Health Insurance Terms & Definitions: Exhaustive List

Terms And Definitions of Health Insurance Actuarial value: A measure of how much of the cost of covered health care services a health insurance plan covers

"It is not good not to have health insurance; that leaves the family very vulnerable."

— Elizabeth Warren

Health insurance plays a vital role in safeguarding individuals and families from the financial burden associated with medical expenses. It provides access to quality healthcare services and protects against unexpected medical emergencies. So, are you familiar with the terms related to health insurance?

Do you know what does actuarial value, catastrophe plan, durable medical equipment coverage, and exclusive provider organisation mean when it comes to health insurance?

We understand as well as anyone else that the health insurance language can be difficult to comprehend. Despite this, it’s becoming increasingly important that health care consumers have a basic understanding of the language used in the industry.

That is why, this guide aims to provide a comprehensive overview of health insurance, its importance, terms and definitions of health insurance, its types, and much more!

All to help you buy the best health insurance for yourself.

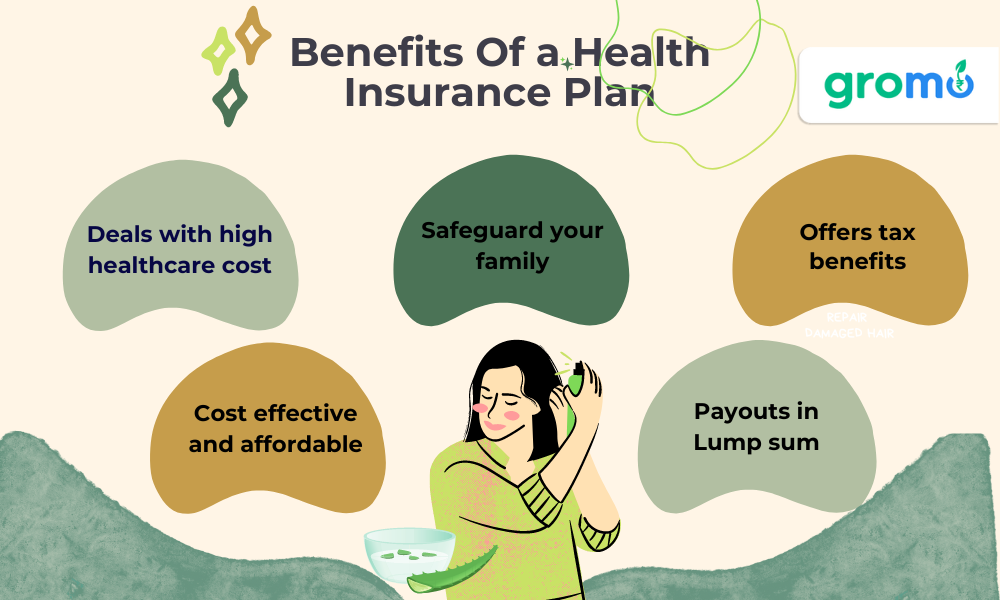

Importance Of Health Insurance

Life without knowing what's going to happen next is scary. There’s nothing worse than the thought of your loved ones going through a medical emergency. That's where health insurace plays an important role.

Health insurance offers numerous advantages, including financial protection, access to a wide range of medical services, preventive care, and peace of mind. It acts as a safety net, ensuring that individuals can receive necessary medical treatments without facing exorbitant costs.

Let’s take a closer look at some of the factors that make medical insurance even more important.

1. Cope With A Shift In Lifestyle

It’s no shock that more people are getting sick younger because of lifestyle changes. Now more than ever, medical insurance is essential. You may not be aware of it, but we are becoming more and more exposed to health hazards as a result of our lifestyle.

While it’s important to take preventative steps, it’s also important to understand how important health insurance is for you.

2. Protect Your Loved Ones

When you’re searching for a good health insurance plan, your family’s needs come first. The cost of providing healthcare for multiple people on a single income stream is unfathomable. For instance, if your parents are getting older, they're more susceptible to illnesses and need better care.

You need to figure out how much health insurance you need early in your life to be prepared and have enough financial backing.

3. Medical Expenses Are On The Rise

The cost of high-quality care has skyrocketed in recent years. Health insurance plays an important role in managing medical inflation. You can manage them efficiently if you know why health insurance is so important at the right moment.

4. Protect Your Savings

If you don’t have the money to cover the costs of your medical expenses, it will significantly increase your debt. This makes health insurance even more important because it protects your money and helps you recover financially.

You can keep the savings and use it for other things like purchasing a house, paying for your kid's college, and so on.

Terms And Definitions of Health Insurance

Below are just a few of the many terms that you may encounter when you are shopping for health insurance. It is important to understand these terms so that you can make an informed decision about your coverage.

1. Actuarial Value: A measure of how much of the cost of covered health care services a health insurance plan covers.

2. Adverse Selection: The tendency for people who are more likely to use health care services to be more likely to purchase health insurance.

3. Annual Deductible: The amount of money that you must pay out of pocket for covered health care services before your health insurance plan begins to pay.

4. Annual Out-Of-Pocket Maximum: The maximum amount of money that you must pay out of pocket for covered health care services in a year.

5. Benefits: All the health care services that are covered by your health insurance plan.

6. Catastrophe Plan (CAT): A type of health insurance plan that has lower premiums than traditional health insurance plans, but that also has higher deductibles and out-of-pocket maximums.

7. Coinsurance: A percentage of the cost of covered health care services that you must pay after you have met your annual deductible.

8. Copayment: A fixed amount of money that you must pay for covered health care services, regardless of the cost of the service.

To sell this product, and many other financial products. DOWNLOAD GROMO. Where you can sell and earn a substantial income sitting at home

DOWNLOAD GROMO

9. Cost Sharing: The portion of the cost of covered health care services that you must pay, either in the form of copayments, coinsurance, or deductibles.

10. Coordination Of Benefits: Benefits coordination is how insurance companies decide how to pay your medical bills when you have multiple health insurance plans.

11. Durable Medical Equipment Coverage (DME): Coverage for medical equipment that is used for more than a short period of time, such as a wheelchair or a walker.

12. Exclusive Provider Organisation (EPO): A type of health insurance plan that covers a limited network of doctors and hospitals.

13. Exclusion: A health care service that is not covered by your health insurance plan.

14. Family Floater Health Insurance: A family floater health insurance policies cover all members of your legal family on a sum nsured basis.

15. Group Health Insurance: Health insurance that is offered by employers to their employees.

16. Health Insurance: A type of insurance that helps to pay for the cost of health care services.

17. Health Savings Account (HSA): A tax-advantaged savings account that can be used to pay for qualified medical expenses.

18. High-Deductible Health Plan (HDHP): A type of health insurance plan that has a high annual deductible, but that also has lower premiums than traditional health insurance plans.

19. In-Network: A doctor or hospital that is part of your health insurance plan's network.

20. Open Enrollment: A specific period during which individuals can enroll, renew, or make changes to their health insurance plans.

21. Out-Of-Network: A doctor or hospital that is not part of your health insurance plan's network.

22. Outpatient Department Coverage: A coverage that pays for outpatient medical care including doctor consultations, diagnostic tests, rehabilitation, etc.

23. Preauthorization: The pre-approval stage is more akin to a provisional approval, meaning the insurer only informs the hospital if the claim is accepted or rejected.

24. Premium: The monthly cost of health insurance.

25. Prescription Drug Coverage: A type of health insurance coverage that helps to pay for the cost of prescription drugs.

26. Preferred Provider Organization (PPO): A type of health insurance plan that allows you to see doctors and hospitals in and out of network.

27. Preventive Care Coverage: Coverage for health care services that are designed to prevent illness or disease, such as annual physicals and vaccinations.

28. Removal Of Exclusions And Limitations: A provision in some health insurance plans that helps to ensure that you will not be denied coverage for a pre-existing condition.

29. Self-funded Health Insurance: Health insurance that is purchased by an employer or individual directly from an insurance company.

30. Special Enrollment Periods (SEPs): Limited-time periods allowing individuals to enroll or make changes outside of the regular open enrollment period due to specific life events like marriage, job loss, or the birth of a child.

31. Waiting Period: A period of time during which you must wait before your health insurance plan begins to pay for covered health care services.

CHECK OUT NOW!

- Term Life Insurance Definitions: Related Terms Explained

- Top Providers Of Investment Insurance: 10 Providers List

- Investment Products Definitions: Related Terms Explained

- Instant Loans Definitions: Exploring Its Related Terms

Types Of Health Insurance Plans

1. Group Health Insurance Plan

Coverage provided by employers to their employees and sometimes their families. The most popular kind of group insurance is the Group Medical Cover (GMC). You may not have to wait at all to receive the benefits of the policy. It may include maternity care, daycare and the Out-patient department.

It may provide additional benefits, including annual health assessments, online doctor visits, and diagnostic tests.

2. Individual Health Insurance Plan

An Individual Health Insurance Policy provides coverage on a case-by-case basis. The Individual Health Insurance Policy (IHIP) provides coverage for a single. It provides coverage for hospitalisation costs for injuries/illness, operations, daycare care, room costs, etc.

3. Family Floater Health Insurance Plan

It is the coverage purchased directly by families from insurance companies. Family Floater health plans are family health plans for the whole family. The insured amount is the same for all plan beneficiaries. It is one health insurance plan that covers the whole family.

This plan provides financial protection against hospitalisations, operations, treatments, and daycares.

4. Government-Sponsored Plans

As the name implies, a government health insurance plan is a medical insurance plan sponsored and/or funded by the government at all levels, including the central and state levels.

One of the ways the state can improve the health and wellbeing of its citizens is by building strong public health systems and working with the private sector to set up health insurance plans, such as Ayushman Bharat and Awaz Health Insurance Scheme.

5. Senior Citizen Health Insurance Plan

If you want to buy a health insurance plan for your parents or other senior citizens, you should opt for this plan. Senior Citizen Health Insurance is designed for people over the age of 65.

The premium may also be higher than that of an Individual or Family Floater Health Insurance Plan, as older people are more likely to experience health problems.

6. Critical Illness Insurance Plan

The Critical Illness Plan is intended to protect you financially in the event of a diagnosis of a critical disease or condition. If you file a claim against your policy, the insurer will pay you a lump sum. You should have a minimum of 30 days to live after being diagnosed with a critical illness.

The policy ends when the insured amount is paid out as a single lump sum.

7. Top-up Health Insurance Plan

A Top-up health Insurance Plan is perfect if you want coverage that covers the amount you’re insured up to, or up to, a certain limit. Once you have used the maximum claim amount, the plan is activated. Most plans may require you to pay a fixed deductible amount.

8. Personal Accident Insurance Policy

Medical bills resulting from injuries from an accident can wreak havoc on your finances. Personal Accident Insurance Policies provide coverage for accidental death, accidental injury, and permanent/partial disability. It also provides one-off payments in the event of death or permanent disability.

9. Maternity Health Insurance Plan

In addition to the basic plan, you can also choose to add on the Maternity Health Insurance Plan. If you are thinking about starting a family, this is the plan for you. The Maternity Health Insurance Plan provides coverage for pre and post-partum health care, as well as the baby's delivery.

Some of these plans may provide coverage for the newborn for a certain period of time.

10. Mediclaim Insurance Plan

If you want health insurance that only covers in-patient costs, you can look into Mediclaim Insurance. This type of plan is typically available in the form of group medical insurance, individual medical insurance, and overseas medical insurance.

11. Disease Specific Health Insurance Plans Such As Corona Kavach

Disease Specific Health Insurance Plans provide one time premium payment. There are no deductibles involved and they offers daily hospital cash. They also come with AYUSH treatment.

12. Hospital Daily Cash

Hospital Daily Cash is an insurance policy that provides you with a fixed cash benefit for every day of your hospital stay due to illness or injury. This cash benefit is paid to you regardless of any medical expenses incurred during your hospital stay.

13. ULIPs

ULIP stands for Unit Linked Insurance Plan. It’s a combination of insurance and investment products. In a ULIP, part of the policyholder’s premium is used to pay for life insurance coverage, while the rest is invested in different market-based instruments, such as stocks, bonds, or a mix of both.

Key Considerations For Choosing Health Insurance

1. Coverage: Evaluate the extent of coverage for services like hospitalization, prescription drugs, maternity care, and preventive care.

2. Network: Assess the network of healthcare providers and hospitals included in the plan to ensure access to preferred doctors or specialists.

3. Costs: Compare premiums, deductibles, copayments, and coinsurance to determine the most cost-effective plan.

4. Prescription Drug Coverage: Evaluate the formulary and coverage for medications required on a regular basis.

5. Additional Benefits: Look for additional benefits such as telemedicine, wellness programs, and preventive care services.

CHECK OUT!

- Motor Insurance Terms And Definitions: Exhaustive List

- Term Life Insurance Definitions: Exhaustive List

- Investment Insurance Definitions: Related Terms Explained

- Top Providers Of Vehicle Loans: 5 Providers In India

Looking for an app for earning online? GroMo is your answer! Now earn with each sale by selling various kinds of financial products

Tips For Utilizing Health Insurance Effectively

1. Familiarize Yourself with Policy Details: Understand the coverage, network, and benefits offered by your health insurance plan.

2. Regularly Review Your Plan: Assess your needs and determine if your current plan meets your requirements.

3. Maintain A Healthy Lifestyle: Preventive care and healthy habits can help reduce healthcare costs in the long run.

Key Takeaways

- Health insurance is essential for financial protection against unexpected medical expenses.

- There are various types of health insurance plans available, including employer-sponsored plans, individual and family plans, etc.

- When selecting a health insurance plan, consider factors such as coverage, network of healthcare providers, costs, etc.

- Open enrollment is a designated period during which individuals can enroll, renew, or make changes to their health insurance plans.

- To make the most of your health insurance, familiarize yourself with the policy details, including terms like preauthorization, in-network, etc.