Earn Up to ₹1 Lakh with GroMo: Zero Investment Online Income

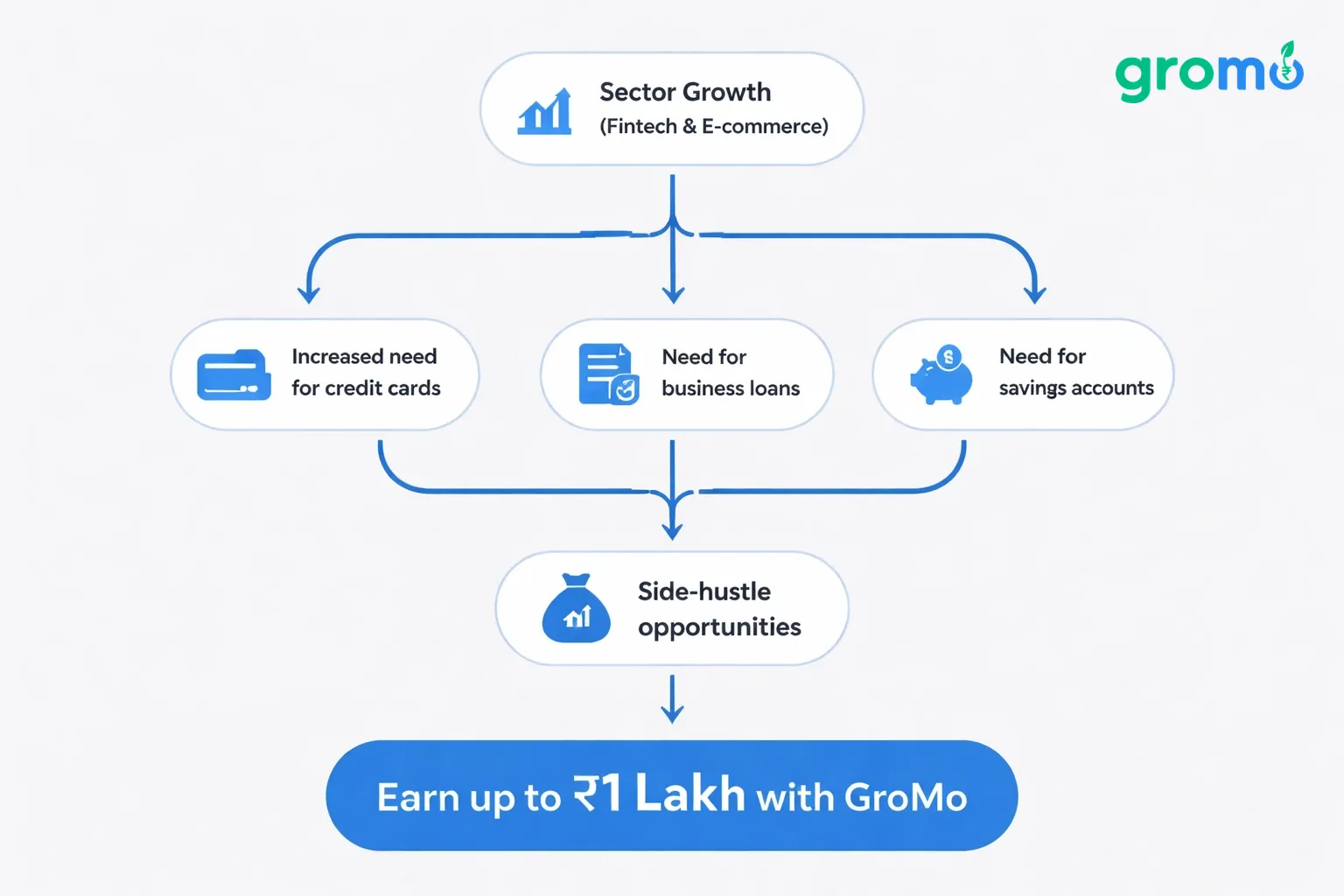

India's fastest-growing business sectors fintech, e-commerce, renewable energy are scaling fast. Usually, you'd think you need to launch a startup to cash in on this. But you don't. You can actually partner as a financial-product distributor on GroMo, earning up to ₹1 lakh monthly without putting down any capital.

Here’s a breakdown of ten high-growth sectors and exactly how GroMo partners sell savings accounts, credit cards, and loans to the people working in them. You don't need an office, inventory, or a team. You just need your phone and a network.

Why Sector Growth Matters for Side Hustles

It’s pretty simple. When an industry doubles in size, the people working there need new financial tools. They need credit cards for expenses, business loans for inventory, and savings accounts for daily wages.

India's GDP is growing steadily, but sectors like fintech and e-commerce are exploding at 15–40% annually. These aren't just numbers on a chart. They represent millions of new earners freelancers, gig workers, small business owners who are often "new-to-credit." Traditional banks sometimes ignore them. That's where you come in. If you understand sector trends, you can pitch the right product Kotak 811 for gig workers, Axis Flipkart credit cards for sellers, Upstox demat for investors and your conversion rates will climb.

Top 10 Fastest-Growing Business Sectors in India (2026 Rankings)

1. Fintech & Digital Payments (30–35% CAGR)

It's no surprise this sits at #1. We're talking about UPI platforms, neobanks, and lending apps. Transaction volumes on UPI crossed 12 billion per month in early 2026.

Every new digital user needs a bank account. As a GroMo partner, this is your bread and butter. You sell Kotak 811 savings accounts (₹550–₹850 payout), Airtel Payments Bank (₹170–₹300), and personal loans from IDFC or InCred. The volume here means more opportunities to sell.

Target customers: Gig workers, freelancers, small business owners moving from cash to digital.

2. E-Commerce & Quick-Commerce (25–30% CAGR)

Online retail is projected to hit $350 billion GMV by 2030. It's not just big cities; tier-2 and tier-3 adoption is driving this. Quick-commerce (10-minute delivery) is creating thousands of jobs and vendor partnerships monthly.

E-commerce sellers need business current accounts (Tide), working-capital loans (ClickPe Business Loan), and cashback credit cards (Axis Flipkart, Swiggy HDFC). Every new seller on Meesho or Amazon is a potential lead for zero-investment business ideas.

Target customers: Kirana stores joining JioMart, home bakers on Instagram, resellers.

3. Edtech & Online Learning (22–28% CAGR)

India's edtech market is valued near $10 billion. Even with funding cooling off, hybrid learning and parental spending keep the sector alive.

Students and parents booking expensive courses need financing. That's where you offer zero-cost EMI cards (Bajaj Insta EMI). Freelance tutors need GST-ready accounts. If you're near colleges, you can distribute SBI credit cards and Kotak 811 accounts to students. Check out part-time business ideas targeting students.

Target customers: College students, freelance tutors, coaching center owners.

4. Healthtech & Telemedicine (20–25% CAGR)

Digital health consultations and online pharmacies are serving over 100 million users annually. Government schemes like Ayushman Bharat are pushing digital records into rural areas.

Doctors setting up tele-clinics need current accounts and business loans. Diagnostic labs expanding to smaller towns need working capital. While GroMo doesn't sell insurance anymore, you can still offer credit cards with health perks and demat accounts for those investing in healthcare stocks.

Target customers: Doctors, physiotherapists, pharmacy owners, diagnostic lab franchisees.

5. Renewable Energy & EV Infrastructure (18–24% CAGR)

Solar installations and EV charging stations are scaling fast, thanks to subsidies like PM Surya Ghar and FAME-II.

Entrepreneurs installing solar panels need MSME loans (Poonawalla Fincorp, ClickPe). Electricians joining this workforce need their first savings accounts and credit-builder cards like the KIWI Rupay. Position yourself in zero-investment business clusters near solar hubs or EV dealerships.

Target customers: Solar installers, EV dealership staff, battery technicians.

6. Logistics & Warehousing (16–22% CAGR)

Third-party logistics and last-mile delivery networks are expanding to support e-commerce growth. The government's National Logistics Policy aims to cut costs, boosting demand for tech-enabled freight.

Truck owners need commercial-vehicle loans. Delivery partners need instant digital accounts like Airtel Payments Bank to manage daily earnings. Check remote jobs and online income strategies if you're targeting gig-logistics workers.

Target customers: Fleet owners, truck drivers, warehouse managers, delivery partners.

7. Agritech & Food Processing (15–20% CAGR)

Precision farming and farm-to-consumer platforms are modernizing agriculture. Startups are offering soil-testing apps and tractor rentals.

Agri-entrepreneurs need business loans with quick turnaround. Farmers adopting digital payments need zero-balance savings accounts. If you're in rural areas, look at zero-investment business ideas in West Bengal or Punjab.

Target customers: Agri-input dealers, food processing unit owners, tractor-rental operators.

8. SaaS & Enterprise Software (18–23% CAGR)

Cloud-based CRM and HR tools are replacing legacy systems in Indian SMEs. Companies like Zoho and Freshworks are scaling globally.

Tech employees earn well but often lack financial planning. They are perfect candidates for demat accounts (Upstox) to invest surplus income, premium credit cards (HDFC Pixel Play), and personal loans. Target co-working spaces and tech meetups with commission-based online income strategies.

Target customers: Software developers, digital marketers, startup founders.

9. Travel & Hospitality (Post-Pandemic Rebound: 20–25% CAGR)

Domestic tourism is booming. India recorded 1.4 billion domestic tourist visits in 2025.

Hotel owners need working-capital loans to refurbish properties. Travel influencers use credit cards with travel rewards (Scapia Federal). Position yourself in tourist hubs like Goa or Rajasthan. Read about zero-investment business in Delhi, a key tourism market.

Target customers: Homestay owners, tour operators, cab-service providers.

10. D2C Consumer Brands (15–20% CAGR)

Direct-to-consumer brands in beauty, fashion, and wellness are bypassing retail to sell directly on Instagram and websites.

D2C founders need business current accounts and inventory-financing loans. Their customers need buy-now-pay-later options (Bajaj Insta EMI). Tap into entrepreneur communities in metros check out zero-investment ideas in Mumbai, Bangalore, Hyderabad, and Pune.

Target customers: D2C brand founders, social-media managers, influencers.

How to Profit from Sector Growth

Map your network. List everyone you know. Your cousin driving for Swiggy? Logistics sector. Your neighbor installing solar panels? Renewable energy.

Match needs to products.

| Sector | Primary Need | Recommended Product | Payout |

|---|---|---|---|

| Fintech workers | Savings account, credit card | Kotak 811, SBI Credit Card | ₹550–₹3,750 |

| E-commerce sellers | Business account, working capital | Tide, ClickPe Business Loan | ₹440–₹3,000 |

| Edtech freelancers | Personal loan, credit card | Bajaj Insta EMI, HDFC Pixel Play | ₹350–₹2,750 |

| Healthtech professionals | Business loan, demat account | Poonawalla Fincorp BL, Upstox | ₹250–₹3% |

| Renewable-energy techs | MSME loan, savings account | ClickPe, KIWI Rupay | ₹550–₹3,000 |

| Logistics gig workers | Zero-balance account, fuel card | Airtel Payments Bank, IOCL Axis | ₹170–₹2,700 |

| Agri-entrepreneurs | Business loan, current account | Poonawalla Fincorp, Tide Business | ₹440–₹3% |

| SaaS employees | Demat, premium credit card | Aditya Birla Money, HDFC Pixel Play | ₹180–₹2,750 |

| Travel operators | Working-capital loan, travel CC | InCred PL, Scapia Federal | ₹1.5%–₹4% |

| D2C founders | Business loan, credit card | ClickPe, Axis Flipkart | ₹350–₹3,000 |

Speak their language. Don't just ask "Do you want a credit card?" Say: "As an e-commerce seller, you can earn 5% cashback on ad spends with the Axis Flipkart card."

Time your outreach. Tax season for business owners, admission season for tutors, Diwali restocking for vendors.

Build credibility. Complete GroMo Academy modules. When a solar installer asks if they qualify for a loan, answer with authority.

Turning Knowledge into ₹1 Lakh Monthly Income

Imagine you live in Pune. You know 50 people across IT, e-commerce, and EV charging stations.

- Month 1: You finish training. You share Kotak 811 and Axis Flipkart links in WhatsApp groups. You earn ₹15,000 from 10 accounts and 3 cards.

- Month 2: You ask happy customers for referrals. You pitch Upstox demat to IT friends and ClickPe loans to sellers. You earn ₹40,000.

- Month 3: You recruit 3 sub-partners. They handle logistics workers while you focus on high-ticket loans. Collective payout crosses ₹1 lakh.

Common Pitfalls

- Ignoring compliance. Loan payouts reverse if the borrower defaults early. Don't push loans to people who clearly won't qualify.

- Over-promising. Approval isn't guaranteed. Set expectations: "I'll help you apply; approval depends on the bank."

- Neglecting follow-ups. A customer who opens an account today might need a loan in six months. Stay in touch.

- Chasing only high payouts. A ₹3,750 SBI card rejection wastes time. Mix in easier products like SBM Novio FD-backed cards.

Why GroMo Works

GroMo's network spans all ten sectors. You aren't locked into one vertical like a traditional franchise. A single partner in Hyderabad can sell Tide accounts to logistics startups in the morning and Upstox demat to IT colleagues at lunch. That flexibility is why partners earn ₹50,000+ monthly with zero investment.

Frequently Asked Questions

Q: Which sector is easiest for beginners? A: E-commerce and gig logistics. High turnover, immediate financial needs, low documentation barriers. Start with Airtel Payments Bank and Kotak 811.

Q: Can I sell to multiple sectors at once? A: Yes. You can refer an edtech tutor to Bajaj Insta EMI, a solar installer to ClickPe, and an IT freelancer to Upstox all in the same week.

Q: Do I need to know everything before starting? A: No. Focus on 3–4 beginner-friendly products like Kotak 811 and SBI Credit Card. Learn the rest as you go using GroMo Academy.

Q: How do I find leads outside my network? A: Join sector-specific WhatsApp groups. Attend local meetups. Offer free financial literacy webinars to attract warm leads.

Q: What if a sector slows down? A: Diversify across three to five sectors. Fintech and e-commerce are structurally supported by policy, making them safer bets than speculative trends.

Q: How long until I see my first payout? A: Instant-payout products like Kotak 811 credit your wallet within hours. Most partners see ₹500–₹2,000 in their first week if they make 5–10 referrals.