Zero-Investment Business in Gujarat with GroMo

Gujarat runs on business. Walk through any industrial estate in Ahmedabad, any textile market in Surat, any diamond polishing unit in Bhavnagar someone is looking for credit, a better savings account, or money for their next expansion. Starting a traditional business here means shelling out lakhs for rent, inventory, licenses. Selling financial products through GroMo costs nothing upfront. You work from your phone and earn anywhere from ₹10,000 to ₹1 lakh monthly.

I'll cover seven approaches that are actually working for people in Gujarat, the compliance stuff you need to know, real earnings data from GroMo partners, and a setup process that takes under two hours. These fit into real life whether you're working a 9-to-5 in Ahmedabad or managing a household in Surat.

Why Gujarat Makes This Easy

The state accounts for 7.6% of India's GDP. Over 500,000 MSMEs operate here. Every textile trader, diamond merchant, and kirana store owner needs financial products credit cards for working capital, business loans for inventory, savings accounts for daily transactions. You can sell all of these through GroMo's platform without renting an office or buying stock.

Gujarati communities are tight-knit. One happy customer typically sends you three relatives. Smartphone penetration sits at 77.3% with 63% internet access, so digital onboarding actually works. Financial literacy runs higher than the national average 48% of adults understand credit scores versus 38% across India which means less explaining.

How GroMo Pays You

Download the free app, do a 15-minute certification, and share product links via WhatsApp or social media. When someone activates a product through your link, you get paid. Commissions range from ₹250 for a demat account to ₹3,750 for a premium credit card. The app tracks everything and deposits earnings to your bank within 72 hours.

| Product | Payout Range | When You Get Paid | Who Needs This |

|---|---|---|---|

| Credit Cards | ₹1,750 – ₹3,750 | Card delivered + first transaction | Salaried employees, shop owners |

| Savings Accounts | ₹550 – ₹850 | Video KYC + ₹500 funding | Freelancers, students, gig workers |

| Demat Accounts | ₹250 – ₹500 | Account opened + first trade | Young professionals, IPO investors |

| Business Loans | ₹1,500 – ₹5,500 | Disbursal + first EMI | MSME owners, traders |

| Personal Loans | ₹3,500 – ₹5,500 | Disbursal + three EMIs | Medical emergencies, weddings |

Most products have no clawback risk. The exception: personal loans and business loans that default in the first three EMIs. GroMo handles customer service, documentation, compliance. You make the introduction.

Seven Business Ideas That Work in Gujarat

Housing Society Finance Advisor

Gujarat has over 23,000 registered housing societies. Each one has 50 to 500 families. Position yourself as the person they call for financial questions. Attend society meetings, offer free workshops on credit scores or tax-saving mutual funds, share GroMo links for products like Kotak 811 savings accounts or SBI credit cards. One Ahmedabad partner signed up 42 families in a single complex ₹38,600 in two months.

Print flyers (about ₹200 if you want) and drop them in mailboxes. Host a 30-minute Sunday session on improving credit scores. Use GroMo's credit score explainer content as your material. Offer WhatsApp consultations for families who don't want to ask questions publicly.

MSME Loan Partner

Gujarat's 265 industrial estates house over 80,000 small manufacturers. They need working capital constantly for raw materials, machinery upgrades, GST payments. Visit 10 to 15 units a week, introduce ClickPe business loans (up to ₹3 lakh, same-day disbursal, PAN and Aadhaar only), share application links. Each disbursed loan pays ₹1,500 to ₹2,500. Ten loans a month: ₹15,000 to ₹25,000.

Target Udyam-registered businesses first. Their approval rates exceed 70% because lenders trust the government registration. Bring a tablet to show eligibility on the spot immediacy converts people who might otherwise say "I'll think about it."

Credit Card Specialist for Salaried Professionals

Ahmedabad, Surat, Vadodara, and Rajkot have about 1.2 million IT, pharma, and textile professionals earning ₹25,000 to ₹60,000 monthly. They qualify for premium cards but don't have time to research. Create a WhatsApp group for "Credit Card Gyaan," post weekly comparisons of SBI, HDFC, and Axis cards, send GroMo links when someone asks. Each approved card pays ₹2,000 to ₹3,750.

Partner with HR departments at mid-sized companies. Offer lunch-hour seminars on credit card rewards. Collect 20 to 30 leads per session. A Surat partner runs two corporate sessions a month ₹55,000 from credit cards alone.

Demat Account Drive for Students

Gujarat has 53 universities and 1,200+ colleges. Students want to invest in IPOs and mutual funds but find traditional brokers intimidating. Run Instagram and YouTube campaigns called "₹250 se Investing Shuru Karo," explain Upstox or 5paisa demat accounts, share links. Each activation pays ₹250 to ₹500. Fifty accounts a month: ₹12,500 to ₹25,000.

Record 60-second reels showing live account opening and first trade. Post in Gujarati and Hindi. Use hashtags like #GujaratInvesting and #FirstDemat.

Digital Gold Partner

Gujaratis buy 18% of India's gold. The spending spikes during Diwali, Dhanteras, wedding season. Promote Aditya Birla Digital Gold as an alternative with zero storage costs and zero making charges. Explain the ₹10 minimum investment, instant liquidity, 24K purity. Earn ₹400 to ₹650 per activated user. Gujarat partners reported 180% higher sign-ups in October 2025 compared to other months.

Create Gujarati content explaining "સોનું ખરીદવાનો નવો રસ્તો" (new way to buy gold). Target WhatsApp groups of married women aged 25 to 45 they're the primary gold purchase decision-makers.

Personal Loan Consultant

Gujarat's per-capita income hit ₹2.4 lakh in 2025, but many families lack emergency funds. Position yourself as the person to call for medical emergencies, wedding expenses, debt consolidation. Promote RBI-approved loan apps on GroMo Poonawalla Fincorp (up to ₹50 lakh), Aditya Birla (up to ₹30 lakh), MyMoneyBazaar (up to ₹30,000 instant). Earn ₹3,500 to ₹5,500 per disbursal. Five loans a month: ₹17,500 to ₹27,500.

Personal loan payouts include a three-EMI clawback clause. Pre-qualify customers using GroMo's eligibility checker. Ask for six months of bank statements and verify employment before sharing application links.

Savings Account Champion

About 12% of Gujarat adults still don't have bank accounts, mostly in rural Kutch, Dahod, and Tapi districts. Offer Kotak 811 or Airtel Payments Bank accounts they need only Aadhaar and a smartphone. Walk customers through video KYC, funding, their first UPI transaction. Each activation pays ₹550 to ₹850. Target migrant laborers, domestic workers, small vendors.

Partner with local NGOs or self-help groups running financial literacy drives. Offer to handle digital onboarding for their beneficiaries. A Rajkot partner activated 67 accounts through a single SHG federation ₹41,850.

Launching in Two Hours

First hour: Download GroMo, sign up with your mobile, verify PAN, watch the training video (15 minutes), pass the certification quiz, link your bank account, browse products and pick five that match your network.

Second hour: Draft WhatsApp templates for credit card, savings account, and business loan pitches. List 50 warm leads relatives, neighbors, shop owners you know. Send personalized messages to 10 people with your referral links. Post an Instagram story about starting your zero-investment business.

Within 48 hours, expect 2 to 4 people to click your links. Follow up by phone, answer questions using GroMo's in-app FAQs, guide them through the application. Your first commission usually arrives in 5 to 7 days.

Legal Stuff You Need to Know

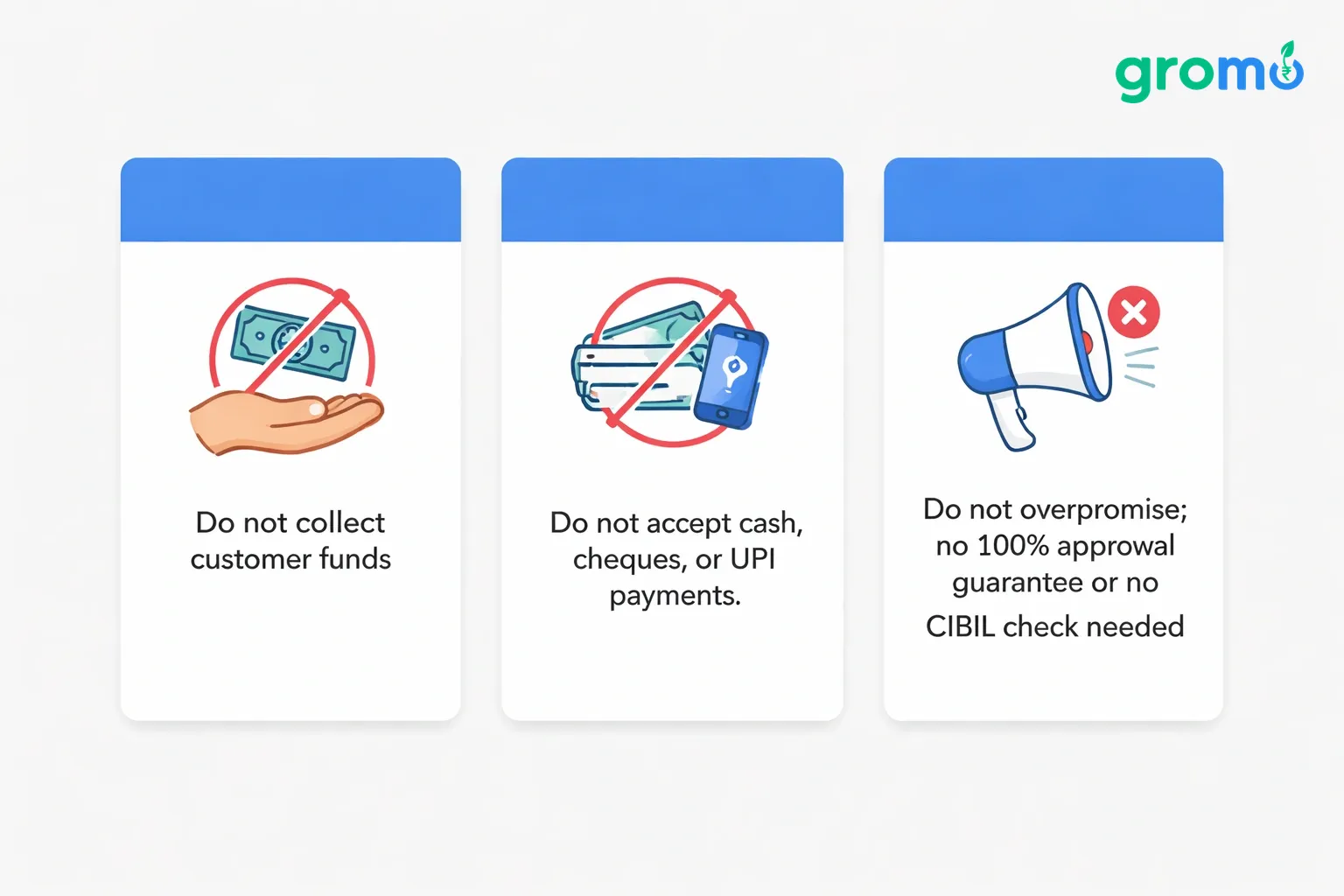

You're operating as an individual referral partner, not a registered financial advisor or NBFC. GroMo holds the institutional partnerships. You make introductions. Three rules matter:

Never collect customer funds. Don't accept cash, cheques, or UPI payments on behalf of banks. All transactions happen directly between customer and institution. Violating this voids your commission and can trigger legal action under Section 43 of the IT Act.

Don't overpromise. Claims like "100% approval guarantee" or "No CIBIL check needed" count as mis-selling. Stick to what's listed in GroMo's product descriptions. Gujarat's consumer forums processed 14,200 financial mis-selling complaints in 2025 don't become one of them.

Respect data privacy. Customer PAN, Aadhaar, and bank details entered through your link stay encrypted. Don't screenshot, store, or share this data. Penalties under the DPDP Act 2023 can reach ₹250 crore for breaches.

Commission income above ₹2.5 lakh annually counts as "income from other sources" under Section 56. File ITR-1 before July 31. If you're earning ₹50,000+ monthly, set aside 20% to 30% for taxes.

What People Are Actually Earning

GroMo's leaderboard shows 823 active partners in Gujarat as of June 2026. Most fall into a few buckets:

Part-timers working 5 to 10 hours weekly through personal networks typically see ₹5,000 to ₹15,000 monthly. That's about 42% of partners.

People running consistent WhatsApp and Instagram campaigns, activating 15 to 25 products monthly, see ₹15,000 to ₹40,000. That's 36%.

Full-timers who've diversified across products and run offline workshops see ₹40,000 to ₹80,000. That's 18%.

The top 4% people with referral teams, corporate tie-ups, and multi-level income see ₹80,000 to ₹1,50,000 monthly.

Priya Desai from Vadodara earned ₹1.23 lakh in April 2026: 18 credit cards (₹37,800), 11 business loans (₹28,500), 47 demat accounts (₹15,650), 28 savings accounts (₹19,600). She works about 25 hours a week, targeting textile MSME clusters and housing societies.

Why Gujarati Networks Give You an Edge

Gujarati business culture works in your favor. The "વેપારી સમાજ" (trading community) means almost every family has 2 to 3 self-employed members who need loans and merchant accounts. They travel for trade and value digital products like Tide Business Accounts or Kotak 811 that work anywhere. Word-of-mouth carries serious weight 67% of Gujaratis act on community recommendations versus 34% influenced by ads.

Join local business associations: Ahmedabad Management Association, Surat Diamond Association, Rajkot Chamber of Commerce. Attend monthly meetings. Sponsor a tea break (₹2,000). Hand out business cards with your GroMo QR code. A Surat partner converted 19 diamond traders in six months just by showing up consistently.

Common Questions People Ask

"Will people trust me without an office?"

Credibility comes from certification, not real estate. Complete GroMo's training, put your digital certificate on your WhatsApp status, share testimonials from your first few customers. Offer video calls to walk people through applications face time builds trust faster than an office visit.

"How do I compete with bank branches?"

You don't. Banks handle complex stuff like home loans and wealth management. You handle quick digital products credit cards for online shoppers, instant EMI cards for appliance buyers, demat accounts for first-time investors. Your advantage is speed and attention. Banks process 50 applications a day. You give five customers your full attention.

"What if I don't know finance jargon?"

GroMo gives you ready-made pitch scripts in English, Hindi, and Gujarati. Copy and paste. The app's chatbot answers 90% of customer questions. Forward the tough ones to GroMo's support team.

"Can I do this with a full-time job?"

Yes. 68% of GroMo partners work salaried jobs. Use lunch breaks and weekends. One hour daily generates 10 to 15 leads a week. Set up automated follow-ups with WhatsApp Business.

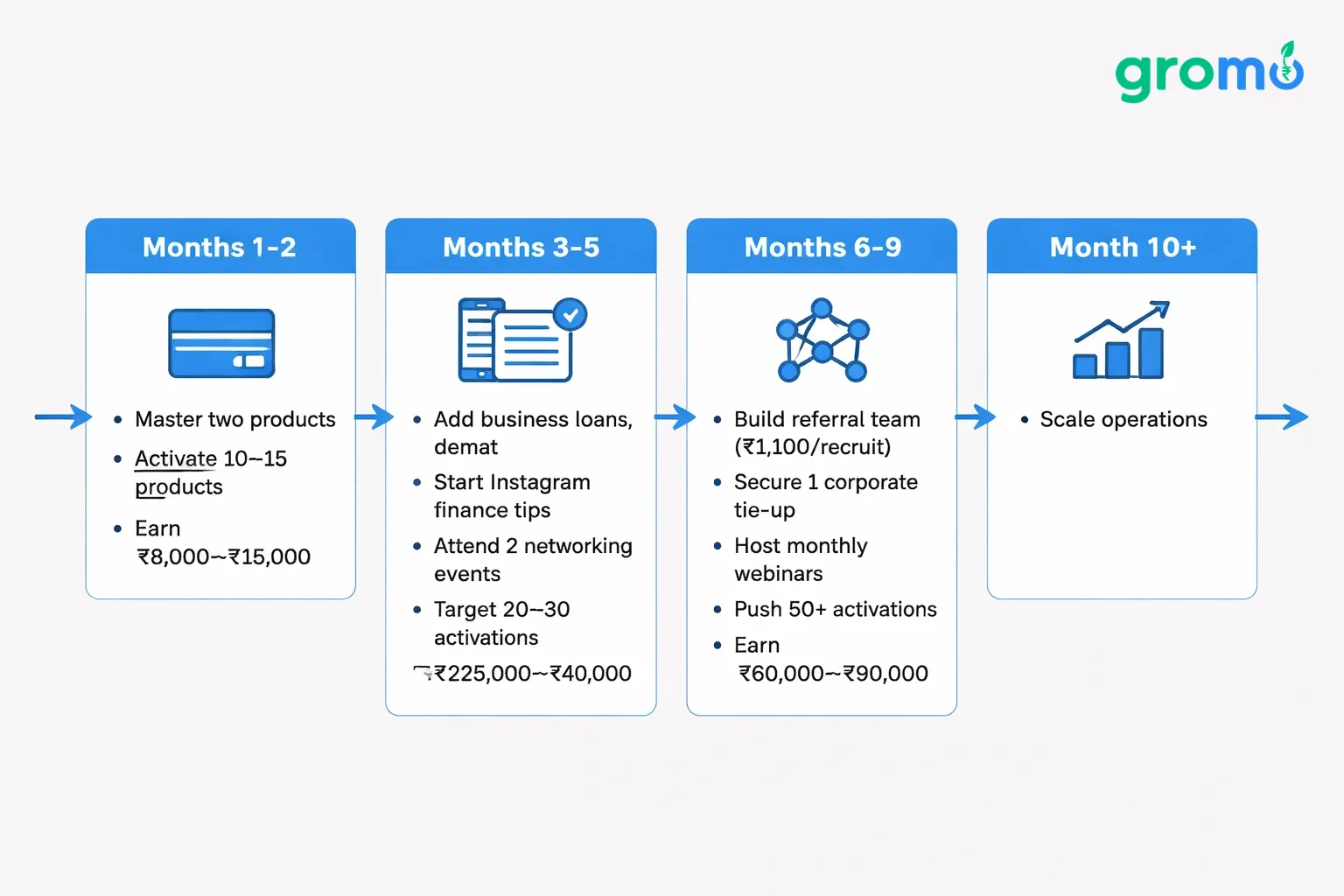

Growing from ₹10K to ₹1 Lakh

Months 1-2: Master two products one credit card, one savings account. Activate 10 to 15 products monthly through personal network. Expect ₹8,000 to ₹15,000.

Months 3-5: Add business loans and demat accounts. Start an Instagram page with Gujarati finance tips three times a week. Attend two networking events monthly. Target 20 to 30 activations. Expect ₹25,000 to ₹40,000.

Months 6-9: Build a referral team using GroMo's ₹1,100-per-recruit program. Secure one corporate tie-up for bulk employee onboarding. Host monthly webinars. Push 50+ activations. Expect ₹60,000 to ₹90,000.

Month 10+: Manage a team of five sub-partners, each activating 10 products. Move into high-ticket business loans and personal loans. Total activations: 80 to 100. Expect ₹1,00,000 to ₹1,50,000.

This takes consistency, not talent or capital. Gujarat's 823 active partners prove it works across cities, towns, and demographics.

How GroMo Compares to Other Options

| Model | Monthly Potential | Time to First Income | Capital | Scalability |

|---|---|---|---|---|

| GroMo | ₹10K – ₹1L+ | 5-7 days | ₹0 | High |

| Freelance Writing | ₹8K – ₹40K | 15-30 days | ₹0 | Medium |

| Instagram Affiliate | ₹5K – ₹60K | 60-90 days | ₹0 | Medium |

| Dropshipping | ₹10K – ₹80K | 30-45 days | ₹5K – ₹20K | Medium |

| Tutoring | ₹15K – ₹50K | 7-14 days | ₹0 – ₹10K | Low |

GroMo gives you immediate payouts, zero capital requirement, and the ability to scale through teams. Unlike money-earning games that pay ₹5 per hour, GroMo pays ₹500+ per closed sale. Unlike freelancing, your income isn't capped by billable hours.

Tools That Help

GroMo provides: 50+ WhatsApp templates in Gujarati, Hindi, and English; product explainer videos; commission calculator; lead tracker with reminders; digital certificate after certification.

What partners use: Canva (free) for Instagram posts and flyers; WhatsApp Business for automated greetings and follow-ups; Google Sheets to track outreach and conversion rates; Grammarly (free) to polish English pitches.

Learn more: GroMo's YouTube playlist on handling objections; RBI consumer education booklets; GroMo's Telegram community (8,600+ partners sharing tips).

Frequently Asked Questions

Do I need licenses or registrations?

No. You're an individual referral partner, not a registered financial advisor. GroMo holds the institutional partnerships. You make introductions. If your annual commission exceeds ₹2.5 lakh, file income tax returns under Section 56 as "income from other sources."

How long until I get paid?

Most payouts arrive in 48 to 72 hours after activation. Credit cards pay after the first transaction. Demat accounts pay after the first trade. Business and personal loans have a three-EMI monitoring period if the customer defaults, your commission gets clawed back. Savings accounts pay after video KYC and ₹500 funding.

Can I run Facebook or Google ads?

GroMo's terms prohibit paid ads that promise guaranteed approval or fixed income figures, or that use brand logos without permission. Organic social posts, WhatsApp sharing, and offline networking are fully allowed. If you want to run ads, contact GroMo's partner support for pre-approved materials.

What if a customer gets rejected?

You earn nothing for rejections. Use GroMo's eligibility checker to pre-qualify leads before they apply. For credit cards, CIBIL score above 700 and monthly income above ₹25,000 gives 80%+ approval odds. For business loans, Udyam registration and six months of bank statements help a lot.

Is this sustainable?

Partners who treat this as a real business consistent outreach, skill building, team development sustain and grow income year over year. India's credit card base will hit 150 million by 2027 (up from 95 million in 2024). Demat accounts are projected to reach 200 million (from 140 million). MSME lending is growing 18% annually. Demand for financial products isn't going away. Your role as a trusted connector becomes more valuable as banks compete harder for customers.

How do I handle complaints?

You're not responsible for bank operations. Direct customers to the provider's helpline (listed in the GroMo app under each product). Your role ends at referral. That said, occasionally following up with the bank on your customer's behalf builds goodwill and generates repeat referrals.