Zero-Investment Income Tamil Nadu 2026: Earn ₹15K-₹50K Monthly

Tamil Nadu in 2026 has zero-investment opportunities that can generate ₹15,000 to ₹50,000 monthly through digital financial product distribution. While traditional businesses like textiles and agriculture still dominate, commission-based models now let anyone with a smartphone earn without needing capital, inventory, or a physical shop.

The state's digital literacy rate sits at 79.8% with strong internet penetration. Tamil Nadu ranks third nationally in startup ecosystems, yet most profitable ventures still require substantial upfront capital. Financial product distribution bypasses this entirely you just need a phone and some persistence.

Why Tamil Nadu works for zero-investment businesses

Tamil Nadu has 3.8 crore smartphone users. That's an enormous market for digital financial services. Chennai, Coimbatore, Madurai, and Tiruchirappalli have growing middle-class populations who need credit cards, loans, savings accounts, and investment products.

The manufacturing and service sectors employ millions who need personal loans and credit lines. MSMEs across textile hubs, automobile clusters, and food processing units need business loans. This demand creates real opportunities for financial product distributors who can connect customers with banking partners.

Trust matters in Tamil culture. Personal recommendations carry weight. When you share financial products with your network, people actually listen. This social capital converts into commission income without requiring storefronts or inventory.

GroMo's platform has enabled 12,000+ partners across Tamil Nadu to earn through financial distribution. The model works in tier-1 cities and tier-3 towns alike.

The business model

Financial product distribution through GroMo requires zero capital. Commission payouts range from ₹250 to ₹5,000 per successful application. Partners share digital links for credit cards, savings accounts, demat accounts, loans, and credit lines with their networks.

You earn only when a customer completes an application and gets approved. No inventory. No customer service burden. No payment collection. GroMo handles compliance, documentation, and fund disbursement.

Tamil Nadu partners typically earn through four revenue streams:

Credit card distribution generates ₹600 to ₹2,400 per approved card. Premium cards from IDFC FIRST, Kotak Mahindra, and AU Small Finance Bank pay higher. A partner sharing 10 credit card links monthly with 30% conversion earns ₹7,200 to ₹21,600 monthly.

Personal and business loan distribution pays 1.5% to 5.5% of sanctioned amounts. A partner facilitating two ₹2 lakh personal loans monthly earns ₹6,000 to ₹22,000 in commissions.

Savings and demat accounts provide ₹250 to ₹700 per account opened and funded. Tide Business Accounts pay up to ₹700 when customers complete activation. Upstox and AngelOne demat accounts reward first trades with ₹250-₹400 payouts.

Credit line products like BharatPe Credit Line or Bajaj Insta EMI generate ₹800 to ₹1,500 per customer, with potential for repeat transactions.

Tamil Nadu's diverse economy means you can target different segments. Salaried professionals in IT hubs need credit cards and investment accounts. Small business owners in textile towns need business loans. Young professionals want their first savings accounts.

How to start in Tamil Nadu

Download the GroMo app from Google Play Store or Apple App Store. Registration takes about three minutes. Enter your mobile number, verify with OTP, complete basic KYC with PAN and Aadhaar, and you're ready.

The app has a Tamil language interface. Product catalogs show commission structures clearly. You see exactly what you'll earn before sharing any link.

Week 1: Complete the free training

GroMo Academy offers certification courses covering all financial products. Learn credit card features, loan eligibility criteria, account opening processes, and compliance requirements. These courses prevent misselling and improve conversion rates.

Focus on 2-3 products initially. Master their features, benefits, and ideal customer profiles. Understanding products deeply lets you answer customer questions confidently.

Week 2-3: Build your target list

Identify 50-100 contacts who might need financial products. Segment them by need. Salaried employees for credit cards and personal loans. Business owners for business accounts and loans. Young professionals for savings and demat accounts.

Share products through WhatsApp, SMS, or direct conversations. Personalize your message. Generic broadcasts convert poorly compared to targeted recommendations.

Week 4 onward: Scale and optimize

Track which products generate highest conversions in your network. Double down on those. If credit cards work well, focus there. If your contacts are business owners, prioritize business loans.

Build teams through GroMo's referral program. When you onboard new partners, you earn a percentage of their commissions. This creates passive income alongside direct sales.

Partners in Coimbatore manufacturing clusters focus on business loans for SMEs. Chennai IT professionals emphasize credit cards and investment accounts. Madurai partners target retail shop owners with business accounts and credit lines. Adapt to your local market.

Top products for Tamil Nadu in 2026

IDFC FIRST WOW Credit Card offers 1.5% unlimited cashback on all spends, which appeals to Tamil Nadu's value-conscious consumers. Zero annual fees and instant approval make it easy to recommend. Partner payout ranges from ₹700 to ₹1,500 per approved card.

Customers need only PAN, Aadhaar, and basic income proof. The fully digital process completes in 15 minutes. Cards reach customers within 7 days. High approval rates for salaried employees with ₹25,000+ monthly income make this a reliable conversion product.

Tide Business Account serves Tamil Nadu's 8.5 lakh MSMEs well. The digital business current account offers 1.5% real cashback on all business spends, prepaid expense cards, and automated bookkeeping features.

The referral code TBA123 enables partners to earn ₹440 to ₹700 per activated account. Customers fund accounts with just ₹50 and complete a utility bill payment for full payout eligibility. No minimum balance requirement.

Upstox Demat Account captures Tamil Nadu's growing investor base. The state has 1.2 crore demat accounts as of 2026, up 35% from 2024. Young professionals seeking to build wealth through stocks and mutual funds drive this growth.

Upstox charges zero account opening fees, zero AMC for the first year, and zero commission on mutual funds and IPOs. Partners earn ₹250 to ₹400 per account when customers complete their first non-intraday trade. The paperless process and user-friendly interface help conversion rates.

Poonawalla Fincorp Business Loan offers unsecured loans up to ₹50 lakhs for self-employed individuals and SMEs. Tamil Nadu's manufacturing sector creates constant demand for working capital and expansion funds.

The product requires minimal documentation: GST/Udyam registration, 7-month bank statements, and owned house proof. Interest rates start at 15% annually with 6-60 month tenures. Partners earn 1.75% to 3% of sanctioned amounts.

AU Small Finance Credit Card targets customers building or repairing credit scores. Tamil Nadu has significant underbanked and new-to-credit populations who struggle with traditional bank rejections.

AU's liberal approval norms and secured card options create opportunities in tier-2 and tier-3 towns. Partner payouts range from ₹600 to ₹1,200 per card.

Success stories from Tamil Nadu partners

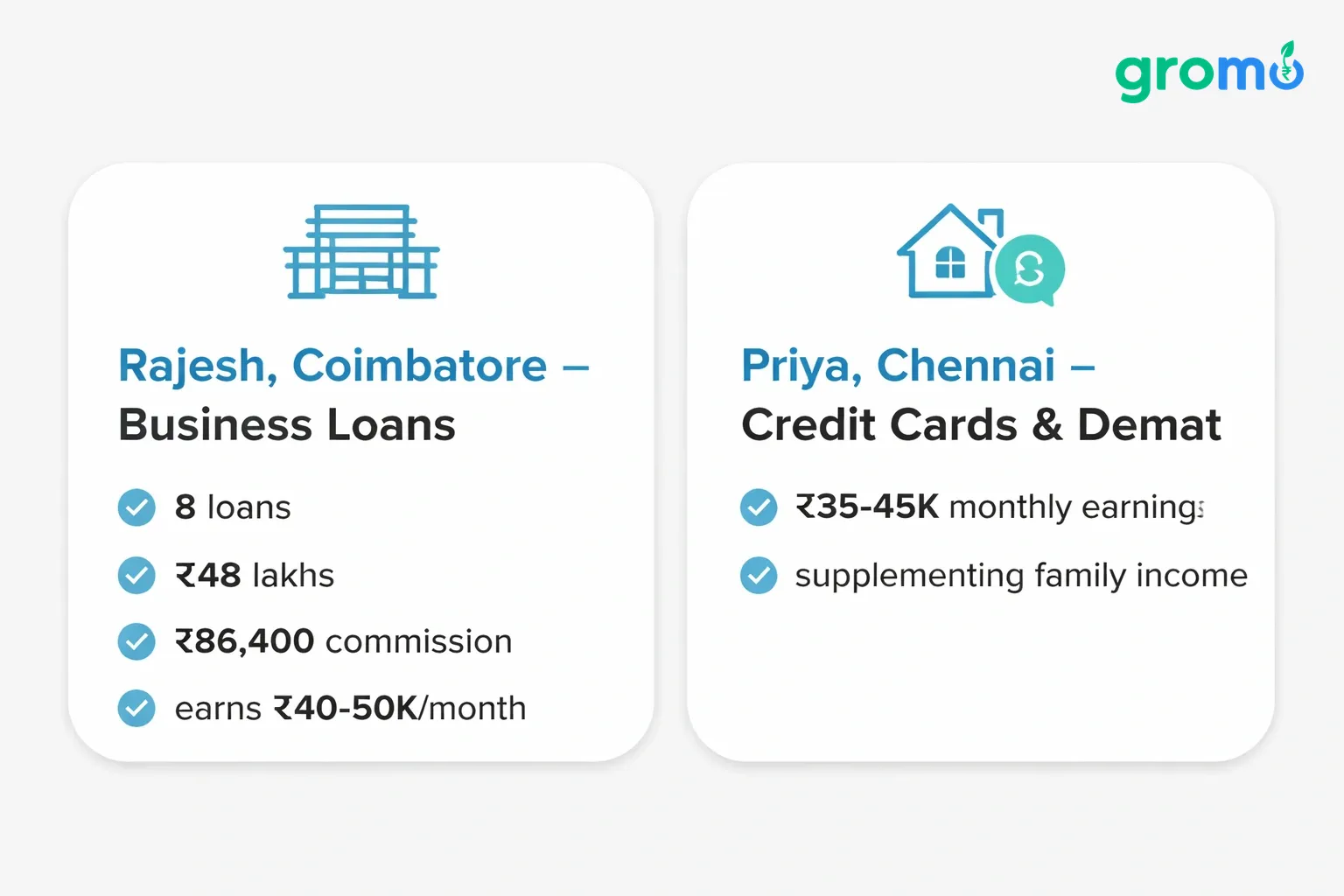

Rajesh from Coimbatore, a textile unit supervisor, started with GroMo in January 2026. He focused on business loans for small manufacturers in his network. By March, he facilitated 8 business loans totaling ₹48 lakhs, earning ₹86,400 in commissions. He now earns ₹40,000-₹50,000 monthly working evenings and weekends.

Priya from Chennai, a homemaker with IT industry connections, specializes in credit cards and demat accounts. She shares products through WhatsApp groups and personal recommendation. Her monthly earnings range from ₹35,000 to ₹45,000, supplementing her family's income without leaving home.

Kumar from Madurai runs a mobile recharge shop. He added financial product distribution to his existing customer interactions. When customers visit for recharges, he assesses their needs and recommends relevant products. This added ₹25,000-₹30,000 to his monthly income without additional time investment.

Lakshmi from Tiruchirappalli, a college student, uses GroMo to earn during her studies. She targets fellow students for savings accounts and young professionals for credit cards. Her flexible schedule allows 2-3 hours daily effort, generating ₹15,000-₹20,000 monthly pocket money.

These partners share common traits: consistency, product knowledge, and targeted customer selection. They don't spam links randomly but identify genuine needs and match appropriate products. This consultative approach builds trust and generates repeat referrals.

How Tamil Nadu partners maximize earnings

Leverage local networks. Tamil culture's strong community bonds create natural distribution channels. Wedding planners connect with couples needing personal loans. Chartered accountants refer business clients for business accounts and loans. Real estate agents introduce home loan seekers to personal loan alternatives.

What professional or personal connections do you have? How can those relationships translate into financial product conversations?

Focus on high-ticket products. Business loans and premium credit cards generate larger commissions per transaction. While savings accounts provide volume, loans create substantial single payouts. Partners earning ₹50,000+ monthly typically focus on 2-3 high-payout products rather than spreading efforts across everything.

Build expert positioning. Create simple educational content about financial products. Short videos in Tamil explaining credit score importance, loan eligibility factors, or investment account benefits establish you as a knowledgeable advisor. This content generates inbound inquiries, reducing your outreach effort.

Share success stories (with permission) showing how your recommendations helped customers. Social proof converts skeptical prospects into applicants.

Use multi-channel outreach. WhatsApp dominates in Tamil Nadu, but don't ignore Facebook groups, local community forums, and offline conversations. Different demographics prefer different channels. Older business owners respond better to phone calls. Younger professionals engage through social media.

Test various approaches and double down on what works for your target segment.

Maintain follow-up discipline. Many applications stall at documentation or verification stages. Partners who follow up proactively see 40-50% higher approval rates. This diligence directly impacts earnings.

GroMo's app tracks customer journey stages. Set daily reminders to check pending applications and nudge customers toward completion.

Common mistakes to avoid

Promising guaranteed approvals. Financial product approvals depend on bank policies and customer eligibility. Never promise certainties. Position yourself as a facilitator who maximizes approval chances by ensuring proper documentation and accurate information.

Misselling or false promises damage your reputation and violate compliance norms. GroMo tracks customer complaints, and repeated violations result in account suspension.

Ignoring compliance training. Each product has specific eligibility criteria and documentation requirements. Skipping training leads to application rejections, wasting your time and frustrating customers. Invest 2-3 hours in GroMo Academy courses before actively promoting products.

Understanding ineligibility factors prevents sharing products with wrong customer profiles. For instance, BharatPe Credit Line requires Aadhaar-linked mobile numbers. Sharing with customers lacking this causes immediate rejection.

Chasing only family and friends. Your immediate network has limits. Successful partners expand beyond personal contacts through content marketing, community engagement, and professional networking. Treat this as a real business requiring customer acquisition strategies.

Join local business associations, professional groups, and community organizations. Offer genuine value before pitching products. Help first, sell second.

Neglecting customer service. While GroMo handles backend operations, your reputation depends on customer experience. Guide applicants through processes, answer questions promptly, and follow up post-approval. Satisfied customers refer others, creating organic growth.

Unhappy customers spread negative word-of-mouth that undermines future conversions. Prioritize customer success even after earning your commission.

Comparing with traditional businesses. This isn't a traditional business requiring premises, staff, or inventory. It's a commission-based distribution model. Success metrics differ. Focus on conversion rates, customer satisfaction, and monthly payout trends rather than traditional business metrics.

How this compares to traditional Tamil Nadu businesses

Traditional profitable businesses in Tamil Nadu textile retail, restaurants, manufacturing units require ₹5 lakhs to ₹50 lakhs initial investment. They involve lease agreements, inventory purchasing, staff hiring, and regulatory compliance. Break-even takes 18-36 months. Failure risks significant capital loss.

Financial product distribution through GroMo requires zero investment. You start immediately without loans, guarantees, or savings depletion. Failure costs nothing beyond time invested. Success generates monthly cash flow from day one.

Traditional businesses demand 10-14 hour daily commitments. You cannot scale beyond physical capacity without hiring staff. Financial distribution scales through digital sharing. Send 10 links or 100, the effort remains similar. Teams multiply earning potential without proportional time investment.

Geographic limitations don't apply. A retail shop serves customers within 5-10 km radius. GroMo partners serve customers across Tamil Nadu or entire India. Your childhood friend in Mumbai, college mate in Bangalore, or relative in Trichy all become potential customers.

Traditional businesses face market saturation. Every neighborhood has multiple grocery stores, restaurants, and textile shops. Financial product distribution faces minimal competition. Most people don't know this earning opportunity exists. Early movers capture market share.

The zero-investment business model changes how Tamil Nadu residents think about entrepreneurship. It makes earning opportunities accessible to students, homemakers, salaried professionals, and retirees equally.

Legal and compliance aspects

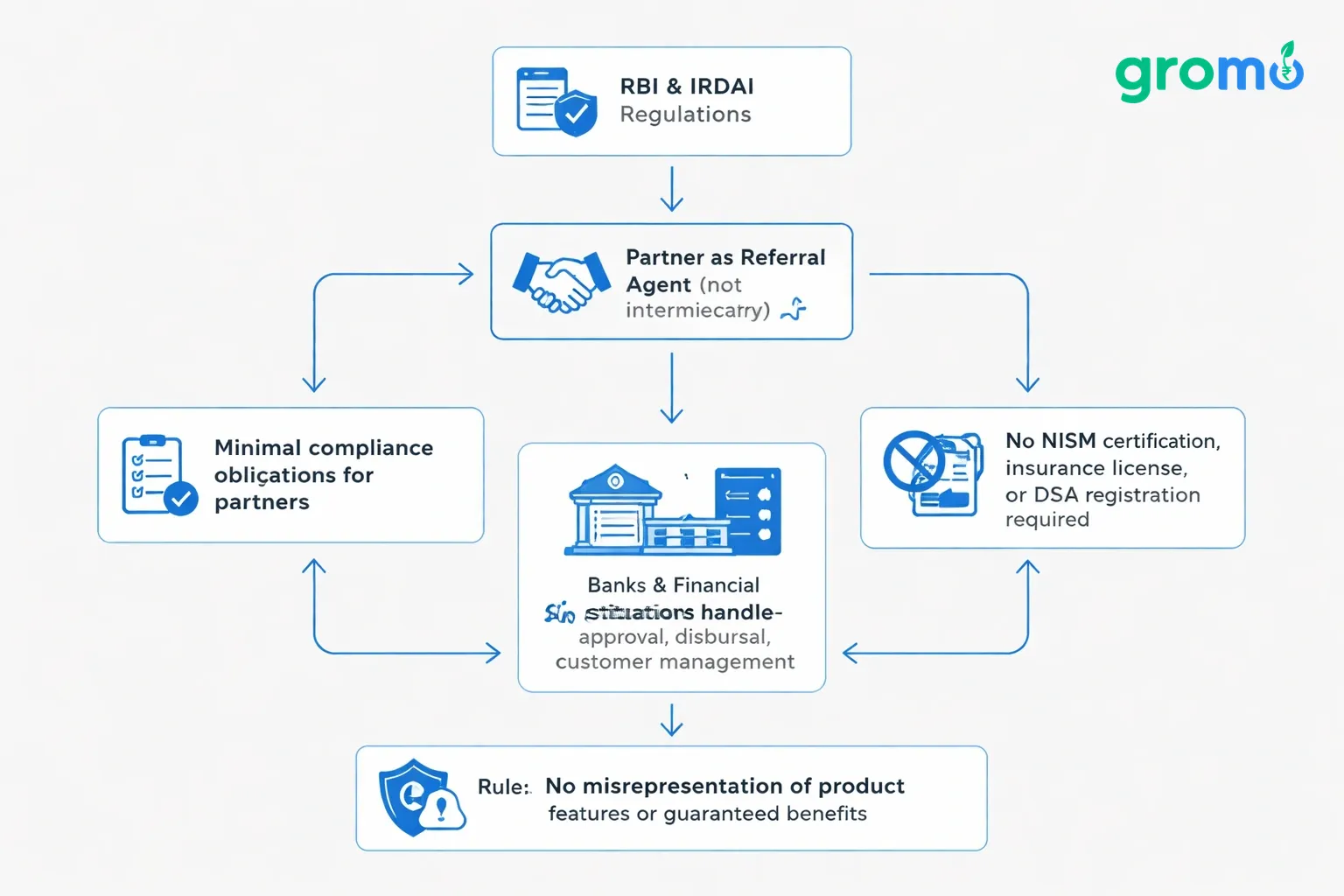

GroMo operates within RBI and IRDAI regulations governing financial product distribution. Partners act as referral agents, not intermediaries. You share product information and facilitate applications. Banks and financial institutions handle approval, disbursal, and customer management.

This structure keeps compliance obligations minimal for partners. You don't need NISM certifications, insurance licenses, or DSA registrations. However, basic rules apply:

Never misrepresent product features or guaranteed benefits. Provide accurate information based on GroMo's product details. Exaggeration or false claims violate regulations and damage the ecosystem.

Respect customer data privacy. Financial information shared during applications is confidential. Using it for unauthorized purposes or sharing with third parties breaches trust and legal norms.

Understand first-three-EMI clawback policies. For loan products, if customers default within the first three EMIs, GroMo may reverse your commission. This discourages facilitating loans for clearly ineligible or risky customers.

Never collect payment from customers for your services. GroMo pays your commissions directly. Charging customers creates liability and violates platform policies.

Tamil Nadu's strong regulatory environment and consumer protection awareness make compliance especially important. Maintain ethical practices to build sustainable long-term income rather than chasing short-term gains through questionable methods.

Combining with other income opportunities

Financial product distribution complements other zero-investment income ideas popular in Tamil Nadu. Partners combine multiple streams for enhanced earnings:

Content creation + financial distribution. Create Tamil YouTube videos about personal finance, credit scores, or loan guides. Embed GroMo product links in descriptions. Educational content builds authority and generates passive applications.

Freelancing + GroMo. Offer freelance services on platforms like Fiverr or Upwork. When building your freelance network, share financial products relevant to fellow freelancers business accounts, tax-saving investments, credit cards for expense management.

Social media influence + product sharing. If you have Instagram or Facebook followings in Tamil Nadu, integrate financial product recommendations naturally. A lifestyle influencer discussing personal finance occasionally can monetize that content through GroMo commissions.

Offline services + digital products. Run a small offline service like tuition classes, salon, or repair shop? Share relevant GroMo products with your offline customers. A tuition teacher can recommend education loans; a salon owner can suggest personal loans or credit cards.

This diversification stabilizes income. If GroMo earnings dip one month, other streams compensate. Multiple income sources reduce dependency on single platforms.

Tamil Nadu partners increasingly adopt portfolio approaches, earning from 2-3 complementary sources rather than single full-time jobs. This strategy provides both security and growth potential unmatched by traditional employment.

Tools and resources

GroMo provides marketing materials within the app: product brochures in Tamil and English, shareable graphics, video content, and automated customer tracking. These assets professionalize your outreach without design or content creation costs.

The app's customer management system tracks leads, pending applications, and completed transactions. Set reminders for follow-ups, add notes about customer conversations, and monitor conversion rates by product.

WhatsApp Business helps organize customer communications. Create broadcast lists for different segments, set automated replies for common questions, and maintain professional separation between personal and business contacts.

Google Sheets or Excel spreadsheets track your daily activities: links shared, follow-ups pending, applications approved. Weekly reviews identify which approaches yield best results.

Tamil language financial education resources blogs, videos, infographics help answer customer questions. Curate these resources into a personal knowledge base, becoming the go-to financial advisor in your network.

Local business networking groups like Lions Club, Rotary, and industry associations provide partnership opportunities. Offer to present financial literacy sessions, positioning yourself as an expert while naturally introducing your distribution services.

The GroMo blog publishes regular guides on product distribution, customer acquisition, and compliance updates. Partners who stay informed about platform changes and new product launches maintain competitive advantages.

Scaling from ₹15K to ₹50K monthly

Entry-level partners earning ₹15,000-₹20,000 monthly typically handle 30-40 customer inquiries, converting 8-10 applications. They work 1-2 hours daily, primarily within existing networks. This level requires minimal skill beyond following GroMo's training protocols.

Growing to ₹30,000-₹35,000 monthly demands expanding beyond immediate networks. Partners at this level develop content marketing strategies, join community groups, and begin building small teams. They handle 60-80 inquiries monthly, converting 15-20 applications. Time investment increases to 2-3 hours daily.

Reaching ₹50,000+ monthly requires a systematic business approach. Top partners run targeted Facebook ad campaigns (₹2,000-₹3,000 monthly budget), maintain educational YouTube channels, and lead teams of 5-10 junior partners. They convert 25-30+ applications monthly while earning overrides on team performance.

This progression takes 4-6 months for focused partners. The path isn't automatic. It requires learning customer psychology, refining product positioning, and developing sales systems. However, the journey costs nothing financially. You invest only time and effort.

Tamil Nadu's literacy rates and business acumen make this progression faster than national averages. Partners grasp financial concepts quickly, explain products clearly, and close sales effectively.

Compare this to traditional business scaling. Growing a retail shop from ₹15K to ₹50K monthly profit requires inventory expansion, staff hiring, and possibly larger premises easily ₹10-20 lakhs additional investment. GroMo scaling requires zero additional capital, just improved skills and expanded reach.

What's ahead for financial distribution in Tamil Nadu

Tamil Nadu's digital financial services market will grow 45% annually through 2028. The state government's digitization initiatives, improving rural internet access, and rising financial literacy create opportunities for distribution partners.

By 2028, an estimated 6 crore Tamil Nadu residents will use digital financial products regularly, up from 3.2 crore in 2026. This expanding market ensures sustainable demand for partners who establish themselves early.

New product categories entering the market include digital gold investments, peer-to-peer lending, invoice financing for SMEs, and embedded insurance. GroMo partners who build customer bases now will cross-sell these products as they launch, multiplying earnings without additional customer acquisition effort.

The platform's product portfolio expands quarterly. January 2026 added three new credit card products. April brought two new business loan partnerships. This continuous innovation provides partners fresh offerings to share with existing customers.

Regional language content and interfaces improve continuously. GroMo's Tamil version receives monthly updates based on partner feedback. Better localization reduces barriers for tier-3 town partners.

Regulatory clarity around digital distribution improves as RBI and SEBI refine frameworks. This professionalization benefits compliant partners by weeding out unethical operators and establishing distribution as a recognized income source.

Tamil Nadu partners entering this space in 2026 position themselves as early participants in a sector that will shape India's financial services distribution for the next decade. Early movers build reputation, teams, and customer bases that become increasingly valuable as markets mature.

Frequently Asked Questions

Do I need prior experience in finance or sales to start?

No prior experience is required. GroMo provides free training through its Academy that covers all financial products, eligibility criteria, and compliance requirements. The courses are available in Tamil. Most successful partners started with zero financial background and learned through the platform's structured training. Your willingness to learn and consistent effort matter more than previous experience.

How quickly can I start earning?

Partners typically earn their first commission within 7-14 days of active sharing. The timeline depends on your network size and product selection. Credit cards and savings accounts have faster processing times (3-7 days from application to approval), generating quicker payouts. Loans take slightly longer (7-15 days) due to verification processes. Payouts reach your bank account within 24-48 hours of customer approval.

Is financial product distribution legal?

Yes, financial product distribution through GroMo is completely legal across India, including Tamil Nadu. You operate as a referral partner, not a direct sales agent or broker. This means you don't need NISM certifications, insurance licenses, or DSA registrations. GroMo holds all necessary regulatory approvals and partnerships with RBI-regulated banks and SEBI-registered financial institutions. Your role is referring potential customers through tracked links. However, you must follow ethical practices: never misrepresent products, respect customer data privacy, and provide accurate information.

Can I do this alongside my full-time job?

Yes, GroMo is specifically designed as a flexible side income opportunity. Most partners maintain full-time jobs or businesses while earning through financial distribution. The model requires only 1-3 hours daily, which you can schedule during commutes, lunch breaks, evenings, or weekends. You work entirely from your smartphone without fixed schedules. Salaried employees share products with colleagues during breaks. Business owners recommend relevant products to existing customers. Students work between classes.

What makes financial distribution more profitable than other zero-investment businesses?

Financial products offer significantly higher commissions than most zero-investment alternatives. While referring e-commerce products pays ₹50-₹200 per sale, credit cards pay ₹600-₹2,400 and loans pay 1.5%-5.5% of sanctioned amounts. A single ₹3 lakh business loan generates ₹4,500-₹16,500 commission equivalent to dozens of e-commerce referrals. Additionally, financial products have higher average transaction values and serious purchase intent. Someone applying for a credit card or loan has genuine need, unlike casual online shoppers who frequently abandon carts.

What support does GroMo provide?

GroMo offers Tamil-language training modules, 24/7 in-app customer support, dedicated partner success managers for high-performers, marketing materials in Tamil and English, and regular webinars covering new products and sales techniques. The app provides real-time tracking of customer applications, automated reminders for follow-ups, and detailed analytics showing which products perform best for your audience. The platform handles all backend operations customer service, documentation processing, compliance management, and payment disbursement allowing you to focus on sharing products and supporting customers.