Why GroMo Beats Money-Earning Games in 2026 | Real Income Guide

Gaming apps that promise real money have exploded across India, flooding social media feeds with screenshots of ₹5,000 payouts and testimonials claiming overnight riches. The phrase "paise wala game" (money-earning game) gets millions of searches every month from Indians hoping to turn their smartphone into an ATM. But here's the uncomfortable truth most won't tell you: 95% of these gaming apps are designed for you to lose money, not make it.

Before you download that colorful rummy app or fantasy cricket platform, let's talk about what actually works in 2026 and why commission-based financial product distribution through platforms like GroMo offers a smarter, sustainable path to real income without gambling your hard-earned savings.

The Real Math Behind Money-Earning Games

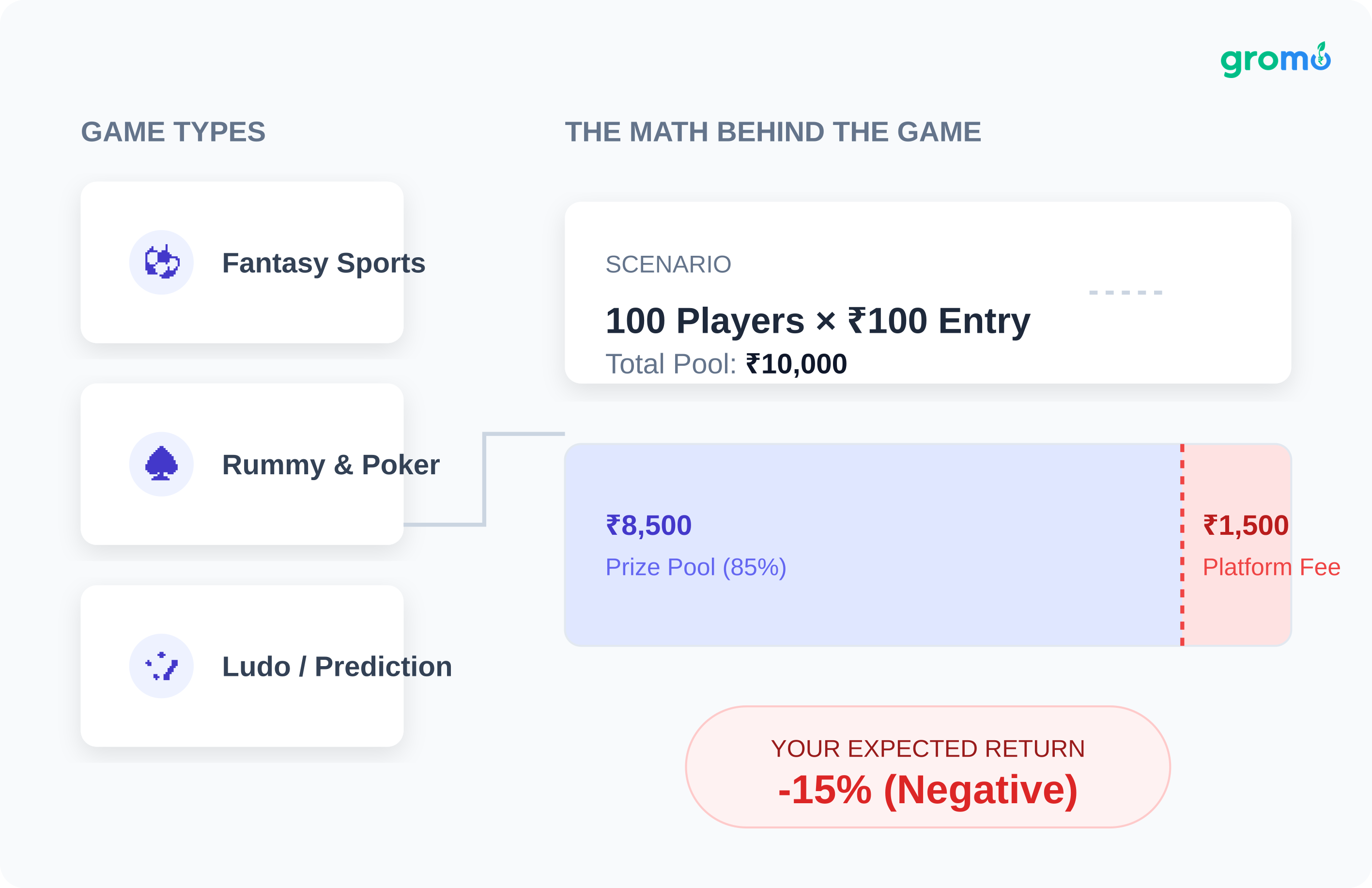

Most paise wala games fall into predictable categories: fantasy sports, rummy, poker, ludo for cash, and prediction apps. Each promises easy money but operates on fundamentals that favor the house, not you.

Fantasy sports platforms take a 10-20% commission on every contest. If 100 people contribute ₹100 each, that's ₹10,000 in the pool but the platform keeps ₹1,500-₹2,000 before distributing prizes. Your actual expected return is negative 15% before you even select your team.

Card games like rummy and poker operate similarly. Even if you're a skilled player, the platform fee and rake ensure the house always profits. For every winner posting their ₹10,000 cash-out, there are dozens who deposited ₹2,000-₹5,000 and lost it all within weeks.

Prediction and spin games are the most deceptive. These apps show you "winning" small amounts initially ₹5 here, ₹20 there to build confidence. But withdrawal minimums are set at ₹200-₹500, and by the time you reach that threshold, you've already watched more ads or made in-app purchases than your "winnings" are worth.

The psychological hooks are sophisticated. Daily login bonuses, referral incentives, and limited-time offers create urgency and FOMO. The apps are engineered by behavioral psychologists who understand dopamine cycles better than you do.

Why Gaming Income Is Unsustainable (Even When You Win)

Let's say you're genuinely skilled at fantasy cricket or rummy and manage to win consistently. You're in the top 5% of players. Even then, three massive problems remain:

Problem 1: Tax Complications

The 2023 Finance Act made all online gaming winnings taxable at 30% TDS (Tax Deducted at Source) from the gross amount. Win ₹10,000? ₹3,000 is deducted immediately. This applies even if you had ₹15,000 in losses that same month. The tax structure doesn't account for net profit only gross winnings.

Problem 2: Account Bans and Restrictions

Winning players get flagged by algorithms. Platforms quietly restrict contest access, increase fees, or shadow-ban accounts that consistently profit. The business model requires losers to subsidize winners; too many winners break the system.

Problem 3: Time Investment vs. Returns

To earn ₹20,000-₹30,000 monthly through gaming requires 4-6 hours daily of research, team building, and active play. That's a part-time job with no benefits, no skill development, and income that disappears the moment you stop playing.

Start Earning Real Income Download GroMo Now

The Commission-Based Alternative That Actually Builds Wealth

Instead of gambling on games, what if you could earn ₹500-₹3,000 per successful referral without risking a single rupee? That's the fundamental difference between gaming apps and financial product distribution through GroMo.

Here's how the math works in your favor:

Zero Risk Capital

Unlike gaming apps where you deposit ₹500-₹5,000 to start playing, GroMo requires zero investment. Download the app, complete free training, and start sharing product links immediately.

Predictable Commission Structure

Credit card approval: ₹300-₹1,000 per card

Personal loan: 1-3.5% of sanctioned amount

Savings account: ₹150-₹400 per account

Demat account: ₹300-₹600 per opening

A single home loan referral can earn you ₹15,000-₹40,000. Compare that to spending 20 hours on rummy hoping to clear ₹5,000.

Compound Growth Through Team Building

GroMo's referral system lets you build a network. When you refer someone who also becomes a GroMo Partner, you earn additional commission on their sales. This creates passive income streams that gaming can never replicate.

Skill Development That Transfers

Learning financial product distribution teaches you sales, customer relationship management, digital marketing, and financial literacy. These skills increase your earning potential across your career. Gaming teaches you… better fantasy team selection.

The GroMo Model: How It Works in Practice

Raj, a 28-year-old IT professional from Pune, used to spend his evenings on dream11 and A23 rummy. After two years, his net gaming return was negative ₹47,000 money he'd deposited hoping for big wins that never materialized.

In January 2026, a friend introduced him to GroMo. Skeptical but intrigued by the zero-investment model, Raj downloaded the app and completed the basic training modules over one weekend.

His first sale was a credit card to his cousin ₹600 commission for a 15-minute conversation. His second was a Kotak 811 savings account to a colleague ₹300 for sharing a link. By March 2026, Raj had earned ₹43,000 through 67 product referrals, spending roughly 10 hours per week.

More importantly, Raj developed a systematic approach: he identified 5-7 people weekly from his social circle who needed financial products, checked their eligibility using GroMo's Success Rate feature, and shared personalized recommendations. His conversion rate hit 40% far better than his 5% win rate in fantasy sports.

Breaking Down the Product Categories

Understanding which financial products to focus on dramatically increases your earning potential. Here's the strategic breakdown:

Credit Cards: Easiest First Sales

Credit cards are the entry point for most GroMo Partners because everyone understands them. Popular cards like HDFC MoneyBack (₹600-₹800 payout) or Axis Neo (₹300-₹500 payout) have broad eligibility criteria.

The key is matching the right card to the customer profile. Young professionals with ₹25,000+ salary qualify for premium cards like HDFC Pixel Play (₹1,000 payout). Students and first-time cardholders work well for AU Altura Plus (₹700 payout) or OneCard (₹1,250 payout).

Savings Accounts: High Volume Potential

Digital savings accounts like Kotak 811 (₹300 payout) or Jupiter (₹400 payout) are perfect for mass outreach. Everyone needs a bank account, and the approval rate is high since there's no credit check.

The strategy here is volume. Share account links in relevant WhatsApp groups, social media posts, or community forums. Ten successful account openings net you ₹3,000-₹4,000 with minimal effort per lead.

Loans: Highest Per-Transaction Earnings

Personal loans and business loans offer percentage-based commissions that can reach ₹15,000-₹40,000 for a single referral. An IDFC Home Loan at 2% commission on a ₹30 lakh sanction means ₹60,000 in your account.

The challenge is identifying qualified borrowers. Focus your loan efforts on people you know are actively seeking credit someone buying property, expanding a business, or consolidating debt. Quality over quantity is critical here.

Demat Accounts: Growing Category

With increasing retail participation in stock markets, demat account referrals for platforms like Upstox (₹600 payout) or Paytm Money (₹500 payout) are trending upward. Young professionals aged 22-35 are the sweet spot.

The pitch is simple: "Start investing with zero brokerage on delivery trades." The application process is fully digital, and approval rates are strong for customers with PAN-Aadhaar linkage.

Common Objections and Reality Checks

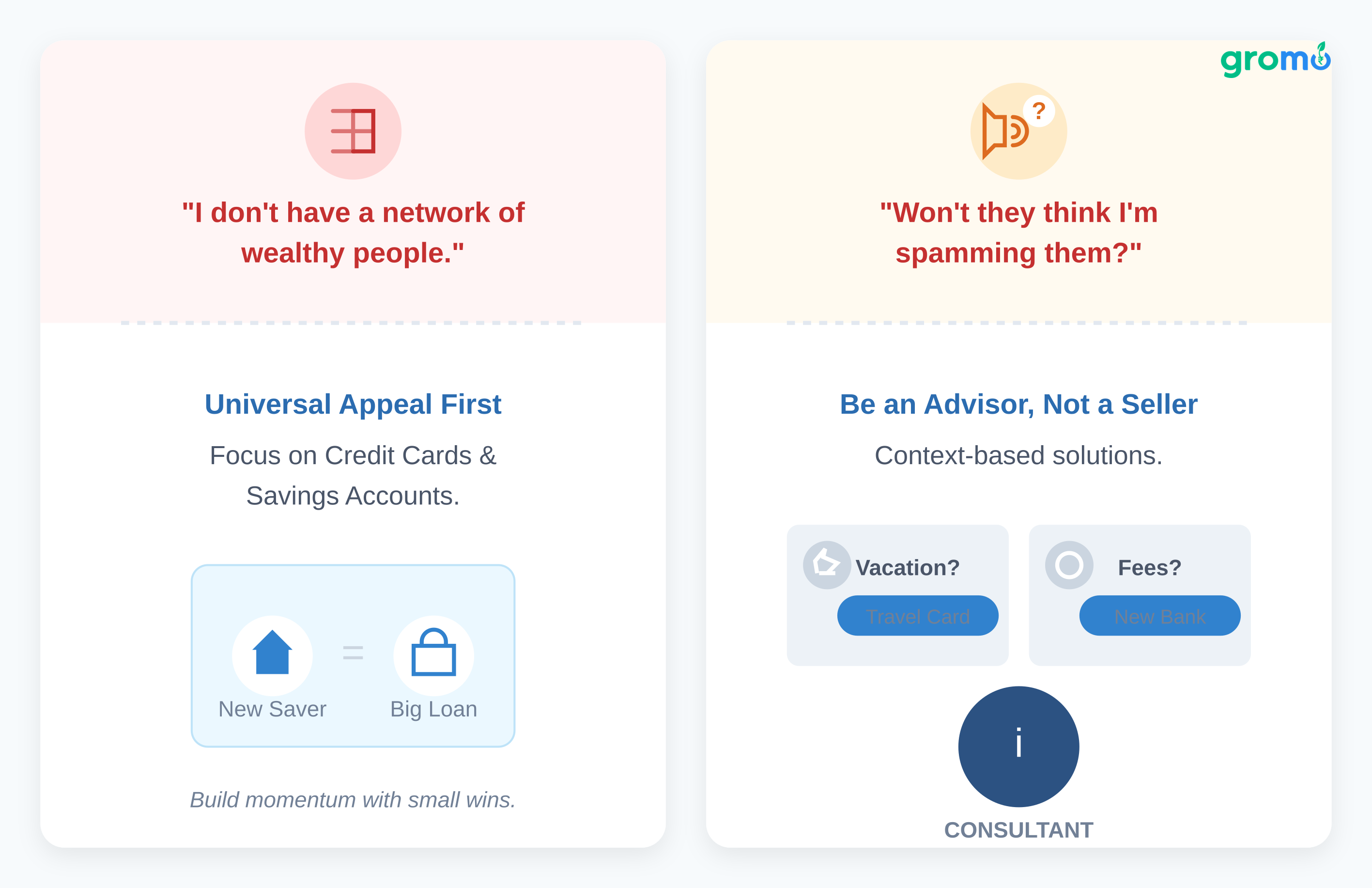

"I don't have a network of wealthy people to sell loans to."

You don't need wealthy contacts. Focus on credit cards and savings accounts initially these have universal appeal. A housewife opening her first digital savings account is as valuable as a businessman taking a loan. Build momentum with small wins before targeting larger products.

"Won't people think I'm spamming them with sales pitches?"

Position yourself as a financial advisor, not a salesperson. When someone mentions they're planning a vacation, suggest a travel rewards credit card. When a friend complains about bank charges, recommend a zero-balance account. Context-relevant recommendations feel helpful, not salesy.

"How is this different from MLM schemes?"

GroMo is not multi-level marketing. You earn commissions on your direct sales, not from recruiting a downline. The optional referral program (building a team) provides additional income but isn't required. There are no inventory purchases, mandatory monthly quotas, or recruitment fees.

"What if the customer defaults on a loan I referred?"

You're not liable for customer repayment. Your commission is paid when the loan disburses. Clawback clauses exist (typically if the customer cancels within 90 days), but default or late payment by the customer doesn't affect your earned commission.

Join 60 Lakh Partners Start Free Today

The Gamification That Actually Helps You Earn

Here's where GroMo borrows the best elements of gaming without the financial risk. The GroMo Premier League (GPL) 2026 is a two-month contest aligned with IPL that turns your sales activities into cricket runs.

Every action scores points:

App open: 1 run

Quiz completion: 2 runs

Lead creation: 4 runs

Successful sale: 6 runs

Match-day activities: 2X multiplier

Daily prizes include ₹1,000 for Man of the Match, ₹500 for Fighter of the Match, and ₹100 each for five Impact Players. The total prize pool exceeds ₹10 lakh.

This gamification creates engagement and motivation without requiring you to risk money. You're earning commissions on real sales while competing for bonus prizes the opposite of gaming apps where you pay to play.

Building a Sustainable ₹1 Lakh Monthly Income

Reaching ₹1 lakh per month through GroMo is absolutely achievable, but it requires strategy, not luck. Here's the realistic roadmap:

Months 1-2: Foundation (₹15,000-₹25,000/month)

Focus on credit cards and savings accounts within your immediate network. Target 25-35 leads per month with a 30-40% conversion rate. This builds confidence and teaches you the platform.

Months 3-4: Expansion (₹35,000-₹50,000/month)

Add loan referrals as you identify qualified borrowers. Start building social media presence with financial tips and product recommendations. Your monthly leads should hit 40-50 with improving conversion.

Months 5-6: Scaling (₹60,000-₹80,000/month)

Implement systematic lead generation through content marketing, referral requests, and community engagement. Consider building a small team of 2-3 sub-partners for additional passive income. Monthly leads: 60-70.

Month 7+: Optimization (₹1,00,000+/month)

Focus on high-ticket products (home loans, business loans) while maintaining steady volume in cards and accounts. Your team contributes 20-30% of income. You're now running a legitimate financial distribution business.

This progression assumes 10-15 hours per week of consistent effort. It's not passive income initially, but unlike gaming, every hour invested builds skills, network, and reputation that compounds over time.

Why April 2026 Is the Perfect Time to Start

The Indian fintech landscape in 2026 offers unprecedented opportunities for individual distributors. Digital lending grew 40% in 2025, and credit card issuances are at record highs as banks push for financial inclusion.

Consumer awareness of digital financial products has matured. People no longer fear app-based banking or online loan applications. This reduces your selling effort you're facilitating decisions people are already inclined to make.

Additionally, GroMo's partnership base of 60 lakh+ distributors creates a proven playbook. The free training academy, instant payout infrastructure, and customer management tools are more sophisticated than ever. You're joining a mature ecosystem, not an experimental platform.

The regulatory environment also favors distributed financial services. RBI guidelines on digital lending and SEBI's focus on retail investor protection have legitimized the online financial product space. Customers trust these applications because they're backed by established banks and licensed NBFCs.

The Psychology of Real Income vs. Gaming Income

Here's the critical mindset shift: gaming income is extractive (money flows from losers to winners, with the platform taking a cut), while commission income is productive (money flows from financial institutions to distributors who provide customer acquisition services).

When you earn ₹800 from a credit card referral, you've created value for three parties:

The bank gains a new customer

The cardholder accesses credit and rewards

You earn fair compensation for connecting the two

No one loses. This is sustainable economics.

When you win ₹800 in a rummy game, someone else lost ₹800 (plus platform fees). This is zero-sum. Eventually, that person stops playing or you stop winning. The model collapses.

Your brain experiences the same dopamine hit from both earnings, but one builds wealth while the other depletes it. Choosing commission-based income over gaming is choosing delayed gratification and compound growth over instant thrills and guaranteed long-term losses.

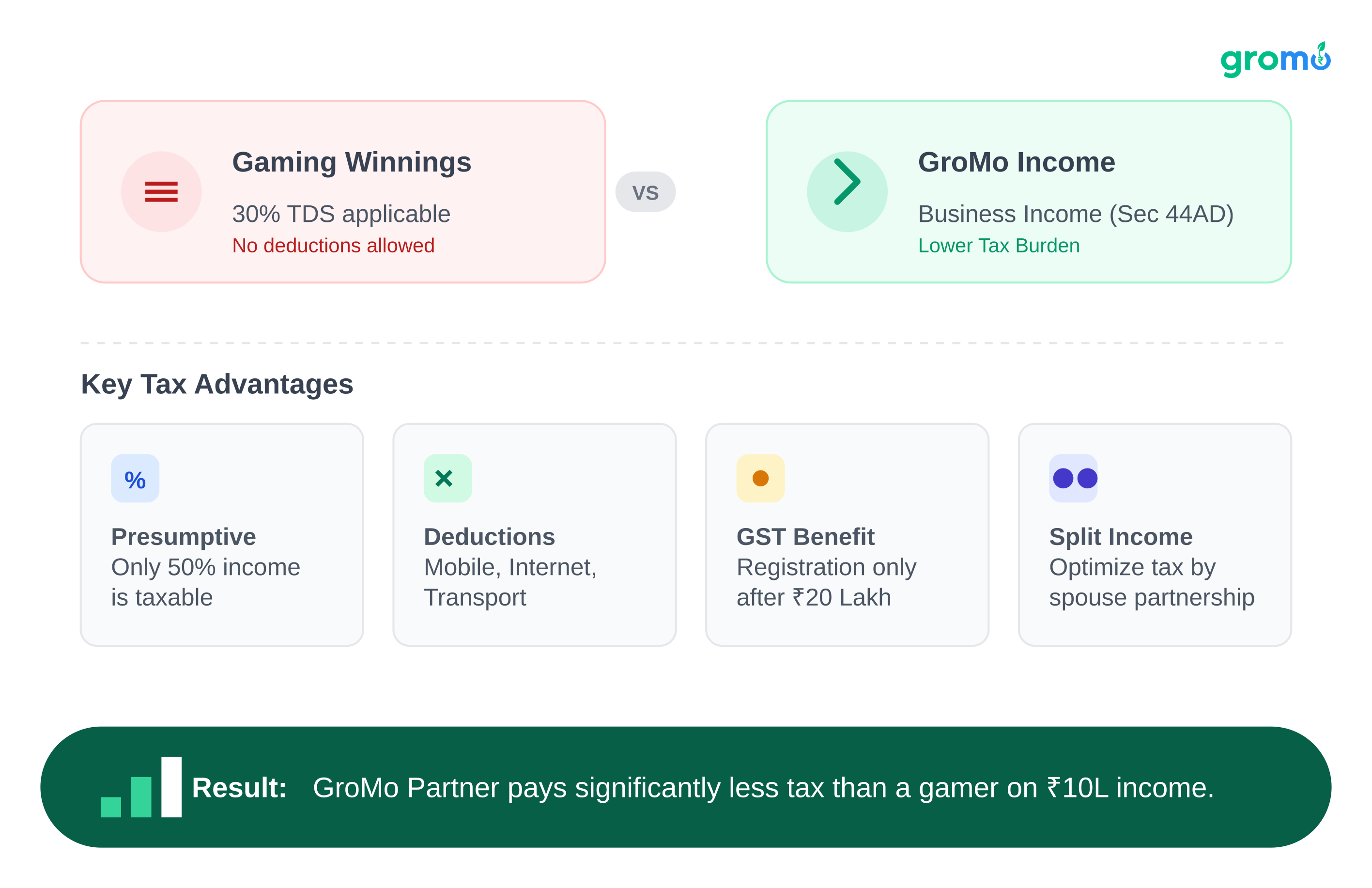

Tax Advantages and Legal Clarity

Unlike gaming winnings taxed at 30% TDS, commission income from GroMo is treated as business income under IT Act Section 44AD. This allows for:

50% presumptive taxation (only 50% of income is taxable if you opt for presumptive scheme)

Business expense deductions (mobile bills, internet, transportation)

GST registration benefits after ₹20 lakh annual income

Income splitting with spouse for tax optimization

A GroMo Partner earning ₹10 lakh annually pays significantly less tax than a gaming professional with the same gross earnings. The legal and tax framework is designed to encourage entrepreneurship, not gambling.

Getting Started: Your First Week Action Plan

If you're ready to move from "paise wala game" to legitimate earning, here's your seven-day launch plan:

Day 1: Download GroMo app and complete registration. Explore the interface and watch the intro videos.

Day 2: Complete at least 3 training modules in the GroMo Academy. Focus on credit cards and savings accounts initially.

Day 3: Make a list of 20 people in your network who might need financial products. Categorize by product type (credit card, savings account, loan).

Day 4: Use the Success Rate checker to identify your 5 highest-probability leads. Prepare personalized pitches for each.

Day 5: Make your first 5 product recommendations. Share links via WhatsApp with context-specific messages.

Day 6: Follow up with leads. Track status in the app and set reminders for pending applications.

Day 7: Review your first week metrics. How many links shared? How many applications started? What's your conversion rate? Adjust strategy for week two.

This structured approach eliminates the trial-and-error that wastes months for most beginners. You're treating this as a business from day one, not a hobby.

The Compound Effect: Where You'll Be in 12 Months

Let's project forward. If you follow the roadmap outlined above, by April 2027 you'll have:

Earned ₹5-7 lakh in total commissions

Built a network of 400-600 satisfied customers who trust your recommendations

Developed transferable skills in sales, digital marketing, and financial advisory

Created 2-3 passive income streams through team building and repeat customers

Established a legitimate side business that can scale to full-time income

Compare that to 12 months of gaming apps:

Net financial position likely negative or barely break-even

Zero transferable skills

High stress from wins/losses volatility

No asset or network built

Same earning potential in month 12 as month 1

The contrast becomes starker with each passing year. Commission-based distribution compounds; gaming income doesn't.

Alternative Platforms Worth Considering

While GroMo is India's largest financial product distribution platform with 60 lakh+ partners, transparency requires acknowledging alternatives. PolicyBazaar offers insurance product distribution, but commissions are typically lower and payouts slower. Bankbazaar focuses on comparison-based lead generation with more limited partner control.

Traditional DSA (Direct Selling Agent) relationships with individual banks offer higher per-transaction commissions but require exclusivity and often upfront investment in marketing materials. GroMo's multi-brand aggregation model provides more flexibility and zero-investment entry.

The key is matching platform to your goals. If you want broad product variety, instant payouts, and zero capital requirements, GroMo's value proposition is unmatched as of April 2026. For specialized niches (pure insurance, pure mutual funds), alternatives exist but with trade-offs.

Final Truth: Entertainment vs. Income

Here's the honest conclusion: if you enjoy gaming purely for entertainment and can afford to lose ₹2,000-₹5,000 monthly, play responsibly with money you'd otherwise spend on movies or dining out. That's recreational, like buying lottery tickets.

But if you're searching "paise wala game" because you genuinely need additional income to pay off debt, support family, save for goals, or achieve financial independence then commission-based earning through platforms like GroMo is the superior choice by every objective measure.

You eliminate financial risk, build transferable skills, create compound growth potential, and earn predictable income from productive economic activity. The initial effort investment is similar to becoming skilled at rummy or fantasy sports, but the long-term payoff is exponentially higher.

The question isn't really "which paise wala game should I play?" It's "am I serious about earning money, or just looking for entertainment?" Answer that honestly, and your path becomes clear.

Frequently Asked Questions

Q: Can I really earn ₹1 lakh per month through GroMo without any investment?

A: Yes, it's possible but requires consistent effort over 6-8 months. Most partners earning ₹1 lakh+ monthly focus on high-ticket products (loans), maintain steady volume in credit cards and accounts, and often build a small referral network. The zero-investment claim is accurate you don't need capital to start, but you do need to invest time learning the products and building your lead pipeline. Expect ₹15,000-₹25,000 monthly in your first quarter, scaling upward with experience.

Q: How is GroMo different from gaming apps that claim I can earn money?

A: Gaming apps operate on zero-sum economics where your earnings come from other players' losses (minus platform fees). GroMo operates on productive commission economics where banks pay you for customer acquisition services. Gaming requires you to risk capital and compete against algorithms designed for you to lose; GroMo requires zero capital investment and pays you for successful referrals regardless of competition. Gaming income is taxed at 30% TDS on gross winnings; GroMo commission is taxed as business income with deductions available.

Q: What happens if someone I refer doesn't repay their loan am I liable?

A: No, you have zero liability for customer repayment. Your commission is paid when the loan disburses. The only clawback scenarios are if the customer cancels the product within 90 days or if fraud is detected in the application process. Default or late payment by the customer after disbursement does not impact your earned commission. You're a referral partner, not a guarantor.

Q: Do I need financial expertise or certifications to start earning through GroMo?

A: No prior financial expertise is required. GroMo provides free training through its Academy that covers product basics, customer profiling, application processes, and compliance requirements. The training takes 2-4 hours to complete for basic certification. You learn by doing your first 10-15 referrals will teach you more than any course. The app also has a Success Rate checker that tells you which products a customer qualifies for, eliminating guesswork.

Q: How long does it take to receive payment after a successful referral?

A: GroMo has the fastest payout system in India's financial distribution market. For credit cards and savings accounts, commission is typically credited within 24-48 hours of card dispatch or account activation. For loans, payment occurs within 48-72 hours of disbursement. Once your GroMo wallet balance reaches ₹100, you can instantly transfer funds to your bank account. There's no monthly payout cycle you get paid as soon as you earn.

Q: Is building a team necessary to reach ₹1 lakh monthly, or can I do it through direct sales alone?

A: You can absolutely reach ₹1 lakh monthly through direct sales alone if you focus on high-ticket products like home loans, business loans, and maintain volume in credit cards and accounts. However, building a small team of 3-5 active sub-partners can contribute 20-30% additional passive income and helps you scale beyond ₹1 lakh more easily. Team building is optional, not mandatory choose based on whether you prefer solo selling or network development.