Credit Cards Meaning: Exhaustive List

Credit cards have become an integral part of our financial lives, offering convenience and flexibility in making purchases and managing expenses

Credit cards have become an integral part of our financial lives, offering convenience and flexibility in making purchases and managing expenses. Understanding the key terms and definitions associated with credit cards is essential for responsible usage and financial well-being. In this article, we will explore and define various terms related to credit cards.

1. Credit Card

A credit card is a payment card issued by a financial institution that allows the cardholder to borrow funds for purchases and pay them back at a later date. It enables individuals to make transactions both online and offline, up to a predetermined credit limit.

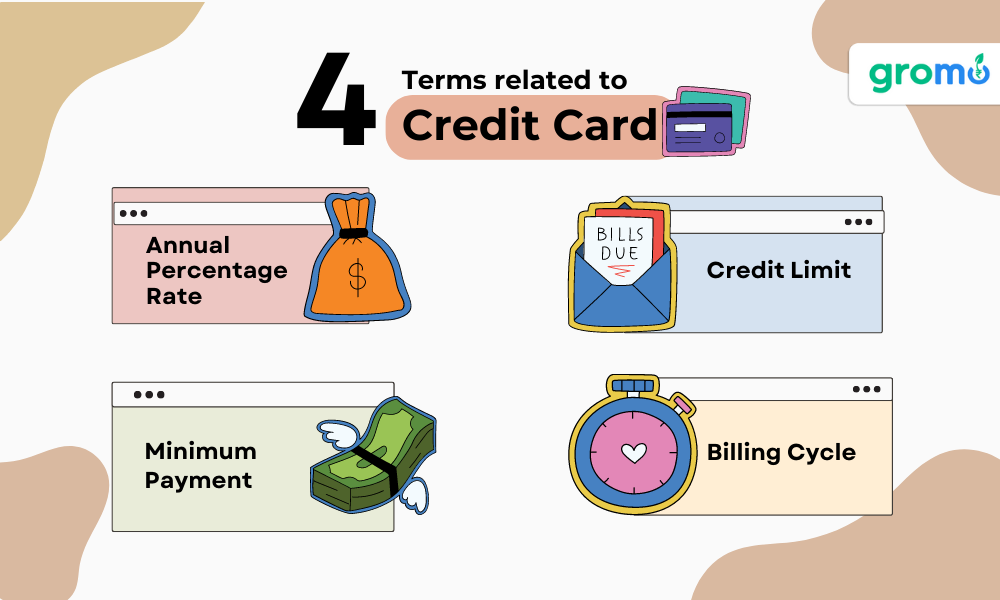

2. Credit Limit

The credit limit refers to the maximum amount of money that a cardholder can borrow on their credit card. It is determined by the credit card issuer based on factors such as the individual's creditworthiness, income, and financial history.

Looking for an app for earning online? GroMo is your answer! Now earn with each sale by selling various kinds of financial products

3. Minimum Payment

The minimum payment is the minimum amount that a cardholder is required to pay each month to maintain their credit card account in good standing. It is usually a small percentage of the outstanding balance or a fixed amount, whichever is higher.

4. Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) is the annualized interest rate charged on credit card balances that are not paid in full by the due date. It represents the cost of borrowing and is expressed as a percentage. Understanding the APR is crucial in managing credit card debt and comparing different credit card offers.

5. Billing Cycle

The billing cycle is the period of time between two consecutive credit card statements. It typically ranges from 25 to 31 days. During this period, all transactions made on the credit card are recorded, and at the end of the billing cycle, a statement is generated.

CHECK OUT!

- Benefits Of Demat Account: 5 Benefits That You Should Know

- Benefits Of Demat Account: 5 Benefits That You Should Know

- Life Insurance Terms And Definitions: Exhaustive List

- Top Providers Of Investment Insurance: 10 Providers List

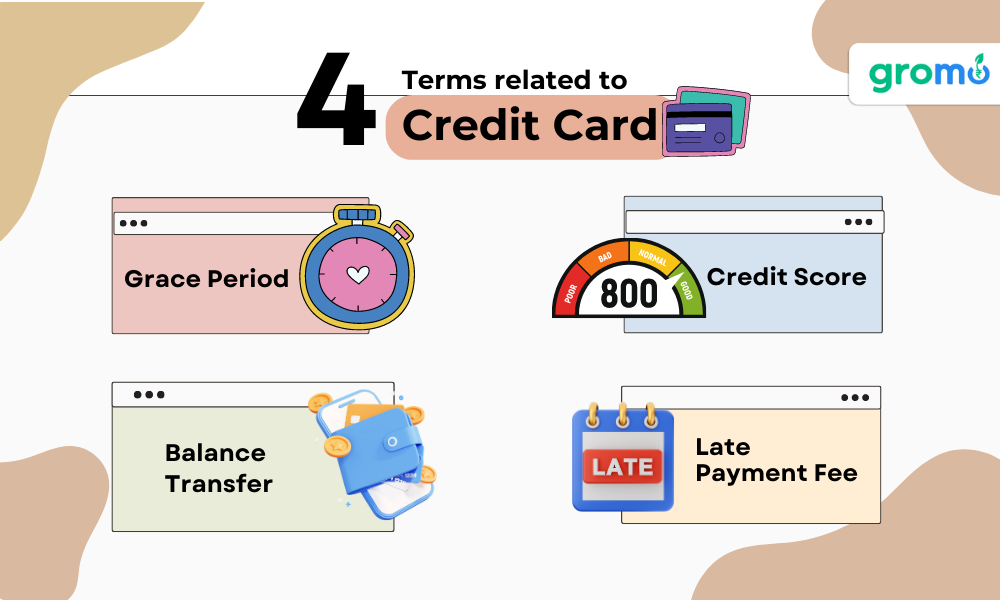

6. Grace Period

The grace period is the period between the end of a billing cycle and the due date of the payment. If the cardholder pays the outstanding balance in full within this period, no interest charges will be applied. Grace periods usually range from 21 to 25 days.

7. Cash Advance

A cash advance is a feature offered by credit cards that allows cardholders to withdraw cash from an ATM or through other means. However, cash advances often come with higher interest rates and additional fees compared to regular purchases.

8. Credit Score

A credit score is a numerical representation of an individual's creditworthiness. It is based on factors such as payment history, credit utilization, length of credit history, and types of credit accounts. A higher credit score indicates a lower credit risk and can lead to better credit card offers and terms.

9. Balance Transfer

A balance transfer is the process of moving an existing credit card balance to another credit card, often with a lower interest rate or promotional offer. This can help individuals consolidate their debt and save on interest charges.

10. Late Payment Fee

A late payment fee is a fee charged to the cardholder if they fail to make the minimum payment or pay the credit card bill after the due date. It is important to make payments on time to avoid incurring these fees and potential negative impacts on credit scores.

These are just some of the key terms and definitions related to credit cards. Familiarizing yourself with these terms will empower you to make informed decisions, effectively manage your credit card usage, and maximize the benefits that credit cards can offer. Remember to always read the terms and conditions of your credit card agreement and seek professional advice if needed.

11. Credit Utilization Ratio

Credit utilization ratio is the percentage of the credit limit that a cardholder has used. It is calculated by dividing the outstanding balance by the credit limit. Maintaining a low credit utilization ratio is generally favorable for your credit score.

12. Rewards Program

A rewards program is a feature offered by many credit cards that allows cardholders to earn points, cashback, or other rewards for making purchases. These rewards can be redeemed for various benefits such as travel, merchandise, or statement credits.

13. Introductory Offer

An introductory offer is a promotional feature offered by credit card issuers to attract new cardholders. It may include benefits such as a low or 0% APR for a specific period, waived annual fees, or bonus rewards. Understanding the terms and duration of the introductory offer is important to make the most of these benefits.

14. Foreign Transaction Fee

A foreign transaction fee is a charge imposed by credit card issuers for purchases made in a foreign currency or from a merchant located outside the cardholder's home country. It is usually a percentage of the transaction amount and can add up significantly for frequent international travelers.

15. Fraud Protection

Fraud protection is a security feature provided by credit card issuers to safeguard cardholders against unauthorized or fraudulent transactions. It may include monitoring systems, alerts, and liability protection in case of fraudulent activity on the card.

16. Secured Credit Card

A secured credit card is a type of credit card that requires a security deposit as collateral. It is typically offered to individuals with limited credit history or poor credit scores. The security deposit acts as a guarantee for the credit line and can be refunded upon closing the account.

17. Contactless Payments

Contactless payments are a convenient and secure way to make transactions using a credit card or other payment methods without physically swiping or inserting the card. It involves tapping the card on a contactless-enabled terminal to complete the payment.

18. Credit Card Insurance

Credit card insurance is an optional feature that provides coverage against specific risks such as fraud, identity theft, or loss of employment. It offers financial protection and peace of mind to cardholders in case of unforeseen circumstances.

19. Co-branded Credit Card

A co-branded credit card is a credit card that is issued in partnership between a credit card issuer and a specific brand or organization. It offers cardholders specialized benefits, rewards, or discounts associated with that brand or organization.

20. Credit Card Statement

A credit card statement is a monthly summary of all transactions, payments, and charges on a credit card account. It includes details such as the transaction date, merchant name, amount spent, and any fees or interest charged. Reviewing the credit card statement is crucial for tracking expenses and detecting any errors or fraudulent activity.

Understanding these additional terms and definitions related to credit cards will further enhance your knowledge and enable you to navigate the world of credit cards with confidence. Remember to always read and understand the terms and conditions of your specific credit card agreement to make informed financial decisions.

21. Minimum Payment

The minimum payment is the minimum amount that a cardholder must pay by the due date to keep the credit card account in good standing. It is typically a small percentage of the outstanding balance, often with a minimum dollar amount. However, paying only the minimum payment can result in accruing interest and prolonging the repayment period.

22. Balance Transfer

A balance transfer is the process of moving the outstanding balance from one credit card to another, usually with a lower interest rate or promotional offer. This can help cardholders consolidate their debt or take advantage of lower interest rates to save on finance charges.

23. Authorized User

An authorized user is an individual who is given permission by the primary cardholder to use their credit card. The authorized user can make purchases and share the benefits of the card but is not legally responsible for the card's debt. The primary cardholder remains responsible for all charges and payments.

24. Grace Period

The grace period is the timeframe during which a cardholder can pay the outstanding balance in full without incurring any interest charges. It typically ranges from 21 to 25 days from the billing cycle's closing date. By paying the balance in full within the grace period, cardholders can avoid interest on new purchases.

25. Credit Limit Increase

A credit limit increase is the approval by the credit card issuer to raise the maximum amount that a cardholder can borrow on their credit card. It allows cardholders to have access to more available credit, which can positively impact their credit utilization ratio and provide greater financial flexibility.

26. Pre-approval

Pre-approval is the initial evaluation process conducted by credit card issuers to assess an individual's creditworthiness before extending a credit card offer. It involves a soft inquiry on the credit report and provides an indication of the likelihood of being approved for a particular credit card.

27. Credit Bureau

A credit bureau, also known as a credit reporting agency, is a company that collects and maintains credit information on individuals. The credit bureau compiles credit reports, which include credit history, payment patterns, and other financial information. Lenders and credit card issuers use these reports to assess creditworthiness.

28. Credit Freeze

A credit freeze, also known as a security freeze, is a measure taken by individuals to restrict access to their credit report. It prevents new credit accounts from being opened in their name without their explicit authorization. A credit freeze can help protect against identity theft and fraudulent credit applications.

29. EMV Chip

An EMV chip is a small microchip embedded in credit cards that enhances security during transactions. It generates a unique code for each transaction, making it difficult for fraudsters to clone or counterfeit the card. EMV chip cards offer greater protection against fraudulent activity compared to traditional magnetic stripe cards.

30. Digital Wallet

A digital wallet is a virtual wallet that allows users to securely store payment information and make contactless payments using their smartphones, smartwatches, or other digital devices. Digital wallets offer convenience and enhanced security by replacing the need to carry physical credit cards.

By familiarizing yourself with these additional terms and definitions related to credit cards, you can expand your knowledge and make more informed decisions when managing your credit card accounts. Remember to always review the specific terms and conditions of your credit card agreements to fully understand the features and benefits they offer.

To sell this product, and many other financial products. DOWNLOAD GROMO. Where you can sell and earn a substantial income sitting at home

Importance of Credit Cards

Credit cards offer several key benefits and play a crucial role in personal finance. Here are some reasons why credit cards are important:

Convenience: Credit cards provide a convenient and widely accepted mode of payment, both online and offline.

Financial Flexibility: Credit cards allow individuals to make purchases even when they don't have immediate cash available.

Emergency Fund: Credit cards can serve as a backup during emergencies or unexpected expenses.

Building Credit History: Responsible credit card usage can help individuals build a positive credit history, which is important for future financial endeavors.

Rewards and Perks: Many credit cards offer rewards programs, cashback, travel perks, and other benefits to cardholders.

Different Types of Credit Cards

Credit cards come in various types, each catering to different needs and preferences. Some common types of credit cards include:

Standard Credit Cards

These are basic credit cards that offer a line of credit for general use.

Rewards Credit Cards

Rewards credit cards provide various incentives for spending, such as cashback, points, or airline miles.

Secured Credit Cards

Secured credit cards require a security deposit and are typically targeted towards individuals with limited or poor credit history.

Business Credit Cards

Business credit cards are designed specifically for business expenses and often offer features tailored to business needs.

Student Credit Cards

Student credit cards are designed for students with limited credit history and often come with lower credit limits.

CHECK OUT NOW!

- Savings Account Terms And Definitions: Exhaustive List

- Investment Products Terms And Definitions: Exhaustive List

- Motor Insurance Terms And Definitions: Exhaustive List

- Top Providers Of Vehicle Loans: 5 Providers In India

KEY TAKEAWAYS

-

Credit cards offer convenient access to credit and provide a flexible payment option for purchases, allowing cardholders to make transactions without carrying physical cash.

-

Understanding credit card terms and definitions is crucial to managing your credit effectively and avoiding unnecessary fees or penalties. Familiarize yourself with concepts like APR, credit limit, grace period, and billing cycle to make informed decisions.

-

Credit card benefits, such as rewards programs, cashback offers, and purchase protection, can provide additional value and perks for cardholders. Take advantage of these features to maximize the benefits of your credit card.

-

Responsible credit card usage involves making timely payments, keeping credit utilization low, and monitoring your credit card statements for any suspicious activity. This helps maintain a good credit score and financial well-being.

-

It's essential to read and understand your credit card agreement to know the terms, fees, and conditions associated with your card. This knowledge empowers you to make smart financial choices and use your credit card responsibly.