Personal Loans Without Income Proof: How to Get Approved in India

Needing cash urgently but missing the standard income proofs is a familiar headache. It happens to thousands of Indians monthly freelancers, gig workers, small business owners, and salaried professionals caught between jobs. The lending space has shifted, though. Personal loans without income proof are now accessible through platforms that look at your actual money flow rather than your paperwork.

Here is how to secure a personal loan without salary slips or ITR documents, what lenders actually accept, and how platforms like GroMo fit into the picture both for borrowing and earning.

Why This Is Even Possible Now

Traditional banks are stuck on salary slips, Form 16, and ITRs. But over 40% of India's workforce doesn't fit that mold. They earn regularly but lack the "official" trails that banks trust.

Fintech lenders have adapted. They look at other signals:

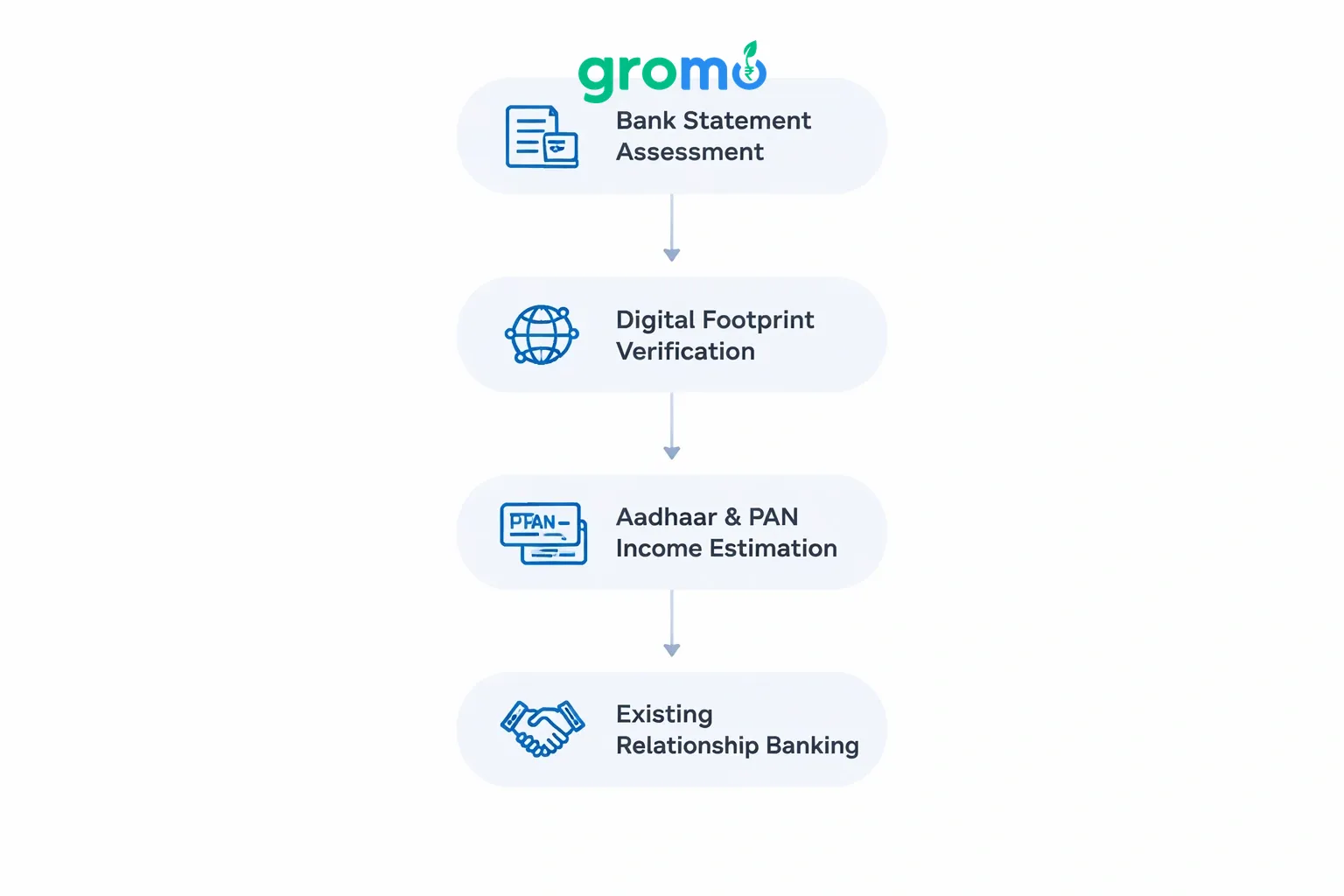

Bank Statement-Based Assessment

Instead of salary slips, lenders analyze your bank statements over 3-6 months. They look for regular credits, average balance, and spending behavior. This is a solid path for freelancers and business owners with direct payment inflows.

Digital Footprint Verification

Some use your digital presence GST returns, professional email, even app usage patterns to gauge reliability.

Aadhaar & PAN-Based Income Estimation

With consent, lenders can access linked financial data through account aggregators, getting a clearer picture without physical docs.

Existing Relationship Banking

If you have a savings account, credit card, or past loans with good repayment history, many lenders will approve based on that relationship alone.

Lenders Who Actually Approve These Loans

Let's get specific. If you're exploring these for yourself or want to help others access them here are the real options:

1. Tez Credit Personal Loan

Tez Credit targets entry-level salaried professionals with minimal documentation. Coverage is wide (8,000+ pincodes).

Loan amount: ₹5,000 to ₹2,50,000

Minimum salary requirement: ₹18,000/month

Documents needed: PAN + Aadhaar + basic salary proof (bank statements with regular credits often suffice)

Approval: Instant digital approval

Payout for distributors: 3.5% commission

Tez Credit is accessible even if you've just started working and don't have months of salary slips.

2. Lendingplate Personal Loan

Lendingplate built its model around bank statement analysis.

Assessment method: Bank statement-based (Account Aggregator or manual upload)

Key requirement: Current residence must match application pincode

Alternative address proof: Gas bills, rent agreements, electricity bills, or property documents work if you live elsewhere

Verification: Workplace ID and work email instead of salary slips

Payout: 3.5% commission for distributors

You upload 3-6 months of bank statements. Their AI analyzes income patterns and repayment capacity.

3. Zype Personal Loan

Zype offers a very fast approval process roughly 6 minutes with digital income verification.

Loan amount: Up to ₹5 lakhs

Tenure: Flexible up to 36 months

Processing fee: 2-4% + GST

ROI: Rates based on credit profile

Verification: Digital credit bureau check + basic employment details

Payout: 2.75% commission

The mobile-first approach means you can apply entirely through their app. Their underwriting focuses on credit behavior over physical docs.

4. Smartcoin Personal Loan

This one suits self-employed individuals and small business owners.

Loan amount: Up to ₹1 lakh

Tenure: Shorter repayment periods

Special offer: Coupon code DADA50 gets you 50% off processing fees (up to ₹250)

Acceptance: Business income, freelance earnings, and regular bank credits

Payout: 2.25% commission

Smaller ticket sizes make this ideal for urgent, short-term needs without the documentation burden.

What You Can Submit Instead of Salary Slips

If you're applying without standard proofs, here's what actually works:

For Salaried Professionals:

3-6 months of bank statements showing salary credits

Last 3 months' payslips (even unofficial email versions)

Employment contract or offer letter

Form 16 from the previous year (if available)

Professional email ID verification

Employer confirmation letter

For Self-Employed/Freelance Workers:

Bank statements showing client payments

GST returns (for registered businesses)

Current account statements

Client contracts or payment agreements

Professional invoices

Trade license or business registration

CA-certified income statements

For Business Owners:

Business bank account statements (6 months)

GST filings

Udyam/MSME registration certificate

Business PAN card

TDS certificates

Profit & Loss statements

Universal Alternatives:

Fixed Deposit receipts

Property ownership documents

Investment portfolio statements

Existing loan repayment track record

Credit card statements with regular repayments

How the Bank Statement Method Actually Works

Since bank statement assessment is the most common alternative, let's look at what lenders actually hunt for:

Monthly Income Pattern

They analyze credits over 3-6 months. They want to see:

Regular, consistent credits (amounts can vary)

Multiple income sources are fine

Average monthly credit hitting their minimum threshold (usually ₹18,000-₹25,000)

Financial Stability Indicators

Your statements reveal:

Average monthly balance

How often you hit zero

Overdraft usage

Returned cheques or failed transactions

EMI payment regularity

Spending Behavior

Your spending tells them:

Fixed obligations (existing EMIs, rent)

Discretionary spending habits

Savings capacity

Red Flags

These hurt your chances:

Frequent cash deposits without a clear source

Circular transactions (money moving in and out within days)

Gambling or betting transactions

Heavy ATM withdrawals suggesting a cash-based lifestyle

Bounced cheques

Practical advice: If you're planning to apply, clean up your banking habits for at least 3 months prior. Keep a decent average balance, avoid unnecessary overdrafts, pay existing EMIs on time, and favor digital payments over cash.

If You Have Zero Credit History (NTC)

If you've never taken a loan or owned a credit card, you're NTC (New to Credit). This makes traditional income proof even more critical for standard lenders.

But some platforms handle NTC customers:

Approach for NTC Applicants:

Start small (₹25,000-₹50,000) where approval is easier

Try secured loans first (against FD or property) which don't need income proof

Build credit history gradually through small loans with perfect repayment

Use low-limit credit cards and keep utilization around 30%

Look at NBFC products over traditional banks initially

Products like Tez Credit are more NTC-friendly because they look at current employment and bank behavior rather than lengthy credit history.

The GroMo Angle: Earning From What You Learn

Here's the part most people miss: while you're researching loans for yourself, you can also become a loan distributor and earn by helping others.

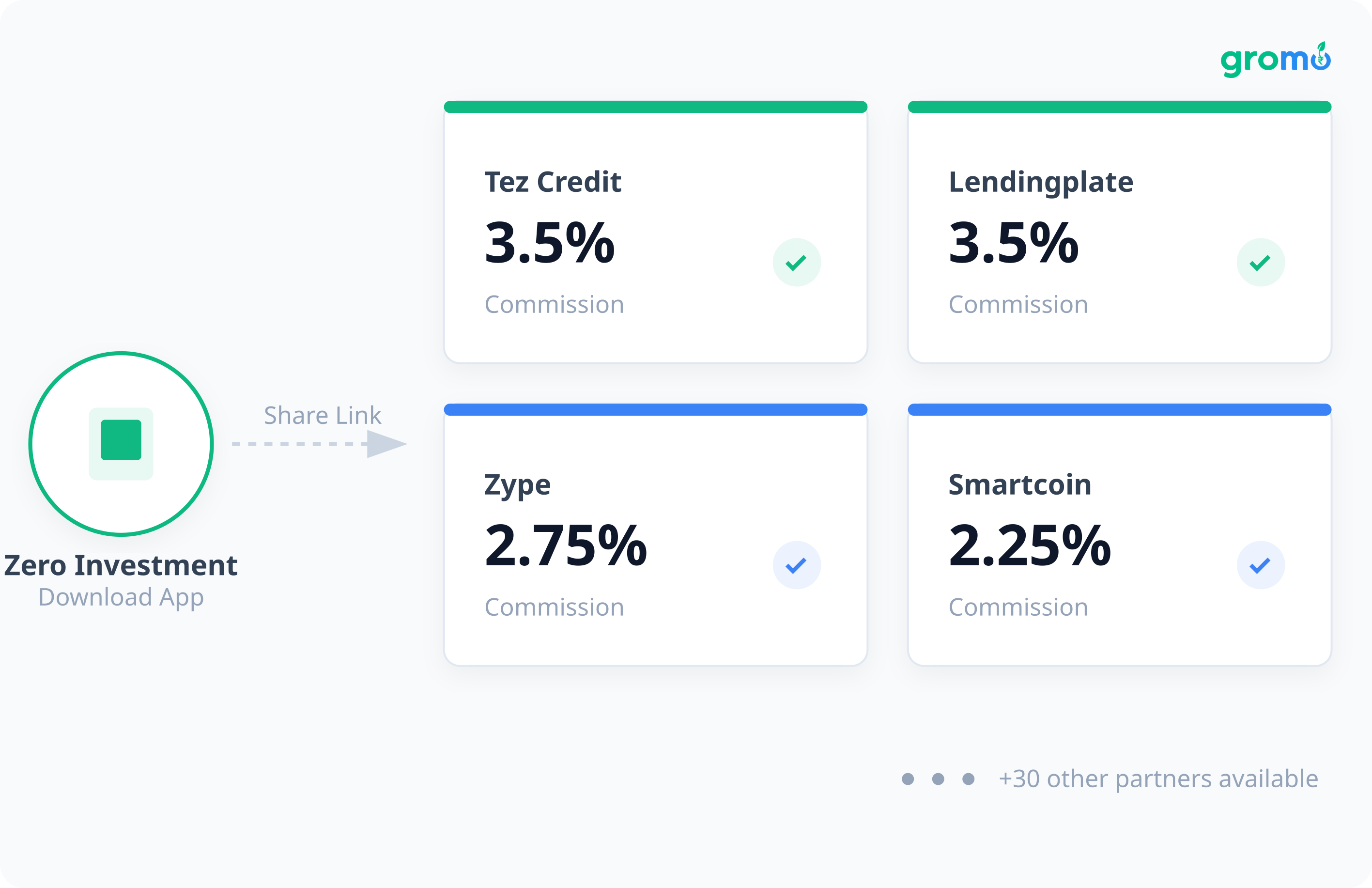

GroMo partners with Tez Credit, Lendingplate, Zype, Smartcoin, and 30+ others.

Zero Investment Model

Download the GroMo app and you're ready. No upfront cost.

Commission on Every Approved Loan

Share a loan product link through GroMo. When someone gets their loan approved and disbursed, you earn:

3.5% on Tez Credit loans

3.5% on Lendingplate loans

2.75% on Zype loans

2.25% on Smartcoin loans

Example Earnings:

Help 10 people get personal loans of ₹1 lakh each through Tez Credit:

Total loan value: ₹10 lakhs

Your commission at 3.5%: ₹35,000

Free Training & Certification

GroMo offers free courses on financial products, lending regulations, and sales techniques. You can become a certified financial advisor without paying for courses.

Customer Management Tools

Track leads, set reminders, monitor application status, and receive instant payout all in the app.

Myths vs. Reality

Let's knock down some common misconceptions:

"These are high-interest scams"

Not true. RBI-registered lenders offer competitive rates (starting from 9.99% p.a. for products like IDFC First Bank Personal Loan). The rate depends on your credit score, not documentation type.

"Only people with bad credit need these"

Freelancers and entrepreneurs with excellent credit use these products because they're more convenient than paperwork stacks.

"Approval amounts are tiny"

Lenders like IDFC First Bank and InCred offer up to ₹10-15 lakhs with alternative verification if you have good credit history.

"These loans hurt your CIBIL score"

Any RBI-regulated personal loan builds credit if repaid on time. Only unregulated lenders cause damage.

"You can't prepay"

Products like IDFC First Bank Personal Loan offer zero foreclosure charges. You can prepay anytime.

The Application Timeline: What Really Happens

Here's a realistic view of the process using alternative documentation:

Day 1: Research & Application

Compare options on platforms like GroMo

Check eligibility (age, pincode, credit score)

Download 6 months of bank statements

Apply via lender's app or website

Day 1-2: Initial Verification

Mobile number verification (OTP)

PAN and Aadhaar submission

Bureau check consent

Basic personal and professional details

Day 2-3: Income Assessment

Upload bank statements or link via Account Aggregator

AI analyzes your income pattern

Soft offer generated

Day 3-4: KYC & Documentation

DigiLocker-based Aadhaar verification

Selfie verification

Address proof (if current address differs from Aadhaar)

Work email verification

References (2-3 contacts)

Day 4-5: Final Approval

Manual review by lender

Final amount and rate determined

Loan agreement sent for e-signature

Day 5-7: Disbursal

Set up auto-pay mandate

Sign digitally

Money hits your account

Total timeline: 5-7 working days for most. Zype claims 6-minute approvals for pre-qualified profiles.

How to Improve Your Odds

Before You Apply:

Check your credit score aim for 700+

Clean up your bank statements: 3-6 months of healthy behavior

Reduce credit card utilization below 30%

Avoid multiple applications in short periods

Stay at your current address for at least a year if possible

During Application:

Be accurate: Mismatches cause rejections

Use official email ID: Professional addresses score better for self-employed

Keep documents ready: PAN, Aadhaar, statements, address proof

Respond quickly: Fast responses speed up processing

After Approval:

Set up auto-pay: Never miss an EMI

Avoid prepayment in first 3 months: Clawback clauses can reverse your GroMo commission

Maintain the account: This proves creditworthiness for future needs

Dealing with Rejection

Rejection happens. Here's what to do:

Immediate Steps:

Ask for the rejection reason

Check if it's soft (retry later) or hard

Verify your credit report for errors

Common Rejection Reasons & Fixes:

Reason | Solution |

|---|---|

Low credit score (<650)< p> | Wait 3-6 months, pay existing dues on time, reduce utilization |

Insufficient income proof | Try lenders with lower thresholds (Tez Credit at ₹18k) or show additional income |

High existing debt | Pay off smaller loans, close unused cards |

Employment stability issues | Wait until you have 1 year at current job |

Pincode not serviceable | Try different lenders |

Recent loan enquiries | Wait 3 months |

Alternative Routes:

Secured loans (against FD, property, mutual funds)

Credit cards for short-term needs

Gold loans (asset-based)

Peer-to-peer lending platforms

Turning This Into Income

Once you understand these loans, you have valuable knowledge. Here's how to monetize it via GroMo:

Your Target Audience:

Freelancers and gig workers you know

Small business owners nearby

Young professionals who switched jobs recently

Self-employed consultants

Traders and commission agents

Your Pitch:

"I can help you get a personal loan without salary slips just your bank statements."

Earnings Potential:

Average loan: ₹2 lakhs

Average commission: 3%

Earnings per case: ₹6,000

5 cases a month: ₹30,000

15 cases: ₹90,000-₹1 lakh

Getting Started:

Download the GroMo app

Complete free certification

Share links via WhatsApp or direct conversation

Guide applicants

Track in your dashboard

Get paid on disbursal

Read more about how GroMo partners earn.

Staying Legal and Compliant

As a Borrower:

Borrow only from RBI-registered lenders (learn how to spot them)

Read the agreement before signing

Know the effective interest rate and all charges

Never share OTPs or credentials

Report harassment to RBI Ombudsman

As a GroMo Partner:

Never guarantee approval

Don't pitch "salaried only" products to self-employed people

Use only UTM-tracked links from GroMo

Remember clawback clauses (first 3 EMIs must be paid)

Give accurate info

Don't encourage faking documents

Real Examples

Rajesh, Freelance Graphic Designer, Mumbai

"I've freelanced for 4 years with solid income but no salary slips. Banks rejected me for a ₹3 lakh wedding loan. Through GroMo, I found Lendingplate. They approved it based on bank statements showing client payments. Took 6 days."

Priya, Boutique Owner, Bangalore

"Needed ₹5 lakhs for inventory. I don't file ITR yet. Tez Credit accepted my business statements and GST records. I got the loan, then started using GroMo to help other boutique owners now I'm making ₹40k monthly from commissions."

Amit, Marketing Consultant, Delhi

"Switched from corporate to consulting. Three months in, I needed funds. Old salary slips didn't count. Zype's 6-minute approval using bank statements saved me. I shared the option with consultant friends and made ₹18,000 in my first month as a GroMo partner."

Where This Is All Going

Income verification is changing fast.

Account Aggregator Framework: RBI's AA system allows instant, consent-based access to financial data across institutions. No more manual docs.

Alternative Credit Scoring: Fintechs look at utility payments, rent payments, even smartphone usage patterns.

Open Banking: APIs connect banks, lenders, and borrowers for real-time verification.

UPI Analysis: Your UPI credits and debits create a digital income trail lenders can assess instantly.

Traditional income proof is fading. A healthy digital financial footprint is becoming the new standard.

Next Steps

If You Need a Loan:

Download 6 months of bank statements

Check your credit score

Compare options on GroMo

Apply to the lender fitting your profile

Keep digital docs ready

If You Want to Earn:

Download the GroMo app

Do the free certification

Start with friends and family

Build your network

Track and scale

You don't need stacks of paperwork anymore. With alternative verification and platforms like GroMo connecting borrowers to lenders, access to credit is opening up. Just remember: prioritize transparency, stick to RBI-regulated lenders, and think long-term financial health, not just quick cash or commissions.

Frequently Asked Questions

Q: Can I get a personal loan without any income proof whatsoever?

A: You don't need traditional salary slips, but lenders need to assess repayment. The minimum is usually 3-6 months of bank statements showing regular credits (salary, business income, freelance payments). Lenders like Tez Credit and Lendingplate accept bank statement-based verification.

Q: Will applying for a loan without income proof hurt my credit score?

A: Documentation type doesn't affect your score. Repayment behavior does. A well-managed loan improves your score. Only multiple rejections or missed EMIs hurt. Apply selectively to lenders matching your profile.

Q: How long does approval take using bank statements?

A: Similar to traditional loans 5-7 working days. Some like Zype claim 6-minute approvals for pre-qualified profiles. Have clean statements, PAN, Aadhaar, and address proof ready. Analysis takes 2-3 days, verification and disbursal another 2-3.

Q: What's the minimum credit score needed?

A: Most prefer 700+ for unsecured loans. Some like Tez Credit and Smartcoin are flexible, approving 650-675 if bank statements show strong income. Below 650, build your score first via secured products or smaller loans.

Q: Can self-employed people get the same loan amounts as salaried?

A: Yes. Lenders like Lendingplate, Smartcoin, and InCred cater to self-employed borrowers. Amounts depend on income and credit history, not employment type. Successful entrepreneurs often qualify for larger amounts (₹5-15 lakhs) than entry-level salaried applicants. Demonstrate consistent income and maintain good credit.

Q: How does GroMo's commission work?

A: Share a loan link. When your referral gets approved and disbursed, you earn a percentage (1.75% to 3.5% depending on lender). A ₹2 lakh loan via Tez Credit (3.5%) earns ₹7,000. Payout is instant to your GroMo wallet. Watch for clawback clauses if the borrower defaults in the first 3 EMIs, commission may be reversed. Guide people responsibly.