Health Insurance Terms & Definitions: Exhaustive List

Terms And Definitions of Health Insurance Actuarial value: A measure of how much of the cost of covered health care services a health insurance plan covers

Terms And Definitions of Health Insurance

-

Actuarial value: A measure of how much of the cost of covered health care services a health insurance plan covers.

-

Adverse selection: The tendency for people who are more likely to use health care services to be more likely to purchase health insurance.

-

Affordable Care Act (ACA): A federal law that was enacted in 2010 and that has expanded health insurance coverage to millions of Americans.

-

Annual deductible: The amount of money that you must pay out of pocket for covered health care services before your health insurance plan begins to pay.

-

Annual out-of-pocket maximum: The maximum amount of money that you must pay out of pocket for covered health care services in a year.

-

Benefit: A health care service that is covered by your health insurance plan.

-

Blue Cross and Blue Shield: A group of health insurance companies that offer health insurance plans in all 50 states.

-

Catastrophe (CAT) plan: A type of health insurance plan that has lower premiums than traditional health insurance plans, but that also has higher deductibles and out-of-pocket maximums.

-

Coinsurance: A percentage of the cost of covered health care services that you must pay after you have met your annual deductible.

-

Copayment: A fixed amount of money that you must pay for covered health care services, regardless of the cost of the service.

To sell this product, and many other financial products. DOWNLOAD GROMO. Where you can sell and earn a substantial income sitting at home

DOWNLOAD GROMO

-

Cost sharing: The portion of the cost of covered health care services that you must pay, either in the form of copayments, coinsurance, or deductibles.

-

Coordination of benefits: A provision in some health insurance plans that helps to prevent you from being billed for the same health care service more than once.

-

Deductible: The amount of money that you must pay out of pocket for covered health care services before your health insurance plan begins to pay.

-

Employer-sponsored health insurance: Health insurance that is offered by employers to their employees.

-

EPO: A type of health insurance plan that covers a limited network of doctors and hospitals.

-

Exclusion: A health care service that is not covered by your health insurance plan.

-

Health insurance: A type of insurance that helps to pay for the cost of health care services.

-

Health savings account (HSA): A tax-advantaged savings account that can be used to pay for qualified medical expenses.

-

High-deductible health plan (HDHP): A type of health insurance plan that has a high annual deductible, but that also has lower premiums than traditional health insurance plans.

-

In-network: A doctor or hospital that is part of your health insurance plan's network.

-

Out-of-network: A doctor or hospital that is not part of your health insurance plan's network.

-

Out-of-pocket maximum: The maximum amount of money that you must pay out of pocket for covered health care services in a year.

-

Premium: The monthly cost of health insurance.

-

Prescription drug coverage: A type of health insurance coverage that helps to pay for the cost of prescription drugs.

-

Primary care doctor: A doctor who provides general health care services, such as checkups and preventive care.

-

PPO: A type of health insurance plan that allows you to see doctors and hospitals in and out of network.

-

Removal of exclusions and limitations: A provision in some health insurance plans that helps to ensure that you will not be denied coverage for a pre-existing condition.

-

Self-funded health insurance: Health insurance that is purchased by an employer or individual directly from an insurance company.

-

Specialist: A doctor who is an expert in a particular area of medicine, such as cardiology or oncology.

-

Surprise billing: A situation in which you are billed for health care services by a doctor or hospital that is not part of your health insurance plan's network.

-

Umbrella health insurance: A type of supplemental health insurance that can help to pay for the cost of health care services that are not covered by your primary health insurance plan.

-

Waiting period: A period of time during which you must wait before your health insurance plan begins to pay for covered health care services.

CHECK OUT NOW!

- Term Life Insurance Definitions: Related Terms Explained

- Top Providers Of Investment Insurance: 10 Providers List

- Investment Products Definitions: Related Terms Explained

- Instant Loans Definitions: Exploring Its Related Terms

-

Deductible: The amount of money that you must pay out of pocket each year before your health insurance plan starts to pay for covered services.

-

Durable medical equipment (DME): Medical equipment that is used for more than a short period of time, such as a wheelchair or a walker.

-

Exclusion: A service or condition that is not covered by your health insurance plan.

-

In-network: A doctor, hospital, or other health care provider that has a contract with your health insurance plan.

-

Out-of-network: A doctor, hospital, or other health care provider that does not have a contract with your health insurance plan.

-

Premium: The monthly amount that you pay for your health insurance plan.

Prescription drug: A medication that is prescribed by a doctor.

39 Preventive care: Health care services that are designed to prevent illness or disease, such as annual physicals and vaccinations.

- Surprise medical bill: A bill for health care services that you received from an out-of-network provider, even though you thought you were seeing an in-network provider.

CHECK OUT!

- Motor Insurance Terms And Definitions: Exhaustive List

- Term Life Insurance Definitions: Exhaustive List

- Investment Insurance Definitions: Related Terms Explained

- Top Providers Of Vehicle Loans: 5 Providers In India

These are just a few of the many terms that you may encounter when you are shopping for health insurance. It is important to understand these terms so that you can make an informed decision about your coverage.

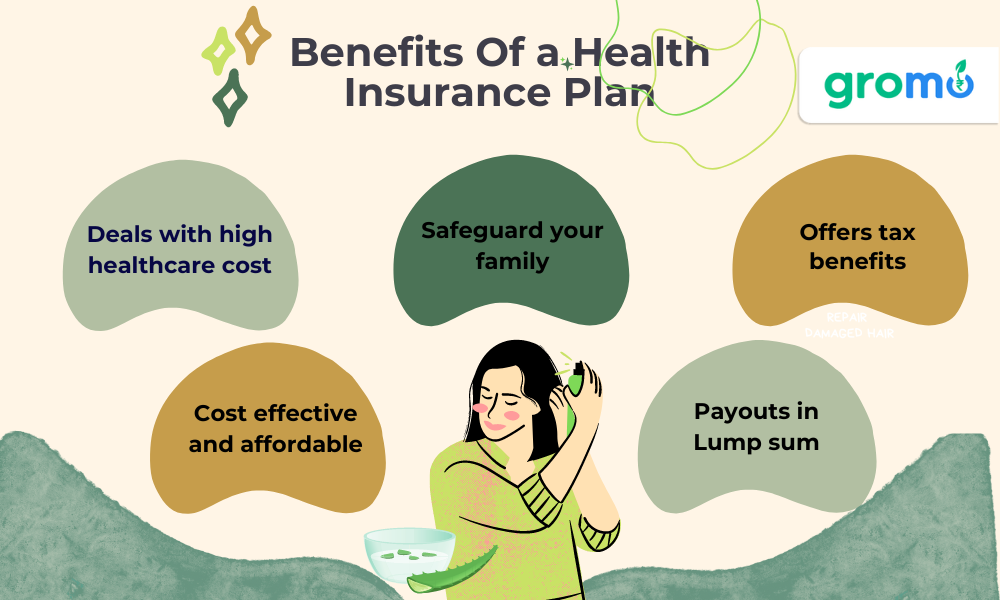

Health insurance plays a vital role in safeguarding individuals and families from the financial burden associated with medical expenses

It provides access to quality healthcare services and protects against unexpected medical emergencies. This guide aims to provide a comprehensive overview of health insurance, its benefits, types, key terminologies, and tips for choosing the right coverage.

Importance of Health Insurance:

Health insurance offers numerous advantages, including financial protection, access to a wide range of medical services, preventive care, and peace of mind. It acts as a safety net, ensuring that individuals can receive necessary medical treatments without facing exorbitant costs.

Understanding Health Insurance Basics:

a. Premiums: The amount paid periodically to maintain coverage.

b. Deductibles: The initial out-of-pocket amount paid by the insured before the insurance coverage kicks in.

c. Copayments and Coinsurance: Cost-sharing mechanisms where the insured pays a percentage of the medical expenses while the insurer covers the rest.

d. Out-of-Pocket Maximum: The maximum amount an insured individual has to pay during a policy year.

Types of Health Insurance Plans:

A. Employer-Sponsored Plans: Coverage provided by employers to their employees and sometimes their families.

B. Individual and Family Plans: Coverage purchased directly by individuals or families from insurance companies.

C. Government-Sponsored Plans: Such as Medicare for seniors and Medicaid for low-income individuals.

D. Health Maintenance Organization (HMO): A managed care plan that requires individuals to choose a primary care physician and obtain referrals for specialist visits.

E. Preferred Provider Organization (PPO): A plan that offers more flexibility in choosing healthcare providers without the need for referrals.

F. Point of Service (POS): A hybrid plan that combines features of HMO and PPO, allowing individuals to choose between in-network or out-of-network providers.

Key Considerations for Choosing Health Insurance:

a. Coverage: Evaluate the extent of coverage for services like hospitalization, prescription drugs, maternity care, and preventive care.

b. Network: Assess the network of healthcare providers and hospitals included in the plan to ensure access to preferred doctors or specialists.

c. Costs: Compare premiums, deductibles, copayments, and coinsurance to determine the most cost-effective plan.

d. Prescription Drug Coverage: Evaluate the formulary and coverage for medications required on a regular basis.

e. Additional Benefits: Look for additional benefits such as telemedicine, wellness programs, and preventive care services.

Open Enrollment and Special Enrollment Periods:

A. Open Enrollment: A specific period during which individuals can enroll, renew, or make changes to their health insurance plans.

B. Special Enrollment Periods (SEPs): Limited-time periods allowing individuals to enroll or make changes outside of the regular open enrollment period due to specific life events like marriage, job loss, or the birth of a child.

Understanding Terms:

A. Preauthorization: Prior approval required by the insurance company for certain medical procedures or services.

B. In-Network and Out-of-Network: Healthcare providers that have contracted with the insurance company are considered in-network, while those who haven't are considered out-of-network.

C. Explanation of Benefits (EOB): A summary of services rendered, the amount billed, the amount covered by insurance, and the amount the insured is responsible for.

Looking for an app for earning online? GroMo is your answer! Now earn with each sale by selling various kinds of financial products

Tips for Utilizing Health Insurance Effectively:

a. Familiarize Yourself with Policy Details: Understand the coverage, network, and benefits offered by your health insurance plan.

b. Regularly Review Your Plan: Assess your needs and determine if your current plan meets your requirements.

c. Maintain a Healthy Lifestyle: Preventive care and healthy habits can help reduce healthcare costs in the long run

KEY TAKEAWAYS

-

Importance of Health Insurance: Health insurance is essential for financial protection against unexpected medical expenses. It provides access to quality healthcare services and ensures peace of mind, knowing that necessary treatments can be received without incurring significant costs.

-

Understanding Coverage Options: There are various types of health insurance plans available, including employer-sponsored plans, individual and family plans, and government-sponsored plans like Medicare and Medicaid. It is crucial to understand the different options and choose a plan that suits your specific needs and budget.

-

Evaluating Plan Features: When selecting a health insurance plan, consider factors such as coverage, network of healthcare providers, costs (premiums, deductibles, copayments, and coinsurance), prescription drug coverage, and additional benefits like telemedicine and wellness programs. Carefully assessing these features will help ensure that you choose the most suitable plan for your healthcare needs.

-

Open Enrollment and Special Enrollment Periods: Open enrollment is a designated period during which individuals can enroll, renew, or make changes to their health insurance plans. Additionally, special enrollment periods (SEPs) are available for specific life events such as marriage, job loss, or the birth of a child. Understanding these enrollment periods is essential for making timely decisions regarding health insurance coverage.

-

Effective Utilization of Health Insurance: To make the most of your health insurance, familiarize yourself with the policy details, including terms like preauthorization, in-network, out-of-network, and explanation of benefits (EOB). Regularly review your plan to ensure it meets your changing needs, and focus on maintaining a healthy lifestyle and utilizing preventive care to minimize healthcare costs in the long run.