-ins create recurring revenue.

Reputation builds snowballs. Word-of-mouth, testimonials, network presence new customers seek you out.

Skill upgrades maintain advantage. Certifications (NISM, IRDAI if regulations change), industry webinars, advanced sales techniques.

Market expansion. Success in Coimbatore? Try Tiruppur or Pollachi. Strong with professionals? Develop strategies for self-employed or government employees.

How This Compares to Alternatives

Compare with gaming apps often scams promising unrealistic returns. Survey sites legitimate but low-income (₹2,000-5,000 monthly). Dropshipping zero inventory but heavy customer service demands.

Financial distribution: ₹40,000-100,000 monthly achievable in 6-12 months. Similar time investment (10-20 hours weekly). Dramatically higher hourly earnings.

Legitimacy: Platforms partner with RBI, SEBI, IRDAI-regulated institutions. Products legal, commissions legitimate, customers protected. Unlike unregulated gaming apps or crypto schemes.

Skill development: Understanding credit, loans, investments benefits your personal finances and builds transferable expertise. Gaming or surveys develop no marketable skills.

Realistic Timelines

Month 1: ₹3,000-8,000. Training complete, first products shared, first applications processed.

Months 2-3: ₹12,000-25,000. Process systematic, product-customer fit understood, referrals starting.

Months 4-6: ₹25,000-50,000. Network expanding, conversion improving, category strengths identified.

Month 12+: ₹60,000-100,000+ for top performers combining direct acquisitions and team overrides. Twenty to thirty hours weekly investment.

Common Problems

Document collection. Customers lack papers, send blurry photos, delay. Fix: Checklist messages with sample photos showing acceptable quality.

Application rejections. Banks reject for credit scores, documentation, eligibility. Fix: Pre-qualify with screening questions. Approval rates improve from 40-50% to 70-80%.

Income inconsistency. ₹40,000 one month, ₹18,000 the next. Fix: Emergency buffers during high months. Diversify products. Multiple income streams reduce dependence on single sources.

"I'll think about it." Fix: Ask clarifying questions. "What concern?" or "What information would help?" Uncover real objections.

7-Day Action Plan

Day 1: Download GroMo, register with PAN and bank details, explore dashboard. 30 minutes.

Day 2: Complete credit card and savings account training. Get certified. 2-3 hours.

Day 3: Identify 10 potential customers from your network. List names, products, reasons. 45 minutes.

Day 4: Share product links with 5 people via personalized WhatsApp messages. 1 hour.

Day 5: Follow up with yesterday's contacts. Share links with remaining 5 people. 1.5 hours.

Day 6: Complete loan and demat training. Research product-customer fit. 2 hours.

Day 7: Review the week links shared, conversations, applications. Set next week's goals. Join partner communities. 1 hour.

FAQ

Can I really start without investing money? Yes. Free app. Free training. Use your existing phone and internet. Marketing materials, tools, resources free. Commissions only on successful applications. Payouts directly to your bank. No hidden fees.

How much time for meaningful income? Partners earning ₹30,000-50,000 monthly invest 2-3 hours daily or 15-20 hours weekly. Sharing links, following up, training, social media. Flexible mornings, evenings, weekends. Even 1 hour daily generates ₹8,000-15,000 while building.

Do I need qualifications or sales experience? No. Platform training covers products, handling customers, compliance. Sales experience helps, but most successful partners had zero finance or sales background. Tamil communication, smartphone skills, willingness to learn matter more. Certification transforms beginners into advisors.

What if customers have problems after applying? Banks, lenders, platforms handle all post-sale service. Your responsibility ends at application assistance. No technical support, dispute resolution, complaint handling expected. Limited liability makes this practical without infrastructure.

Only major cities? No. Chennai, tier-2 cities, smaller towns same opportunity. Digital distribution needs only internet. Smaller cities actually offer advantages: less competition, lower living costs, strong community networks. Bangalore, Punjab, West Bengal proven pan-India.

Building trust when starting? Begin with family, friends, close colleagues who already trust you. Help genuinely solve needs while learning. Request testimonials and referrals. Share certification credentials. Post educational content. After 8-10 successful cases, reputation grows organically.