How to Get Cash from Credit Cards: Costs & Alternatives

Credit cards are useful until you actually need cash. Swiping for groceries is easy, but try moving that money to your bank account and suddenly the fees pile up. If you are staring down a medical bill or an emergency where a card swipe won't work, you need to know your options.

Here is how to get cash from your credit card, what it will actually cost you, and why you should think twice before doing it.

Why Move Money From a Credit Card?

Usually, it's necessity, not choice. You might have a landlord who refuses cards, a vendor who needs a bank transfer, or an emergency that emptied your savings.

Just remember: this is expensive money. It works in a pinch, but relying on it is a fast track to debt problems.

Method 1: Cash Withdrawal at ATM (The Expensive Way)

You can walk up to an ATM and use your credit card just like a debit card. It’s called a cash advance.

The catch: It is incredibly expensive.

Fees: You pay 2.5% to 3% just to take the money out, plus an ATM fee.

Interest: You get hit with 2.5% to 3.5% per month (that’s over 30% a year).

No grace period: Interest starts the second the cash leaves the machine.

Example: Withdraw ₹10,000.

You pay roughly ₹750 in fees and interest for the first month alone. That’s an instant 7.5% tax on your own money.

Explore Better Financial Solutions – Download GroMo Now

Method 2: Digital Wallets (The Cheaper Workaround)

Apps like Paytm, PhonePe, and Amazon Pay let you "load" money via credit card and then transfer it to your bank. It’s a few extra steps, but it saves money.

The Process

Add money to your wallet using your credit card.

Transfer that balance to your bank account.

The Cost

Expect to pay about 2% to 2.5% in fees. It’s cheaper than an ATM, but you still lose a chunk.

Wallet | Daily Limit | Transfer-to-Bank Fee |

|---|---|---|

Paytm | ₹50,000 | Free (basic KYC) |

PhonePe | ₹1,00,000 | Free |

Amazon Pay | ₹10,000 | Free |

Method 3: UPI Apps (Limited)

You can link credit cards to UPI now (HDFC, ICICI, Axis, and others support this). But here’s the fine print: it’s meant for paying merchants, not transferring cash to friends or your own account.

If you try to use it like a wallet, the app will likely treat it as a cash advance and charge you those high rates anyway.

Method 4: Fund Transfer Apps

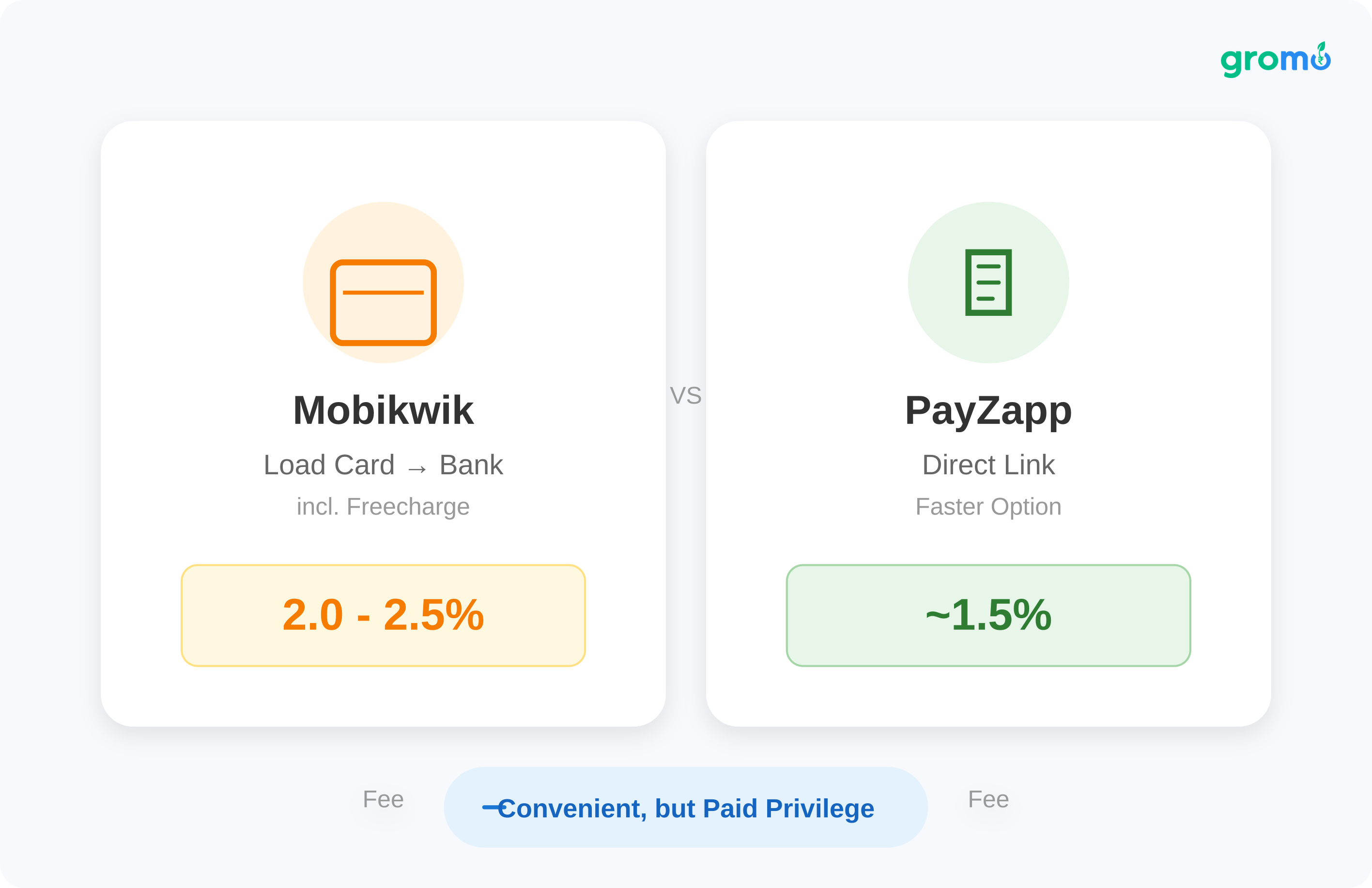

Apps like Mobikwik and Freecharge specialize in this.

Mobikwik: Load with a card, transfer to a bank. Fees hover around 2-2.5%.

PayZapp: Often cheaper, around 1.5%.

It’s convenient, but you are paying for the privilege.

Method 5: Balance Transfer to Personal Loan (The Smart Way)

If you need the money for more than a few weeks, stop looking at cash advances. Look at a balance transfer.

This converts your credit card debt into a personal loan.

Interest: Drops from 36-42% to around 11-18%.

Time: You get 6 to 60 months to repay.

The Math:

On a ₹1,00,000 transfer, a cash advance could cost you ₹36,000+ in interest a year. A personal loan might cost you ₹15,000. The difference is massive. Most major banks (HDFC, ICICI, SBI) offer this instantly through their apps.

Start Your Financial Journey – Join 60L+ Partners on GroMo

Method 6: Pay Bills, Keep the Cash

This is a hack, not a transfer. Use your credit card to pay your rent, electricity, or insurance through apps like Cred or BillDesk. Then, keep the cash you would have spent on those bills.

You pay a small convenience fee (maybe ₹100-₹300), but you avoid cash advance interest entirely and keep your 45-day interest-free window.

Smart Alternatives

Before you pay the fees, consider:

Personal Loan: Cheaper interest, fast approval.

Salary Advance: Many employers offer this for free.

Side Income: It sounds preachy, but earning an extra ₹10,000 a month solves the problem better than borrowing. You can sell financial products via GroMo or check out zero-investment business models to build a buffer.

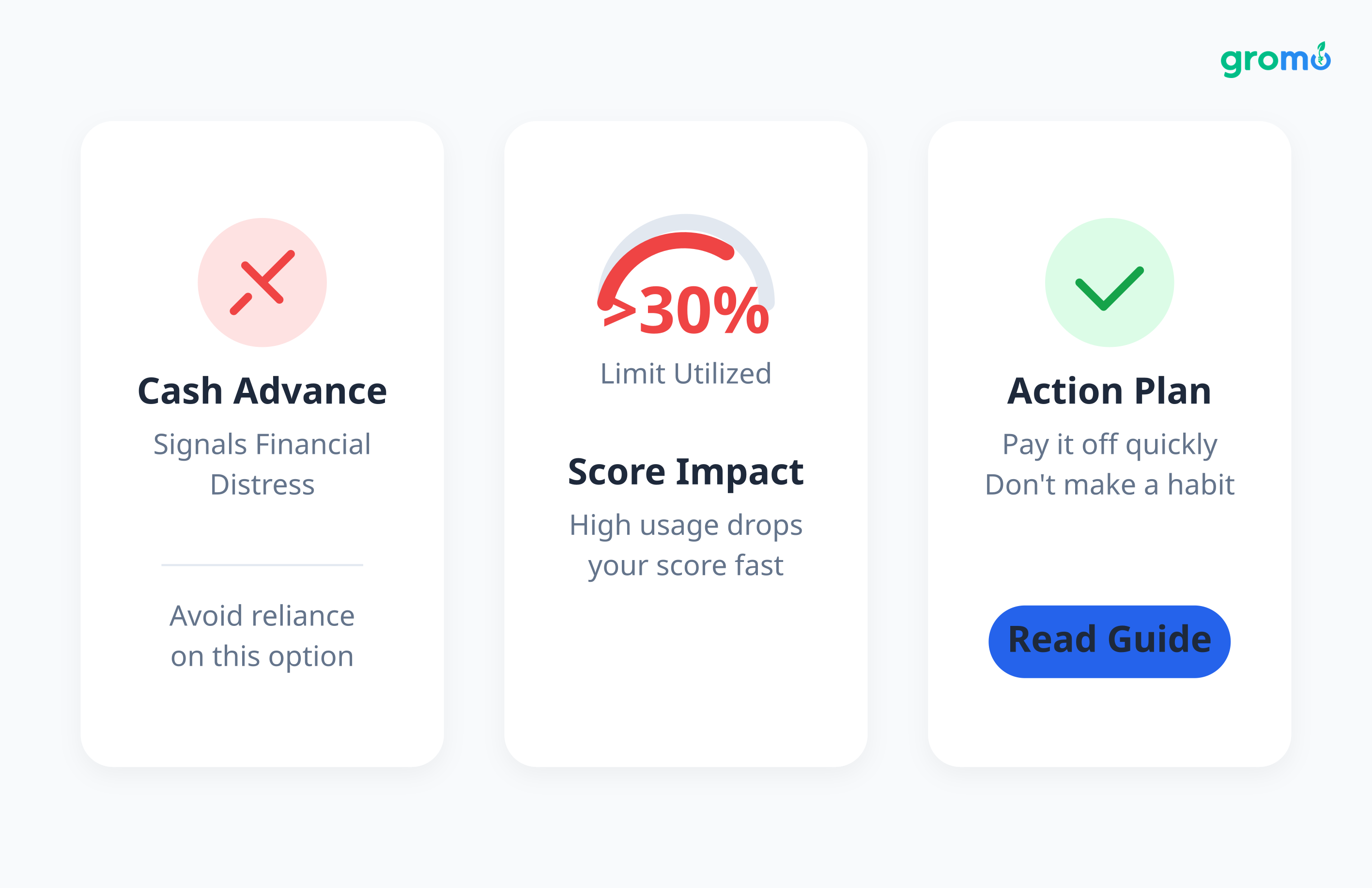

Your Credit Score Will Take a Hit

Cash advances signal financial distress. High utilization (using more than 30% of your limit) drops your score fast. If you go this route, pay it off quickly and don't make a habit of it. If your score is already suffering, read our guide on improving your credit score.

Tax and Legal Notes

The transfer isn't taxed, but moving large sums (over ₹2 lakhs) attracts scrutiny. Keep receipts to show where the money went.

Also, beware the debt spiral. I have seen people start with a ₹10,000 transfer and end up in a ₹1,00,000 hole six months later because they borrowed to pay off the previous month. If you are using credit for daily expenses, check out legitimate income opportunities instead of digging deeper.

Walkthrough: Moving ₹50,000 the Smart Way

If you need ₹50,000, don't use an ATM. Do this:

Day 0: Open your banking app. Find "Credit Card to Loan" or "Balance Transfer."

Day 0: Enter the amount and tenure (12 months).

Day 1-2: Get approved (usually instant for existing customers).

Day 2-5: Money hits your account.

Cost Comparison:

ATM Advance: ~₹19,550 in fees and interest.

Balance Transfer: ~₹5,300. You save nearly ₹15,000.

When to Just Say No

Do not use credit card transfers for:

Gambling or speculation.

Paying off other credit cards (this is a trap).

Luxury items you can't afford.

For medical needs, check if the hospital offers EMI. For business, look at MUDRA loans. For everything else, try to wait until you have the cash.

Frequently Asked Questions

Q: Is this legal?

A: Yes. Banks call it a cash advance. But keep records of how you use the funds.

Q: Wallet vs ATM?

A: Wallets are cheaper (around 2% vs 4%+). Loans are cheapest for long-term needs.

Q: Will it hurt my credit score?

A: Yes. It increases your utilization ratio and looks like risky behavior to lenders.

Q: Can I transfer to someone else's account?

A: Technically yes, but it triggers fraud alerts. Use official channels like a balance transfer if you are helping family.