Zero Investment Business Ideas in Punjab 2026 | Earn ₹50K Monthly

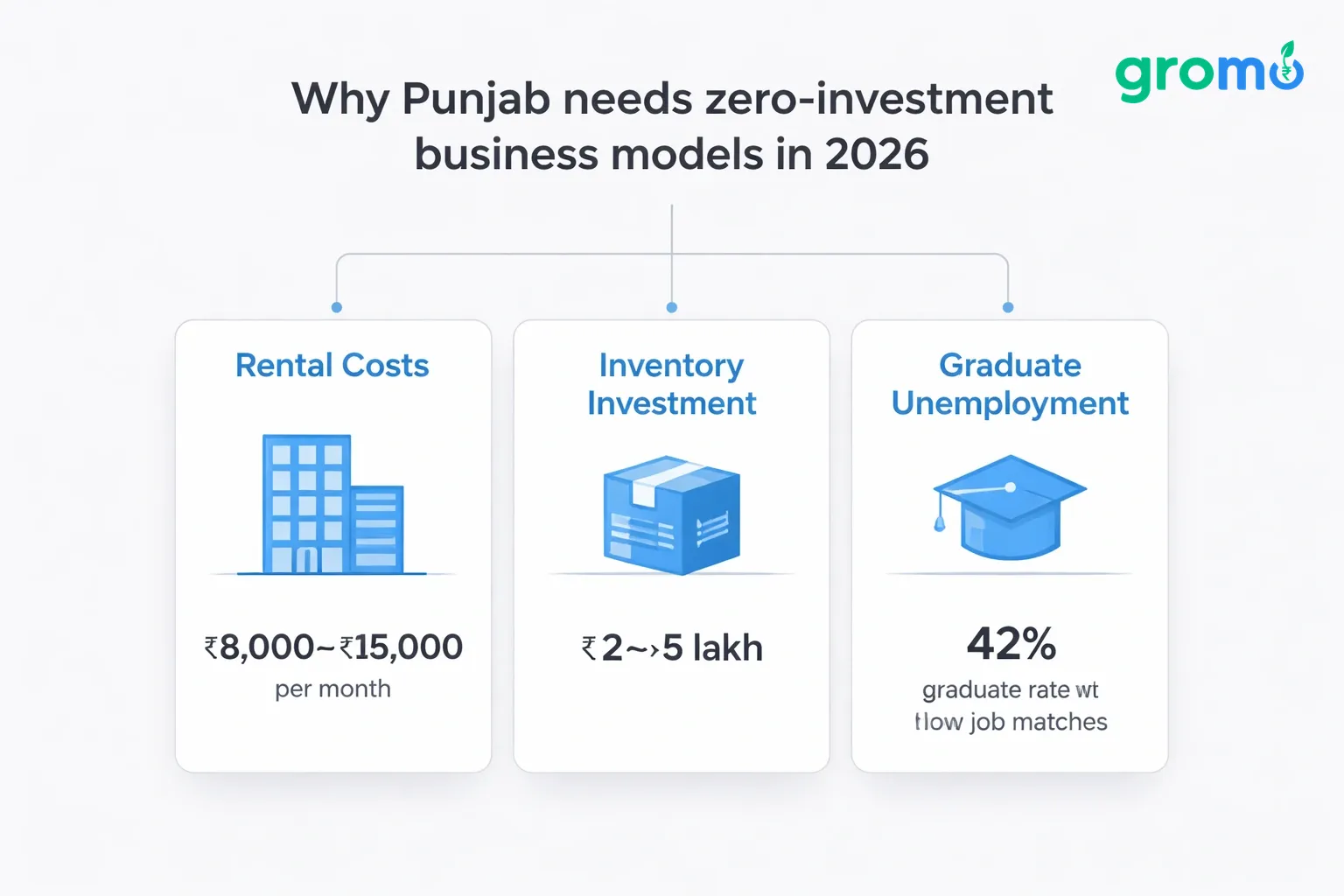

Getting a business off the ground in Punjab usually costs money most people don't have. Shop rent in Ludhiana or Amritsar runs ₹8,000-₹15,000 a month for a decent spot. Inventory for a textile or electronics shop? That’s ₹2-5 lakh gone before you make your first sale.

But in 2026, you don't need a shop or stock to make ₹50,000 a month. Selling financial products credit cards, loans, savings accounts through apps like GroMo has become a real alternative for people who want income without upfront capital.

It works here because Punjab has high smartphone usage and a culture where business runs on relationships. You don't need land or a storefront. You can run this from a chai shop, a college campus, or your bedroom. Payouts hit your bank account within 48 hours.

Why Punjab needs zero-investment business models in 2026

The math for traditional business just doesn't add up for most families.

Commercial real estate in cities like Ludhiana, Amritsar, and Jalandhar has detached from local earning power. A standard retail space costs ₹8,000-₹15,000 monthly. Inventory-based businesses textiles, electronics, grocery demand ₹2-5 lakh for initial stock alone.

It creates a squeeze. Punjab has a high graduation rate (around 42%), but educated youth often can't find jobs that match their skills, and their families lack the surplus cash to fund a startup. Agricultural income doesn't provide the safety net it once did. Factory workers in Mohali and Patiala take home ₹15,000-₹25,000 a month, leaving almost nothing to save for a business venture.

Zero-investment models bypass this. You monetize your network and your ability to explain things. You connect people to financial products they need credit cards, loans, savings accounts. The bank handles the infrastructure, compliance, and delivery. You get paid for the introduction.

Digital adoption drives this. Punjab's 4G coverage (around 91% as of March 2026) and familiarity with UPI mean customers complete applications on their phones. No office visits. No handling physical paperwork. Just conversation and a link.

Top zero-investment business ideas for Punjab residents

Financial product distribution offers the highest return for the time invested. Platforms like GroMo let you sell credit cards (₹600-₹2,400 per approval), personal loans (1.5%-5.5% of the loan amount), business loans (1.75%-3%), demat accounts (₹250-₹400), and savings accounts (₹100-₹550). A single credit card approval can pay more than a week's wages at a factory.

Credit card referrals work well because Punjab has a consumption-driven middle class. Families in Chandigarh, Mohali, and Patiala want cashback cards for fuel, groceries, and online shopping. Partner banks like Axis, HDFC, and ICICI offer cards with instant digital approval. Your commission arrives 7-30 days after the customer activates the card. It’s a model that has worked for people in Mumbai's zero-investment sector, too.

Loan facilitation taps into the state's MSME base. Small manufacturers in Ludhiana need working capital. Kirana stores need inventory finance. Transport operators need vehicle loans. Products like ClickPe Business Loans (up to ₹3 lakh, 1.5%-2.5% payout) or Poonawalla Fincorp (up to ₹50 lakh, 1.75%-3% payout) solve real problems. A ₹10 lakh business loan at 2.5% commission earns you ₹25,000.

Investment account opening serves a growing audience. NRIs sending money home, salaried professionals building portfolios, and agricultural families diversifying from land all need demat accounts. Upstox and Aditya Birla Money pay ₹250-₹400 per account. Once you know the KYC process, you can open 3-5 accounts a day just by talking to people.

Digital savings account distribution targets the unbanked or underbanked. Tide Business India accounts or IDFC FIRST Bank offerings with zero balance requirements appeal to small business owners and freelancers. The payouts stack up: you earn for the account opening, bill payments, and card usage, totaling ₹500-₹800 per customer.

Building a referral network extends your reach. Once you know the ropes, the GroMo referral program pays you ₹1,100 for every qualified distributor you recruit. If you have 10 team members each closing 5 deals a month at ₹1,000 average commission, you earn ₹50,000 in override income alone.

How Punjab's culture accelerates zero-investment success

Business in Punjab runs on vishwas (trust) and rishte (relationships). This fits financial distribution perfectly. When you recommend a credit card, you aren't cold-calling. You are using the social capital you already built.

Family structures provide a built-in network. The average Punjabi has 15-30 immediate family members across three generations, plus connections back in the pind (village). A family wedding involves 200-500 guests. Every one of them is a potential lead. Your cousin's factory, your uncle's transport business, your sister's boutique they all need loans or cards.

NRI connections are a major asset. Punjab sends more migrants abroad than any other state. These NRIs maintain strong ties. They need Indian bank accounts for property, demat accounts for stocks, and loans for family businesses. If you position yourself as their India-based financial coordinator, you access a segment with higher ticket sizes.

Community spaces concentrate your audience. Gurudwaras, wedding halls, sports clubs, and akhadas bring people together physically. Unlike Bangalore's dispersed tech workforce, Punjabis gather in person regularly. A conversation after langar or during a kabaddi match can yield leads. Word travels fast.

Language matters, too. Financial products intimidate people who don't speak English. Terms like "credit score," "EMI," and "KYC" confuse rural and semi-urban customers. When you explain in Punjabi "ek lakh da loan, sirf do hazaar mahina EMI" they get it. You aren't selling; you are translating.

Step-by-step: Launching your Punjab zero-investment business

Register on GroMo. It takes 10 minutes. Download the app, enter your mobile number, verify with OTP, provide PAN and Aadhaar. No fees, no deposits. You get immediate access to 15+ products. Like full-time employees earning extra income elsewhere, you can start on evenings or weekends.

Do the product training. GroMo Academy offers free courses. Spend 2-3 hours learning eligibility criteria and documentation. This separates you from people who just spam links.

Identify your first 10 customers from your network. Don't start with strangers. Look for friends who need a credit score boost, family members seeking investment accounts, or business owners needing working capital. These warm leads convert at 40%-60%. Cold outreach converts at 5%-10%.

Start conversations about problems, not products. Don't ask "Kya tumhe credit card chahiye?" Ask "Fuel expenses kitne aate hain monthly?" or "Business ke liye urgent cash need hai kya?" Find the need first. Share your GroMo link and promise to guide them.

Track applications on the dashboard. The platform shows real-time status for every customer. Follow up on incomplete applications. Upload missing documents. This active help distinguishes you from people who send a link and disappear.

Get paid. Commissions land in your bank account within 7-45 days depending on the product. Credit cards pay within 30 days of the first transaction. Loans pay 7-15 days after disbursal. GroMo shows exactly when to expect payment.

Punjab-specific strategies for maximum earnings

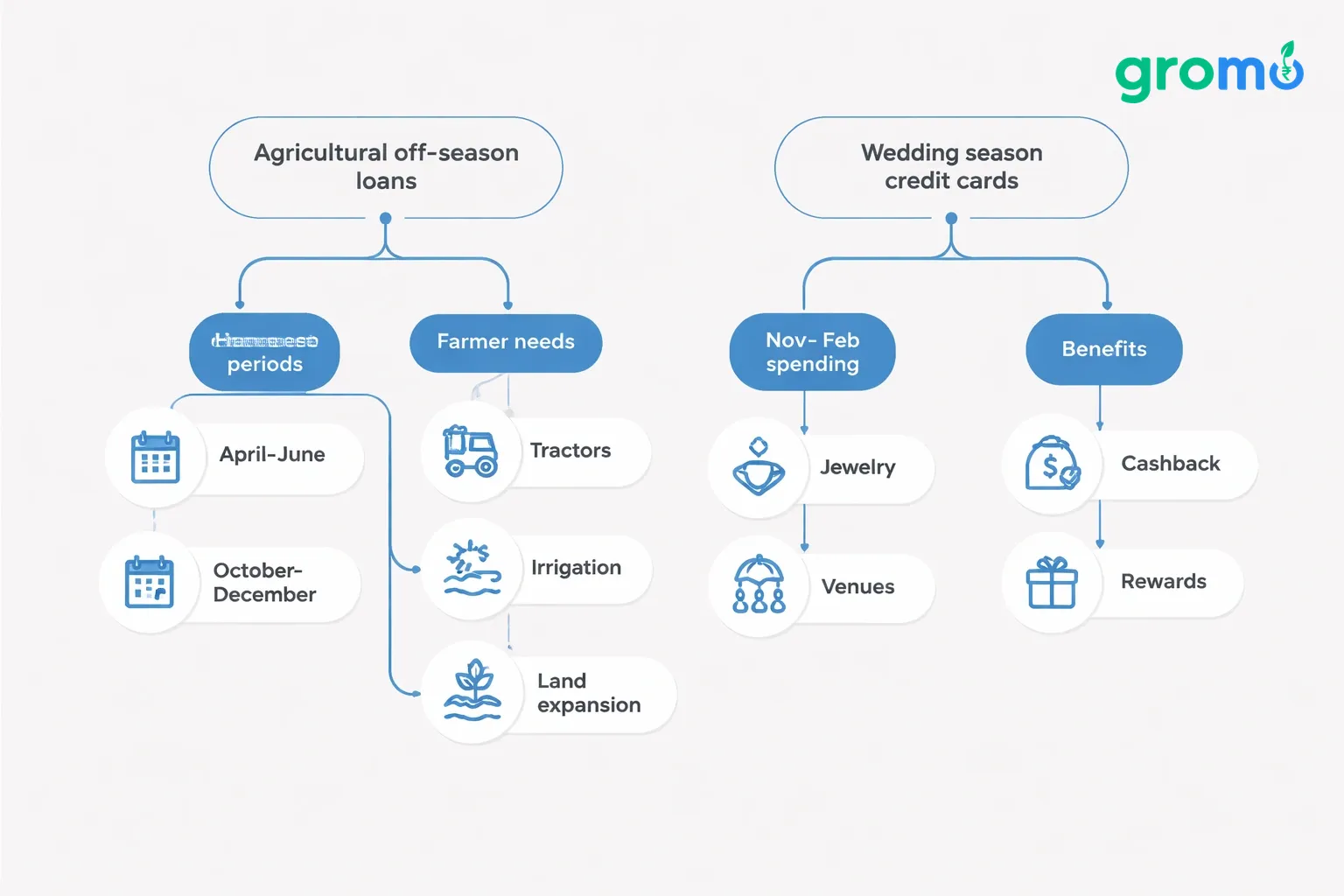

Target the agricultural off-season for loans. After harvest (April-June, October-December), farmers have cash and expansion plans. They buy tractors, upgrade irrigation, or expand land. If you understand khet-khaane (farming operations), you can help them secure loans against expected crop income rather than salary slips.

Leverage wedding season for credit cards. November through February sees massive household spending. Families drop lakhs on jewelry, venues, and catering. They need cashback and rewards cards to manage that spend. Show them a comparison: "If you spend ₹5 lakh on wedding expenses, this card saves you ₹15,000-₹25,000."

Partner with local trade groups. Ludhiana's textile merchants, Jalandhar's sports goods manufacturers, Amritsar's handicraft exporters these groups hold monthly meetings. Offer to run a free workshop on "Working Capital Management" or "How to Maximize Loan Eligibility." Position yourself as an expert, not a salesperson.

Create Punjabi-language content. Short videos on "Credit Score Kaise Badhaye" or "Business Loan Documents Checklist" get shared heavily on WhatsApp locally. Use local landmarks and accents. This builds authority and brings inquiries to you, similar to strategies in India's broader zero-investment business ecosystem.

Move to high-ticket products later. Start with credit cards and small loans to learn the ropes. Once you have 15-20 transactions under your belt, shift focus to business loans (₹10,000-₹25,000 commissions) and premium accounts.

Common mistakes Punjab distributors must avoid

Over-promising approval. Banks make the final call based on algorithms and credit scores. Never guarantee "pakka approval milega." A rejection hurts your reputation. Instead, say "hum eligibility check karke best option suggest karenge bank ka final decision hoga." Honesty builds trust.

Ignoring compliance. Uploading fake salary slips or inflated bank statements triggers fraud alerts. It gets you banned. Verify that customer documents are authentic. Your reputation depends on clean submissions.

Disappearing after the sale. If a customer's card gets declined or they can't access their demat account, help them. Responsive support turns a one-time customer into a source of referrals. Spend 30 minutes a day on follow-up calls.

Competing on kickbacks. Some distributors offer customers ₹500 cashback from their own commission to close a deal. This attracts price-sensitive customers who won't stick around. Compete on service and speed instead.

Selling only one product. Credit cards alone won't get you to ₹50,000 monthly unless you close 20-25 a month. Mix high-frequency, low-value products (cards, savings accounts) with low-frequency, high-value ones (business loans).

Scaling to ₹1 Lakh+ monthly in Punjab

Build a team. Recruit 10-15 people college students, housewives, unemployed youth from your network. Train them on 2-3 products each. You earn ₹1,100 per qualified recruit via the GroMo referral program, plus a percentage of their transaction volume. A 15-person team averaging ₹20,000 monthly each generates ₹3 lakh in volume. Your 10%-15% override yields ₹30,000-₹45,000.

Assign territories. Give team members specific areas one person covers Ludhiana Model Town, another Jalandhar Cantt. This increases accountability. They become the go-to financial advisor for their zone.

Offer value-added services. Don't just send links. Offer "Credit Score Improvement Consultation" or "Business Loan Readiness Audit." This positions you as a consultant, justifying higher margins and multiple sales per customer.

Tap NRI networks. If you have family in the UK, Canada, or the US, position yourself as their India-side financial coordinator. NRIs transact in higher amounts (₹10-50 lakh loans are common) and value reliability over small commission savings. One NRI client can generate ₹25,000-₹1,00,000 across multiple products.

Shift from doer to owner. After 3-6 months, reinvest earnings into team building and basic marketing. Delegate execution to the team. Focus on relationships and strategy. This creates income that doesn't depend on your personal hours a key trait of true business ownership.

Technology tools to boost Punjab distribution efficiency

Use GroMo's in-app CRM. It tracks every link shared and application status. Set reminders for follow-ups. Tag customers by potential ticket size. This organization prevents leads from slipping away.

WhatsApp Business API helps manage volume. Create broadcast lists for different customer types business owners, salaried pros, students. Send targeted offers: business loans at quarter-end, credit cards during festivals. Use labels to track conversation stages.

Screen recording apps are useful. Record yourself completing a sample application. Add Punjabi voiceover. Share the video with customers before they start. It reduces confusion and incomplete submissions.

UPI expense tracking keeps you honest. Tag every commission payout by product type in apps like Walnut. After 3 months, you'll see which products pay the best for your time and which customer segments convert highest.

Regional keyword research helps you get found. Use Google Trends to see what locals search for: "Ludhiana mein business loan kaise milta hai" or "demat account kaise khole." Create content addressing these exact queries with your referral links. This legitimate online earning strategy brings leads to you.

Real Punjab success story: Gurpreet's journey

Gurpreet Singh from Patiala started on GroMo in August 2025 while working at a textile showroom for ₹18,000 a month. He spent evenings helping friends understand financial products. His first month: 3 credit card approvals (₹3,600) and 1 personal loan (₹2,200) ₹5,800 total for about 12 hours of work.

By November, he had a system. He identified 50 textile traders in his network who needed working capital. He made a simple Punjabi presentation on loan eligibility. He ran four Saturday workshops at different mandis. He generated 22 applications. Fourteen got approved. At an average 2.2% commission on ₹8 lakh loans, he earned ₹2,46,400 in November alone.

He quit the showroom job in January 2026. He recruited 8 team members former colleagues and friends. His personal sales dropped to ₹30,000-₹40,000 monthly, but team overrides added ₹45,000-₹65,000. By May 2026, his income averaged ₹95,000-₹1,35,000 monthly. Total investment: ₹0. Total earnings: nearly ₹7 lakh.

Gurpreet’s edge: he focused on B2B (business loans) first, specialized in the textile trader segment he knew well, followed up on every application, and reinvested his time into building a team. His path mirrors others in Punjab's financial distribution economy.

Legal and compliance considerations for Punjab

You are a lead generator, not a licensed advisor. Don't claim to be a bank employee or certified financial planner unless you have the papers. You facilitate introductions. The bank decides.

Protect customer data. Never screenshot Aadhaar, PAN, or bank statements onto your personal phone. Use GroMo's secure upload. Sharing data with third parties can get you banned and fined under the Digital Personal Data Protection Act 2023.

Watch for clawbacks. If a customer defaults on the first 3 EMIs, the bank might reverse your commission. Don't push products on people who can't repay. Keep a 90-day emergency fund to handle potential clawbacks.

GST registration. If annual commissions cross ₹20 lakh, you need a GST number. It’s a sign you’ve scaled. A local CA in Ludhiana or Jalandhar can handle the filings for a few thousand rupees a year.

Be honest with recruits. Don't promise "guaranteed income" when building a team. Commission work has ups and downs. Be clear about the effort required.

Why this works better than traditional Punjab businesses

No real estate costs. A shop in a decent Punjab city location requires a security deposit and renovation often ₹3-8 lakh upfront. Zero-investment models need a smartphone and internet.

No inventory risk. Ludhiana textile traders have ₹5-10 lakh tied up in stock. Grocery stores have receivables. Financial distribution has zero inventory. You sell a service, not a product you have to store.

Scalability. A shop serves a 3-5 km radius. You can serve anyone in India with a phone. A client in Bathinda or Amritsar is as easy to serve as one next door.

Faster profit. A traditional retail business takes 18-36 months to break even. Financial distribution costs nothing to start. Your first sale is pure profit.

Transferable skills. Learning to sell financial products teaches you about credit, sales, and digital marketing. These skills have value even if the specific platforms change.

Next steps for Punjab residents ready to start

Download GroMo and register. It takes 10 minutes. You don't need an interview or a fee. Your location is an asset you have the network, the trust culture, and a market that traditional banks haven't fully saturated.

Do the training before you talk to anyone. GroMo Academy takes 3-4 hours. It explains credit scores, eligibility calculators, and product differences. This knowledge increases your conversion rate.

Find your first 5 customers today. Don't wait for a pitch. Text the friend who mentioned a credit card, the cousin asking about a loan, the neighbor interested in stocks. Share the link with a note: "Yeh product tere kaam ka lag raha hai main guide kar sakta hoon application mein."

Set milestones. Aim for ₹5,000-₹10,000 in Month 1. ₹15,000-₹25,000 in Month 2. Treat it like a business, not a hobby. Put in 2 hours daily.

Connect with other Punjab partners on the app. Learn how they handle objections. 60 lakh partners nationally use this model. Your job is execution.

Frequently asked questions

Q: Can I really earn ₹50,000+ monthly in Punjab without any investment?

A: Yes. It is commission-based. Two to three business loans a month plus 15-20 credit cards can generate ₹50,000-₹80,000. Punjab’s relationship culture actually helps compared to metros.

Q: How long before I receive my first payout?

A: Depends on the product. Credit cards pay 7-30 days after the first transaction. Loans pay 7-15 days after disbursal. GroMo shows the payout date for each transaction.

Q: Do I need to know English?

A: No. Conversational Punjabi and smartphone skills are enough. Your job is matching the customer to the product. The bank handles the backend analysis.

Q: What if the application is rejected?

A: You earn nothing on rejections. Pre-qualify your customers. Use GroMo's eligibility checkers. Properly qualified applications convert at 50%-70%. Rejections don't penalize you beyond lost time.

Q: Can I do this while working full-time?

A: Most people start part-time. 2 hours in the evening plus weekends is enough. Punjab’s social culture means you can talk business at social events. Many people keep their jobs and just enjoy the extra income.

Q: Is this sustainable?

A: India's credit penetration is growing. Banks are shifting to digital distribution. As a local advisor, you become more valuable over time, not less. Build the relationships now to capture that growth.