Zero-Investment Business in India 2026: GroMo Guide

Zero-investment business setup in India 2026: A guide using GroMo

You can start a business in India right now with nothing but a phone. No capital, no office, no inventory. Platforms like GroMo let you sell credit cards, loans, and savings accounts on commission. You bring the network; they handle the product, the compliance, and the payouts.

The "zero-investment" label isn't a trick. It's a shift in how distribution works. You don't need to build the infrastructure because it already exists. Over 60 lakh partners across India use these platforms to build side incomes or full-time livelihoods.

Side income opportunities have changed. A shopkeeper in Jaipur made ₹47,000 last month just by sharing credit card links with customers who were already in his shop. A techie in Bangalore made ₹83,000 helping colleagues open savings accounts during lunch. The infrastructure is there. The question is whether you use it.

The legal bit (easier than it sounds)

You don't need a license. GroMo holds the regulatory approvals from RBI and SEBI. You operate under their umbrella. It's referral work, not financial advice.

The income is commission-based. For taxes, it's treated as professional income. You don't need GST unless you cross ₹20 lakhs in annual turnover.

To start, you need:

- PAN card

- Bank account

- Aadhaar

- A phone with internet

GroMo doesn't do insurance, which is a good thing. Selling insurance requires IRDAI exams and licenses. Financial product distribution without insurance skips that headache entirely.

One thing: don't promise people they'll get approved. You're not the bank. You just make the introduction.

What you're selling

GroMo's catalog includes credit cards, savings accounts, demat accounts, and loans. The commissions differ based on how hard the product is to sell and the ticket size.

Credit cards

The Axis Flipkart Credit Card pays ₹2,000 to ₹3,000 per approval. It sells itself to anyone who shops on Flipkart or Myntra 5% cashback is real money. The customer needs a decent credit score and income proof. There's a video KYC within 72 hours.

The IDFC WOW Credit Card is for people who can't get a normal card. It's secured by a fixed deposit (start at ₹5,000). Good for college kids or people rebuilding credit. The commission is lower, but it converts well because almost anyone with ₹5,000 gets approved.

Savings accounts

Tide Business India Account is for freelancers and small business owners. It’s a current account with a 1.5% cashback on spends. The payout is staggered you get paid in chunks as the customer hits milestones (opening, bill pay, card usage). You need them to stay active for two months to see the full commission.

Demat accounts

Upstox pays ₹250 to ₹400 per account. The draw is simple: zero opening fees, zero maintenance for the first year. The catch is the customer has to place a trade within seven days, or you don't get paid.

Indiabulls Securities and Aditya Birla Money are similar. Aditya Birla has stricter criteria (age 25+, income ₹50,000+), which means fewer leads but better quality.

Business loans

ClickPe Business Loan (Muthoot Finance) pays 1.5% to 2.5% on loans up to ₹3 lakhs. It’s same-day money for the customer just PAN, Aadhaar, bank statement. Good for shopkeepers who need cash fast.

Poonawalla Fincorp Business Loan goes up to ₹50 lakhs, with 1.75% to 3% commission. More paperwork required (GST, bank statements, owned house proof).

Heads up: both have clawback clauses. If the customer defaults on the first three EMIs, you lose the commission.

Personal loans and credit lines

FatakPay Credit Line is small money up to ₹20,000. Commission is 1% to 2%. It's a volume play. You need a lot of these to make it count.

HDFC Smart EMI lets HDFC cardholders convert their limit to EMIs. Commission is 0.5% to 1%.

Getting customers

Financial distribution businesses live or die on your ability to get people to click a link.

Start with the obvious

List 50 people you know. Family, friends, colleagues, the electrician, the gym trainer. Next to each name, write what they probably need. The 28-year-old software engineer? Probably wants a credit card or a demat account. The 45-year-old shop owner? Maybe a business loan.

Don't spam. "I saw you talking about investments Upstox is free for the first year if you're interested" works better than "Open demat account now."

Content helps

GroMo gives you brochures and images. Post one thing on WhatsApp status every day. Explain how a product works. If you understand how credit card cashback actually calculates, tell people. Being helpful beats being salesy.

Location matters

Zero-investment businesses in specific cities leverage what's around you. Delhi has density. Mumbai entrepreneurs target gig workers. Bangalore tech professionals focus on startup employees.

Rural areas are wide open. Partners in Punjab help farmers and traders access loans via Aadhaar.

The timeline

Month 1: Learning

Download the app. Do the certification. Figure out who qualifies for what nothing ruins trust faster than pitching a product to someone who can't get it.

Make a list of 50 people. Practice explaining a product out loud. If you sound like a script, try again.

Goal: Finish training, list 50 people, make 10 calls.

Month 2: First money

Start with easy stuff. Credit cards for friends with decent salaries. Demat accounts for people curious about stocks. Follow up. People forget.

Goal: ₹10,000 to ₹20,000.

Month 3: A system

Set targets. 15 new conversations a week. Make WhatsApp groups by category. Ask happy customers for referrals.

Goal: ₹40,000 to ₹60,000.

Months 4-6: Rhythm

By now you know which products close fast and which drag. You have a pipeline. Professionals working full-time who put in 2 hours a day can hit ₹80,000 to ₹1 lakh by month six.

Tools

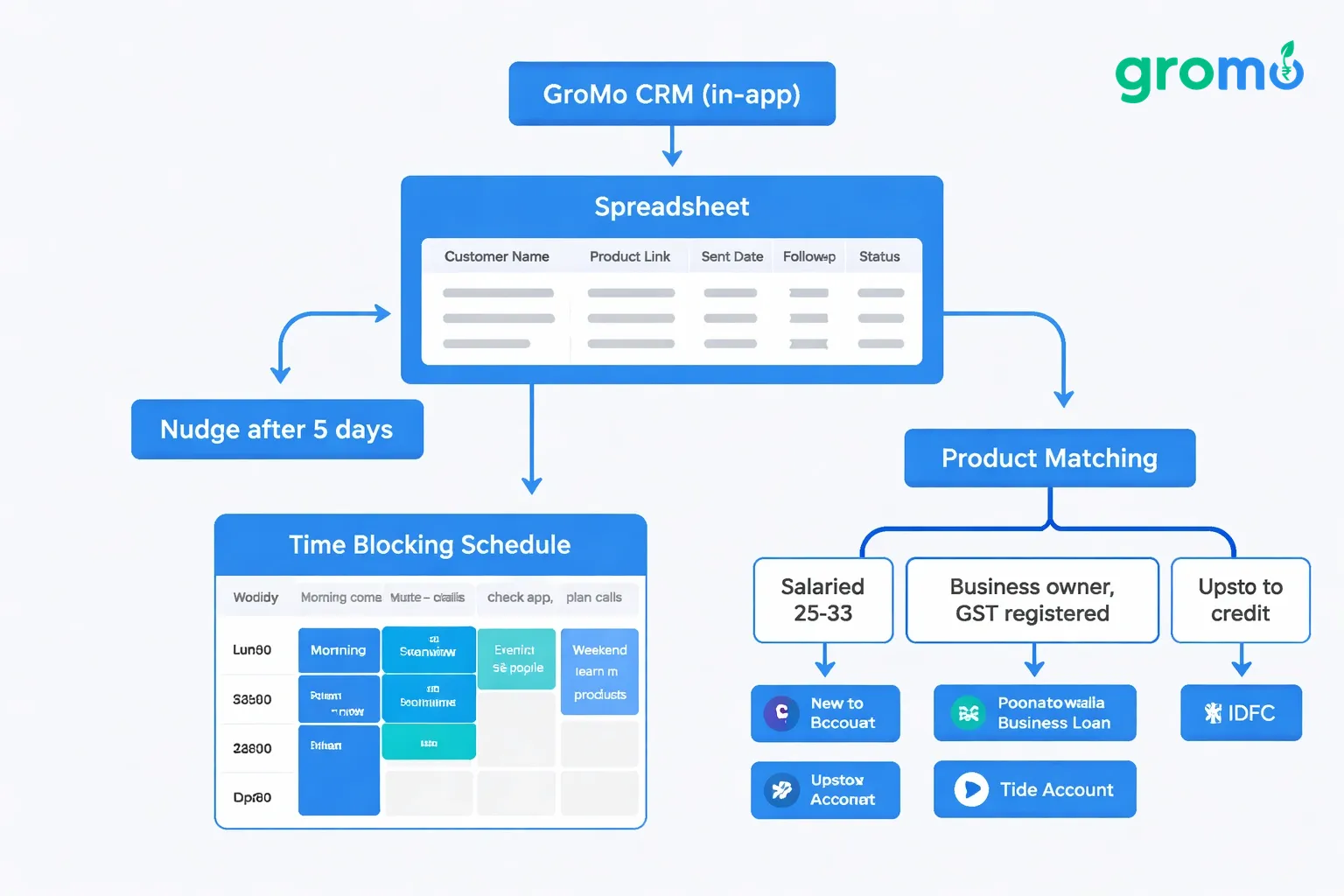

GroMo has a CRM inside the app. Use a spreadsheet too:

- Customer name

- Product

- Link sent date

- Status

- Follow-up date

Set reminders. "I'll do it next week" needs a nudge on day five.

Time blocking

If you have a job, part-time income generation needs a slot on your calendar:

- Morning commute: Check app, plan calls.

- Lunch: Call 5 people.

- Evening: Follow up.

- Weekend: Learn new products.

Matching products to people

Salaried, 25-35, decent credit:

- Axis Flipkart Card (₹2,000-3,000)

- Upstox Demat (₹250-400)

Business owner, GST registered:

- Poonawalla Business Loan (1.75-3%)

- Tide Account

New to credit:

- IDFC WOW Card

- Savings accounts

Building a team

GroMo lets you earn from people you refer. If you bring on a CA who talks to business owners, or a real estate agent who meets buyers, you get a cut of their sales.

Train them. Share your scripts. Make a WhatsApp group. A 10-person team where everyone makes ₹30,000 creates a pot of ₹3 lakhs. You take an extra 10-20% on top.

Managing the money

Commission is lumpy. You might close a ₹15,000 loan commission one week and nothing the next.

Expectations

- Months 1-2: ₹5,000 to ₹15,000.

- Months 3-6: ₹25,000 to ₹60,000.

- Months 7-12: ₹60,000 to ₹1,00,000+.

Cash flow

GroMo pays quickly, but approvals take time. Keep a 3-month buffer if you want to do this full-time. Mix fast products (cards) with slow ones (loans).

Taxes

It's "Income from Business or Profession." Save your statements. Get a CA when you cross ₹5 lakhs a year. GST at ₹20 lakhs.

The parts that suck

Low conversions

New people get 5-10% conversion on links. Experienced ones get 25-30%. The difference? Asking the right questions before you send a link. Offer to help them fill the form. Follow up.

Rejections

Banks say no. Credit scores are bad. Documents are missing. Learn the criteria so you don't pitch to the wrong people.

Trust

Online earning opportunities face skepticism. People think it's a scam. Show your earnings. Explain that the bank pays you, not the customer. Mention the Y Combinator backing.

Time

Balancing this with a job is hard. Use the commute. Use lunch. Use weekends. Five real conversations beat twenty spam messages.

Real examples

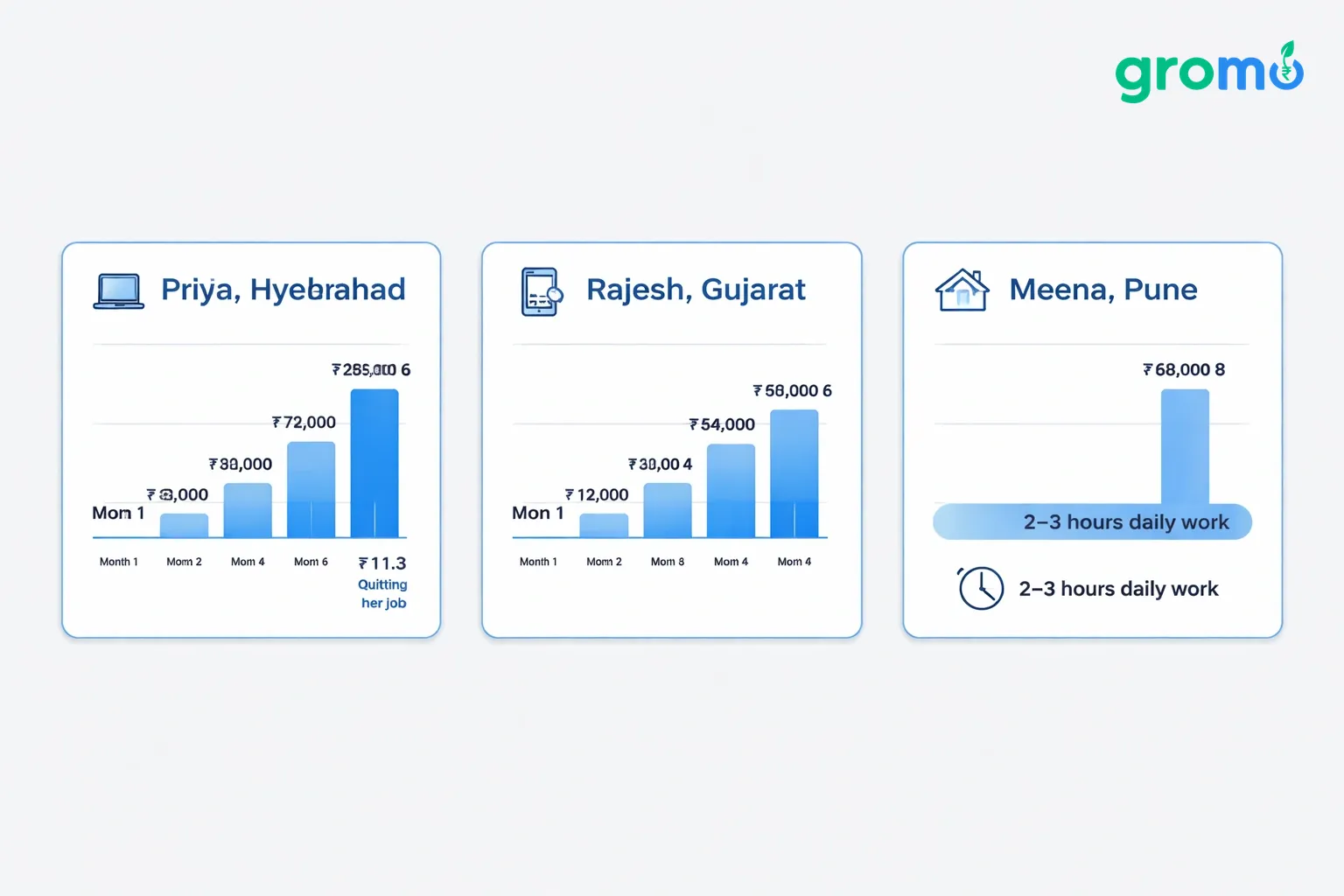

Priya from Hyderabad was a marketing exec making ₹35,000. She started in January 2025. Month 1: ₹8,000. Month 6: ₹72,000. She quit her job in December 2025 and now makes ₹1.3 lakhs with a team.

Rajesh from Gujarat runs a mobile repair shop. He pitches credit cards to customers while they wait. Month 1: ₹12,000. Month 4: ₹54,000. He kept the shop; the side income adds ₹40,000-60,000.

Meena, a housewife in Pune, used her housing society network. She focuses on savings accounts for housewives and cards for working parents. Month 8: ₹68,000. She works 2-3 hours a day from home.

These aren't special cases. They're just people who kept going. Slow start, then momentum.

The tech

The app tracks customers, applications, and payouts. It has training videos, product catalogs, and marketing materials you can download. You can generate a visiting card inside the app.

Works on iOS and Android. Needs an Aadhaar-linked phone number.

Other options

India has zero-investment income opportunities besides this.

Freelancing: Pays well if you have skills, but you're still trading time for money.

Food delivery / Ride-sharing: Instant cash, but you need a vehicle and the pay caps around ₹30,000-40,000.

Affiliate marketing: Similar model, but commissions are tiny (₹100-500) and you need a big audience.

Money-Earning Games: Mostly a waste of time. Hours of effort for ₹50-200.

Financial distribution hits a middle ground: no special skills, high per-sale payout, works part-time, scales with a team.

Rules to follow

Don't promise approvals. You don't decide.

Don't charge customers. The platform pays you. If you charge the customer, you'll get banned.

Don't lie. If a loan takes 3 days, don't say "instant."

Protect data. Keep customer info on the platform. No screenshots.

Don't impersonate banks. You're a partner, not a bank employee.

Don't cheat. Fake leads will get your account shut down.

The long game

India's financial distribution market is growing. Digital adoption in Tier 2/3 cities is just getting started.

To last:

- Keep learning. Products change.

- Specialize. Be the person for business loans or demat accounts.

- Build a name. LinkedIn, WhatsApp, content.

- Keep relationships. A customer who takes a card today might need a loan in two years.

- Mix products. Fast ones for cash flow, big ones for the check size.

It shifts from "selling" to "managing a network." 500 people who trust you and come back twice a year is a real business.

FAQ

Is GroMo legit? Yes. Y Combinator-backed. ₹100+ crores paid out. 60 lakh partners.

Zero investment really? Yes. App is free. Training is free. You need a phone.

Month one earnings? Probably ₹5,000-15,000. You're learning. Month 3-4 can be ₹30,000-50,000 with consistent effort. Month 6 can be ₹80,000-1 lakh.

License needed? No. GroMo has the licenses.

Customer defaults? For loans, you lose the commission if they default in the first 3 EMIs. Cards and demat accounts don't have clawback.

Can I do this with a job? Most partners do. 2 hours a day. Commute, lunch, evening. Weekends for learning.