Small Franchise Businesses in India: Pros, Cons & Zero-Investment Alternatives

Small franchise businesses in India let you skip the "building from zero" phase. You get a brand, a system, and a playbook. The catch: you pay for it, and you keep paying.

Investments range from ₹50,000 for a food kiosk to ₹10 lakhs for a retail outlet. But the price tag doesn't determine success. Location does. Brand strength does. How efficiently you run operations does.

Franchise models also lock you into fixed royalty payments, territorial restrictions, and brand guidelines. Before you commit capital to a franchise agreement, you should at least look at zero-investment income models like financial product distribution through GroMo. Comparable or higher earnings, no upfront fees, no franchise obligations, no geographical constraints. Worth understanding before signing anything.

Understanding Small Franchise Business Models in India

A franchise is a licensing arrangement. An established brand (the franchisor) grants an individual (the franchisee) the right to operate under their trademark and business system. You pay an initial fee plus ongoing royalties usually 5-10% of gross revenue. In exchange, you follow their operational standards, marketing guidelines, and product specifications.

The value proposition is straightforward: you get brand equity and proven systems without the trial-and-error phase. Indian franchises span food and beverage (chai stalls, ice cream parlors), retail (cosmetics, apparel), education (tutoring centers, coding classes), and services (laundry, fitness). Investment requirements vary from ₹25,000 for mobile-cart food franchises to ₹20 lakhs for established retail brands.

The agreement typically includes training programs, operational manuals, supplier networks, and marketing support. But you sacrifice autonomy. Pricing, product selection, and vendor choices are predetermined. Profit margins after royalty payments, rent, and labor typically run 15-25%. Location selection and operational efficiency determine whether you survive.

Lowest Investment Franchise Options for 2026

Food and Beverage Franchises dominate the budget segment. Chaayos Chai Point kiosks start at ₹3-5 lakhs with 6-8% royalty. Giani's Ice Cream parlors require ₹5-7 lakhs. Amul Ice Cream distributorships need ₹2-3 lakhs for freezer deposits and initial stock. These models benefit from brand recognition and centralized supply chains. They depend heavily on foot traffic. Seasonal demand fluctuations can hurt.

Retail and Service Franchises offer alternatives. Jawed Habib Salon franchises begin at ₹10-15 lakhs including equipment and training. Kirana Now grocery store partnerships require ₹5-8 lakhs. These provide recurring revenue streams but face intense competition from digital commerce. They also require skilled staff management to maintain service standards.

Mobile and Cart-Based Models have the lowest barrier to entry. Subway sandwich carts operate at ₹1.5-2 lakhs. Ice-cream bicycle franchises from local brands start at ₹25,000-50,000. These minimize real-estate costs but limit growth potential. They also face regulatory challenges regarding municipal permits and hygiene certifications across different cities.

Start Earning Without Franchise Fees – Download GroMo

Hidden Costs Beyond the Initial Franchise Fee

Franchise agreements list an initial fee. The operational reality includes multiple ongoing expenses that sales pitches gloss over.

Royalty payments typically range 5-10% of gross revenue regardless of profitability. A franchise generating ₹2 lakh monthly pays ₹10,000-20,000 in royalties before accounting for rent, inventory, or salaries. This reduces net margins significantly.

Marketing contributions add another 2-4% of revenue to centralized brand campaigns. This builds overall brand equity, but local franchisees see uneven benefits. A TV campaign increases urban awareness but provides limited value in tier-3 towns. These mandatory contributions drain working capital without guaranteeing proportional returns at the individual outlet level.

Renovation and compliance costs emerge during operations. Franchisors mandate periodic store upgrades, equipment replacements, and technology adoptions. A café franchise might require a ₹2 lakh interior refresh every 3-4 years. Non-compliance can trigger agreement termination, forcing franchisees to absorb sunk costs without recourse.

Comparing Franchise Business vs Financial Product Distribution

Traditional franchises lock capital into physical infrastructure rent deposits, equipment, inventory. This creates exit barriers. A ₹10 lakh franchise investment becomes illiquid. Selling requires franchisor approval, transfer fees, and finding buyers who meet brand criteria. During economic downturns, franchisees absorb losses while continuing royalty obligations regardless of performance.

Financial product distribution through platforms like GroMo requires zero upfront investment and no fixed costs. Partners earn commissions on credit card referrals (₹500-3,000), loan applications (0.5-3.5% of disbursement), and savings account openings (₹250-1,010) without inventory, rent, or franchise fees. Earnings scale with effort rather than territorial restrictions or brand-imposed volume targets.

The flexibility differential matters for working professionals and part-time entrepreneurs. Franchise operations demand 10-12 hour daily commitments, physical presence, and staff management. Financial product distribution operates remotely. Partners share product links via WhatsApp, explain benefits over calls, and track applications through mobile dashboards while maintaining existing employment.

Location Selection Strategies for Physical Franchises

Footfall analysis determines viability for retail and food franchises. Locations generating 500+ daily footfalls (near colleges, metro stations, office complexes) justify premium rents of ₹1-2 lakh monthly. Calculate break-even: if average transaction value is ₹150 and margin after royalties is 20%, you need 100 daily transactions generating ₹15,000 to cover ₹45,000 in base costs.

Competition mapping prevents market saturation. Franchisors promise territorial exclusivity but definitions vary. A "protected territory" of 2 km radius in dense urban areas overlaps with multiple similar brands. Survey existing competitors. If three similar coffee franchises operate within 500 meters, market share dilution makes profitability challenging regardless of brand strength.

Accessibility and parking drive customer convenience. Ground-floor locations with visible signage and two-wheeler parking convert significantly higher than first-floor outlets requiring navigation. Rent differentials of 20-30% between ground and first floors pay back through 15-20% higher walk-ins. Negotiate lease terms carefully. Longer tenures (5-7 years) provide stability but lock you into unviable locations if market dynamics shift.

Operational Challenges in Small Franchise Management

Inventory and wastage control hit profitability directly. Food franchises face 8-12% spoilage rates. An ice-cream parlor purchasing ₹50,000 monthly inventory loses ₹4,000-6,000 to expired stock. Centralized franchise supply chains often prohibit alternative sourcing, preventing cost optimization even when local suppliers offer 15-20% savings.

Staff recruitment and retention create constant friction. Quick-service franchises require 3-5 employees with specific training. Monthly wage costs of ₹60,000-80,000 compound with 30-40% annual attrition. Retraining cycles reduce service quality. Franchise standardization demands skill levels that budget wages cannot reliably attract in competitive labor markets.

Compliance and inspections multiply regulatory burdens. Food licenses (FSSAI), fire safety certificates, municipal trade licenses, and GST registrations all require navigation. Franchise brands mandate their own standards exceeding regulatory minimums, increasing compliance costs. A single FSSAI violation triggers brand audits, potential fines, and reputational damage.

Financial Projections and Break-Even Timelines

Most small franchises project 18-24 month break-even periods. Ground realities often extend timelines.

Calculate conservatively: a ₹8 lakh food franchise generating ₹2.5 lakh monthly revenue with 22% net margins yields ₹55,000 monthly profit. Deducting franchise royalties (₹12,500) and marketing fees (₹5,000) leaves ₹37,500. That's 21 months to recover initial investment assuming everything goes according to plan.

Factor ramp-up periods where initial months generate 40-60% of projected revenue while costs remain constant. First six months typically run losses or minimal profits as brand awareness builds locally. Working capital requirements of 3-4 months' operating expenses (₹2-3 lakhs) add to initial outlay but rarely appear in franchise promotional literature.

Seasonal variations affect specific categories disproportionately. Ice-cream franchises generate 60-70% of annual revenue during March-September. Education franchises peak during admission cycles. Annual profitability averaging requires surviving low-revenue months without compromising quality or staffing demanding financial reserves that small franchisees often lack.

Earn ₹1 Lakh Monthly Without Physical Stores – Join GroMo

Due Diligence Before Signing Franchise Agreements

Existing franchisee validation reveals operational realities. Franchisors provide "model" outlet financial projections, but actual multi-unit franchisee performance tells the real story. Visit 5-7 existing franchises. Speak to owners during off-peak hours. Ask direct questions about actual revenues, hidden costs, and franchisor support quality versus promises made during sales pitches.

Agreement clause scrutiny prevents future disputes. Examine renewal terms. Do fees increase at predetermined rates? What triggers termination? Can the franchisor buy back underperforming outlets at book value or market rates? Legal review by franchise-experienced attorneys costs ₹15,000-25,000 but prevents expensive litigation and protects interests during conflicts.

Financial health verification of the franchisor matters critically. Request audited financial statements, expansion plans, and existing franchisee count growth rates. Rapidly expanding brands diluting territories or facing negative cash flows pose higher risks. Franchise brands with stable, profitable multi-unit franchisees indicate sustainable systems versus aggressive expansion models prioritizing fee collection over franchisee success.

Digital Alternatives to Physical Franchise Models

India's digital economy enables earning models without franchise constraints. Social commerce, content creation, and affiliate marketing allow individuals to build audiences and monetize without inventory or territorial limits. Platform-based businesses eliminate lease agreements, staffing challenges, and physical infrastructure while reaching national markets.

Financial product referral programs specifically offer commission structures comparable to franchise profit margins without capital requirements. Selling credit cards yields ₹500-3,000 per approval, personal loans pay 0.5-2.25% of disbursement, and demat account referrals generate ₹250-1,400. A partner referring 20 credit cards and 5 loans monthly earns ₹40,000-60,000 without franchise fees or physical presence.

The zero-investment model through GroMo includes free training programs, compliance certification, customer management tools, and instant payout cycles matching franchise "support" without restricting autonomy. Partners customize their product portfolios, target customers based on personal networks, and scale efforts according to time availability rather than franchisor-mandated operational hours.

Franchise Exit Strategies and Resale Challenges

Franchise agreements rarely include clear exit mechanisms favorable to franchisees. Most contracts grant franchisors first right of refusal at "fair market value" a term interpreted unilaterally. A franchisee building a profitable outlet might expect 2-3x annual profit valuations, but franchisors often cite brand equity belonging to them, limiting exit proceeds to equipment depreciated value plus inventory.

Transfer approval processes create friction. Prospective buyers must meet all original franchisee criteria, undergo training, and pay transfer fees (5-10% of initial franchise fee). This narrows buyer pools significantly. During economic downturns, finding qualified buyers willing to invest becomes nearly impossible, trapping franchisees in underperforming businesses.

Closure costs compound exit difficulties. Lease break-penalties, staff severance, equipment disposal, and franchisor termination fees accumulate. A franchisee closing a ₹10 lakh investment often recovers ₹3-4 lakhs after all exit costs representing 60-70% capital loss plus opportunity costs of time and effort invested over operational years.

Legal and Contractual Considerations in Franchise Agreements

Indian franchise agreements lack standardized regulation compared to markets like the USA. The Franchising Association of India provides voluntary guidelines, but legal enforceability depends on contract-specific terms. Franchisees operate as independent businesses bearing all risks while franchisors maintain control without profit-sharing obligations an inherently imbalanced structure.

Dispute resolution clauses typically favor franchisors through arbitration in their home jurisdiction. A Delhi-based franchisee operating in Bangalore might face arbitration proceedings in Delhi, increasing legal costs and procedural disadvantages. Examine jurisdiction clauses carefully and negotiate neutral arbitration locations during initial agreement stages.

Intellectual property protection cuts both ways. While franchisees benefit from established trademarks, they cannot build independent brand equity. Years of customer relationship-building legally belongs to the franchisor. Post-termination non-compete clauses (typically 2-3 years within protected territories) prevent leveraging accumulated expertise and customer goodwill in similar businesses limiting future entrepreneurial options.

Scalability and Growth Potential in Franchise vs Digital Models

Multi-unit franchise ownership appears attractive but requires proportional capital multiplication. Adding three more outlets demands 3x investment, separate staff teams, and divided management attention. Many single-unit franchisees discover operational complexity increases exponentially. Three outlets require 5x management effort, not 3x, due to coordination overhead.

Digital financial product distribution scales linearly without capital constraints. A partner earning ₹30,000 monthly from 50 customer interactions can double income to ₹60,000 by doubling effort to 100 interactions. No additional infrastructure, staff, or franchise fees required. Top GroMo partners earning ₹1 lakh+ monthly expand through team-building and referral networks rather than capital deployment.

The growth trajectory differential matters. A franchisee building three outlets over five years invests ₹30 lakhs total and manages operational complexity. A financial product distributor investing zero capital over the same period builds customer databases, product expertise, and reputation-based referral networks that compound returns without proportional time increases creating genuinely passive income streams.

Tax Implications and Financial Documentation

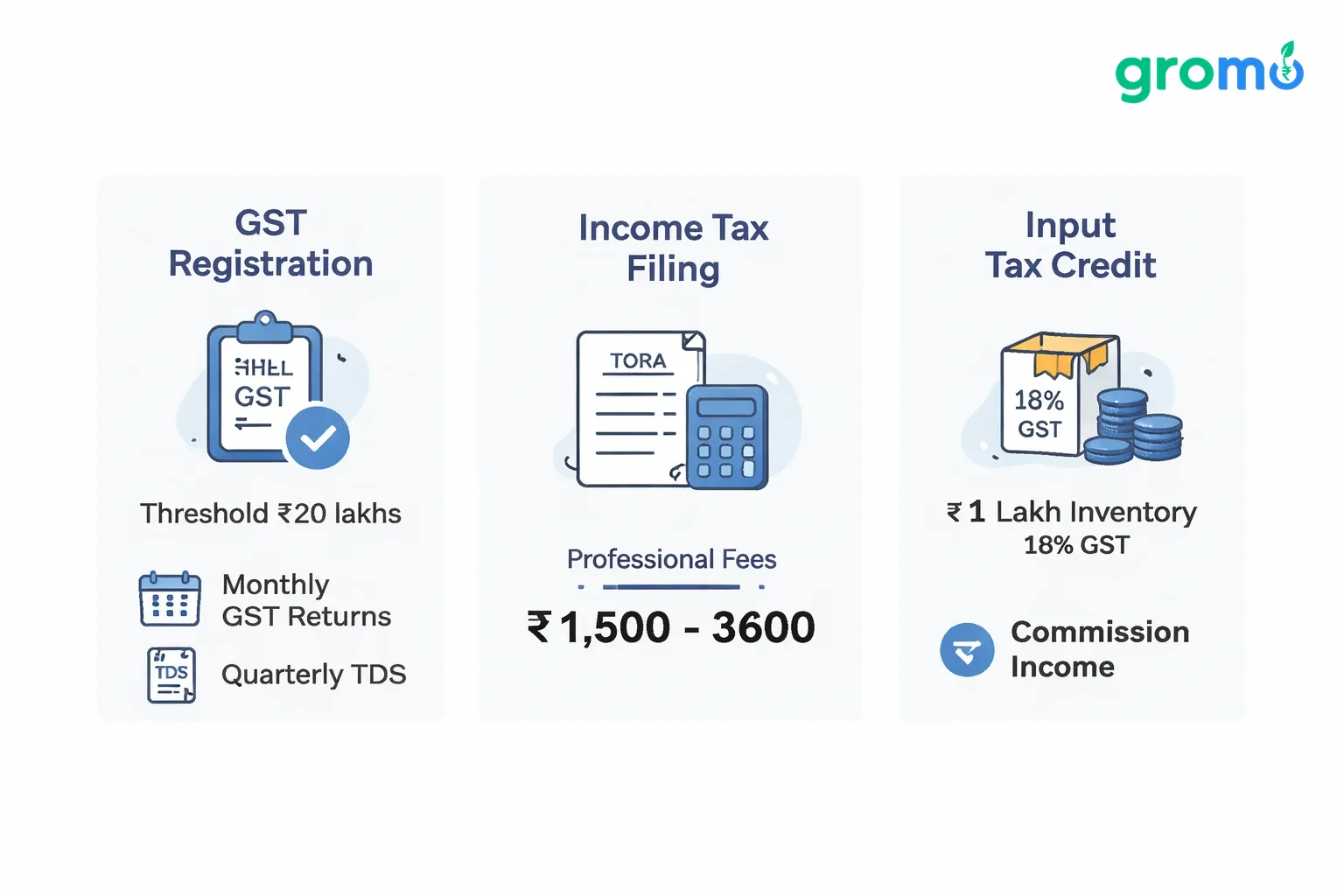

Franchise businesses operate as registered entities proprietorships, partnerships, or private limited companies requiring GST registration (mandatory for turnover exceeding ₹20 lakhs), income tax filings, and TDS compliance. Monthly GST returns, quarterly TDS returns, and annual income tax filings demand accounting expertise. Professional fees of ₹1,500-3,000 monthly add to operating costs.

Input tax credit benefits depend on vendor compliance. Franchise supply chains typically enable full GST credit recovery, but local purchase constraints reduce optimization opportunities. A franchisee purchasing ₹1 lakh monthly inventory at 18% GST pays ₹18,000 but recovers this only if output sales generate equivalent or higher GST liability creating cash flow timing mismatches.

Commission income through platforms like GroMo simplifies tax treatment. Partners receive income as business income (requiring ITR-3/ITR-4 filings) but without GST obligations unless annual commissions exceed ₹20 lakhs. Simplified book-keeping, lower compliance burden, and reduced professional fees make financial management significantly more accessible for part-time participants.

Insurance and Risk Management Considerations

Physical franchises require comprehensive insurance coverage property, liability, fire, theft, and business interruption. Annual premiums of 2-3% of asset value add ₹15,000-40,000 to operating costs. Underinsurance to reduce premiums exposes franchisees to catastrophic losses. A fire destroying ₹8 lakh in assets might yield ₹3 lakh claim settlements if declared value was ₹4 lakh.

Liability exposure from customer injuries, food poisoning, or product defects creates ongoing risk. While franchise agreements typically indemnify franchisors, franchisees bear primary liability as operators. A single litigation case even if eventually dismissed consumes ₹50,000-1,00,000 in legal fees and management time, disrupting operations.

Digital business models eliminate physical asset risks entirely. Financial product distribution carries no inventory, premises, or customer liability exposure. Compliance violations trigger at most commission reversals the clawback mechanism on first 3 EMI defaults represents the maximum downside, capped at earned commission amounts rather than multiplying through legal battles or asset losses.

Training and Skill Development Requirements

Franchise training programs span 1-4 weeks covering operations, customer service, inventory management, and brand standards. Initial training appears comprehensive, but ongoing skill development depends on franchisee initiative. Technology updates, menu changes, and operational refinements require continuous learning a commitment franchisees often underestimate during the excitement of launching ventures.

Staff training responsibilities fall entirely on franchisees despite brand standardization requirements. Training new hires every 3-4 months due to attrition creates perpetual onboarding cycles. Franchise-provided training materials help but cannot replace hands-on skill transfer. Service quality degradation during staffing transitions directly impacts customer satisfaction and revenue.

GroMo's free certification programs train partners on financial product features, regulatory compliance, customer handling, and sales techniques. Unlike franchises requiring travel to training centers, digital certification completes through mobile apps. Ongoing webinars, product updates, and sales strategy workshops maintain skill currency without operational disruption enabling continuous improvement parallel to earning activities.

Technology and Digital Infrastructure Needs

Modern franchises mandate POS systems, inventory management software, and digital payment integration representing ₹50,000-1,50,000 in hardware and ₹2,000-5,000 monthly software subscriptions. Technology obsolescence requires upgrades every 3-4 years. Cloud-based systems reduce upfront costs but create permanent operational dependencies on internet connectivity and subscription services.

Digital marketing obligations imposed by franchisors require managing social media presence, Google My Business listings, and review responses. While brand provides templates, execution demands 5-10 hours weekly. Hiring digital marketing help costs ₹8,000-15,000 monthly another line item rarely discussed during franchise sales pitches.

Financial product distribution operates entirely through mobile applications like GroMo requiring smartphones partners already own. Customer management, application tracking, commission monitoring, and payout tracking integrate into single platforms. Zero additional technology investment required. Partners start earning within hours of downloading apps rather than weeks of infrastructure setup.

Market Saturation and Competitive Positioning

Popular franchise brands face market saturation in urban centers. Ten similar café franchises within 2 km radius dilute customer traffic. Brand recognition becomes commoditized when excessive outlets undermine scarcity value. Franchisees discover they're competing against fellow brand partners rather than just external competitors a conflict of interest inherent in aggressive franchise expansion models.

Differentiation limitations under franchise contracts prevent local adaptation. A franchisee identifying customer preference for specific menu variations cannot implement changes without corporate approval. This rigidity causes gradual market share erosion to independent competitors who adapt faster to local tastes, pricing sensitivities, and cultural preferences.

Financial product markets remain undersaturated with distribution partners. India's 140 crore population includes 90 crore adults, but only 3-4 crore hold credit cards and 8-10 crore have demat accounts. Distribution opportunity measured in tens of crores of potential customers vastly exceeds current intermediary capacity. Competition exists but market size accommodates unlimited new entrants earning sustainably.

Funding Options for Franchise Investments

Banks offer franchise-specific loans at 11-14% interest rates with 30-40% margin money requirements. A ₹10 lakh franchise needs ₹3-4 lakh own funds plus ₹6-7 lakh debt. EMI of ₹18,000-22,000 monthly for 5-year tenure strains cash flows during initial break-even periods when profits barely cover operating expenses.

MUDRA loans under Pradhan Mantri Mudra Yojana provide up to ₹10 lakh at subsidized rates (8-10%) without collateral for small business ventures including franchises. Processing times of 2-3 months and documentation requirements (business plan, franchisee agreement, financials) delay launches. Approval rates vary significantly across banks based on franchise brand reputation.

Zero-debt business models eliminate interest burdens entirely. Starting financial product distribution through GroMo requires no loans, no EMIs, and no repayment pressures. Every rupee earned is net income after effort no interest servicing, no working capital loans, and no debt-induced stress during income fluctuation months.

Time Commitment and Work-Life Balance Impact

Franchise operations demand 60-80 hour work weeks during initial years. Physical presence requirements, staff management, inventory oversight, and customer service necessitate 10-12 hour daily commitments. Weekend and holiday operations prevent traditional time off. Many franchisees report work-life balance deterioration the independence of entrepreneurship transforms into 24/7 responsibility.

Family involvement becomes necessary for survival in small franchises. Spouses manage counters, children help during peak hours, parents oversee operations during owner absences. While reducing staff costs, this unpaid family labor creates household stress and limits social mobility for all members trapped in business operations.

Remote earning through financial products enables flexible time allocation. Partners dedicate 2-3 hours daily during commutes, lunch breaks, or evenings maintaining full-time employment or other businesses simultaneously. The work-from-anywhere model allows geographic flexibility impossible with location-bound franchises. Top earners structure sales activities around existing schedules rather than rebuilding lives around business requirements.

Success Rate Statistics and Ground Realities

Industry estimates suggest 30-40% of franchises shut down within first three years higher than often-cited "90% failure rate" for independent startups but nowhere near guaranteed success promotional materials suggest. Survival bias makes visible successful franchises while failed outlets disappear quietly. Franchisor-provided success stories showcase outliers rather than median outcomes.

Location lottery determines outcomes as much as effort. An identical franchise concept succeeds spectacularly in one location and fails completely 2 km away due to micro-market dynamics. Traffic patterns, demographic composition, competitor proximity, and parking availability create wildly divergent results impossible to predict reliably during site selection.

Skill-based earning models reduce luck dependencies. Financial product distribution success correlates directly with communication skills, product knowledge, and network size factors entirely under individual control. While market conditions affect overall conversion rates, partners consistently applying proven sales techniques generate predictable monthly incomes regardless of geographic accidents.

Frequently Asked Questions

Q: What is the cheapest franchise to start in India?

A: Mobile cart and kiosk franchises represent the lowest entry points, ranging from ₹25,000-50,000 for ice-cream bicycle franchises to ₹1.5-2 lakhs for branded food carts like Subway. However, these models limit growth potential and face regulatory challenges. Digital alternatives like GroMo require zero investment while offering comparable or higher earning potential through financial product commissions.

Q: Can I start a franchise with 20k?

A: Legitimate branded franchises rarely operate below ₹50,000 minimum investment due to equipment, training, and initial inventory costs. Options at ₹20,000 typically involve unorganized local brands lacking proper support systems. Instead of stretching budgets for minimal franchise participation, starting with zero-investment financial product distribution through GroMo enables immediate earnings without capital constraints.

Q: What is the 7 day rule for franchise?

A: The "cooling-off period" concept requires franchisors to provide disclosure documents at least 14 days before signing agreements in regulated markets like the USA. India lacks standardized franchise regulation, so protection varies by agreement. Most Indian franchisors don't offer formal cooling-off periods. Review all contracts with legal counsel before signing, as franchise agreements rarely allow penalty-free exits once executed.

Q: Which franchise in India is most profitable?

A: Profitability depends on location, management, and market timing rather than brand alone. Food franchises like Domino's and Subway show strong performance in high-traffic areas, while education franchises like BYJU'S tuition centers generate steady revenues. However, most profitable franchises require ₹20+ lakh investments and 2-3 year break-even periods. Digital financial product distribution offers faster profitability with zero capital risk and flexible scaling.