Zero-Investment Business in India: Earn ₹50K+ with GroMo

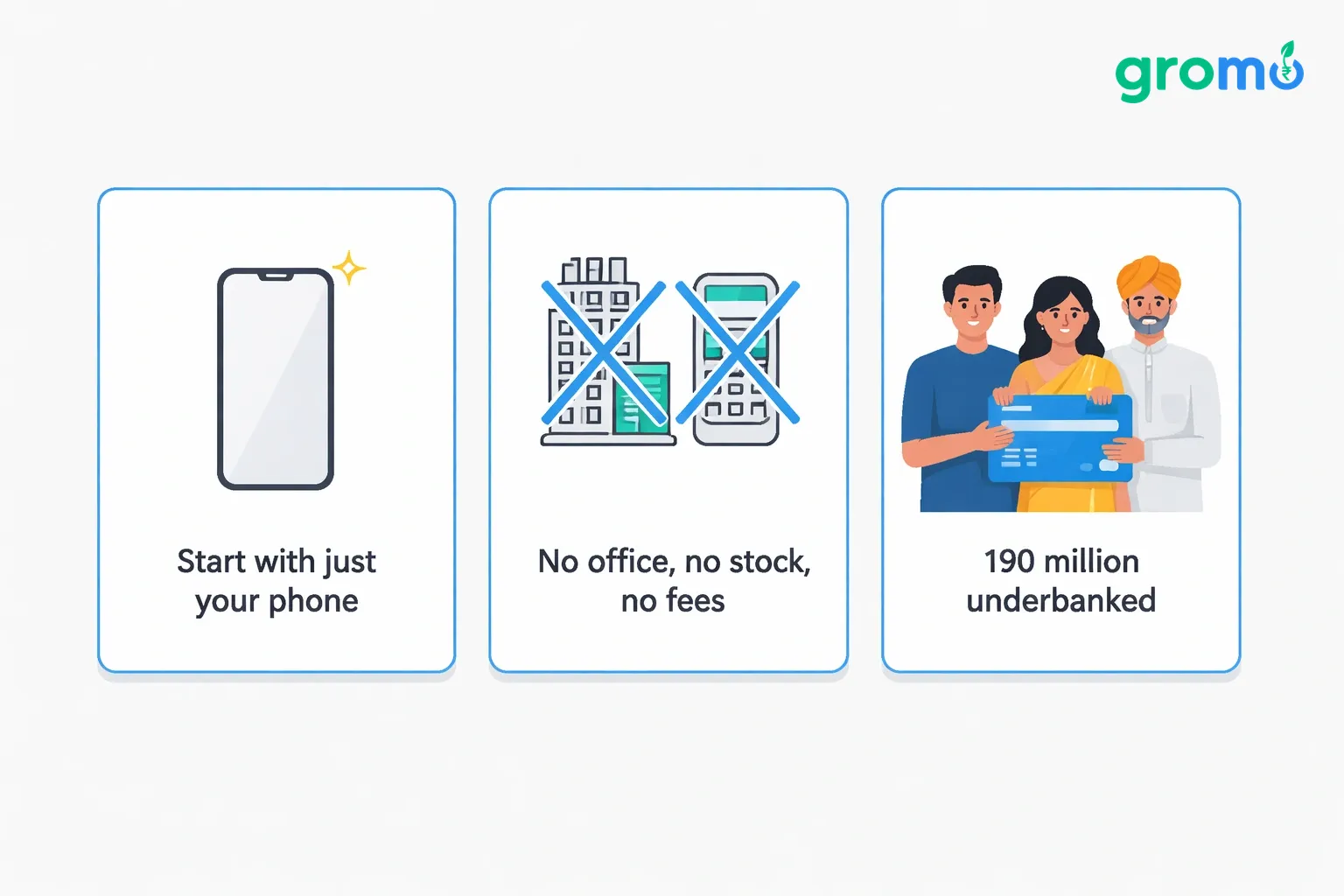

"Make in India" usually summons images of factories and assembly lines. But there's a quieter digital side to it that doesn't get as much press: starting a business with zero capital. Platforms like GroMo let you distribute financial products savings accounts, credit cards, loans from your phone. It fits the self-reliance narrative, sure, but the appeal is more immediate: regular people are earning ₹50K to ₹1 lakh a month without renting an office or buying stock.

The startup wave is real, but the barrier to entry usually involves funding, tech teams, and inventory. Financial product distribution cuts through that. You don't need a warehouse; you need a smartphone. By mid-2026, over 6 million Indians on GroMo had collectively earned ₹100 crores. It’s a staggering number, but it signals a shift in what "starting up" actually looks like for the average person.

Why it costs nothing to start

The Make in India push is about building for Indian markets using Indian platforms. GroMo fits this by building a distribution layer for homegrown financial services.

The biggest difference is infrastructure. Traditional startups bleed money on office space, payment gateways, and legal compliance. GroMo handles all of that. They give you the customer management tools, the payouts, and the marketing content. You just have to find the customers.

There’s also a genuine market need. Roughly 190 million Indians lack bank accounts or credit access. When you help someone open a savings account or secure a digital loan, you’re plugging a hole in the market while earning a commission. It makes the pitch easier when you know you’re solving a problem, not just pushing a product.

The model isn't just a hack. GroMo has Y Combinator backing and appeared on Shark Tank India. That doesn't guarantee you'll get rich, but it proves the model is a recognized business structure, not a side-hustle fad.

The products and the math

GroMo partners can sell six types of financial products from over 30 brands. The money varies depending on what you sell.

Credit cards are the heavy hitters, paying ₹2,000-₹3,000 per approval. If you can sell the Axis Flipkart Credit Card or IDFC FIRST WOW! Credit Card, the returns are solid. You’re looking for middle-class families who want cashback on groceries or UPI transactions.

Savings accounts are a slower burn about ₹250-₹600 per account. Something like the Tide Business India account pays out in stages: when the account opens, when a bill is paid, and when the card is used. These are great for freelancers and small business owners in Tier 2 and Tier 3 cities.

Demat accounts earn ₹250-₹400 per activation. Upstox and Indiabulls require the user to make a trade before you get the full payout. Your audience here is younger, first-time investors.

Personal loans and business loans operate on a percentage model usually 1.5%-3% of the sanctioned amount. If you help a shop owner secure a ClickPe Business Loan, you get a cut of the total. The paperwork is minimal often just PAN, Aadhaar, and bank statements.

Credit lines are more niche. HDFC Smart EMI converts a card limit into a loan. It’s a specific product for existing HDFC cardholders who need cash without maxing out their card.

Stop spamming, start solving

The partners who make real money don't just dump links into WhatsApp groups. They build trust. It sounds soft, but it's the difference between a one-time sale and a steady stream of referrals.

It helps to actually be helpful. If you join local business groups, don't pitch immediately. Answer questions about credit scores or documentation. When you eventually share a link, people listen because you've already provided value.

Keep your contacts organized. Don't pitch a business loan to a college student. Keep lists for salaried professionals, business owners, and students. When Axis launches a new card, you know exactly who to message.

Follow up. A lot of people start an application and get distracted by the video KYC step or a document upload. A message 24 hours later asking if they need help can save the sale.

And ask for referrals. Once a loan clears or an account opens, ask: "If you know anyone else who needs this, send them my way." That’s how you scale without spending on ads.

Our guide on zero-investment business ideas across India explains how to structure outreach effectively.

The training actually matters

GroMo Academy offers free courses, and they aren't just formalities. They teach you to be an advisor, not just a salesperson.

You need to know the products. When a customer asks the difference between a personal loan and a credit line, "I don't know" kills the sale. The courses break down interest rates and eligibility so you can answer confidently.

You need to handle objections. "My credit score is low" doesn't have to end the conversation you can pivot to secured cards. "I don't trust online apps" is a chance to explain RBI regulations.

Compliance is also critical. You learn to spot fake documents and avoid prohibited practices. One mistake here can mean losing your commissions or getting banned entirely.

The monthly webinars are worth attending. They cover new products and trends. Partners who stay updated tend to earn more because they get first dibs on high-commission campaigns.

Top part-time jobs in India compares GroMo’s training support against other platforms.

The network effect

Having 60 lakh partners on the platform creates a strange advantage.

You can steal strategies that work. The partner forums and Telegram groups are full of pitch templates and customer handling tips. You don't have to guess.

You can build a team. GroMo pays you when your recruits make sales. If you bring in 10 people who are actually active, that can add ₹20,000-₹30,000 to your monthly income through overrides.

You get data, not just intuition. The app tells you which products have the highest approval rates in your area. If your city approves 70% more demat accounts than credit cards, you should probably lean into that.

The tech you don't pay for

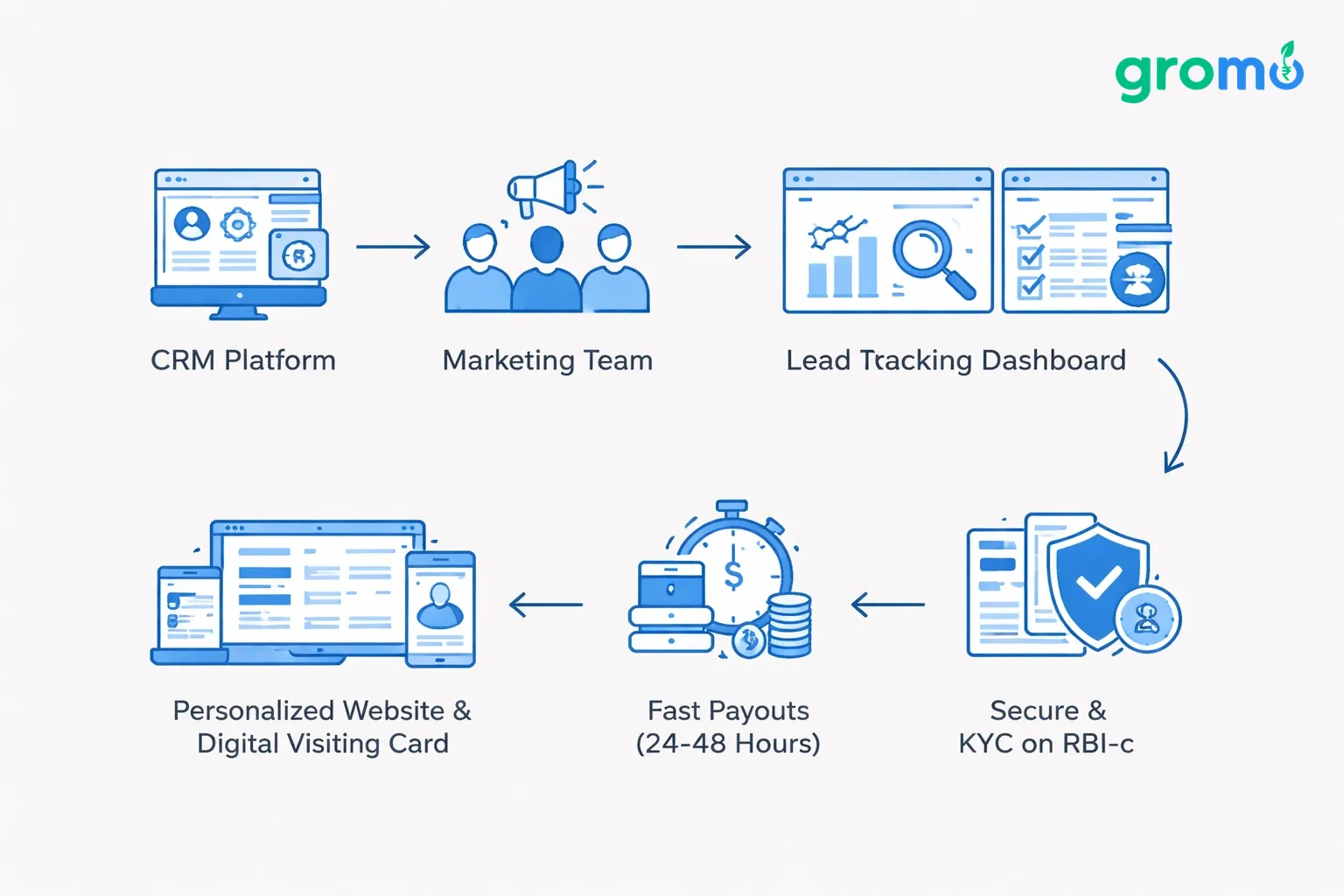

GroMo basically gives you a CRM, a marketing team, and a payment system for free.

The dashboard tracks every lead, pending document, and payout estimate. You don't need a separate subscription for Salesforce or Trello.

It generates marketing content for you. You get a personalized website and digital visiting card with your details. It looks professional without hiring a designer.

Payouts are fast 24 to 48 hours after approval. Traditional finance distribution often makes you wait months. That liquidity matters when you're just starting out.

The security is on them. KYC documents live on RBI-compliant servers. You never touch the sensitive data, which keeps you out of legal trouble.

And it's mobile-first. You can run the whole thing while commuting or on a lunch break.

Start earning ₹50K+ monthly with zero investment details the full stack.

What you can realistically earn

Income scales with effort. There is no magic trick.

Part-time (10 hours/week): Expect ₹15,000-₹30,000 monthly. Focus on one or two products like credit cards. Target your immediate circle. You might close 8-12 applications a month.

Active (25 hours/week): Expect ₹50,000-₹80,000 monthly. You'll expand into business loans and demat accounts. You'll need to be active in community groups. 25-35 applications a month is the benchmark.

Full-time (40+ hours/week): ₹1,00,000-₹2,50,000 monthly. You handle all categories and start building a team. You might even create content like YouTube videos to drive leads.

Team leaders: ₹3,00,000+ monthly. You recruit and train 20-30 partners. Your income is a mix of your sales and their overrides.

Festivals and budget announcements usually spike conversions by 50%. Plan your hustle around those windows.

The comparison with a "real" startup

The risk profile is completely different.

| Dimension | Traditional Startup | GroMo Model |

|---|---|---|

| Initial Capital | ₹5-50 lakhs | ₹0 |

| Time to First Revenue | 6-18 months | 1-7 days |

| Regulatory Burden | High (FSSAI, GST, etc.) | Zero (GroMo handles it) |

| Scalability | Limited by capital/floor space | Unlimited (digital) |

| Risk | Inventory, debt, receivables | Only your time |

| Exit Value | Equity, acquisition | Commission stream |

A traditional startup needs funding rounds and a business plan just to open the doors. You can start selling on GroMo the same day you download the app.

If a traditional business fails, you lose your savings. If GroMo doesn't work out, you're just out the time you spent trying.

The catch is you don't build equity. You build an income stream. If you want to build a company to sell later, do the traditional route. If you want cash flow now, this is the better bet.

Low-cost franchises versus GroMo explores this trade-off in depth.

Why people fail at this

It’s not usually the market that stops people. It’s their own habits.

Spray-and-pray doesn't work. Sending links for 30 products to everyone you know just annoys them. Focus on one product per conversation based on what the person actually needs.

Skipping training causes headaches. If you rush through the Academy, you'll upload the wrong docs or promise things you can't deliver. That leads to clawbacks and bans.

Ghosting leads costs money. Most people who drop off during an application would finish if you just reminded them. If you don't follow up, you're leaving cash on the table.

Relying only on friends limits you. Your warm network dries up fast. You have to find strangers through content, community groups, or partnerships.

Where you are changes what you sell

Demand isn't uniform across the country.

Maharashtra and Karnataka are credit card territory. Urban professionals in Mumbai and Bangalore have the credit scores for premium cards. Our Mumbai zero-investment business guide has specifics.

Punjab and Haryana are business loan markets. Traders and small manufacturers need working capital. See Punjab-specific earning strategies for the paperwork details.

Tamil Nadu and West Bengal prefer savings accounts. The culture is more conservative with money. Tamil Nadu earning ideas cover this well.

Gujarat is big on demat accounts. People there tend to invest surplus cash in equities. Check the Gujarat zero-investment businesses page.

Delhi NCR is a mix. You can sell credit cards in Gurgaon corporate parks and business loans in Lajpat Nagar markets.

Hyderabad financial distribution opportunities and Pune selling strategies are also worth a read if you're in those cities.

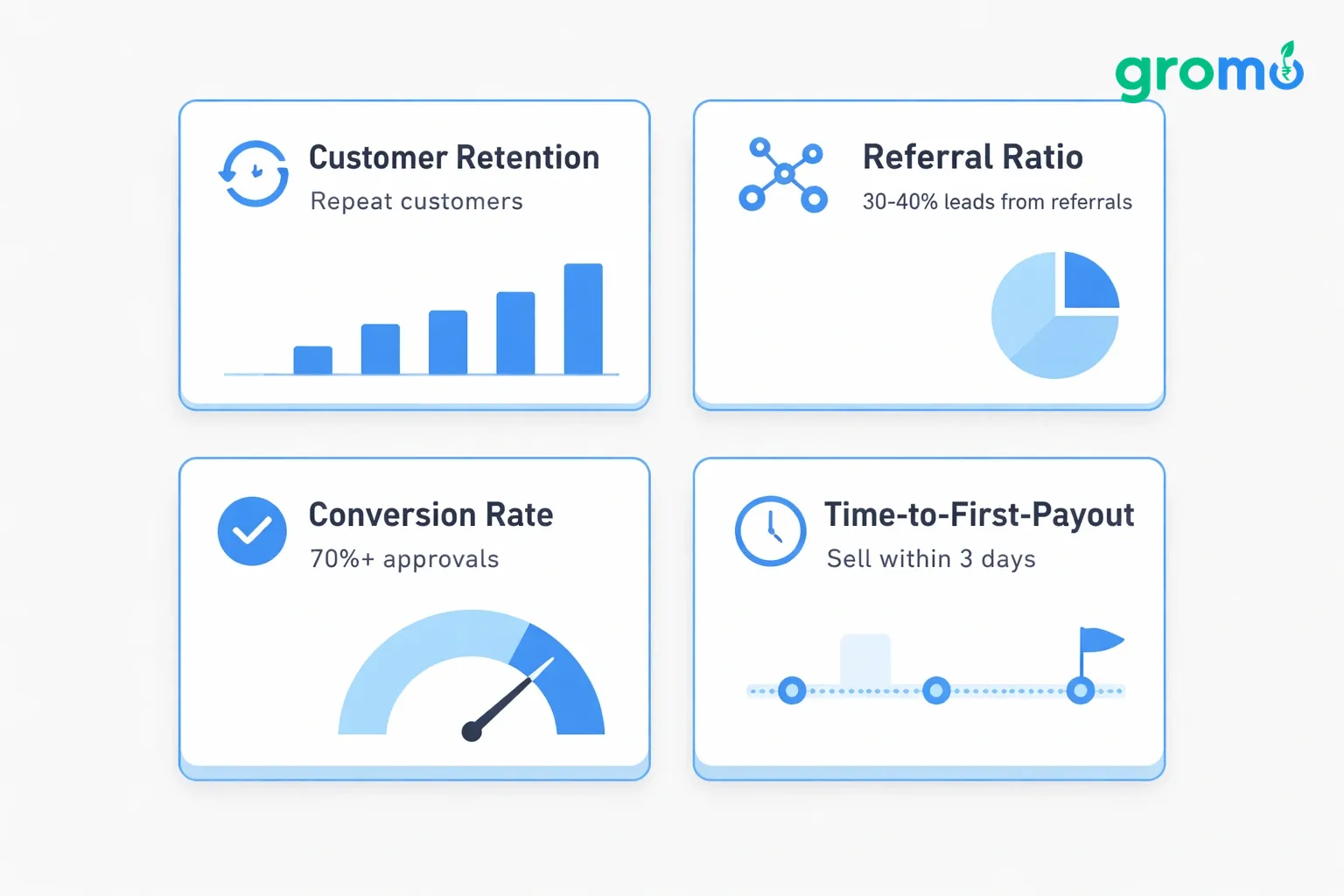

Metrics that actually tell you something

Don't just stare at the bank balance. Look at the underlying numbers.

Customer retention: Do people come back? If someone opens a savings account and returns six months later for a loan, you're doing it right.

Referral ratio: If 30-40% of your leads come from other customers, your reputation is working for you.

Conversion rate: If you're getting 70%+ approvals, you're qualifying people correctly. If not, you're wasting time on bad leads.

Time-to-first-payout: The best partners usually sell something in the first 3 days. If it takes you two weeks, go back to the training modules.

Mixing it with other work

You don't have to put all your eggs in this basket.

If you make content, embed GroMo links in your personal finance videos. It’s passive income.

If you freelance, mention it to clients. A web developer working with small businesses can casually bring up business loans.

If you're in real estate, you already know people buying homes who need credit cards for furnishings.

Making money online in India lists other streams that fit well with this.

The long game

This can be a career path if you treat it like one.

Phase 1 (Months 1-6): Learn to sell. Hit ₹30,000-₹50,000 monthly.

Phase 2 (Months 7-12): Start recruiting. Overrides will bump your income.

Phase 3 (Years 2-3): Specialize. Become the expert in two or three products. Make content.

Phase 4 (Year 3+): Go pro. Register a company. Hire an assistant to handle the admin. Maybe diversify into insurance or tax filing.

Financial product distribution careers in India maps out the progression.

The government wind at your back

Policy changes are making this easier.

Jan Dhan accounts brought 460 million people into the banking system. They are now looking for credit and investment options.

UPI made digital payments normal. People who pay via UPI are comfortable applying for financial products online.

GeM vendors need working capital. You can target government suppliers with business loans.

Startup India registration gives you credibility and tax perks.

ONDC expansion is creating more small merchants who need financial tools.

India's fintech revolution trends explains the landscape.

The risks are real

Zero capital risk doesn't mean zero risk.

Clawbacks happen. If a customer defaults on their first three EMIs, you lose your commission. You have to vet people, not just sign them up.

Regulations change. The RBI shifts rules occasionally. If you only sell one type of product, a rule change can hurt you. Diversify.

You are dependent on the platform. If GroMo changes its payout structure, you have to adapt. Keep your own email lists and customer relationships so you own the asset, not just the access.

Network exhaustion is real. Your friends list isn't infinite. You have to constantly find new ponds to fish in.

Zero-investment business models and their risks goes deeper into this.

FAQ

Q: Can I do this with a full-time job? A: Yes. Most partners do. You work on your own schedule commutes, evenings, lunch breaks. There are no shifts.

Q: Do I need a finance background? A: No. The training fills the gap. You just need to actually do the modules.

Q: When do I get paid? A: 24-48 hours after approval. For simple products like savings accounts, you could theoretically earn within two days of joining.

Q: What if a sale falls through? A: You don't get paid. The dashboard shows why, so you can learn from it.

Q: Any hidden fees? A: No. It's free to join. GroMo gets paid by the banks, not by you.

Q: Can I build a team? A: Yes. You earn a cut of your recruits' sales. It's how the top earners scale past ₹2-3 lakhs a month.