Earn ₹50K+ Monthly with Zero Investment via GroMo

The old advice get a degree, land a 9-to-5, retire at 60 feels increasingly out of touch in India right now. Traditional jobs haven't disappeared, but they're no longer the only path to stability. Over 60 lakh Indians are now earning anywhere from ₹10,000 to over ₹1 lakh a month through commission-based work. They aren't opening offices or buying inventory. They're using their phones and their networks to distribute financial products.

The gig economy in India is growing fast about 17% annually through 2027. This isn't just about delivery jobs or ride-sharing anymore. It's about flexible work that reaches beyond the metros into Tier 2 and Tier 3 cities. Whether you are a student, a homemaker, or someone looking to exit a corporate job, platforms like GroMo offer a legitimate way to build income without upfront capital.

Why the traditional job math doesn't work anymore

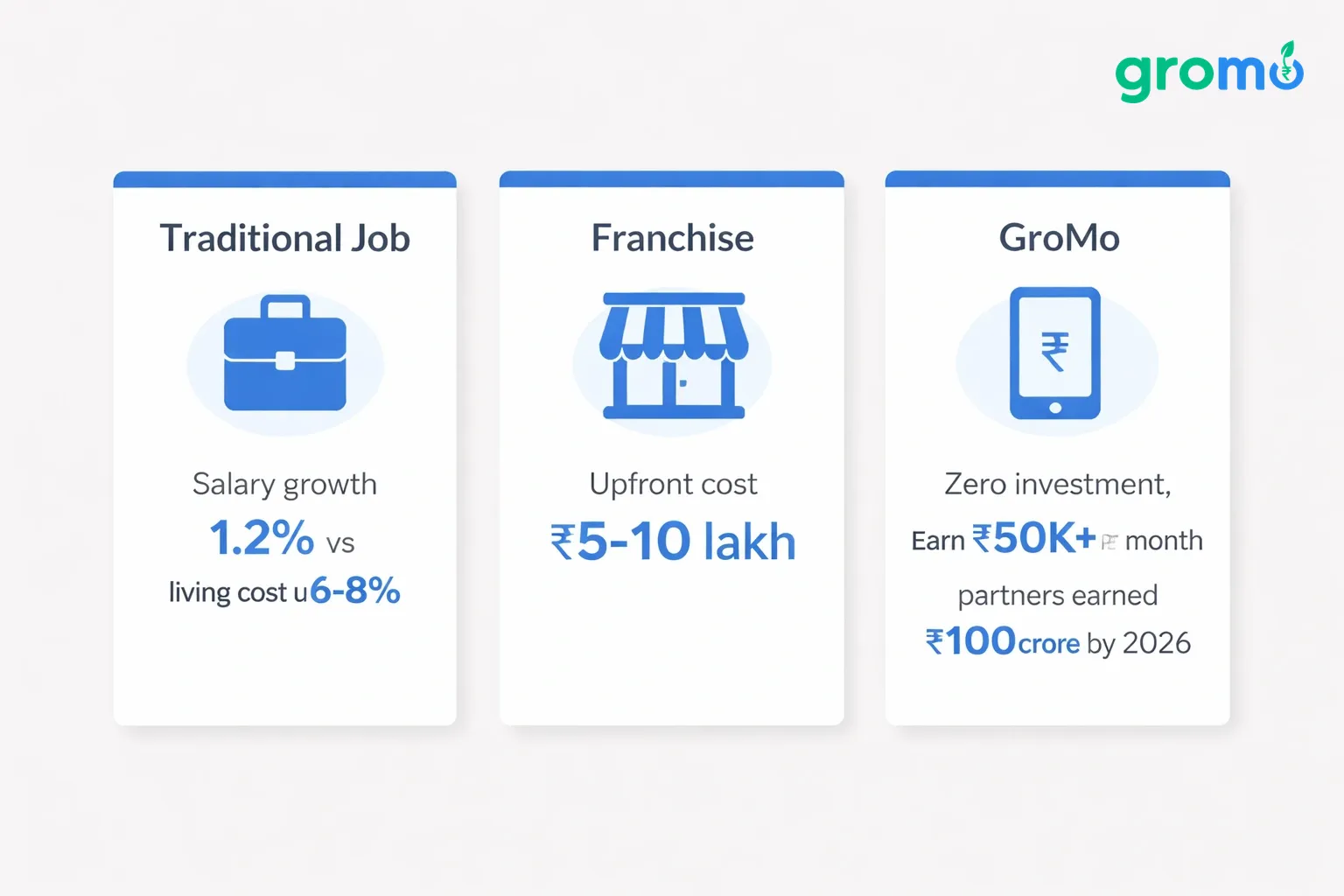

Salaries in many sectors have stagnated. RBI data shows real wage growth averaged just 1.2% in 2025, while urban living costs climbed 6-8% annually. That gap creates real pressure.

Commission-based work removes geographic barriers and lets you set your own hours. Unlike a franchise, which might demand ₹5-10 lakh upfront, or a traditional business requiring inventory and shop space, digital financial distribution needs only a smartphone and a decent internet connection.

The numbers back this up. By mid-2026, partners on GroMo had collectively earned ₹100 crores. Top performers regularly clear ₹1 lakh monthly just through referrals. It opens up income opportunities that were previously restricted to licensed agents or financial professionals.

The five best income streams in India right now

Commission-based financial product distribution sits at the top for zero-investment returns. Partners earn ₹800-₹3,000 per credit card application, ₹250-₹650 per savings account, and 1.5-2.5% on loans disbursed. Getting an HDFC credit card approved pays around ₹2,400. Refer ten of those a month, and you're looking at ₹24,000 with zero inventory risk.

Demat account referrals offer a nice secondary income. Platforms like Upstox and Indiabulls pay ₹250-₹400 per activated account. Once customers start trading, partners often get secondary commissions on transaction volumes. If you have 50 active trading clients, you can realistically generate ₹12,000-₹20,000 a month passively.

Loan distribution pays the most per transaction. Business loans through ClickPe (Muthoot Finance) pay 1.5-2.5% of the disbursed amount. A ₹3,00,000 business loan approval puts ₹4,500-₹7,500 in your pocket. Five of those a month is ₹22,500-₹37,500.

Savings account openings provide steady volume. IndusInd Bank accounts pay ₹650-₹1,000 each; Tide Business accounts offer staggered payouts that total similar amounts. If you target small business owners in your network, 20-30 account openings a month is realistic (₹13,000-₹30,000).

Credit line products like IDFC FatakPay or HDFC Smart EMI offer 0.5-1% commissions on credit extended. These products appeal to existing credit card holders who need instant liquidity, leading to high conversion rates if you know who to target.

The common thread? These products solve real problems. You aren't pushing unnecessary purchases; you're helping people access credit, build portfolios, or manage cash flow.

How to hit ₹50,000+ monthly with GroMo (a realistic timeline)

Month 1: Figuring it out (Target: ₹5,000-₹15,000)

Week one, download GroMo, finish your KYC, and take the free training modules on credit cards, loans, and accounts. The certification matters it gives you the product knowledge you need to actually convert people.

Weeks two through four, start close to home. Family, friends, colleagues. Match products to their needs: credit cards for people who spend heavily, demat accounts for friends curious about stocks, business loans for entrepreneur contacts. Aim for 10-15 conversions.

What you might earn: 3 credit cards (₹6,000) + 7 savings accounts (₹5,000) + 2 demat accounts (₹600) = ₹11,600.

Month 2: Scaling up (Target: ₹20,000-₹35,000)

Build a referral system. Every happy customer is a potential referral source. Ask them to introduce friends who need similar products. Create a WhatsApp broadcast list where you share useful updates not spam, but actual value about financial products.

Get involved in community groups: local business associations, housing society chats, alumni networks. You can offer free financial literacy sessions on how credit cards build CIBIL scores or how demat accounts work.

What you might earn: 8 credit cards (₹16,000) + 15 savings accounts (₹10,000) + 5 business loans (₹15,000 average) = ₹41,000.

Month 3+: Making it sustainable (₹50K+)

Look at your data from the first two months. Which product converts best for you? If it's credit cards, specialize. Learn every card's benefits and eligibility inside out. Specialization makes your pitch better.

Use GroMo's customer management tools. Many applications get stuck at the VKYC or document upload stage. Following up proactively pushes approval rates from 40% to over 70%.

Build a team. GroMo has a referral program for recruiting others. Train 2-3 motivated people using what you've learned and earn secondary commissions on their sales.

Potential earnings: 10 credit cards (₹20,000) + 20 savings accounts (₹13,000) + 8 business loans (₹24,000) + team commissions (₹5,000) = ₹62,000.

The key is consistency. Doing a little bit every day beats sporadic bursts of effort. Learn how full-time employees balance this.

Who is actually making money?

Working professionals (35% of top earners) use their existing networks. A Bangalore IT consultant earning ₹80,000 salary adds ₹40,000 monthly just by referring credit cards to colleagues and helping them optimize rewards. Time spent: about 1.5 hours a day during commutes.

Housewives (28% of top earners) rely on community trust. A Delhi homemaker built a ₹55,000 monthly income focusing on IndusInd and Tide Business accounts for neighborhood shop owners. Her advantage: she already knows and trusts the people in her residential complex.

Students (18% of top earners) use their digital skills. A Chennai college student earns ₹25,000 monthly promoting demat accounts through Instagram reels explaining stock market basics. Content creation brings in organic leads, and conversion happens through GroMo links.

Retirees (12% of top earners) monetize lifetime networks. A retired Mumbai banker generates ₹35,000 monthly distributing business loans to former colleagues who now run their own businesses. Decades of relationships translate directly to high-trust conversions.

Small business owners (7% of top earners) cross-sell to existing customers. A Pune accounting firm owner adds ₹20,000 monthly by offering business accounts and loans to tax clients.

The pattern is clear: success correlates with network quality, not size. Ten trusted contacts beat 1,000 strangers. Housewives specifically have built sustainable models around this principle.

The products that actually convert

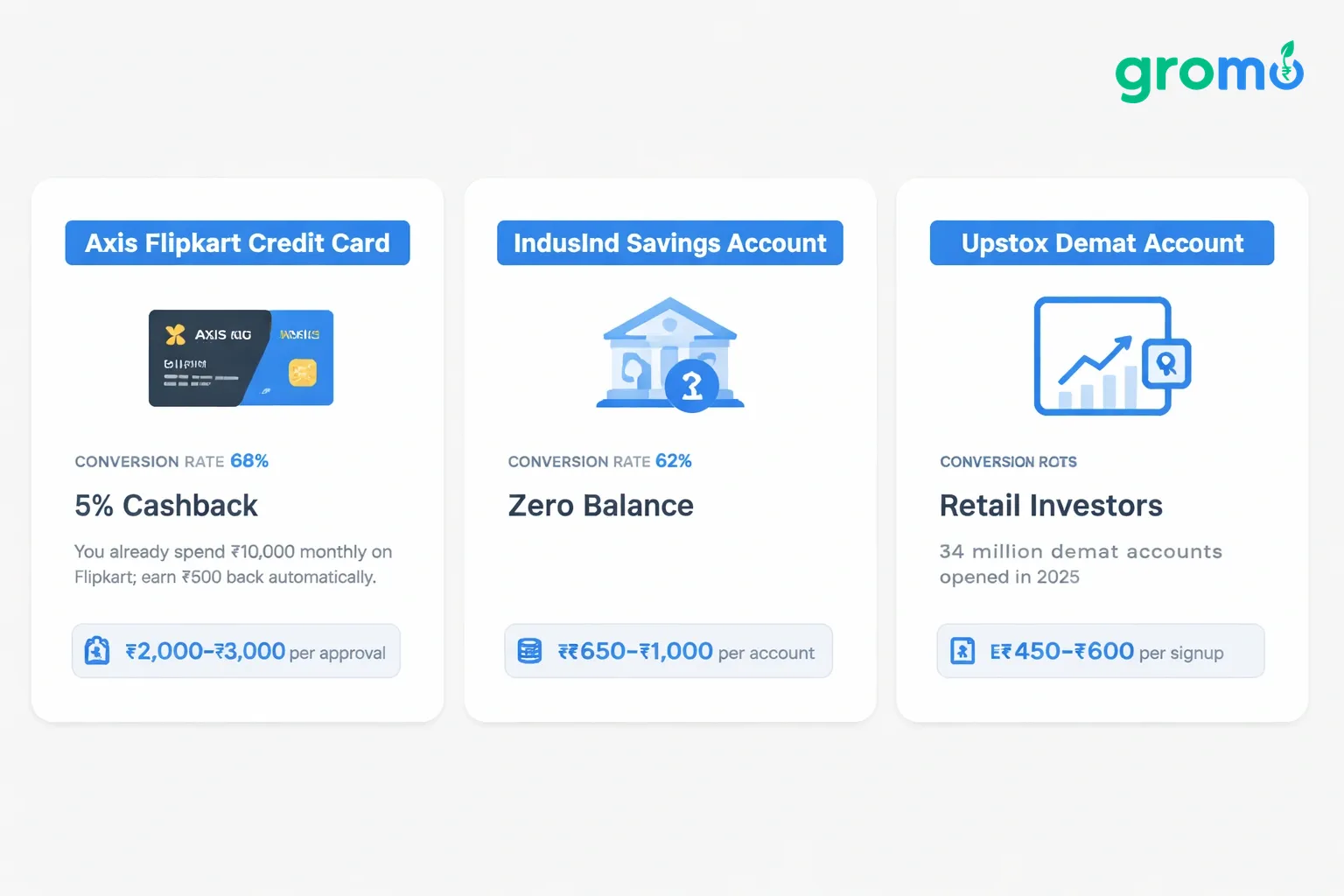

Axis Flipkart Credit Card has the highest conversion rate at 68% among eligible applicants. The 5% Flipkart cashback resonates with almost everyone. The pitch is simple: "You already spend ₹10,000 monthly on Flipkart; earn ₹500 back automatically." Earning: ₹2,000-₹3,000 per approval.

IndusInd Savings Account converts at 62% because it has zero balance requirements. Customers fear minimum balance penalties; IndusInd removes that barrier. Earning: ₹650-₹1,000 per account.

Upstox Demat Account targets the growing retail investor base 34 million demat accounts opened in 2025 alone. Zero opening fees make it an easy sell. Conversion rate: 58%. Earning: ₹250-₹400.

ClickPe Business Loan works because traditional banks reject 40% of MSME loan applications. ClickPe approves within hours. Conversion rate among eligible businesses: 54%. Earning: 1.5-2.5% of loan amount.

IDFC Credit Card Against FD solves the "no credit history" problem. Students and homemakers get approved by putting down a ₹5,000 FD. Conversion rate: 71%. Earning: ₹700-₹1,000.

These products win because they solve immediate pain points without asking customers to change their behavior.

Common mistakes that keep earnings low

Pitching without understanding needs kills conversion. A salaried employee doesn't need a business loan. A homemaker with no credit history won't qualify for a premium card. Solution: Ask three qualifying questions before recommending anything.

Ignoring follow-up wastes half your potential earnings. Many applications stall at VKYC or document upload. A single WhatsApp message 24 hours later increases completion rates by 40%. Use GroMo's in-app reminders.

Spreading yourself thin dilutes expertise. Partners promoting 15 products earn 30% less than those who specialize in 3-4 categories. Shallow knowledge reduces your credibility.

Targeting only high-income networks limits volume. Five solid conversions at ₹6,000 earnings each beat one premium customer who takes weeks to close.

Treating it as passive income immediately sets you up for disappointment. The first two months require active effort. Passive income kicks in later, once your referral network matures.

Comparing yourself to the top 1% is demotivating. GroMo highlights partners earning ₹1 lakh+, but median earnings in Month 1 are ₹8,000-₹12,000. Realistic expectations matter.

Legal and compliance basics

You are not a financial advisor. GroMo partners are distributors. Never claim to "advise" customers say you "share product information." This distinction keeps you compliant with SEBI/IRDA regulations.

Customer data security is non-negotiable. Applications must happen on the customer's device using their own number. Never collect PAN, Aadhaar, or OTP on your phone. Violations lead to account suspension and potential legal trouble under the IT Act 2000.

Misrepresentation voids payouts. Don't promise guaranteed approvals or inflate benefits. Stick to official T&Cs.

Clawback provisions exist. If a customer closes an account within 90 days or defaults on early EMIs, your commission gets reversed. This incentivizes quality referrals.

Tax obligations kick in above ₹5 lakh annual income. GroMo doesn't deduct TDS, so you are responsible for filing ITR.

Other income streams to consider

Freelancing on Upwork or Fiverr lets you monetize skills like writing or design. Earning: ₹20,000-₹80,000 monthly. Time: 15-20 hours weekly.

Content creation on YouTube or Instagram can generate ad revenue. A Hyderabad creator teaching personal finance earns ₹45,000 from ads plus ₹30,000 from sponsorships. Time to monetize: 4-6 months.

Online tutoring through Vedantu or Unacademy pays ₹15,000-₹50,000 for subject experts. Time: 10-15 hours weekly.

Affiliate marketing beyond finance works for niche audiences. A fitness blogger earns ₹22,000 promoting supplements.

Reselling via Meesho or Shopify lets you curate products without inventory. A Jaipur partner earns ₹30,000 reselling ethnic wear through WhatsApp.

Digital services like SEO or social media management can earn ₹25,000-₹1,00,000 monthly once you have clients.

Stack these smartly. A GroMo partner earning ₹40,000 could add ₹20,000 through weekend freelancing. Multiple income streams build resilience.

Where Indians earn the most

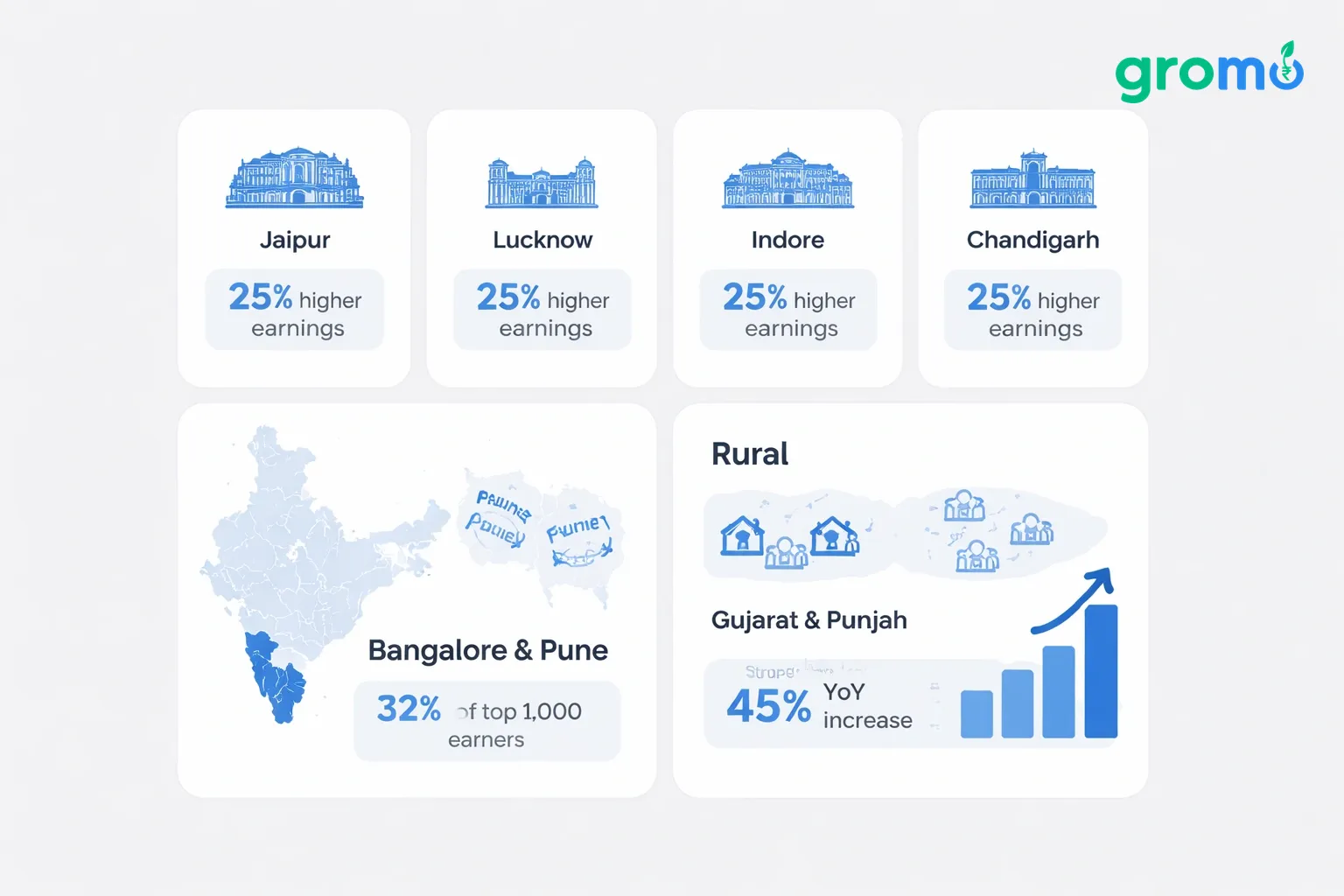

Tier 2 cities lead adoption. Jaipur, Lucknow, Indore, and Chandigarh partners earn 25% more on average than those in metros. Lower living costs mean ₹30,000 goes much further there.

Bangalore and Pune dominate absolute numbers 32% of GroMo's top 1,000 earners live in these cities. Tech exposure makes users comfortable with app-based work.

Gujarat and Punjab show the highest rural penetration. Village-level partners use tight community networks effectively. A Patiala partner serves 150+ farming families. Trust translates to conversion.

UP and Bihar are the fastest-growing markets 45% YoY increase in active partners. Rising smartphone use and digital payment adoption drive this.

The insight? Success isn't limited to metros. Small-town advantages include strong community ties and lower customer acquisition costs.

Tech tools that help

GroMo's in-app CRM tracks the customer journey. Set reminders for VKYC follow-ups. Partners who use these features earn 35% more.

WhatsApp Business lets you create broadcast lists. Share value content weekly, not spam. Open rates hit 65% versus 18% for email.

Canva creates professional infographics quickly. Visual content increases engagement by 40% over text-only messages.

Google Sheets helps you track your funnel. Log every lead: source, product, status, payout. Analyzing this monthly reveals what works.

Calendly professionalizes VKYC scheduling. Send a link instead of playing phone tag. It reduces dropouts by 22%.

Notion or Evernote helps you organize product knowledge. Keep a personal wiki of eligibility, benefits, and pitch templates.

Where this is headed (2026-2028)

AI-assisted selling is becoming a competitive edge. GroMo's Guru AI bot answers product queries in real-time, reducing training time. Early adopters see 28% higher conversion rates.

Video-based KYC will be standard by Q4 2026, cutting approval times from days to hours. Faster approvals mean faster payouts.

Embedded finance is expanding product catalogs UPI credit lines, BNPL integrations, and micro-investments. More products mean more opportunities.

Hyperlocal specialization pays off. Partners who become the "go-to" person for specific communities like CAs for CA networks command premium conversion rates.

Regulatory clarity around gig work will likely mandate insurance and benefits by 2027. Stick with established platforms like GroMo that have a compliance track record.

Tax optimization

ITR-4 filing works for most partners earning ₹50,000-₹2,00,000 annually. The presumptive taxation scheme assumes 50% of receipts as profit.

Section 44ADA covers professionals earning commission. It lets you declare 50% of gross receipts as expenses without detailed books. Above ₹5 lakh, get a CA consultation.

80C investments reduce taxable income by ₹1.5 lakh. Invest commission earnings in PPF, ELSS, or NPS.

Quarterly advance tax is mandatory above ₹10,000 annual tax liability. Pay on time to avoid penalties.

Rule of thumb: Invest 10% of monthly commission into tax-saving instruments so you aren't scrambling at year-end.

Frequently Asked Questions

Q: Can I really earn ₹50,000+ monthly with zero investment, or is GroMo exaggerating? A: The potential is real, but it's not automatic. Median earnings in Month 1 are ₹8,000-₹15,000. That grows to ₹30,000-₹50,000 by Month 4-6 if you're consistent. Top 10% earners make over ₹1 lakh. Zero investment is accurate; earnings scale with effort.

Q: Do I need financial qualifications? A: No. GroMo provides free training. You are a distributor, not an advisor, so you don't need SEBI/IRDA licenses. You do need to complete GroMo's training before sharing links.

Q: How long until I get paid? A: Commissions credit within 24-72 hours of approval. Withdraw anytime from your GroMo wallet. Some products like Tide Business accounts have staggered payouts tied to customer activity.

Q: What if a customer defaults or closes their account? A: Clawback applies. If a customer defaults on the first three EMIs or closes an account within 90 days, your commission is reversed. Focus on quality referrals.

Q: Can I do this with a full-time job? A: Yes. Most successful partners work 1.5-2 hours daily. It happens on your personal phone using your own time. Your employer won't know unless you tell them.

Q: Is this sustainable long-term? A: Financial product distribution is still undersaturated in India. Only 3% of eligible Indians own demat accounts. However, competition will increase. Long-term success requires specialization and building deep trust.