IRDAI Exam 2026: How to Pass & Start Earning with Insurance Sales in India

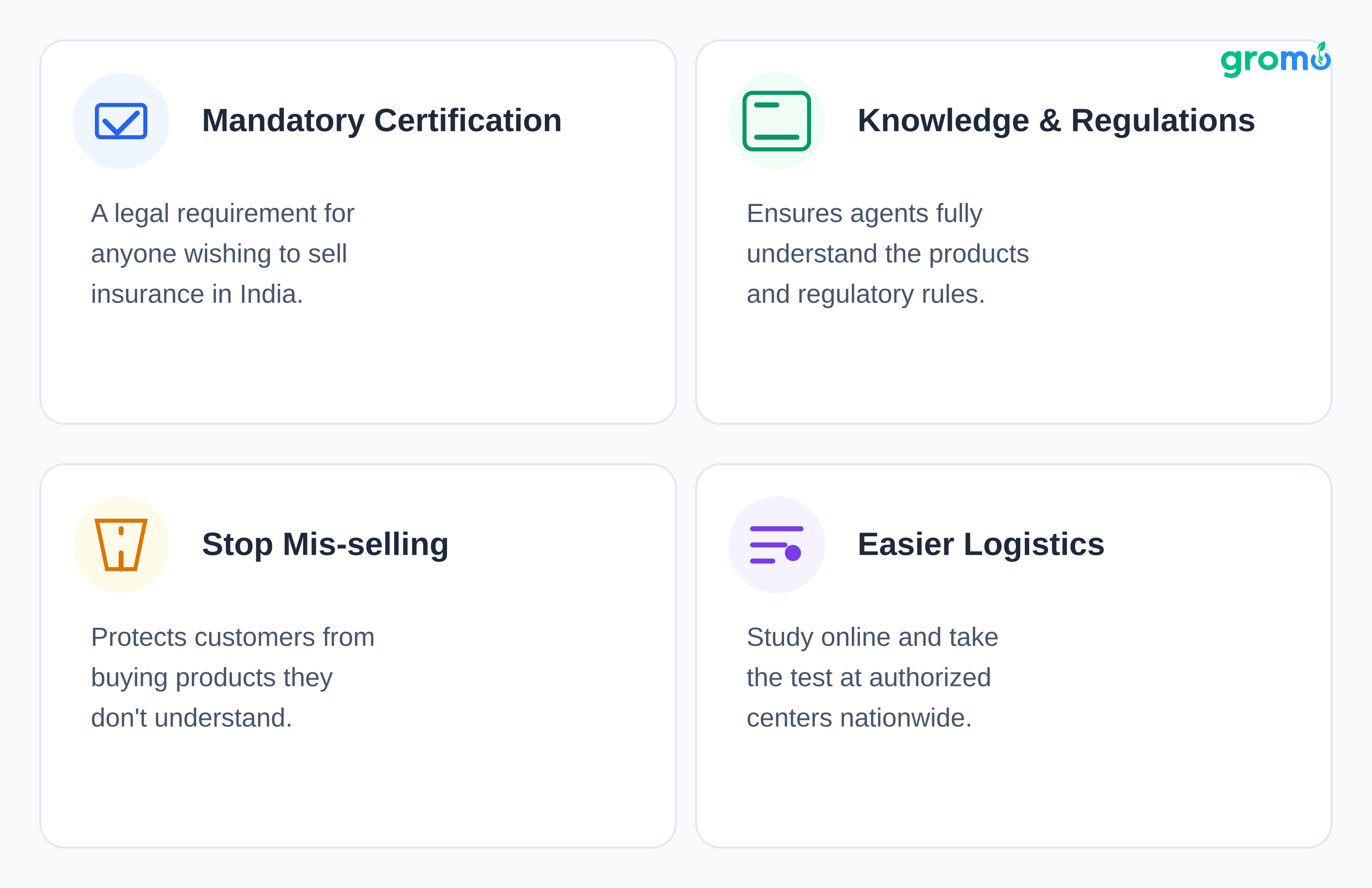

If you want to sell insurance in India, you have to pass the IRDAI exam. No way around it. The Insurance Regulatory and Development Authority of India made this certification mandatory for anyone distributing life, general, or health insurance policies. The rules for 2026 are pretty much the same, but the process is less of a headache now than it used to be.

It doesn't matter if you're a professional looking for side income, a student, or someone exploring financial product distribution as a business. You need this license to operate legally.

What Is the IRDAI Exam?

It's a mandatory certification test. Without it, you can't legally sell insurance in India. The point is to ensure agents understand what they're selling and the regulations around it mostly to stop people from mis-selling products to customers who don't understand them.

The exam substance hasn't changed much, but the logistics are easier. You can prep online and take the test at authorized centers across the country.

Why Certification Matters for Income

India's insurance penetration is low. Recent reports put life insurance at around 4% and general insurance below 1%. That's a big gap. It means there's actual room for agents who can explain these products to people who need them.

Passing the exam gives you a few concrete advantages:

Credibility: Customers trust a license. It shows you've met a basic standard.

Legal standing: Selling without certification invites penalties. The license keeps you compliant.

Access to insurers: Most major insurance companies only work with licensed agents.

Renewal income: This is the real one. Insurance policies pay commissions on renewals. A policy you sell today can generate income for years.

Start Your Financial Products Journey Today

Exam Structure and Content

The exam is 100 multiple-choice questions. You get 60-90 minutes. The passing score ranges from 35-50 marks depending on the category.

There are different exams based on what you want to sell:

Life Insurance (IC-38): Covers term plans, endowment policies, ULIPs, and pension plans.

General Insurance (IC-38): Focuses on motor, property, marine, and liability insurance.

Health Insurance (IC-38): A specialized test for standalone health policies.

Composite License: For agents who want to sell both life and general insurance.

The syllabus covers the basics: insurance principles, product details, IRDAI regulations, the sales process, and ethics. You need to understand how to analyze a customer's needs, fill out proposals, and handle claims. You'll also get tested on anti-money laundering rules and KYC norms.

How to Prepare

Don't overthink this. A 4-6 week timeline is realistic if you study 1-2 hours a day.

Official material: IRDAI provides study materials on its website. Start there.

Online courses: If you need structure, plenty of platforms offer video lectures and mock tests.

Apps: Useful for studying during commutes or breaks.

YouTube: Free content is everywhere.

Focus on understanding concepts. The exam tests practical knowledge, not just memory.

Registration Process

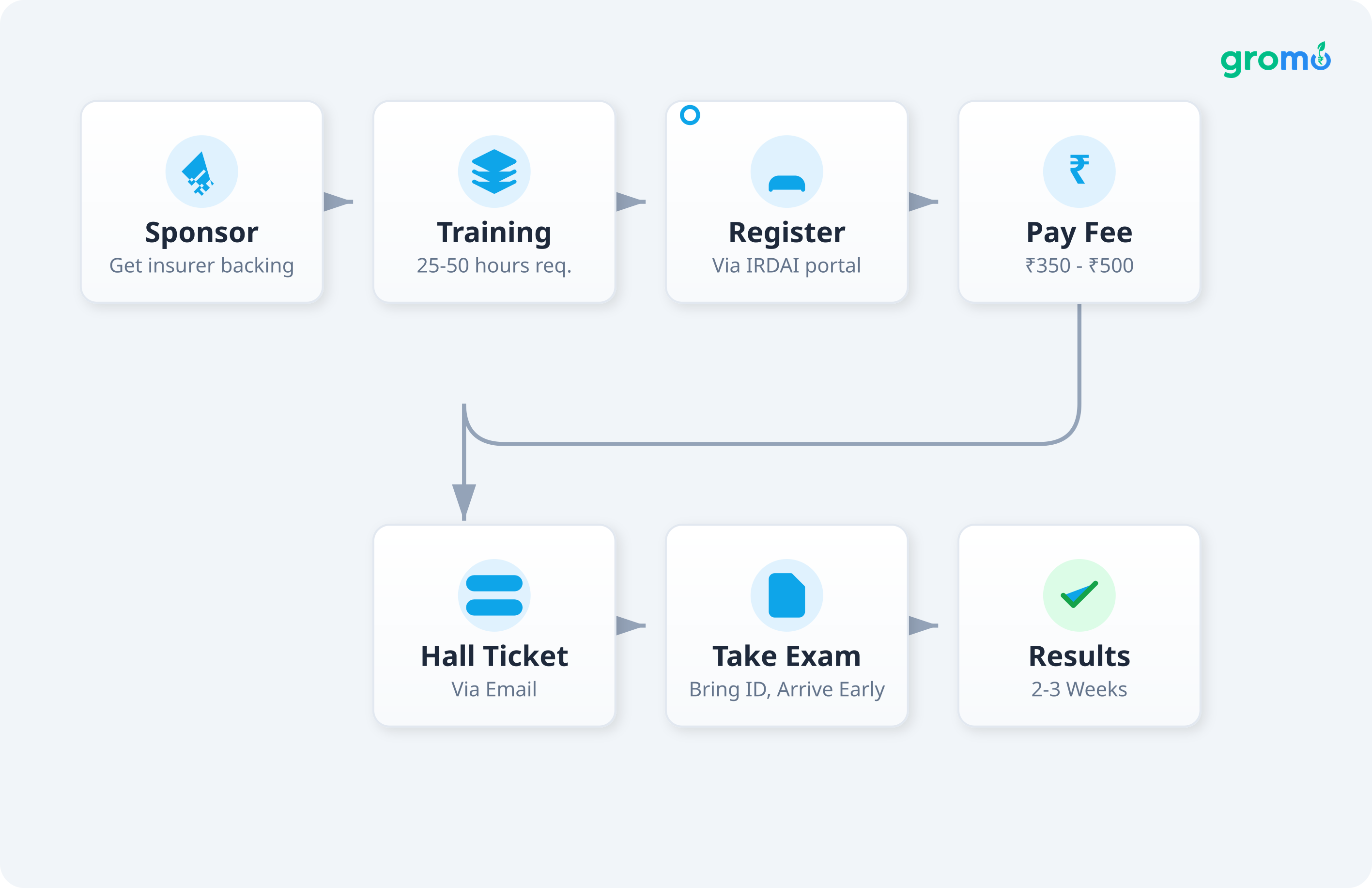

Step 1: Get sponsored. You can't just walk in and take the exam. An insurance company must sponsor you. Contact insurers you want to work with.

Step 2: Training. Sponsors usually require 25-50 hours of training. The company often provides this for free.

Step 3: Registration. Your sponsor registers you through the IRDAI portal.

Step 4: Pay the fee. It costs around ₹350-₹500. Sometimes the sponsor reimburses this.

Step 5: Hall ticket. You'll get it via email a few days before the exam.

Step 6: Take the exam. Bring ID and arrive early.

Step 7: Results. Expect results in 2-3 weeks. If you pass, the certificate is valid for three years.

Expanding Beyond Insurance

The IRDAI certification is just one piece of the puzzle. You can make significantly more money if you sell other financial products too credit cards, loans, savings accounts. That's where platforms like GroMo come in.

If you only sell insurance, you leave money on the table. A customer might need term insurance, but also want a credit card or a demat account. Without access to those products, you lose the commission.

With GroMo, you can sell:

Credit cards (Axis, IDFC, RBL)

Savings accounts (Kotak 811, IndusInd)

Demat accounts (Upstox, Groww)

Loans and mutual funds

You become a one-stop shop. It's better for the customer, and better for your income.

Join 60L+ Partners Earning with GroMo

What You Can Actually Earn

Insurance commissions break down like this:

First year: You earn 15-35% of the annual premium. Sell a policy with a ₹50,000 premium, and you make ₹7,500-₹17,500.

Renewals: You get 5-7.5% for the next 5-10 years. That same policy pays you ₹2,500-₹3,750 annually.

General insurance: Pays 10-20% per policy.

Add other products:

Credit cards: ₹300-₹1,400 per card

Savings accounts: ₹100-₹400

Demat accounts: ₹200-₹500

Personal loans: 1-2% of the loan amount

A part-time agent moving 5-10 policies a month, plus some cards and accounts, can make ₹30,000-₹50,000. Full-time agents with a good client base can clear ₹1 lakh monthly once renewals kick in.

Common Mistakes

Mis-selling: Don't promise returns that aren't guaranteed. It's illegal and ruins your reputation.

Ignoring renewals: New agents chase new sales. The money is in renewals. Stay in touch with clients.

Bad paperwork: Incorrect forms lead to rejections and lost commissions. Learn proper documentation early.

Skipping training: The exam is the minimum. Keep learning.

Putting commission first: If you sell the wrong product for a quick buck, the customer leaves. If you sell the right product, they refer others.

Technology and Training in 2026

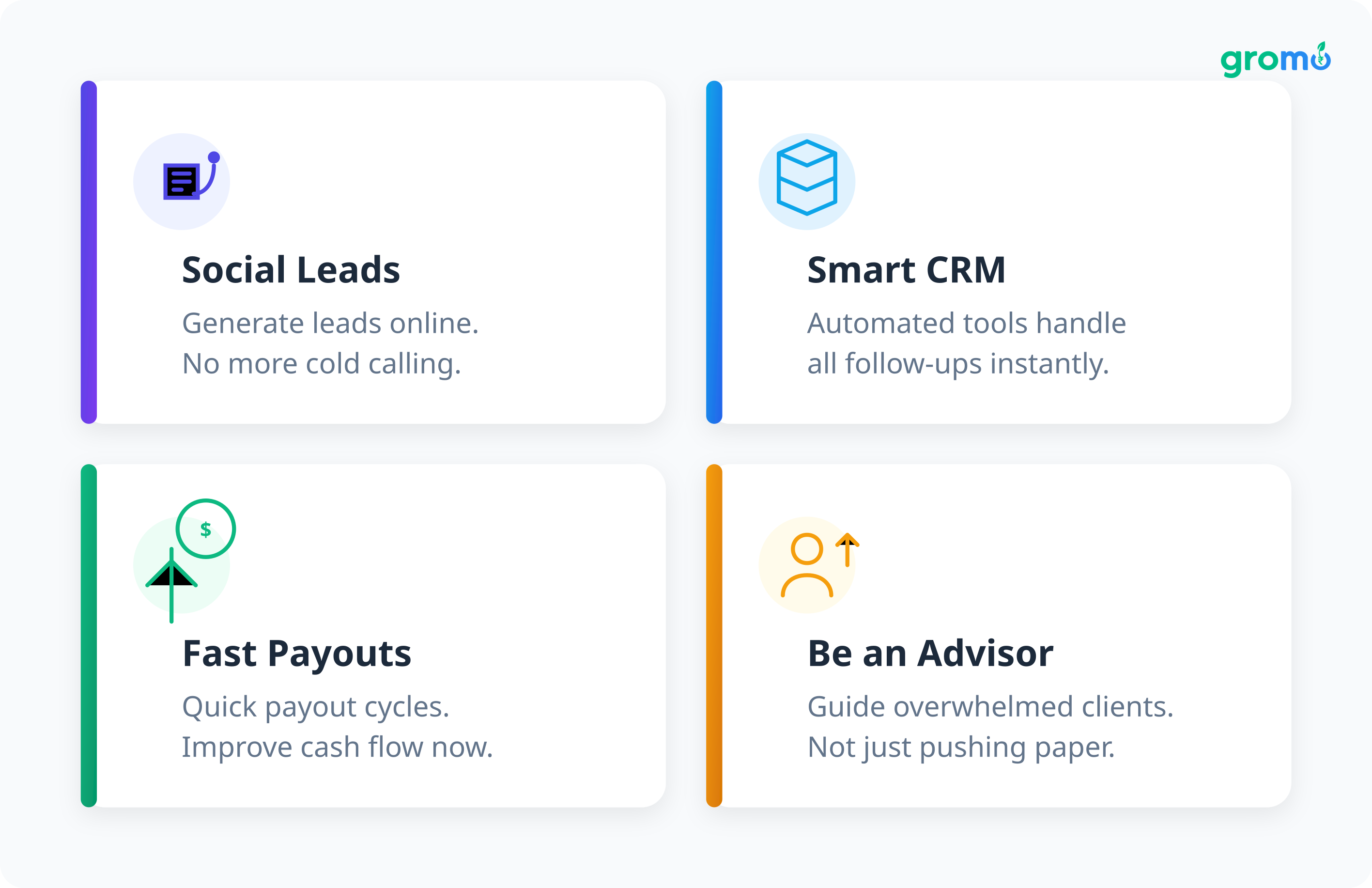

The tools available now make this easier than it was five years ago. You can generate leads on social media instead of cold calling. CRM tools handle follow-ups. Payouts are faster platforms like GroMo offer quick cycles that help your cash flow.

The job has changed. You're not just pushing paper. You're advising people who are overwhelmed by options.

Building a Business

Month 1-3: Pass the exam. Set up a WhatsApp Business account. Join GroMo. Make your first 20 sales.

Month 4-6: Build a routine. Track your conversion rates. Attend advanced webinars.

Month 7-12: Scale up. Use digital marketing. Maybe build a team. Specialize in products that sell best for you.

Year 2+: Live off renewal income. Mentor new agents. Look into additional certifications like NISM for mutual funds.

Is This Right for You?

It makes sense if you want a long-term business, don't mind following up with people, and are okay with delayed income (commissions take time).

It's not for you if you need immediate cash or hate sales.

The Future

The market is growing. Post-pandemic, people understand the need for health and life insurance. Credit cards and loans are reaching smaller cities. If you have the certification and the tools, you're in a good position.

Frequently Asked Questions

Q: How hard is the IRDAI exam?

A: It's moderate. Pass rates are around 60-70%. If you study the official material for a month, you should pass on the first try.

Q: Can I sell financial products without IRDAI?

A: Yes, but only non-insurance products. You can sell credit cards, loans, and accounts through GroMo without it. But you can't sell insurance.

Q: How long is the certification valid?

A: Three years. Renewal is a simpler process usually a shorter exam or training module.

Q: What's the investment?

A: The exam fee is ₹350-₹500. Often sponsors reimburse it. The real investment is time training and prep take about 50-80 hours total.

Q: Can I do this part-time?

A: Yes. Many agents start part-time. You can work evenings and weekends. Digital tools make it possible to handle most things remotely.

Q: What should I sell first?

A: Start with products that have quick approval cycles credit cards, savings accounts. They give you quick wins. Work on insurance in parallel for the long-term renewal income.