Zero Investment Business in Delhi: Earn ₹50K-Month with GroMo

You don't need capital to start a business in Delhi. You just need to know where the money is flowing.

Right now, people are earning ₹50,000 to ₹1.5 lakh a month selling credit cards, loans, and demat accounts through GroMo. It's not magic. It's commission work. You have a smartphone, you find the customer, the bank pays you.

Delhi is arguably the best place in India for this. The city is dense with government employees, corporate transplants, and small business owners people who actually need credit. And thanks to the Metro, you can cover Noida, Gurgaon, and Central Delhi in a single afternoon without spending a fortune on fuel.

Here is how the math actually works on the ground.

Why Delhi works

Delhi has density. 32 million people. A huge chunk are salaried government staff in RK Puram, tech workers in Gurgaon, traders in Chandni Chowk.

The Metro is your office. You can live in Dwarka and meet a client in Noida in under 90 minutes. That mobility matters. You don't need to rent a space; you just need to show up where the customers are.

The financial plumbing works better here. People have PAN cards. They have Aadhaar linked. They have credit scores. In tier-2 cities, you often spend weeks just sorting out paperwork. In Delhi, if the person is eligible, the application moves fast.

The products that actually pay

Credit Cards Target the government colonies. RK Puram, Vasant Kunj, Chanakyapuri. These are central government employees earning ₹40,000+. They have steady paychecks and clean credit. GroMo's IDFC FIRST WOW Credit Card pays ₹2,400 per approval. If you close five of those a month, that's your rent sorted.

Business Loans Chandni Chowk, Karol Bagh, Sadar Bazaar. Over 90,000 traders operate there. They need working capital before Diwali and Eid. ClickPe Business Loans just require PAN, Aadhaar, and bank statements no CA-certified balance sheets. The commission is 1.5% to 2.5% of the loan amount. A ₹10 lakh loan puts ₹15,000-₹25,000 in your pocket.

Demat Accounts Young professionals along the Gurgaon-Delhi corridor are opening investment accounts at a crazy rate. Upstox and Aditya Birla Money pay ₹250-₹400 per account. Run a workshop in a Lajpat Nagar café on a Saturday, get 10 signups, walk away with ₹3,000.

Personal Loans People in Delhi switch jobs every 3.2 years on average more frequently than the rest of India. Relocation costs money. New furniture, rental deposits. Poonawalla Fincorp and Prefr offer 2.1% to 3.5% commission on personal loans up to ₹5 lakh.

Finding customers without spending on ads

RWA Meetings Delhi runs on Resident Welfare Associations. There are 2,400+ of them. They meet monthly. Go there. Offer a 15-minute talk on credit scores. Don't sell. Just teach. Hand out your GroMo link to the 5 people who come up to you afterward.

Coworking Spaces Connaught Place, Aerocity, Nehru Place. These places are packed with freelancers and startup employees. Join their Friday networking drinks. The 25-year-old developer you chat with needs a credit card and a demat account.

Alumni Groups DU, JNU, NSUT. Jump into the WhatsApp groups. Post a "Financial Product Alert" once a month. Keep it practical: "This savings account gives you a ₹500 bonus." Don't post theory.

Trade Associations Sadar Bazaar traders have a federation. They meet weekly. March and September are inventory stocking months. That's when they need loans. Show up in August.

Neighborhood specific advice

South Delhi (GK, Defence Colony) Sell lifestyle. Premium cards with lounge access. These people don't care about ₹500 cashback. They care about status. Loan ticket sizes here are high ₹8 lakh average.

West Delhi (Janakpuri, Rajouri) Sell savings. Middle-class families here are conservative. Savings accounts with sweep-in FD features. Sunday mornings at community centers are your prime time.

East Delhi (Laxmi Nagar, Preet Vihar) Sell business loans. It's a hub for coaching centers and small shops. Partner with local CAs. Give them 10% of your commission for referrals.

North Delhi (Rohini, Model Town) Hybrid approach. Credit cards for the parents, demat accounts for the students in Kamla Nagar.

Central Delhi (CP, Karol Bagh) High foot traffic. Set up a popup desk near a mall entrance on weekends. Focus on instant approval products people walking by don't want a 3-day process.

You don't need an office, you need a presence

Delhi people trust a face they can find.

Get a Google Business Profile. List yourself as a "Financial Advisor - GroMo Partner." When someone searches "credit card agent near me" (47,000 searches a month in Delhi), you show up. It costs nothing.

Collect video testimonials. A 45-second video of a client saying "He got my card approved in 3 days" is worth more than a flyer. Delhi runs on word-of-mouth.

Finish GroMo's certification. Put the badge on your WhatsApp status. It signals that you aren't just some guy in a basement you're part of a network.

Host webinars. "How to fix your CIBIL score" or "Best credit cards for 2026." Record them. Throw them on YouTube. Even 50 views builds authority.

Managing your time

Part-Time (15 hours/week) Call people between 7-9 PM. That's when they are home. Meet people on Saturdays. Do your admin on Sunday. Expect ₹30,000-₹50,000 a month.

Full-Time (40 hours/week) Mornings are for traders (10 AM - 1 PM). Afternoons for paperwork. Evenings for salaried clients. If you're disciplined, you hit ₹80,000-₹1.5 lakh.

Weekend Warrior If you have a 9-to-5, just work Saturdays and Sundays. Leverage your existing network. You can pull in ₹15,000-₹25,000 a month without touching your weekday job.

Delhi traffic is real. Use the phone for follow-ups. Save the physical visits for big loans (₹3 lakh+).

Play the calendar

Jan-Mar: Tax season. Push SIPs and tax-saving investments. Apr-Jun: Appraisal season. People get raises and switch jobs. Sell upgrades and relocation loans. Jul-Sep: Festival prep. Business loans for inventory peak here. Oct-Dec: Wedding season. Short-term loans and premium cards for honeymoon bookings.

Don't be shady

Never promise approval. You will look like a fraud. Instead, say: "With your profile, you have an 80% chance."

Disclose fees. If the card has a ₹499 joining fee, say it. If you hide it, the customer will find out, complain, and you'll lose the commission.

Don't touch the money. You are an advisor. The bank handles the transaction. This protects you from legal headaches.

Check the documents. Fake bank statements waste your time. Use GroMo's verification tools.

Scaling up

Once you know the game, recruit others. Train 5 people across different zones. Take 10-15% of their commission. You can generate ₹40,000-₹60,000 passively this way.

Focus on the big loans. A ₹30 lakh business loan pays ₹60,000-₹90,000. Two of those a month beats fifty credit card applications.

Approach HR departments. A single IT company in Noida with 200 employees is a goldmine for bulk credit card applications.

Common screw-ups

Trying to sell everything. Learn three products inside out. It beats knowing ten products superficially.

Forgetting to follow up. 30% of people need a nudge. Call them.

Ignoring your cousins and colleagues. Your phone contact list is your first leads. Use it.

Stopping learning. Products change. Spend two hours a week on GroMo's training.

Resources

Join the GroMo Telegram channels. 8,500 Delhi partners share tips there daily. It's the best support group you'll find.

Use the Delhi Public Library for meetings. Free WiFi, professional setting. Connaught Place and Mayapuri branches are solid.

Go to Nehru Park or Lodhi Garden meetups. Partners meet twice a month. You'll learn more in one hour there than in a week of reading.

Check out zero-investment business models for ideas outside Delhi. The strategies work in Bangalore and Mumbai too.

Read the guide to side income for the broader picture.

Legal and tax stuff

Commission is taxable income. Keep an Excel sheet.

If you cross ₹20 lakh a year, you need GST. Most partners won't hit that initially.

If you're consistently making ₹75,000+, register as a sole proprietor. It makes banking easier. Costs about ₹5,000 online.

Get professional indemnity insurance once you cross ₹1 lakh/month. It costs ₹12,000-₹15,000 a year. Worth it in Delhi.

Real examples

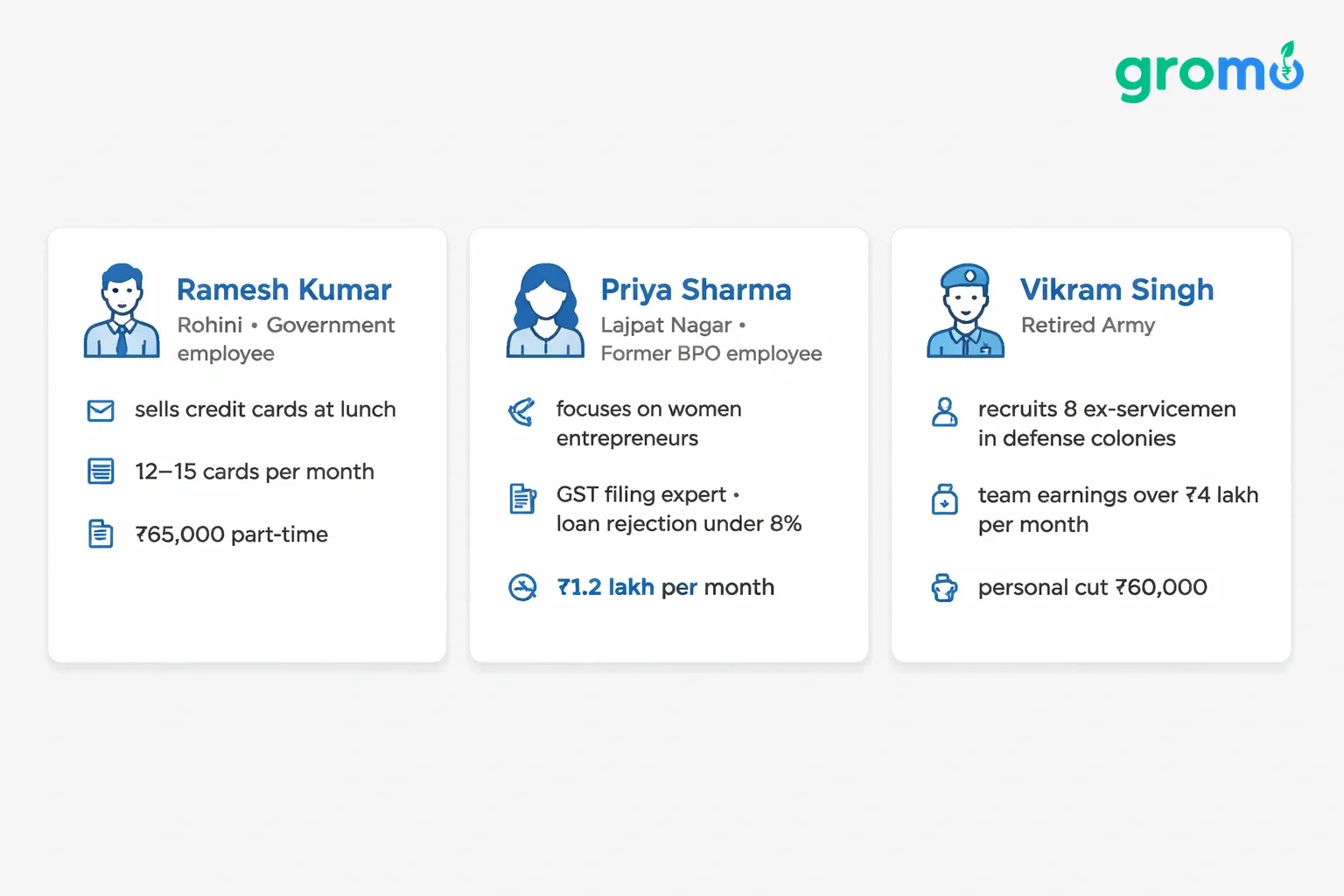

Ramesh Kumar in Rohini is a government employee. He sells credit cards to his colleagues during lunch. 12-15 cards a month. He pulls in ₹65,000 part-time. He pitches them as "45 days of free credit" instead of "a card."

Priya Sharma left her BPO job. She focuses on women entrepreneurs in Lajpat Nagar. She knows GST filings inside out, so her loan rejections are under 8%. She makes ₹1.2 lakh a month.

Vikram Singh is retired Army. He recruited 8 other ex-servicemen. They cover the defense colonies. The team makes over ₹4 lakh a month. He keeps ₹60,000 as his cut.

Start this week

Day 1-2: Download GroMo. Do the KYC. Finish the credit card module. Day 3-4: Make a list of 50 people in your phone. Sort them by income. Day 5: Message 10 of them. "I'm helping people get better financial products. No spam. Just if you need a card or loan." Day 6-7: Talk to three people. Try to close one.

From week two, aim for 5 conversations a week.

Check out how students do it. It shows how accessible this is. Compare Hyderabad and Pune markets to see the difference.

Learn from Punjab and West Bengal partners too. Different places, same model.

The long game

Year 1: You're selling. Building a name. Making ₹40,000-₹80,000. Year 2: You build a team. Get corporate clients. Income hits ₹1.5-₹2 lakh. Year 3: You're an advisor. You add mutual funds and insurance. Top partners make ₹3-5 lakh.

GroMo has paid out ₹100 crore. The model isn't a theory.

Why now

There is room. A neighborhood of 5,000 houses can support 2-3 partners. Being first in your colony matters.

The stigma is gone. Selling financial products is now a legit side hustle.

Rates are stable. Selling loans makes sense again.

Checklist

- [ ] Get the app. Register.

- [ ] Get certified.

- [ ] Set up WhatsApp Business.

- [ ] Write three pitch scripts.

- [ ] Find two spots for weekend outreach.

- [ ] Google Business Profile.

- [ ] Join the Telegram group.

- [ ] Block 10 hours a week.

- [ ] Make a comparison sheet for top cards.

- [ ] Go to your first RWA meeting.

Delhi's 32 million people need credit. You have the phone. You have the platform. You just need to show up.

Balance this with a full-time job. Avoid scams by sticking to legit methods. Learn the fundamentals of commission work.

Position it as remote work. Compare it to part-time jobs to see the upside.

FAQ

Do I need a license? No. You are a referral partner. GroMo's bank partners handle the compliance.

When do I get paid? Cards: 3-5 days after dispatch. Loans: 7 days after disbursement. Demat: 48 hours after first trade. Straight to your bank account.

Can I do this with a government job? Yes. You are a partner, not a business owner. Just don't do it on office time or property.

How fast does income grow? Month 1 is slow (₹5k-₹12k). By month 6, if you're consistent, you should be at ₹35k-₹60k.

Where is it easiest? Middle-class RWAs (Dwarka, Rohini) are easier than ultra-rich areas (Jor Bagh) where people have private bankers.

Does the customer pay me? No. Never. The bank pays you. If you ask a customer for money, you're breaking the rules and ruining your reputation.