RBI-Approved Loan Apps in India 2026: Safe Borrowing & Earnings

The digital lending market in India is crowded. Thousands of apps offer instant loans, but a significant number of them operate outside the law. With predatory recovery agents, hidden fees, and data theft on the rise, the Reserve Bank of India (RBI) has cracked down hard.

If you need a personal loan or a credit line in 2026, knowing which apps are legitimate matters. Using the wrong one can lead to harassment or a damaged credit score. This guide covers the apps backed by RBI-regulated entities, how to spot the fakes, and how platforms like GroMo let you earn by distributing these products.

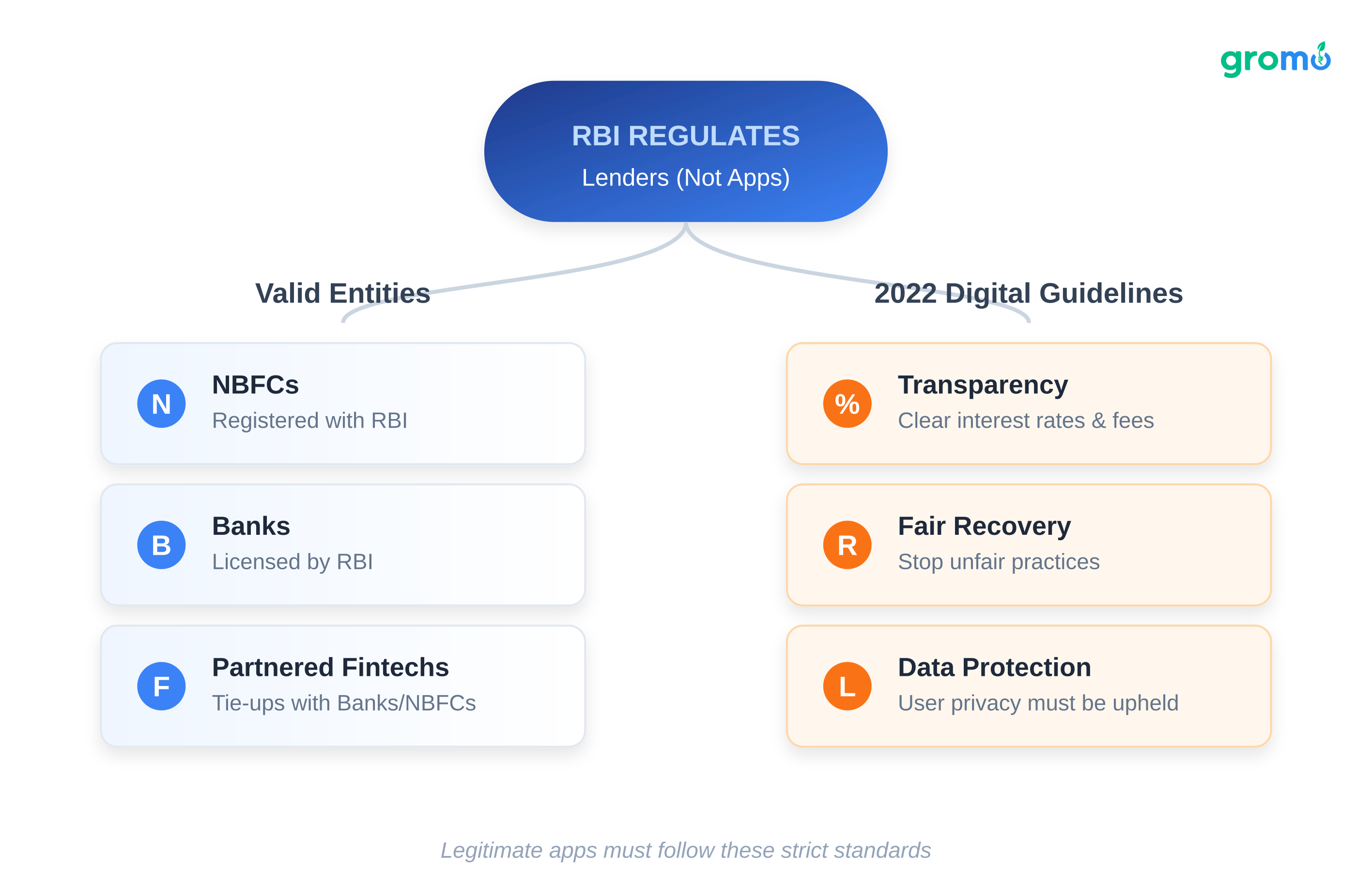

What "RBI-Approved" Actually Means

The RBI does not approve apps. It regulates the lenders.

When we talk about "RBI-approved loan apps," we mean apps backed by entities the RBI oversees:

Non-Banking Financial Companies (NBFCs) registered with the RBI

Banks licensed by the RBI

Fintech platforms that have partnered with the above

In 2022, the RBI released Digital Lending Guidelines. These rules force lenders to be transparent about interest rates, stop unfair recovery practices, and protect user data. Any legitimate app must follow these standards.

How to Spot Illegal Loan Apps

Before downloading anything, look for these red flags:

No clear lender name: If the app doesn't disclose which bank or NBFC is lending the money, it’s likely illegal.

Upfront fees: Legitimate lenders deduct processing fees from the loan amount. They never ask you to pay a fee before you get the money.

Data theft: Does the app demand access to your contacts, photos, or location? Decline. Better yet, uninstall it.

Harassment: Illegal apps are notorious for threatening calls and public shaming.

Hidden costs: If the interest rate or processing fee isn't visible on the main screen, don't trust it.

Report suspicious apps immediately via the Sachet Portal or your local cybercrime cell.

Start Earning with RBI-Approved Loan Products

Legitimate Loan Apps in India (2026)

Here is a list of apps backed by RBI-regulated banks and NBFCs.

Apps from Banks

IDFC FIRST Bank Personal Loan

IDFC offers loans up to ₹10 lakhs. Because it is a scheduled commercial bank, you get full regulatory protection.

Amount: Up to ₹10 lakh

Rate: From 9.99% p.a.

Tenure: 9–60 months

Key detail: Zero foreclosure charges.

Eligibility: CIBIL score of 700 or higher.

Axis Bank Insta Personal Loan

Existing Axis Bank customers can get pre-approved loans instantly via the mobile app.

Amount: Up to ₹40 lakh

Speed: Instant disbursal for pre-approved users.

Rate: Starts at 10.49% p.a.

Kotak Mahindra Bank InstaLoan

Kotak provides fully digital loans through its app.

Amount: Up to ₹25 lakh

Tenure: Up to 5 years

Apps from NBFCs

Bajaj Finserv Insta EMI Card

Bajaj Finserv is one of India’s largest NBFCs. Their EMI card functions like a pre-approved loan.

Limit: Up to ₹3 lakh

Rate: From 13% p.a.

Usage: Works at over 1.5 lakh partner stores.

Fullerton India Personal Loan

Fullerton is an RBI-registered NBFC with a strong physical presence.

Amount: ₹50,000 to ₹25 lakh

Rate: From 11.99% p.a.

Eligibility: Open to both salaried and self-employed individuals.

Tata Capital Personal Loan

Part of the Tata Group, this NBFC offers flexible repayment options.

Amount: Up to ₹35 lakh

Rate: From 10.99% p.a.

Muthoot Finance Personal Loan

Known for gold loans, Muthoot also offers personal loans.

Amount: Up to ₹50 lakh

Advantage: Quick processing if you visit a branch.

Fintech Platforms (NBFC Partnerships)

MoneyTap Credit Line

MoneyTap provides a revolving credit line backed by RBL Bank.

Limit: Up to ₹5 lakh

Model: Pay interest only on what you use.

EarlySalary Instant Loan

Targeted at young professionals, EarlySalary offers salary advances.

Amount: ₹5,000 to ₹5 lakh

Speed: Disbursal within 24 hours.

CASHe Instant Personal Loan

CASHe uses AI to assess creditworthiness based on social data.

Amount: Up to ₹4 lakh

Tenure: 3 to 18 months

KreditBee Personal Loan

Backed by Equitas Small Finance Bank, KreditBee is popular for quick disbursals.

Amount: Up to ₹4 lakh

Rate: Starts at 14% p.a.

InCred Personal Loan

InCred specializes in unsecured loans for salaried employees.

Amount: ₹50,000 to ₹15 lakh

Rate: From 1.33% per month

Moneyview Personal Loan

Moneyview partners with multiple NBFCs.

Amount: ₹5,000 to ₹5 lakh

Requirement: Salary must come via bank transfer.

Verification Checklist

Before you apply, do this:

Check the "About" section: Look for an NBFC registration number or bank license.

Search the RBI website: Go to rbi.org.in, look for "Lists of Entities Regulated," and search for the company name.

Check disclosures: Legitimate apps show interest rates and fees on the home screen.

Verify the address: Do they have a physical office?

Read reviews: Filter for keywords like "harassment" or "fraud."

Earning by Distributing Loans

If you want to help people find these loans or build a side income GroMo is a platform built for that exact purpose.

Only Compliant Products

GroMo works exclusively with RBI-regulated banks and NBFCs. You can refer customers to these products knowing they are legitimate.

Products currently available on GroMo include:

IDFC FIRST Bank Personal Loan (1.20% payout)

InCred Personal Loan (1.75% payout)

Moneyview Personal Loan (1.75% payout)

Lendingplate Personal Loan (3.5% payout)

SmartCoin Personal Loan (3.5% payout)

Zero Investment Required

You do not need capital to start. You earn a commission when a loan is disbursed. Payouts are instant there is no 30-day waiting period.

Training and Tools

GroMo Academy offers free training on loan products, eligibility, and compliance. The app also handles the backend work: tracking applications, managing data security, and processing payouts.

Download GroMo and Start Your Financial Business Today

The Business Model

The system works because it aligns interests:

Customers get verified loan options.

You earn a commission.

Banks get quality customers through your referrals.

GroMo claims over 60 lakh partners have earned a total of ₹100 crores through the platform. It is a scalable way to build income from anywhere. You can learn more about how to earn online with GroMo and the broader financial product distribution opportunity in India.

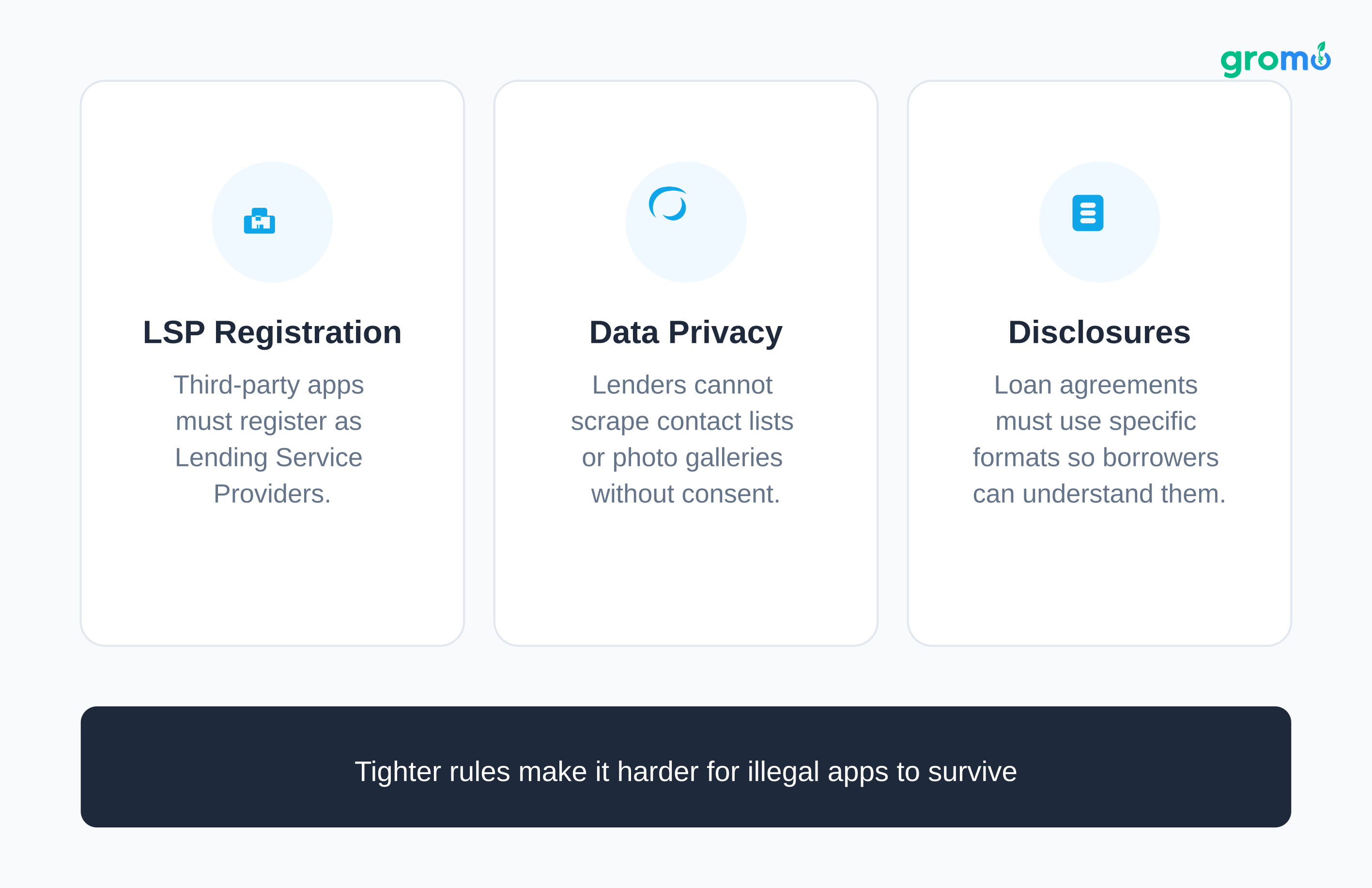

Regulation in 2026

The RBI continues to tighten the screws. Recent changes include:

LSP Registration: Third-party apps must now be registered as Lending Service Providers.

Data Privacy: Lenders cannot scrape your contact list or photo gallery.

Standardized Disclosures: Loan agreements must use a specific format so borrowers can actually understand them.

These rules make it harder for illegal apps to survive, but they also place more responsibility on legitimate distributors to stay compliant.

Borrowing Tips

If you are taking a loan:

Compare at least 3 different offers.

Look at the total interest payable, not just the EMI.

Check for prepayment penalties.

Read the agreement before signing.

Don't apply to five apps at once it hurts your credit score.

Keep your total EMIs under 50% of your monthly income.

Building an Income Stream

Distributing financial products is a viable option for professionals, students, or homemakers looking for flexible work.

The advantages are clear:

No inventory or capital needed.

Recurring income as your customer base grows.

Scalable through the GroMo referral program.

You build credibility as a financial advisor.

With training from GroMo Academy, you can learn the ropes in a few weeks, even with no prior financial background.

Conclusion

Digital lending is convenient, but only if you stick to RBI-regulated entities. Whether you are borrowing or distributing loans, verification is critical. Platforms like GroMo help by filtering out the bad actors and providing the tools to build a legitimate business.

Legitimate lending never involves upfront fees or harassment. Always check the RBI's list if you are unsure.

Ready to start? You can turn your network into income by connecting people with safe financial products. It is open to everyone.

Frequently Asked Questions

Q: How can I verify if a loan app is actually RBI-approved?

A: Go to the RBI website (rbi.org.in). Navigate to "Supervision" and then "Lists of Entities Regulated." Search for the lender's name. Legitimate apps will list their NBFC registration number or bank license clearly. They will also have a physical address and transparent fee structures.

Q: What's the difference between RBI-approved and RBI-regulated loan apps?

A: The RBI does not approve apps. It regulates the financial institutions (banks and NBFCs) behind them. An "RBI-approved" app is simply an interface for an RBI-registered lender.

Q: Can I earn money by distributing RBI-approved loan products?

A: Yes. Platforms like GroMo allow individuals to distribute financial products without investment. You earn a commission on successful disbursals. GroMo only partners with RBI-regulated entities. Payouts vary usually between 1.20% and 3.5% of the loan amount or a flat fee per disbursal.

Q: What should I do if I've already borrowed from an illegal loan app?

A: Document everything: calls, messages, and transactions. File a complaint on the RBI's Sachet Portal (sachet.rbi.org.in) and report it to the cybercrime cell. Do not pay charges that were not in the agreement. If the harassment continues, speak to a lawyer.

Q: Are personal loans from NBFCs as safe as bank loans?

A: Yes, provided the NBFC is registered with the RBI. Registered NBFCs must follow the same fair practices and transparency rules as banks. They often have faster approval times, but always verify their registration status first.

Q: How much can I realistically earn by distributing loan products through GroMo?

A: It depends on your network and effort. Active distributors earn anywhere from ₹10,000 to ₹1 lakh per month. For context, facilitating ten personal loans of ₹2 lakh each at a 3% commission yields ₹60,000. GroMo provides training and instant payouts.