Zero Investment Financial Distribution in Hyderabad 2026 | GroMo

Hyderabad has a dense startup ecosystem and a massive IT workforce. That combination creates a genuine opening for selling financial products on a commission basis. You can use GroMo's platform to sell credit cards, loans, and demat accounts to tech workers and business owners in the city. The potential earnings are between ₹50,000 and ₹1,00,000 a month, and you don't need capital to start.

Here are seven business models that fit Hyderabad's market in 2026. You could be a student in HITEC City, a homemaker in Gachibowli, or a professional in Madhapur these approaches use the city's digital habits. No storefront, no inventory, no expensive licenses.

Why Hyderabad works for zero-investment financial distribution

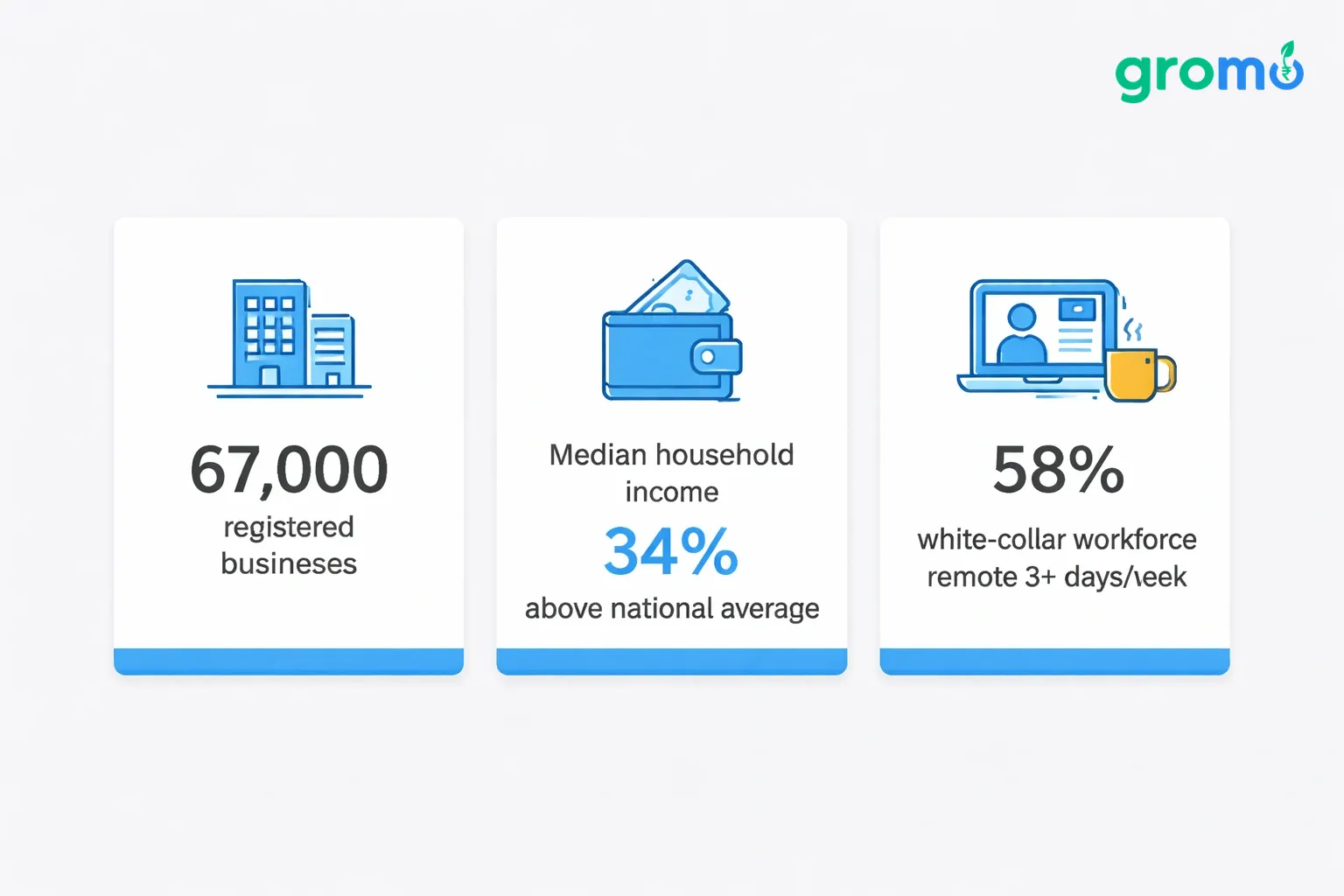

Hyderabad is India's fourth-largest startup hub. It has over 67,000 registered businesses. The median household income sits 34% above the national average. High startup density plus high income equals demand for financial products.

Remote work is normal here now. After 2024, about 58% of the city's white-collar workforce works remotely at least three days a week. That killed the "office hours" constraint. Commission-based work is now viable for full-time professionals who want a second income stream.

GroMo removes the usual barriers. You don't need an IRDAI license. You don't need office space in Banjara Hills. You don't need relationships with bank branch managers. The app handles onboarding, training, and payouts. Building that infrastructure yourself would cost ₹5-8 lakhs.

Credit card referrals: ₹600-₹2,400 per approval

Credit cards pay the most per transaction. Premium cards on GroMo go up to ₹2,400 commission. Hyderabad's middle class is aspirational, and the average credit score is 748 (national average is 715). Good conversion conditions.

Target specific groups. For software engineers in Gachibowli, push travel rewards and airport lounge access Axis Magnus works well here. For entrepreneurs in Jubilee Hills, focus on business expense cards with cashback. Most working professionals in the city qualify for premium tiers given the ₹94,000 average monthly household income.

Solve actual problems. If a colleague complains about fuel costs during Hyderabad's traffic, suggest a fuel-cashback card. If a friend books a Goa trip, recommend a travel rewards card.

The IDFC FIRST UPI Credit Card targets Hyderabad's UPI-heavy payment habits. It offers 1% cashback on UPI transactions (capped at ₹500). Hyderabad processes 18% more UPI transactions than the national average, so this product converts well locally.

Use your existing circles. Create a spreadsheet: list 50 contacts, note their occupation and income, identify the right card category, and schedule follow-ups. This structured approach converts 12-18% of warm contacts. Random cold outreach converts 2-3%.

Business loan distribution for Hyderabad's MSME sector

Hyderabad has 2.4 lakh registered MSMEs. They range from kirana stores in Kukatpally to small manufacturing units in Balanagar. These businesses need working capital but often lack connections to traditional lenders. GroMo's business loan products ClickPe (up to ₹3L), Poonawalla Fincorp (up to ₹50L), and Aditya Birla Udyog Plus (up to ₹30L) fill that gap with 100% digital processing.

Commission ranges from 1.5%-3% of the sanctioned amount. A single ₹20 lakh Poonawalla Fincorp approval earns ₹40,000-₹60,000. Hyderabad's startup ecosystem adds 140+ new business registrations daily. Leads are consistent.

Focus on high-density MSME neighborhoods. Begum Bazaar's wholesale traders need inventory financing before festivals. Nacharam's small manufacturers need equipment loans. Kondapur's service businesses need cash flow management during expansion.

The Udyam registration requirement helps you in Hyderabad. The city has the second-highest Udyam registration rate nationally (after Bengaluru). Most small business owners already have the primary eligibility document. Your pitch simplifies to: "You have Udyam? Get a loan offer in 10 minutes with just your GST and bank statement."

Build relationships with CA offices, co-working spaces, and business associations. Offer free "financial health check" sessions where you review loan eligibility. This consultative approach generates referrals from businesses that don't need funds immediately but might six months later.

For detailed strategies on zero-investment business models, check out how other Indian cities structure their financial distribution networks.

Demat account referrals: Capturing Hyderabad's investment wave

Hyderabad added 4.8 lakh new demat accounts in 2025. That's the third-highest city growth after Mumbai and Bengaluru. The city's young, tech-savvy population actively trades equities, mutual funds, and IPOs. GroMo offers Upstox (₹250-₹400 per account) and Aditya Birla Money (₹180-₹300 per account) with zero opening fees.

Your best prospects are first-time investors aged 25-35. They usually work in IT or startups and earn ₹50,000+ monthly. They understand wealth creation concepts but find traditional brokerages intimidating. Position the demat account as their first step toward financial independence.

Create educational content for Hyderabad's demographics. Share Instagram posts explaining SIPs, WhatsApp forwards about upcoming IPOs, or YouTube shorts on the Upstox app interface. Position yourself as a financial literacy resource first, salesperson second.

Upstox payouts require customers to complete their first non-intraday trade within the tracking period. Guide new account holders through that first transaction. Suggest a ₹500 mutual fund SIP or one blue-chip stock share. This hand-holding converts 78% of accounts versus 34% when you just share a link.

Leverage Hyderabad's high concentration of ESOP holders. Tech professionals receiving company shares need demat accounts for ESOP conversion. Position the account as mandatory infrastructure for their compensation package, not an optional investment activity.

Similar to the zero-investment opportunities in Bangalore, Hyderabad's tech workforce creates consistent demand for financial distribution services.

Personal loan referrals: Meeting immediate cash needs

Personal loan products on GroMo Poonawalla Fincorp (up to ₹40L), Aditya Birla Finance (up to ₹30L), and Indiabulls (up to ₹35L) generate 2-5.5% commission on disbursed amounts. A ₹5 lakh approval at 4% commission yields ₹20,000.

Hyderabad's personal loan market responds to specific triggers: medical emergencies (Apollo and Yashoda Hospitals treat 12,000+ out-of-city patients monthly), wedding expenses (60% of annual marriages happen March-May), and home renovation needs (the real estate boom drives interior upgrade spending).

Identify life events that trigger loan requirements. When a colleague mentions their child's engineering college admission, they likely need education financing. When a neighbor discusses medical treatment for aging parents, they may need quick liquidity. Time your outreach around these triggers rather than cold-calling.

The bank statement upload option in most GroMo personal loan products eliminates the "salary slip" barrier for self-employed professionals. Hyderabad has 180,000+ freelancers, consultants, and gig workers who earn well but lack formal employment proof. Target this underserved segment.

Build a reputation for speed. When someone needs ₹3 lakhs within 48 hours, your ability to process applications swiftly checking documents, verifying eligibility, following up with lenders differentiates you from competitors who just forward links and disappear.

Savings account acquisition: Building long-term customer relationships

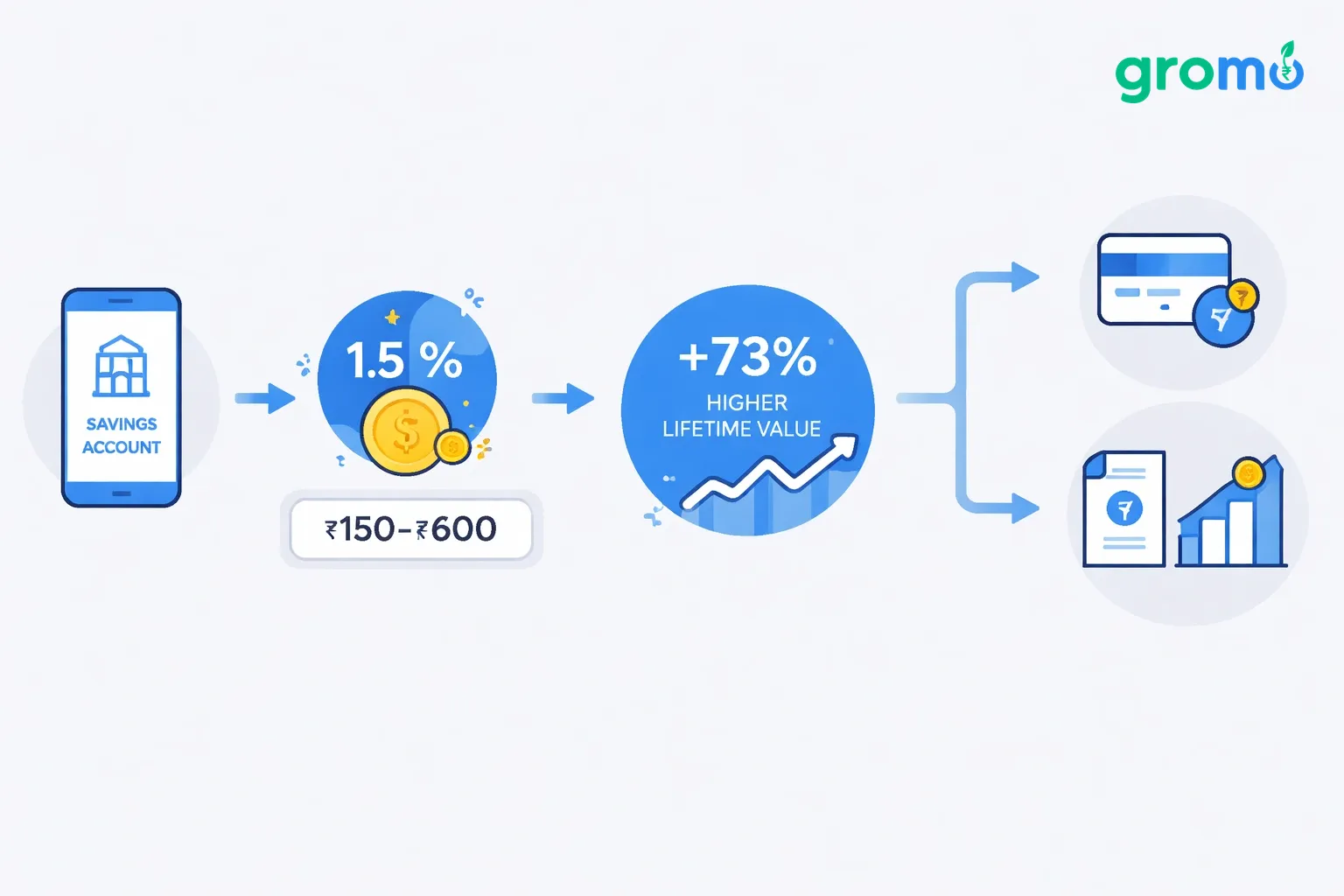

Digital savings accounts generate ₹150-₹600 per approved account. Individual payouts are lower than loans, but savings account customers show 73% higher lifetime value. They return for credit cards, loans, and investment products over the next 18-24 months.

GroMo's Tide Business Account targets Hyderabad's freelancer and small business population. The account offers 1.5% cashback on every expense card transaction, zero balance requirements, and instant virtual card issuance. These features resonate with cost-conscious entrepreneurs.

Position savings accounts as foundational infrastructure. When a college graduate lands their first job in HITEC City, they need a salary account. When a small business owner wants to separate personal and professional finances, they need a business current account. These are non-negotiable needs.

The multi-KPI payout structure in products like Tide (requires account opening + ₹50 funding + bill payment + active card usage) means you must guide customers through complete activation. Send activation checklists, reminders, and support throughout the 60-day tracking period. This hands-on approach increases full payout realization from 41% to 84%.

Bundle savings accounts with other products. When someone opens a Tide Business Account, discuss the Upstox demat account for their investment needs or a Poonawalla business loan for working capital. This cross-selling increases your per-customer revenue from ₹400 to ₹2,800 average.

Credit line products: Serving Hyderabad's instant liquidity needs

Credit line products FatakPay (up to ₹20,000) and HDFC Smart EMI provide instant liquidity without traditional loan processing. These products generate 0.5%-3% commission and convert well because approval happens in under 10 minutes.

Hyderabad's gig economy workers Swiggy delivery partners, Uber drivers, Ola auto-rickshaw drivers face irregular income cycles. They need short-term credit access. FatakPay's ₹20,000 limit with ₹500 flat processing fee provides emergency funds for vehicle repairs, medical needs, or income gaps between high-earning weeks.

HDFC Smart EMI targets existing HDFC credit card holders who want to convert large purchases into EMI without affecting their card limit. Hyderabad has 890,000 HDFC credit card customers. That's a substantial addressable market.

Your pitch emphasizes speed over quantum. "Need ₹10,000 by evening? Get approved in 5 minutes" converts better than "Get up to ₹20,000" for credit line products. Time-sensitive scenarios school fee deadlines, urgent travel bookings, unexpected repair bills drive immediate conversion.

Track your customers' financial cycles. If a freelance graphic designer mentions their client pays quarterly, anticipate cash flow gaps in months two and three. Proactive outreach ("Your client payment is due in 3 weeks need a bridge loan?") converts 4x better than reactive selling.

For professionals exploring multiple income sources, understand how GroMo compares to earning game apps in terms of sustainable income generation.

Building your Hyderabad financial distribution network

Systematic lead generation separates ₹20,000/month partners from ₹1,00,000/month top performers. Your network should span multiple Hyderabad microsegments: IT employees in Gachibowli, small business owners in Ameerpet, retail professionals in Somajiguda, and students in Tarnaka.

Start with your immediate circle family, college friends, previous colleagues, apartment complex residents. Document 100 contacts with their profession, approximate income, and current financial products. This becomes your priority target list for the first 30 days.

Leverage Hyderabad's active community groups. Join local Facebook groups, WhatsApp communities, and Telegram channels focused on specific neighborhoods or professional networks. Participate genuinely in discussions, offer financial advice without immediate selling, and build credibility before promoting products.

Host informal "financial literacy" sessions in community centers, apartment clubhouses, or co-working spaces. A 30-minute presentation on "5 Financial Products Every Professional Needs" positions you as an expert while naturally introducing GroMo products. These sessions generate 8-12 qualified leads per event average.

The GroMo referral program creates passive income streams. Every partner you recruit generates ₹500-₹1,100 commission for you, plus ongoing revenue share on their sales. In Hyderabad's collaborative startup culture, building a 10-15 person team under you within six months is achievable. That adds ₹15,000-₹25,000 monthly passive income.

Track everything. Use simple spreadsheets documenting: leads contacted, products pitched, applications submitted, approvals received, and payouts credited. This data reveals which products convert best in which customer segments, allowing you to optimize your pitch approach continuously.

Much like the strategies employed in Punjab's zero-investment business landscape, Hyderabad requires localized approaches to financial distribution.

Hyderabad-specific challenges and solutions

Language diversity requires multilingual capability. English dominates professional circles, but small business owners in areas like Charminar or Malakpet prefer Telugu or Urdu. The GroMo app supports multiple languages, but your personal communication should adapt to customer comfort levels.

Competition from traditional financial advisors intensifies in affluent neighborhoods like Jubilee Hills and Banjara Hills. Differentiate through speed (instant digital processing versus week-long traditional approvals), transparency (clear commission disclosure versus hidden fees), and accessibility (WhatsApp support versus office visit requirements).

Traffic congestion discourages in-person meetings. Build your entire business on digital communication video calls, WhatsApp messages, document sharing via Google Drive. This scales better; you can serve 40 customers monthly versus 15 with in-person dependency.

The monsoon season (June-September) reduces foot traffic and outdoor activities, which can impact networking opportunities. Compensate by increasing digital outreach during these months Instagram content, LinkedIn posts, email newsletters to your database. Weather-proof your income by not depending solely on physical networking.

For broader context on building online income streams, check out proven digital business models that complement financial product distribution.

Realistic income projections for Hyderabad partners

Month 1 (₹8,000-₹15,000): Focus on your immediate network. Aim for 20 applications across credit cards and savings accounts from friends and family. Your credibility is highest here; conversion rates reach 35-40%. Use this time to take GroMo's free training modules.

Month 2 (₹18,000-₹30,000): Expand to your secondary network colleagues, extended family, apartment neighbors. Aim for 35-40 applications. Your testimonials from Month 1 reduce skepticism. Start systematic lead tracking.

Month 3 (₹35,000-₹55,000): Launch community outreach. Join 5-7 Hyderabad-specific groups, host your first financial literacy session, start Instagram educational content. Target 50-60 applications. Figure out which product categories convert best for you.

Month 4 (₹50,000-₹75,000): Optimize based on Month 3 data. If personal loans convert best, double down. Identify 3-4 life-event triggers and target those scenarios specifically. Recruit your first 2-3 team members to activate passive income streams. Target 60-70 applications.

Month 5-6 (₹70,000-₹1,00,000): Scale systematically. Your team contributes ₹10,000-₹15,000 passive income. Your optimized product-customer matching increases approval rates by 15-20%. You're now processing 70-85 applications monthly with better efficiency.

This assumes 10-12 hours weekly effort. Full-time partners (40 hours weekly) often reach ₹1,00,000 monthly by Month 3-4. The key variable is consistent daily activity 3-5 applications daily compounds over 180 days.

For those exploring how to balance full-time employment with side income, look into time management strategies that successful GroMo partners employ.

Regulatory compliance and risk management

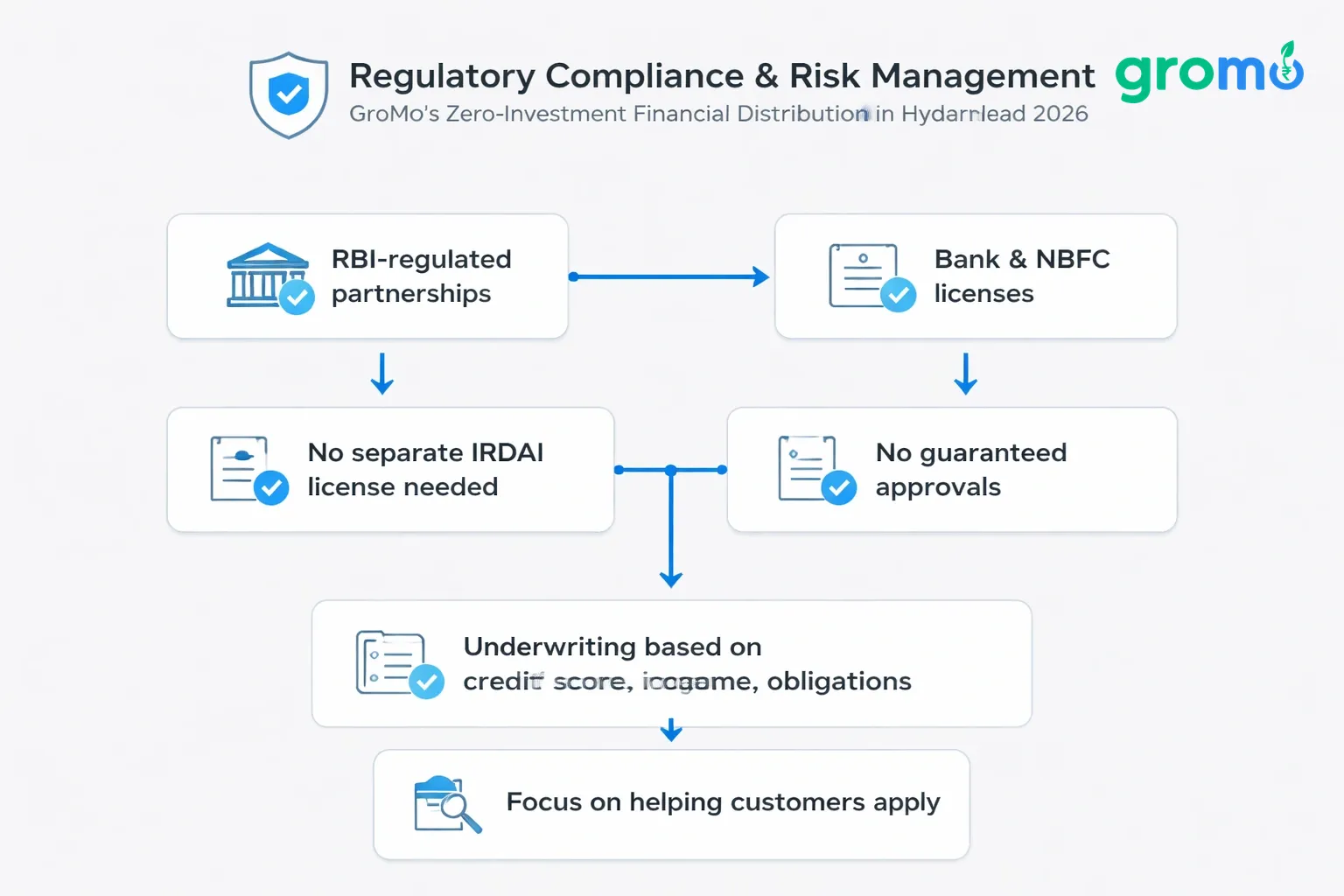

GroMo operates under RBI-regulated financial institution partnerships. Every bank and NBFC on the platform holds valid licenses. Your role as a distribution partner doesn't require separate IRDAI licensing since you're not providing financial advice or handling customer funds directly.

Never promise guaranteed approvals. Lending decisions stay with banks' underwriting algorithms based on credit scores, income verification, and existing obligations. Focus on "helping customers apply" rather than "guaranteeing approval." That language distinction protects you from disputes.

Customer data security is non-negotiable. Never screenshot or store customer KYC documents on personal devices. Process all sensitive information directly through the GroMo app, which maintains encryption and compliance standards. A single data breach can result in partnership termination and legal liability.

Understand clawback clauses. Many loans and credit lines implement first-3-EMI clawback. If customers default within initial payments, your commission is reversed. Manage this risk through proper customer qualification don't push products on clearly ineligible prospects and explain EMI obligations clearly.

The multi-KPI payout structure in products like Tide Business Account requires customer activation across multiple touchpoints. Budget time for post-approval follow-through sending activation reminders, helping with first transactions. These 10-15 minutes of extra effort protect your full payout.

Discover more about legitimate online earning platforms and why commission-based financial distribution outperforms speculative income apps.

Essential tools and resources

Your smartphone is your entire business infrastructure. You need reliable internet, adequate storage for the GroMo app, and proper security (PIN lock, biometric authentication). A ₹15,000-₹20,000 mid-range Android phone works fine.

WhatsApp Business (free) enables professional customer communication with catalog features, automated greeting messages, and quick replies. Create saved responses for frequent questions like "What documents do I need?" This saves time.

Google Sheets (free) handles lead tracking until you're processing 100+ applications monthly. Create columns for: contact name, date contacted, product pitched, application status, approval amount, expected payout, and actual payout received.

Canva (free tier) creates professional-looking social media posts. Pre-designed templates for Instagram and Facebook reduce content creation time. Visual content generates 4x more engagement than text-only updates.

Zoom or Google Meet (free tiers) facilitate video consultations with customers who prefer detailed discussions before applying. Screen sharing walks them through application forms step-by-step, reducing abandonment rates from 35% to 12%.

GroMo's in-app training academy provides free certification courses on financial products, sales techniques, and regulatory compliance. Complete at least 8-10 courses in your first 30 days to build foundational knowledge.

Explore GroMo's comprehensive earning opportunities including current promotional contests and bonus payout structures available in June 2026.

Tax implications

Income from GroMo is "business income" under Section 44AD of the Income Tax Act. File ITR-4 if your annual income exceeds ₹2.5 lakhs. GroMo provides monthly payout statements for tax documentation.

No GST registration is mandatory unless your annual receipts exceed ₹20 lakhs (₹40 lakhs for services). Most part-time partners earning ₹50,000-₹80,000 monthly stay below this threshold. However, voluntary GST registration adds credibility when approaching corporate clients.

Maintain a separate bank account for GroMo income and related expenses even if you're not formally registering a business. This simplifies tax filing and provides clean financial records if you scale later.

Deductible expenses include: internet charges, phone bills (proportionate business use), co-working space fees, printing costs, and travel expenses. Document everything through digital payment trails (UPI, card transactions).

Consider forming a proprietorship firm once monthly income stabilizes at ₹75,000+. This lets you issue invoices to B2B clients, open current accounts with better transaction limits, and project professionalism. Registration costs ₹5,000-₹8,000 through CA services.

For detailed guidance on financial planning for online income, understand how to manage irregular commission income and build emergency funds.

Success stories from the ground

Priya, a 28-year-old HR professional in Gachibowli, started using GroMo while pregnant in March 2025. Commuting was difficult, so she focused on credit card referrals within her IT network. She approached colleagues preparing for international transfers who needed travel cards. She earned ₹63,000 in her first full month. By month four, she hit ₹1.2 lakhs. The income covered her maternity leave gap.

Ravi, a 34-year-old auto-rickshaw driver in Secunderabad, uses GroMo during his midday gaps when ride demand drops. He focuses on FatakPay credit lines for fellow drivers who need quick funds for repairs or medical emergencies. His peer credibility converts 68% of applications. He averages ₹28,000-₹35,000 monthly, adding to his driving income of ₹45,000-₹50,000.

Anjali, a 42-year-old homemaker in Banjara Hills, built a business loan distribution network through her husband's business contacts. Her social credibility in the entrepreneurial community provides warm introductions. She processes 12-15 business loan applications monthly, earning ₹85,000-₹1.15 lakhs. Her income covers her children's private school fees.

These aren't outliers. They represent systematic execution. The common thread: consistent daily activity (1-2 hours minimum), product-customer matching precision, and persistent follow-through.

For more examples of real income generation through financial distribution, check out case studies across different Indian cities.

Frequently asked questions

Q: Do I need experience in finance or sales? A: No. GroMo provides free training modules covering product knowledge, sales techniques, and compliance. Partners from engineering to homemaking succeed. What matters is consistent effort. The app handles the technical complexity of loan processing.

Q: How long for payouts? A: GroMo processes payouts within 24-48 hours of confirmation from the financial institution. Credit card approvals credit within 3-5 days of card dispatch. Loan payouts arrive within 7 days of disbursal. Savings accounts and demat products follow milestone-based payouts across 30-60 day tracking periods. Your dashboard shows real-time status.

Q: Can I do this part-time with a full-time IT job? A: Yes. 73% of Hyderabad partners operate part-time, dedicating 8-15 hours weekly during evenings and weekends. The model doesn't require fixed hours. You share links via WhatsApp, follow up through calls, and guide documentation digitally. Many process 40-50 applications monthly while employed full-time.

Q: What if a loan application gets rejected? A: Rejections happen. Approval rates average 35-45%. You receive no payout for rejected applications, so pre-qualification matters. Before sharing links, verify basic eligibility: credit score, income thresholds, age, and documents. This improves approval rates to 55-65%.

Q: Is there an earning cap? A: No caps. Income correlates with applications processed and approval values. Top partners earning ₹2-3 lakhs monthly typically process 100-120 applications, maintain 8-10 person referral teams, and focus on high-value products like business loans. Your ceiling is time and network reach.

Q: Do I need to spend on marketing? A: Paid ads are optional. Most partners build through organic methods: personal network, community groups, social media, and referrals. If you try paid ads later, budgets of ₹3,000-₹5,000 monthly generate 15-20 leads. Prove conversion on free leads first.