Low-Cost Franchises vs GroMo: No-Invest Income in India 2026

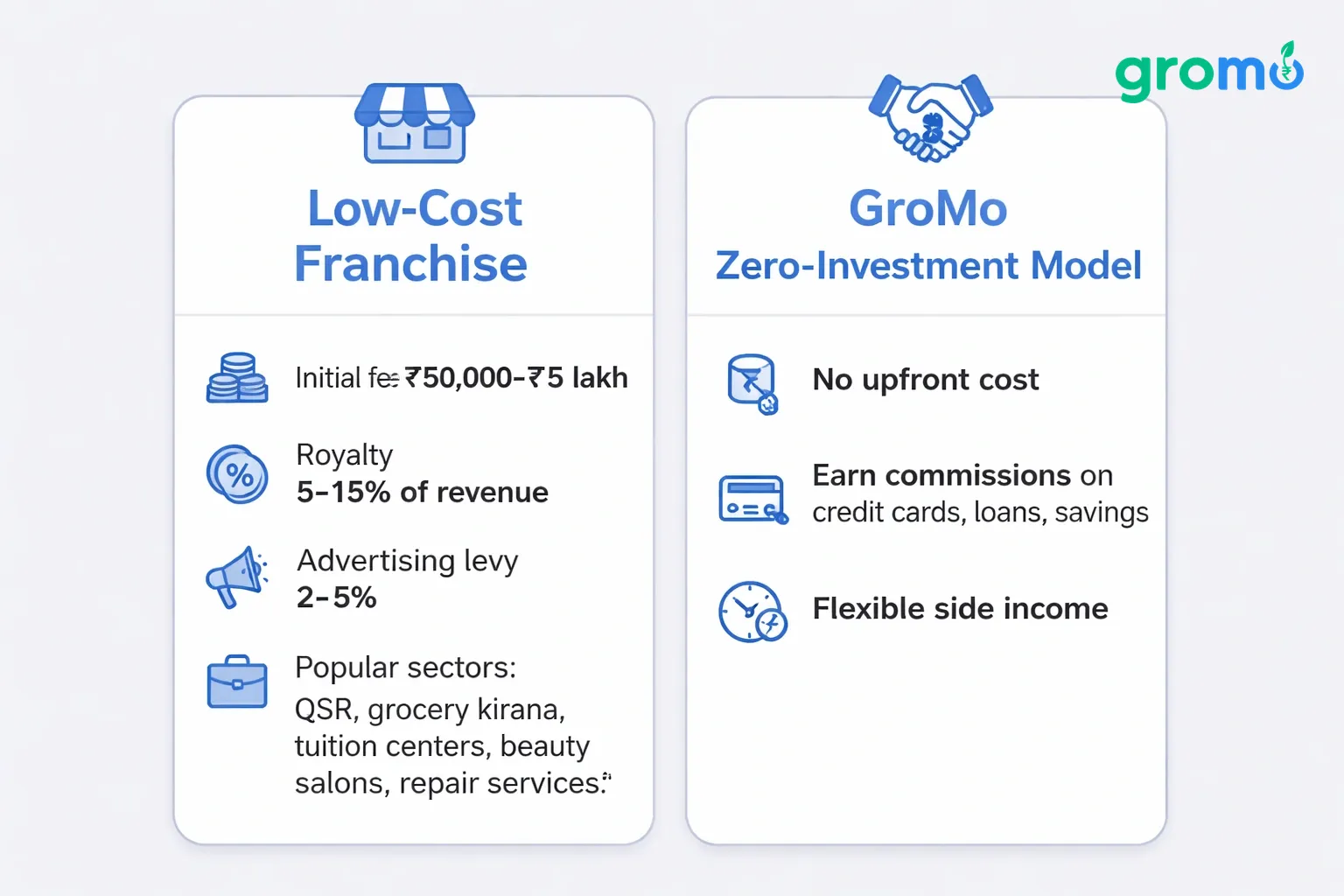

Low-cost franchises in India let you start a branded business for ₹50,000 to ₹5 lakh, covering food, retail, education, or services. They offer brand recognition, training, and operational support but charge royalties (5–15% of revenue), restrict autonomy, and rarely guarantee foot traffic or profitability in the first year.

Traditional franchises demand rent, inventory, staff, and fixed overheads that can drain ₹30,000 to ₹2 lakh monthly before you see profit. In contrast, zero-investment digital platforms like GroMo eliminate upfront capital, letting you earn commissions on credit cards, loans, savings accounts, and demat products from day one. This guide compares 10 popular low-cost franchise models with commission-based financial distribution, shows real payout structures, and explains why 60 lakh+ Indians now choose GroMo to build sustainable side income.

What Is a Low-Cost Franchise in India?

A low-cost franchise is a license to operate under an established brand for an initial fee between ₹50,000 and ₹5 lakh. The franchisor supplies business processes, trademarks, marketing collateral, and training; you pay setup costs plus ongoing royalty (5–15% of gross revenue) and often an advertising levy (2–5%). Popular sectors include quick-service restaurants (QSR), grocery kirana stores, tuition centers, beauty salons, and repair services.

Why entrepreneurs consider franchises:

• Brand equity – Customers trust recognized names, shortening your sales cycle.

• Proven systems – Operations manuals reduce trial-and-error.

• Bulk purchasing – Central procurement lowers product costs.

• Training – Many franchisors offer week-long bootcamps for you and staff.

Hidden costs that inflate budgets:

• Security deposit – ₹1 to ₹3 lakh, refunded after contract end.

• Rent advance – Three to six months' rent upfront, averaging ₹1.5 lakh in Tier 2 cities.

• Interior & equipment – Signage, furniture, POS systems: ₹1.5 to ₹4 lakh.

• Initial inventory – Two to four weeks' stock: ₹50,000 to ₹2 lakh depending on category.

• Staff salaries – Two employees at ₹12,000 each equals ₹24,000 monthly before first sale.

Even a "₹2 lakh franchise" often requires ₹5 to ₹7 lakh working capital when you add these expenses, making the label misleading.

10 Popular Low-Cost Franchise Categories in 2026

1. Food & Beverage (QSR)

Examples: Chaayos (tea café), Faasos (cloud kitchen), Amul (ice cream parlor).

Investment range: ₹5 to ₹15 lakh (excluding rent).

Royalty: 6–10%.

Space: 200–500 sq ft.

Breakeven: 12–24 months if daily footfall exceeds 80 customers and average ticket is ₹120+.

Pros: High repeat business, emotional product (food).

Cons: Perishable inventory, strict hygiene audits, high attrition among kitchen staff, local competition from street vendors who undercut by 40%.

2. Grocery & FMCG Retail

Examples: More Retail (mini-supermarket), Nilgiris, Spar Express.

Investment range: ₹3 to ₹10 lakh.

Royalty: 2–5% plus central billing margin.

Space: 300–800 sq ft.

Breakeven: 18–30 months; margins are 8–12% gross, shrinking to 3–5% net after rent and wages.

Pros: Essential goods ensure steady demand.

Cons: Online grocery apps (Blinkit, Zepto) offer 10-minute delivery, eroding walk-in traffic. Inventory management requires daily stock reconciliation.

3. Education & Tutoring

Examples: Kumon (math & reading), Smartkidz (preschool), British Lingua (English).

Investment range: ₹2 to ₹8 lakh.

Royalty: 10–15%.

Space: 500–1,500 sq ft for classrooms.

Breakeven: 12–18 months if you enroll 40+ students at ₹3,000 per month average fee.

Pros: Recurring monthly fees, limited perishability, parental willingness to invest in education.

Cons: Seasonal enrollment (April, June), teacher recruitment challenges, competition from free YouTube content and edtech apps.

4. Beauty & Wellness

Examples: Naturals (salon), VLCC (wellness center), Looks (unisex salon).

Investment range: ₹4 to ₹12 lakh.

Royalty: 5–8%.

Space: 300–600 sq ft.

Breakeven: 12–18 months with 15–20 daily walk-ins.

Pros: Premium pricing, upsell opportunities (facials, packages).

Cons: Skilled beauticians demand ₹15,000+ salaries, hygiene compliance, customer retention depends on individual staff rapport.

5. Pharma & Healthcare

Examples: Apollo Pharmacy (generic + OTC), MedPlus.

Investment range: ₹8 to ₹20 lakh (includes licensed pharmacist salary).

Royalty: 1–3% (low margin sector).

Space: 200–400 sq ft.

Breakeven: 24–36 months; gross margins 15–20%, net 3–5% after rent and compliance costs.

Pros: Evergreen demand, insurance tie-ups (CGHS, ESI) bring bulk orders.

Cons: Strict drug licensing, expiry-date inventory risk, online pharmacies offering 20% discounts erode foot traffic.

6. Mobile & Electronics Repair

Examples: iCare (Apple service), Poorvika Mobile Care.

Investment range: ₹2 to ₹6 lakh.

Royalty: 5–10%.

Space: 150–300 sq ft kiosk.

Breakeven: 10–15 months if daily repairs exceed 8 devices at ₹500 average bill.

Pros: High margins (40–60% on parts), repeat business for screen cracks and battery swaps.

Cons: Rapid tech obsolescence, customers compare prices on Amazon/Flipkart, warranty fraud risks.

7. Laundry & Dry Cleaning

Examples: FabIndia Laundry, UClean.

Investment range: ₹3 to ₹10 lakh.

Royalty: 6–8%.

Space: 200–400 sq ft pickup point + off-site plant (optional).

Breakeven: 12–18 months with 100 kg daily volume at ₹60 per kg.

Pros: Subscription models ensure predictable revenue; margins 25–35%.

Cons: Stain disputes, machinery downtime costs ₹10,000+ per incident, urban water shortages increase operating costs.

8. Fitness & Gym

Examples: Gold's Gym Express, Snap Fitness.

Investment range: ₹10 to ₹25 lakh.

Royalty: 8–12%.

Space: 1,000–2,500 sq ft.

Breakeven: 18–30 months if membership crosses 150 paying clients at ₹1,500 average monthly fee.

Pros: Recurring membership revenue, upsell opportunities (personal training, supplements).

Cons: Equipment maintenance (₹30,000 quarterly), trainer attrition, January surge followed by 40% drop-off by March.

9. Home Services (Plumbing, Pest Control)

Examples: Urban Company Franchise (hypothetical), HiCare (pest control).

Investment range: ₹1 to ₹5 lakh.

Royalty: 10–15%.

Space: Virtual office; technicians work on-site.

Breakeven: 8–12 months with 50 monthly bookings at ₹1,200 average.

Pros: Low fixed overhead, on-demand business model, digital lead generation via app.

Cons: Technician reliability issues, customer expects franchisor-level service but you own liability, commission split leaves thin margin.

10. Automobile Care

Examples: 3M Car Care, GoMechanic (if franchising resumes).

Investment range: ₹5 to ₹15 lakh.

Royalty: 5–10%.

Space: 500–1,500 sq ft garage.

Breakeven: 15–24 months with 10 vehicles daily at ₹1,500 average billing.

Pros: Growing vehicle ownership (33 million new registrations in 2025), high-value services (ceramic coating, PPF).

Cons: Real-estate costs in accessible locations, trained mechanics scarce, warranty disputes with customers.

Real Costs of Running a Franchise vs. Zero-Investment Digital Platforms

| Expense Head | Low-Cost Franchise (Annual) | GroMo (Annual) |

|---|---|---|

| Franchise / Setup Fee | ₹2,00,000 – ₹5,00,000 | ₹0 |

| Rent (12 months) | ₹1,80,000 – ₹6,00,000 | ₹0 |

| Staff Salaries | ₹2,88,000 (2 staff) | ₹0 (you work solo) |

| Inventory / Stock | ₹50,000 – ₹2,00,000 | ₹0 |

| Utilities & Maintenance | ₹60,000 | Internet ≈ ₹6,000 |

| Royalty (8% of ₹12L) | ₹96,000 | ₹0 |

| Marketing Levy (3%) | ₹36,000 | ₹0 |

| Total | ₹8,10,000 – ₹16,80,000 | ₹6,000 |

Even if a franchise generates ₹12 lakh annual revenue at 20% net margin, you pocket ₹2.4 lakh barely covering your first-year investment. GroMo partners earning ₹2,400 per approved Axis Flipkart credit card only need 10 approvals monthly (₹24,000) to match that net profit, with zero overhead. Read how financial product distribution works to compare models side by side.

Why Zero-Investment Financial Distribution Beats Franchise Economics

No Capital Risk or Debt Trap

Franchise loans at 12–16% interest compound; missing EMIs triggers personal-guarantee enforcement. GroMo requires zero borrowing your smartphone and data plan (₹500/month) are your only tools. Partners in West Bengal and Punjab start same day without bank visits.

Instant Payouts vs. 60–90 Day Cycles

Franchise royalties and supplier payments lock cash for months. GroMo credits commissions within 24–72 hours of customer approval: ₹250–₹400 for Upstox demat accounts, ₹2,000–₹3,000 for Axis credit cards, ₹700–₹1,200 for Kotak 811 savings accounts, and 0.5–3% for business loans. Check the Upstox Demat payout structure for full details.

Scalability Without Hiring or Rent

A single franchise outlet caps daily transactions by space and staff hours. GroMo lets you share product links to 50 WhatsApp contacts in 10 minutes; each approved application pays you. Housewives in Tamil Nadu earn ₹15,000–₹50,000 monthly from home, and professionals in Mumbai layer GroMo income atop 9-to-6 jobs without office leases.

Zero Inventory, Zero Perishability

Franchises write off expired stock, damaged goods, and pilferage losses that eat 3–8% of revenue. Financial products never spoil. A credit card link sent in January converts in March, and you still earn full commission. Learn how to earn ₹1,000 daily by focusing on high-payout products.

No Territory Restrictions or Non-Compete Clauses

Franchise agreements bind you to a 3–5 km radius and forbid opening competing outlets. GroMo imposes zero geographic limits sell to customers in Kerala while living in Delhi, or target NRI families abroad. Your earning ceiling is effort and network size, not franchisor rules.

Free Training & Certification

Franchisors charge ₹20,000–₹50,000 for week-long training that teaches POS operation and brand guidelines. GroMo Academy offers free video modules on credit scoring, loan eligibility, KYC compliance, and objection handling skills that increase your conversion rate without tuition fees. Discover part-time income strategies that fit around existing commitments.

How to Earn ₹50,000+ Monthly with GroMo (Step-by-Step)

Step 1: Download & Onboard (5 Minutes)

Install GroMo from Play Store or App Store, enter mobile number, verify OTP, complete IRDAI certification quiz (15 questions, open-book), and activate your partner dashboard. No documents, no fees, no approval delay.

Step 2: Choose High-Payout Products

Focus on:

• Axis Flipkart Credit Card – ₹2,000–₹3,000 per approval; targets shoppers with ₹40,000+ monthly income.

• Kotak 811 Savings Account – ₹700–₹1,200; appeals to students and first-jobbers needing zero-balance accounts.

• Upstox Demat – ₹250–₹400; investors wanting free AMC for one year.

• Poonawalla Fincorp Business Loan – 1.75–3% of disbursed amount; MSME owners with Udyam registration.

Prioritize products matching your audience's income bracket and immediate needs.

Step 3: Build a Qualified Lead List

Identify 100 contacts who:

• Earn salary or run businesses (eliminates students without income for loans).

• Are 21–55 years old (matches product eligibility).

• Have Aadhaar-linked mobile and PAN (mandatory for KYC).

Segment by need: credit card seekers, first-time investors, business owners needing working capital.

Step 4: Personalize Your Pitch

Never spam generic links. Message:

"Hi [Name], noticed you shop online often Axis Flipkart card gives 5% cashback on every Flipkart purchase, capped ₹4,000 per quarter. Lifetime free if you spend ₹3.5L annually. Shall I share the 3-minute application link?"

Personalization lifts response rates from 8% to 35% because recipients see immediate value, not sales noise.

Step 5: Guide Customers Through KYC

Common drop-off points:

• VKYC call – Customer must answer live video call; remind them to keep PAN card, good lighting, and stable Wi-Fi ready.

• E-mandate setup – For loans, explain that auto-debit authorization isn't a charge today it's future EMI convenience.

• Income proof – Self-employed applicants upload GST returns or bank statements; help them locate PDFs in email or DigiLocker.

A single reminder WhatsApp message "Complete your KYC in next 2 hours to get instant approval" recovers 40% of abandoned applications.

Step 6: Follow Up & Track Status

GroMo dashboard shows "Pending KYC," "Approved," "Rejected." Call customers stuck at "Pending" within 24 hours:

"Hi, your Kotak 811 account is 90% done just video KYC left. Can we schedule it now? Takes 3 minutes."

Persistence converts fence-sitters. Top partners follow up three times over one week before marking a lead cold.

Step 7: Reinvest Time, Not Money

Unlike franchises requiring ₹50,000 inventory top-ups, GroMo profits reinvest as time. Spend two extra hours daily reaching 20 new leads. Month one: 10 approvals × ₹1,500 average = ₹15,000. Month two: 20 approvals × ₹1,800 = ₹36,000. Month three: 35 approvals × ₹2,000 = ₹70,000. Geometric growth costs zero capital.

Case Studies: Real Franchise vs. GroMo Outcomes

Franchise Example: Chaayos Tea Café (Tier 2 City)

Investment: ₹8 lakh (franchise fee ₹2L, interior ₹3L, deposit ₹1.5L, working capital ₹1.5L).

Monthly revenue: ₹2.5 lakh (80 customers/day × ₹100 average).

Gross margin: 60% = ₹1.5 lakh.

Expenses: Rent ₹40,000, staff ₹36,000 (3 people), royalty ₹20,000 (8%), utilities ₹10,000.

Net profit: ₹44,000/month.

Breakeven: 18 months (₹8L ÷ ₹44,000).

Owner works 70 hours/week managing inventory, staff rosters, and customer complaints. After 18 months of 9 AM–11 PM shifts, she earns ₹44,000 less than a ₹50,000 salaried job with weekends off.

GroMo Example: IT Professional in Bangalore

Investment: ₹0.

Time commitment: 10 hours/week (evenings + weekends).

Month 1: 12 credit card approvals (friends, colleagues) = ₹24,000.

Month 3: Added 8 demat accounts, 5 savings accounts = ₹38,000.

Month 6: Referral team of 4 sub-partners contributes override commission = ₹52,000 total.

Breakeven: Immediate (no sunk cost).

He layers GroMo income onto ₹80,000 salary, reaching ₹1.32 lakh combined monthly by month six without quitting his job or touching savings. Read more Bangalore strategies.

Franchise Example: Looks Salon (Metro Suburbs)

Investment: ₹12 lakh (franchise ₹3L, equipment ₹5L, deposit ₹2L, working capital ₹2L).

Monthly revenue: ₹3 lakh (15 walk-ins/day × ₹650 average).

Gross margin: 50% = ₹1.5 lakh.

Expenses: Rent ₹60,000, staff ₹50,000 (2 beauticians + helper), royalty ₹18,000 (6%), products ₹15,000.

Net profit: ₹7,000/month.

Breakeven: Never reached closed after 14 months when lease-renewal hike to ₹80,000 made model unviable.

Owner lost ₹12 lakh investment plus 14 months' effort, now exploring zero-investment alternatives.

GroMo Example: Housewife in Tamil Nadu

Investment: ₹0.

Time commitment: 6 hours/week (post-lunch, after kids' homework).

Month 1: 5 savings accounts (relatives, housing-society neighbors) = ₹5,000.

Month 4: 3 credit cards, 2 business loans (local shop owners) = ₹18,000.

Month 8: Built 10-member referral network; override income ₹12,000 + direct sales ₹20,000 = ₹32,000.

She contributes one-third of household expenses without leaving home or hiring help. See housewife income blueprints.

Common Misconceptions About Franchises vs. Digital Platforms

"Franchises Offer Guaranteed Foot Traffic"

Brand recognition attracts initial curiosity, but sustaining traffic requires your hyperlocal marketing flyer distribution, Google My Business optimization, Instagram reels. Franchisors rarely fund local ads after launch month. GroMo's "foot traffic" is your existing WhatsApp network and warm leads from community groups people who already trust you.

"Commission Work Is Unpredictable Income"

Franchises face seasonality (ice-cream sales drop 60% in monsoon), economic downturns (gym memberships canceled first in recessions), and location risks (road construction cuts walk-ins by half). GroMo income scales with effort 20 leads contacted yield 4–7 approvals consistently across months because financial products (credit, savings, investment) have evergreen demand. Track your daily earning potential.

"You Need Sales Experience for GroMo"

Franchises assume you'll learn operations by doing; many fail because owners lack retail instincts. GroMo provides scripts, objection-handling videos, and 24/7 partner support chat. First-timers earn their first ₹10,000 within 30 days by following step-by-step checklists.

"Franchises Build Sellable Assets"

A franchise license is non-transferable or sells at 40% discount because buyer inherits your location risk and remaining contract term. GroMo referral networks where sub-partners you recruit earn you override commissions compound indefinitely without expiry. Your "asset" is your trained downline, which grows monthly.

Legal & Tax Considerations for Both Models

Franchise Compliance

• GST registration mandatory if turnover exceeds ₹40 lakh (₹20 lakh in special-category states).

• Trade license from municipal corporation: ₹5,000–₹15,000 annually.

• FSSAI license for food franchises: ₹2,000 (basic) to ₹25,000 (state).

• Shop & Establishment Act registration: ₹3,000–₹10,000.

• Income tax on net profit under "Business Income" head; advance tax if liability >₹10,000.

Total compliance burden: ₹15,000–₹50,000 yearly plus CA fees ₹20,000–₹40,000 for filing.

GroMo Compliance

• GST: Optional if commission income <₹40 lakh; most partners stay under threshold.

• Income tax: Declare under "Income from Other Sources" or "Business Income" if systematic; standard deduction available.

• No trade license, FSSAI, or physical-space registrations required.

GroMo auto-generates TDS certificates (if applicable) and annual earning statements for ITR filing, cutting CA dependency. Your compliance cost: ₹2,000–₹5,000 for basic ITR filing.

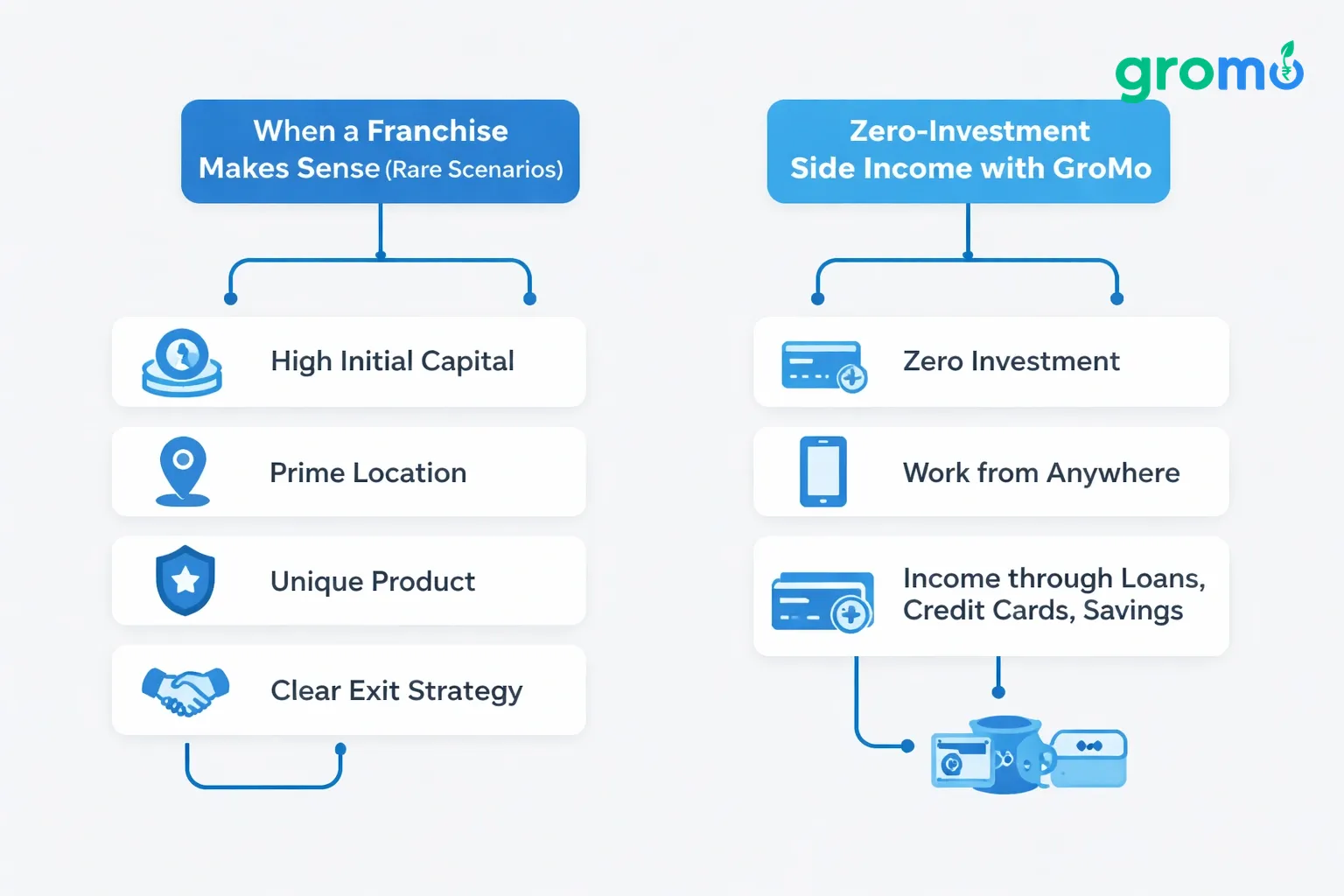

When a Franchise Makes Sense (Rare Scenarios)

Choose franchises if:

- You have ₹10+ lakh idle capital and prefer tangible business ownership over digital income.

- Location guarantees captive audience (hospital canteen franchise, railway-station kiosk, airport lounge).

- Product is non-replicable (patented tech, exclusive import rights).

- Exit strategy exists (franchisor buyback clause at 80% of investment after 3 years).

- You want full-time entrepreneurship identity for visa applications, business loans, or social validation.

For everyone else salaried professionals, students, homemakers, retirees zero-investment side income via GroMo delivers faster breakeven, lower stress, and higher hourly ROI.

How to Transition from Franchise Research to GroMo Execution

Week 1: Audit Your Network

List 50 people across three tiers:

• Tier 1 (20 people): Close family, college friends, current colleagues 90% response rate.

• Tier 2 (20 people): Extended relatives, ex-colleagues, gym buddies 60% response rate.

• Tier 3 (10 people): LinkedIn connections, society members, parents at kids' school 30% response rate.

Tag each by likely need: "credit card," "first savings account," "business loan," "demat."

Week 2: Complete Product Training

Watch GroMo Academy modules:

• "Axis Credit Card Eligibility & Pitch" (12 min).

• "Kotak 811 KYC Walkthrough" (8 min).

• "Upstox Objection Handling" (15 min).

• "Business Loan Document Checklist" (10 min).

Take notes on common customer questions and approved rebuttals.

Week 3: First 10 Conversations

Message Tier 1 contacts:

"Hi! Started partnering with banks to help friends get best credit cards / savings accounts. You mentioned wanting a demat account last month shall I share a link that opens it free in 5 minutes?"

Track responses in a Google Sheet: Name, Product Interest, Link Sent (Y/N), KYC Status, Approval Date, Payout.

Week 4: Optimize & Scale

Review conversion funnel:

• Contacted 20, link sent to 15, KYC started by 10, approved 6 → 30% close rate.

• Identify drop-off stage if 10 started KYC but only 6 completed, your follow-up timing needs tightening.

Add 20 Tier 2 contacts. Repeat. By month-end, 15 approvals × ₹1,800 average = ₹27,000 earned with zero capital deployed. Compare that to waiting 18 months for franchise breakeven.

GroMo Product Portfolio: Diversify Your Commission Streams

| Product Category | Top Offers | Payout Range | Ideal Customer |

|---|---|---|---|

| Credit Cards | Axis Flipkart, HDFC Millennia | ₹2,000–₹3,000 | Online shoppers, 25–40, ₹40K+ income |

| Savings Accounts | Kotak 811, Fi Money (Federal Bank) | ₹700–₹1,200 | Students, first jobbers, zero-balance seekers |

| Demat Accounts | Upstox, AngelOne, Indiabulls Securities | ₹250–₹500 | First-time investors, SIP starters |

| Personal Loans | Fibe (₹5L max), PaySense (₹3L max) | 1–2% of disbursed | Salaried, 23–50, ₹25K+ monthly income |

| Business Loans | Poonawalla Fincorp, ClickPe-Muthoot | 1.75–3% of disbursed | MSME owners with GST/Udyam, 2+ years operation |

| Credit Lines | FatakPay, HDFC Smart EMI | 0.5–1% | Existing cardholders needing emergency liquidity |

Diversification smooths income volatility. If credit-card demand dips in January (post-holiday spending fatigue), pivot to tax-saving investment products (demat accounts for ELSS funds) peaking in February–March.

Long-Term Wealth Building: Franchise Equity vs. GroMo Network Effects

Franchise Equity Illusion

After 5 years, your franchise "valuation" depends on:

• Remaining contract term – 10 years left is attractive; 2 years isn't.

• Location lease transferability – If landlord refuses new tenant, asset worthless.

• Brand health – Franchisor bankruptcy or scandal craters resale value overnight.

Typical resale recovers 40–60% of invested capital, and finding buyers takes 6–12 months.

GroMo Network Compounding

Your referral downline partners you recruit earns you override commissions indefinitely:

• Recruit 10 active partners.

• Each closes 10 deals monthly averaging ₹1,500 commission.

• Your 5% override = ₹750 per partner = ₹7,500 passive monthly income.

• If each of your 10 recruits another 5 sub-partners (50 second-tier), your passive income scales to ₹18,750 monthly without personal sales effort.

This geometric growth mirrors multi-level marketing structure but without inventory purchases or mandatory quotas, making it sustainable and ethical. Learn referral income mechanics.

FAQs: Navigating Low-Cost Franchises in India 2026

Q: Can I negotiate lower franchise fees or royalty percentages?

A: Established brands (Chaayos, Naturals, Amul) set standard terms non-negotiable for individual franchisees to maintain system uniformity. Only if you commit to multi-unit (3+ outlets) might they offer 1–2% royalty discount. Emerging brands with <50 10 outlets may waive setup fees for first franchisees but that signals untested model risk.< p>

Q: Do franchise agreements include territory protection?

A: Most grant "preferred area" within 3–5 km radius but reserve the right to open company-owned outlets or award franchises to others if you underperform (revenue <70% 8 of target for two consecutive quarters). read section ("territory & exclusivity") carefully; if it says "non-exclusive," expect competition from the same brand.< p>

Q: What happens if I want to exit a franchise early?

A: Standard 5-year contracts penalize early termination: forfeit security deposit (₹1–₹3 lakh), pay liquidated damages (3–6 months' average royalty), and sign non-compete preventing you from opening similar business within 10 km for 2 years. Pre-plan exit strategy before signing.

Q: How quickly can I start earning with GroMo compared to opening a franchise?

A: Franchise timeline: 3–6 months (site selection, interior build-out, staff hiring, inventory stocking, soft launch). First profit: month 8–12. GroMo timeline: Day 1 (download app, share link). First commission: 2–7 days (customer approval + payout processing). Proven strategies show ₹10,000 earned within first 30 days.

Q: Are GroMo commissions taxable, and do I need GST registration?

A: Yes, commissions are taxable under "Income from Other Sources" or "Business Income" if systematic. GST registration mandatory only if annual commission exceeds ₹40 lakh (₹20 lakh in special states). Most partners earn ₹3–₹8 lakh annually, staying below threshold. GroMo issues Form 16A if TDS deducted; use it for ITR filing. Consult a CA for personalized advice.

Q: Can I run a franchise and GroMo simultaneously?

A: Legally yes, but time constraints make it impractical. Franchises demand 60+ hours/week on-site presence; GroMo fits into 10–15 flexible hours. If you already own a franchise, use GroMo to monetize downtime (slow afternoons) by offering financial products to walk-in customers. For example, a salon owner can pitch Axis credit cards to clients during 20-minute blow-dry waits, earning ₹2,400 per approval as bonus revenue atop salon service fees. Explore digital distribution strategies for hybrid models.