Earn ₹50K-Monthly Selling Financial Products in Pune with GroMo

Pune has a lot of freelancers and startups. That makes it a solid place to sell financial products on commission using GroMo. You can make ₹50,000–₹1,00,000 a month selling credit cards, loans, and demat accounts without spending money on inventory or office space.

This guide covers how to do it. We'll look at who buys what in Pune, how much you can actually earn, and how to avoid the mistakes that get your account banned.

Why Pune specifically?

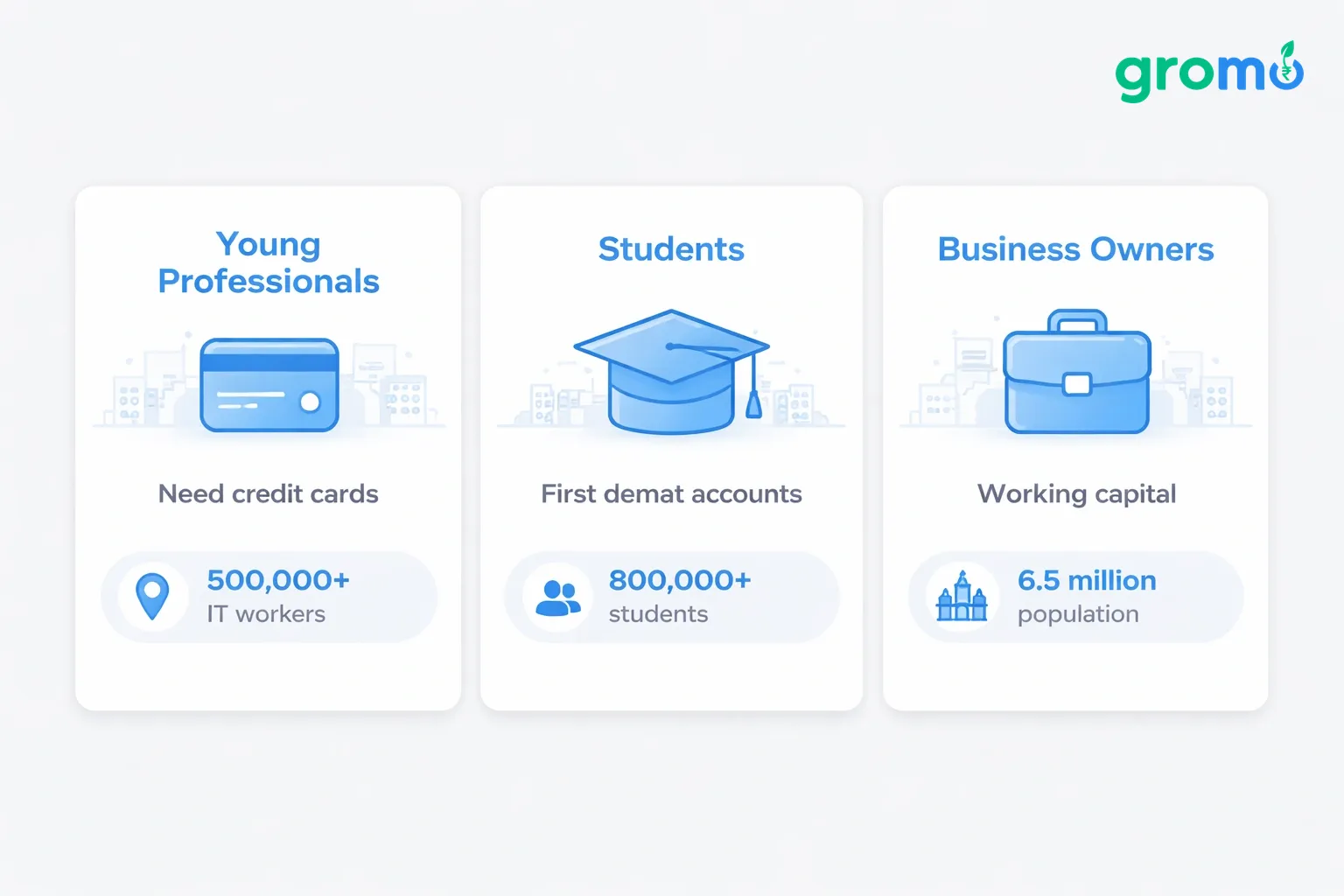

You've got IT hubs in Hinjewadi and Magarpatta, 40+ engineering colleges, and a busy small-business sector. That gives you three clear customer types: young professionals who need credit cards, students opening their first demat accounts, and business owners looking for working capital.

The city has 6.5 million people, including 800,000+ students and 500,000+ IT workers. These are people who buy financial products regularly. You don't need a shop on FC Road to reach them. You just need a phone.

People in Pune are becoming more financially literate, but good advice is still hard to find. Banks pay well to anyone who can bridge that gap. That makes financial product distribution a viable side hustle right now.

What you can sell

Credit cards

You earn ₹600–₹2,400 per approved card. IT professionals in Baner, Aundh, and Viman Nagar are the best targets. They usually have the credit scores to qualify for premium cards.

Share links on WhatsApp or LinkedIn. Don't just blast a link explain why a specific card makes sense for them. If you get 20 approvals a month at an average of ₹1,200, that's ₹24,000.

GroMo works with Axis Bank, IDFC FIRST, and Kotak. The ₹2,400 per credit card referral payouts usually come when you help customers understand the rewards structure. Don't be a salesperson; be the person who explains the fine print.

Personal loans

Commissions are 2%–5.5% of the loan amount. A ₹2 lakh loan gets you ₹4,000–₹11,000. The demand is there: gig workers in Swargate, small business owners in Hadapsar, people renovating their homes.

GroMo partners include Prefr, Poonawalla Fincorp, and Aditya Birla. The process is digital KYC via DigiLocker, approval in 12–24 hours. You don't handle paperwork.

Focus on people who actually need the money: self-employed folks buying equipment, salaried employees consolidating debt. Be clear about EMI terms. Making money online in India this way works better when you solve a real problem for the customer.

Demat accounts

You get ₹250–₹400 per account. Pune added 150,000 new investors in 2025. Target students in Kothrud and tech workers in Hinjewadi.

GroMo offers Upstox and Aditya Birla Money accounts. It takes 10 minutes: PAN check, Aadhaar e-KYC, linking a bank account. You get paid when they make their first trade.

You might need to teach them how it works. Explain IPOs or SIPs. Share a quick story about a local investor. This zero-investment business model scales because people tell their friends.

Business loans

Commissions are 1.5%–3% for loans up to ₹50 lakh. Manufacturers in Pimpri-Chinchwad and retailers on Laxmi Road always need working capital. A ₹10 lakh loan earns you ₹15,000–₹30,000.

Partners like ClickPe-Muthoot and Poonawalla Fincorp offer same-day payouts. They just need PAN, Aadhaar, GST or Udyam registration, and bank statements. No collateral for loans under ₹5 lakh.

Go to local business meetups or co-working spaces like 91Springboard in Viman Nagar. Find out what they need inventory money, new equipment and match them with a loan. Being a financial distribution partner here pays well because the ticket sizes are big.

Savings accounts

Tide Business Banking pays ₹300–₹650 per account. Pune's founders and freelancers need business accounts but hate the paperwork at traditional banks.

Tide is instant, zero-balance, and gives 1.5% cashback on UPI. Customer downloads the app, does VKYC, adds ₹50. You get paid. More payouts follow if they use the card.

Target gig workers in Kalyani Nagar or shop owners in Kothrud. Show them the math: if they spend ₹20,000 on UPI a month, they save ₹3,600 a year. This zero-investment income idea works because the benefit is obvious.

Getting customers in Pune

Use WhatsApp groups

Pune has thousands of WhatsApp groups for housing societies, colleges, and professional networks. Join them. Answer questions about finance. When someone asks about a credit card, DM them your link.

Don't spam. If you spam, you get kicked out. Instead, be the helpful person. "Need a card with low forex fees? Try this one."

Build your own broadcast list. Share tips on saving tax or improving credit scores. Then share a product link occasionally. This referral income strategy works because it's based on trust.

Try co-working spaces and cafés

Freelancers at WeWork or Awfis need business accounts and loans. Offer to do a free "financial health check." Check their credit score, suggest a product, share your link.

Do the same at cafés in Koregaon Park or FC Road. Host a casual meetup: "Coffee & Finance." Talk about demat accounts. It works because face-to-face builds trust. Once they trust you, they refer friends. This part-time job approach creates a steady stream of leads.

Make content for Pune

Post on Instagram or YouTube. Use local keywords: "Best credit cards for Hinjewadi techies" or "How Symbiosis students can start investing." Speak in Marathi and English if you can. It makes you relatable.

Run Facebook ads targeting 25–40 year olds in Baner or Wakad. A ₹500 ad can reach 20,000 people. Even a 0.5% conversion is 100 leads.

Or find a Pune micro-influencer. Offer them a cut if they promote your link. It's a scalable model, similar to what works in Mumbai and Bangalore.

The money part

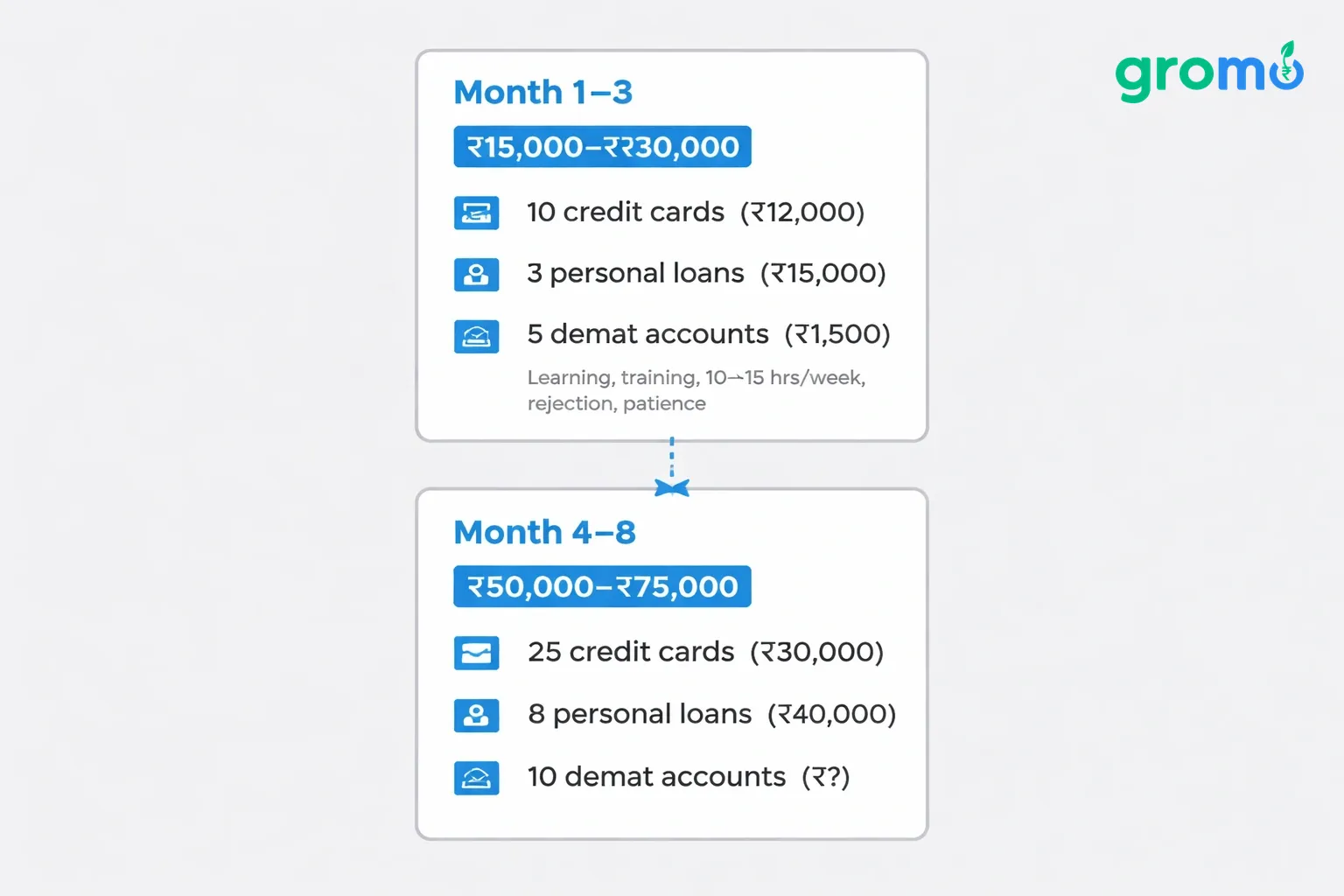

Month 1–3: ₹15,000–₹30,000

You start with friends and family. If you get 10 credit cards (₹12,000), 3 personal loans (₹15,000), and 5 demat accounts (₹1,500), you're at ₹28,500.

This phase is about learning. Do the GroMo training. Figure out your pitch. Most people in Pimpri-Chinchwad start here, working 10–15 hours a week.

It's not easy. You'll face rejection. The commission-based income model needs patience. But the effort adds up.

Month 4–8: ₹50,000–₹75,000

Now you're using community groups and local partners. Aim for: 25 credit cards (₹30,000), 8 personal loans (₹40,000), 10 demat accounts (₹3,000), 2 business loans (₹30,000). Total: ₹1,03,000.

You have templates now. You use the CRM. You work 20–25 hours a week. It's a serious side income source.

Partners near IT corridors like Hinjewadi hit this level faster. They have access to high earners. The shift is from waiting for leads to finding them.

Month 9+: ₹1,00,000+

Top partners earn ₹1.5–2 lakh monthly. They have teams. They recruit sub-partners and earn a cut of their sales.

Breakdown: 40 credit cards (₹48,000), 15 personal loans (₹75,000), 20 demat accounts (₹6,000), 5 business loans (₹75,000), plus ₹30,000 from team overrides. Total: ₹2,34,000.

This is 30–40 hours a week. It's a full-time job. You run ads, do webinars, maybe run a YouTube channel. This is the ₹1 lakh/month benchmark it's real, but it's hard work.

Who buys what?

Salaried IT professionals (50% of Pune market)

Sell them premium credit cards, personal loans for home upgrades, and demat accounts. They have good credit and stable income.

Your pitch: "Use a card that gives you 5% cashback. Invest ₹10k a month in an index fund. It adds up." Use data.

Students and young adults (30% of market)

Sell them first credit cards (secured cards), demat accounts for small investments, and savings accounts. They refer friends.

Your pitch: "Start investing ₹500 a month now. You'll thank yourself later." Use aspiration. Run campus ambassador programs at Fergusson or Symbiosis.

SME owners and entrepreneurs (20% of market)

Sell them business loans and Tide accounts. This pays the most per sale.

Your pitch: "Get ₹5 lakh working capital today. No collateral." Go to MCCIA events. Network.

Don't get banned

Don't promise jobs or fixed returns

GroMo is commission-only. Don't say "guaranteed income." The earning potential depends on sales.

If you mislead people, you'll face backlash. Always be clear: this is variable income.

Keep data private

Don't share PAN or Aadhaar info. GroMo handles KYC securely. You just facilitate.

If you violate privacy rules (DPDP Act 2023), you can lose your account. Pune's tech crowd cares about privacy. Respect it.

Watch out for clawbacks

If a customer defaults on the first 3 EMIs, you lose the commission. Make sure they can pay before you sign them up.

Check income stability for credit cards. Explain EMI terms for loans. This protects your money and your reputation. Read the product documentation to know the rules.

Scaling outside Pune

Once you know the drill in Pune, try Nashik, Ahmednagar, or Solapur. Rural Maharashtra has 110 million people with phones but few advisors.

Use your Pune stories as proof. "Helped 200 people in Pune now helping Satara." Gujarat's market works similarly.

Or go niche. Be the person for "startup business loans in Pune" or "student investments." Niche focus builds trust. Some partners make ₹2 lakh+ just from one category.

Tools you get

GroMo Academy

Free training on credit, loans, and sales. Show your certificate on LinkedIn. It helps when pitching to educated clients.

In-app CRM

Track leads, set reminders, see status. Tag people by area ("Hinjewadi IT") for targeted pitches.

Marketing templates

Get pre-made WhatsApp messages and email drafts. Add Pune references: "Hate Hinjewadi traffic? Work from home with GroMo."

Payout dashboard

See earnings in real time. Know which sale paid out and when. GroMo pays fast.

Taxes and legal stuff

GST

If you make over ₹20 lakh a year, you need GST registration. Most beginners don't hit this. Ask a CA.

Income tax

Report commissions as "Income from Business or Profession" in ITR-3 or ITR-4. Deduct internet and phone costs.

Insurance

Think about professional indemnity insurance (₹5–10 lakh cover) if you're advising on big loans. It costs about ₹3,000 a year. It protects you if a customer sues.

Set aside 10% of earnings for taxes. Pune is business-friendly, but the rules still apply. Check RBI-approved loan app guidelines to stay safe.

Real examples

Rahul from Wakad is a 28-year-old software engineer. He makes ₹65,000 a month selling to his colleagues on LinkedIn. He focuses on premium credit cards and uses his tech background to build trust.

Priya from Kothrud is a homemaker. She makes ₹40,000 a month through WhatsApp groups and kitty parties. She sells personal loans and savings accounts. It's similar to the housewife earning potential stories GroMo shares.

Amit from Pimpri-Chinchwad is a consultant. He crossed ₹1.2 lakh monthly by specializing in MSME business loans. He uses his existing clients as leads.

These aren't fake stories. GroMo has 60 lakh+ partners earning a collective ₹100 crores. Pune is one of the top cities for this because of the mix of tech, education, and money.

FAQs

Q: Can I start without financial knowledge? A: Yes. GroMo has free training. Most partners started as teachers or engineers. They learned on the job.

Q: How much time for ₹50,000 monthly? A: About 20–25 hours a week. It takes more time at the start. Later, you have systems that make it faster.

Q: Are there hidden fees? A: No. No registration fee, no subscription. You need a phone and internet. The tools are free.

Q: Which areas convert best? A: IT hubs (Hinjewadi, Magarpatta) for cards and loans. Colleges (Kothrud) for demat. Industrial areas (Pimpri-Chinchwad) for business loans.

Q: How fast are payouts? A: Within 24–72 hours after approval. Some products have milestone payouts, but most are instant.

Q: Can I do this with a full-time job? A: Yes. 70% of partners do. Work evenings or weekends. Use your lunch break to follow up.