Zero-Investment Business Models in 2026

Starting a business in 2026 sounds great on paper. India's startup ecosystem is booming, digital payments are everywhere, and it feels like everyone you know is launching something. But the reality? Most businesses need money. A lot of it. And time. And patience.

But what if you don't have ₹5 lakhs to drop on inventory? What if you want to see cash flow in a week, not a year?

We looked at the landscape these are the 10 business models that actually make sense for 2026, including the one that's let over 60 lakh Indians earn decent money without investing a single rupee.

1. Financial Product Distribution (The Zero-Investment Winner)

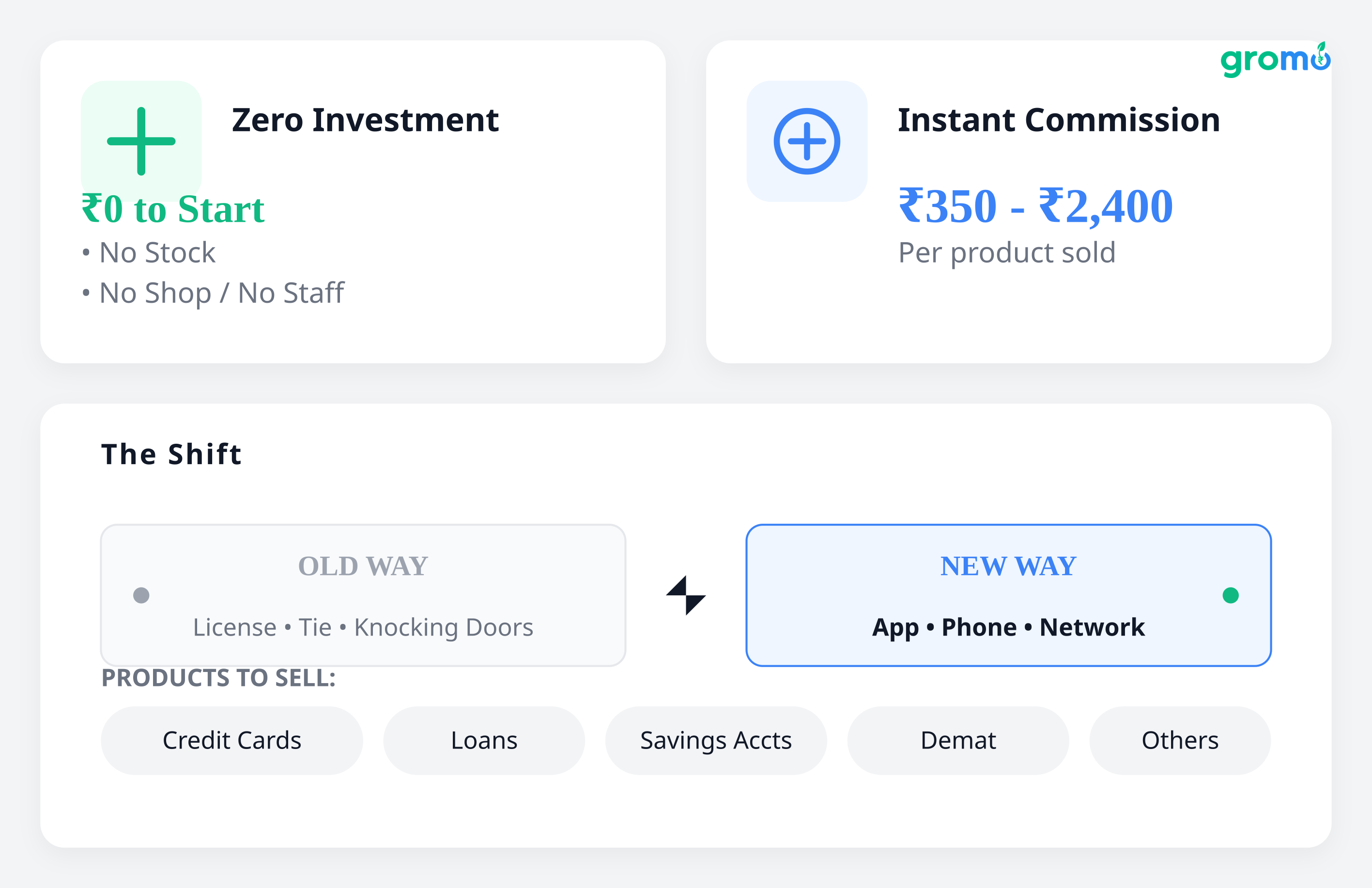

This isn't the business model your parents would recognize. Selling financial products used to mean getting an insurance license, wearing a tie, and knocking on doors. Now? It's an app on your phone.

Platforms like GroMo let you become a certified partner. You sell credit cards, loans, savings accounts, demat accounts to people you already know. You get paid commissions. No stock, no shop, no staff.

Why is this #1 for 2026?

- You need ₹0 to start. Literally just a phone.

- You get paid instantly ₹350 to ₹2,400 per product sold.

- Everyone needs this stuff. Students need savings accounts. Uncles need credit cards. Shopkeepers need working capital loans.

- The training is free and inside the app.

- You can do it from a bus, a bedroom, or a breakroom.

Real numbers: The people crushing it are making ₹1–3 lakhs a month. They're selling 40–100 products consistently. But even if you're just starting, ₹20,000–₹50,000 in the first month is realistic.

Where to start:

- SBI Credit Cards (₹2,400 per approval)

- Kotak 811 Savings Account (₹550)

- Bajaj Finserv Insta EMI Card (₹350)

- Axis Flipkart Credit Card (₹1,950)

You aren't "selling" in the traditional sense. You're just helping people find products they need anyway. Your college friend wants to start trading? He needs a demat account. Your neighbor wants a credit card with lounge access? You send him the link.

2. Digital Marketing Agency

If you're online in 2026, you're fighting for attention. Every business from the chai tapri to the local clothing brand needs Instagram, Google, and WhatsApp visibility.

This takes a laptop and some software subscriptions. Expect to spend ₹30,000–₹1,00,000 upfront.

You need to know social media, basic design, and how to run ads. You can learn most of this on YouTube. Income is all over the place ₹50,000 to ₹5,00,000 a month depending on how many clients you can juggle.

Start small. Offer to handle social media for 5–10 local shops at ₹5,000–₹15,000 a month each. Once you have cash flow, add Google Ads, websites, or influencer tie-ups.

Tip: Don't be a generalist. Pick doctors, real estate agents, or cafes. Specialize.

3. Cloud Kitchen / Home-Based Food Business

Food delivery is a monster. The market is supposed to hit ₹1 lakh crore by late 2026. Cloud kitchens are just cooking facilities without a dining room. You save 60–70% on rent.

But it's not cheap. A proper setup runs ₹2–8 lakhs for equipment, licenses, and initial stock. You need FSSAI clearance and a deal with Zomato or Swiggy.

Margins are tight. The apps take 20–30%. Wastage hurts.

What works right now:

- Regional food people miss from home (Bengali, Kerala, Maharashtrian)

- Healthy tiffin subscriptions for office workers

- Desserts only

- Late-night delivery (9 PM to 3 AM)

It's high effort. If you don't love cooking or operations, skip it.

4. Ed-Tech Tutoring / Skill Training

Parents will cut other expenses before they cut education spending. But the game has changed. It's not just math tutoring anymore.

If you're teaching online, you need ₹10,000–₹50,000. A physical center? That's ₹2–5 lakhs.

What's hot:

- NEET/JEE crash courses

- Stock market basics for teens

- AI and coding bootcamps

- Spoken English + job interview prep

- Government exam coaching

Start with one-on-one sessions over Zoom. Group batches come later.

5. E-Commerce Reselling / D2C Brand

You can sell online without making a product. Resell via Meesho or Amazon, or build a brand on Shopify.

Budget ₹50,000–₹3,00,000 for stock and ads.

Categories that aren't saturated yet:

- Eco-friendly stuff (bamboo brushes, reusable bags)

- Local handicrafts

- Gym supplements

- Custom gifts

- Pet products

Two ways to play it:

Reselling: Buy from IndiaMART, list on Amazon. Margins are 15–25%. Low stress.

D2C Brand: Build your own label. Sell on Instagram and Shopify. Margins are 40–60%. But you have to do the marketing, branding, and customer service yourself.

6. Content Creation / Influencer Marketing

Build an audience, get paid. That's the whole model.

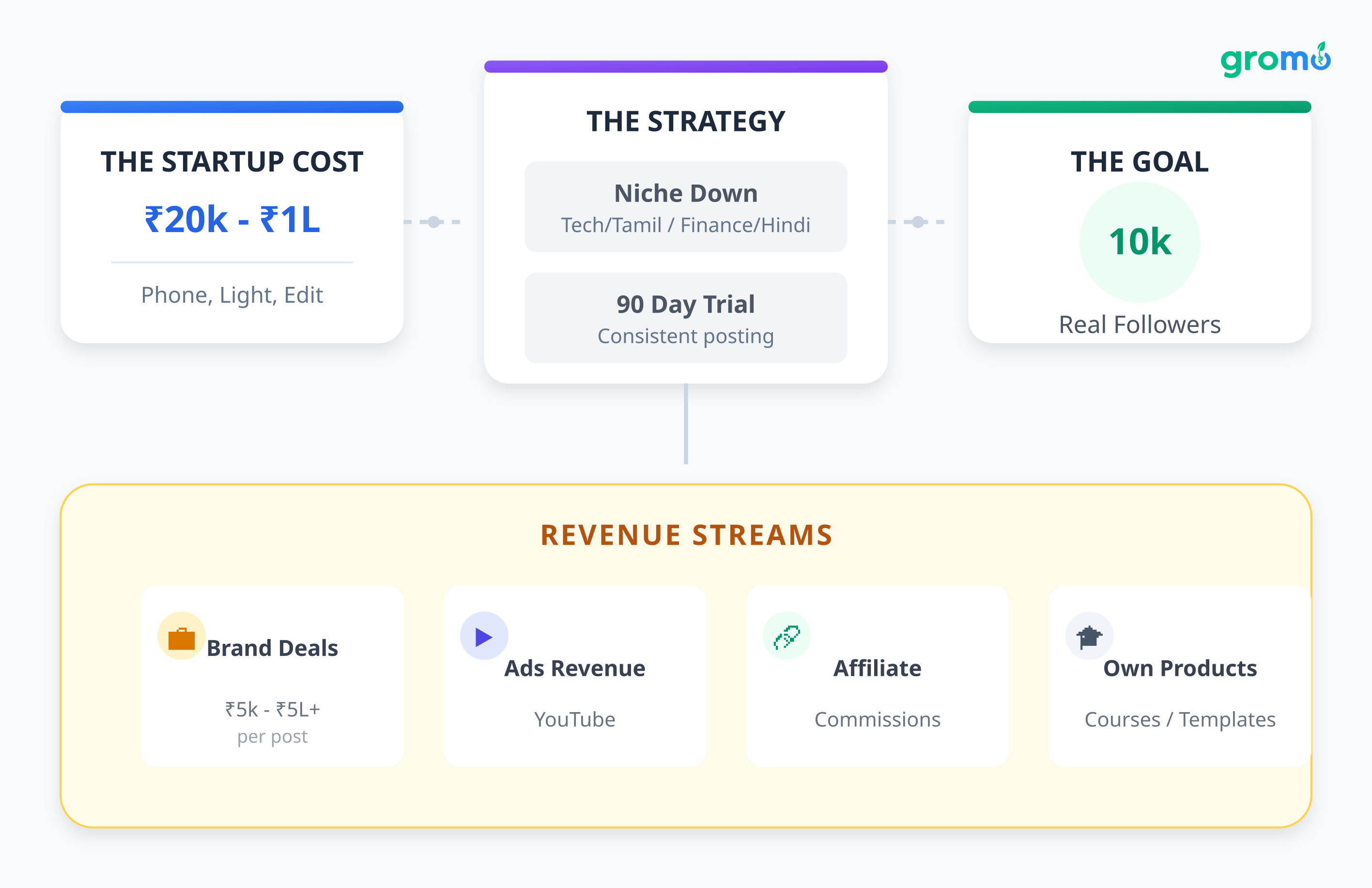

You need a decent phone and maybe some lighting/editing software. ₹20,000–₹1,00,000 gets you started.

How you get paid:

- Brand deals (₹5,000 to ₹5,00,000+ per post if you're big)

- YouTube ad revenue

- Affiliate links

- Selling your own courses or templates

Niche down. "Tech reviews in Tamil" or "Finance tips in Hindi" works better than "lifestyle vlogger."

90 days of consistent posting. That's the trial period. If you can get 10,000 real followers, you can make money.

7. Freelance Services (Writing, Design, Development)

Freelancing is the classic low-cost, high-skill play. India has the world's largest freelance workforce now.

A laptop and internet is all you need. Maybe a portfolio site.

What pays well in 2026:

- AI prompt engineering (yes, that's a job now)

- Technical writing

- UI/UX design

- WordPress/Shopify builds

- Short-form video editing

- Virtual assistant work

Find work on Upwork, Fiverr, LinkedIn, or WhatsApp groups.

Don't charge hourly. Charge by the project. A logo might take you 2 hours. If you charge hourly, you make ₹2,000. If you charge by the project, you make ₹20,000.

8. Real Estate Consulting / Property Dealing

Real estate is waking up again after the 2023 dip. Interest rates are stabilizing. People are buying.

You need RERA registration and a way to get around. ₹20,000–₹1,00,000 covers the basics.

You connect buyers to sellers or developers. Commission is 1–2% of the deal value. One big sale can net you lakhs.

But be warned: deals take months. You might show 50 properties before one closes. It's a game of patience.

9. Health & Fitness Coaching

Health consciousness didn't disappear after the pandemic. It actually grew.

If you go online, costs are low. Offline, you need equipment and space.

Certifications help (ACE, NASM, ISSA), but results matter more. Get 10 people to transform their health, document it, and use those stories to get paying clients.

Services:

- Personal training

- Diet consulting

- Yoga classes

- Corporate wellness

10. Franchise Business (Food, Education, Retail)

If you have ₹5–20 lakhs and want a playbook, buy a franchise.

You get the brand, the training, and the systems. Failure rates are lower than starting from zero.

But you pay royalties (5–10% of revenue) forever. And you can't change the menu, the logo, or the layout.

Options:

- Amul parlor

- Pizza chains

- Kumon learning centers

- Water plants

- FirstCry

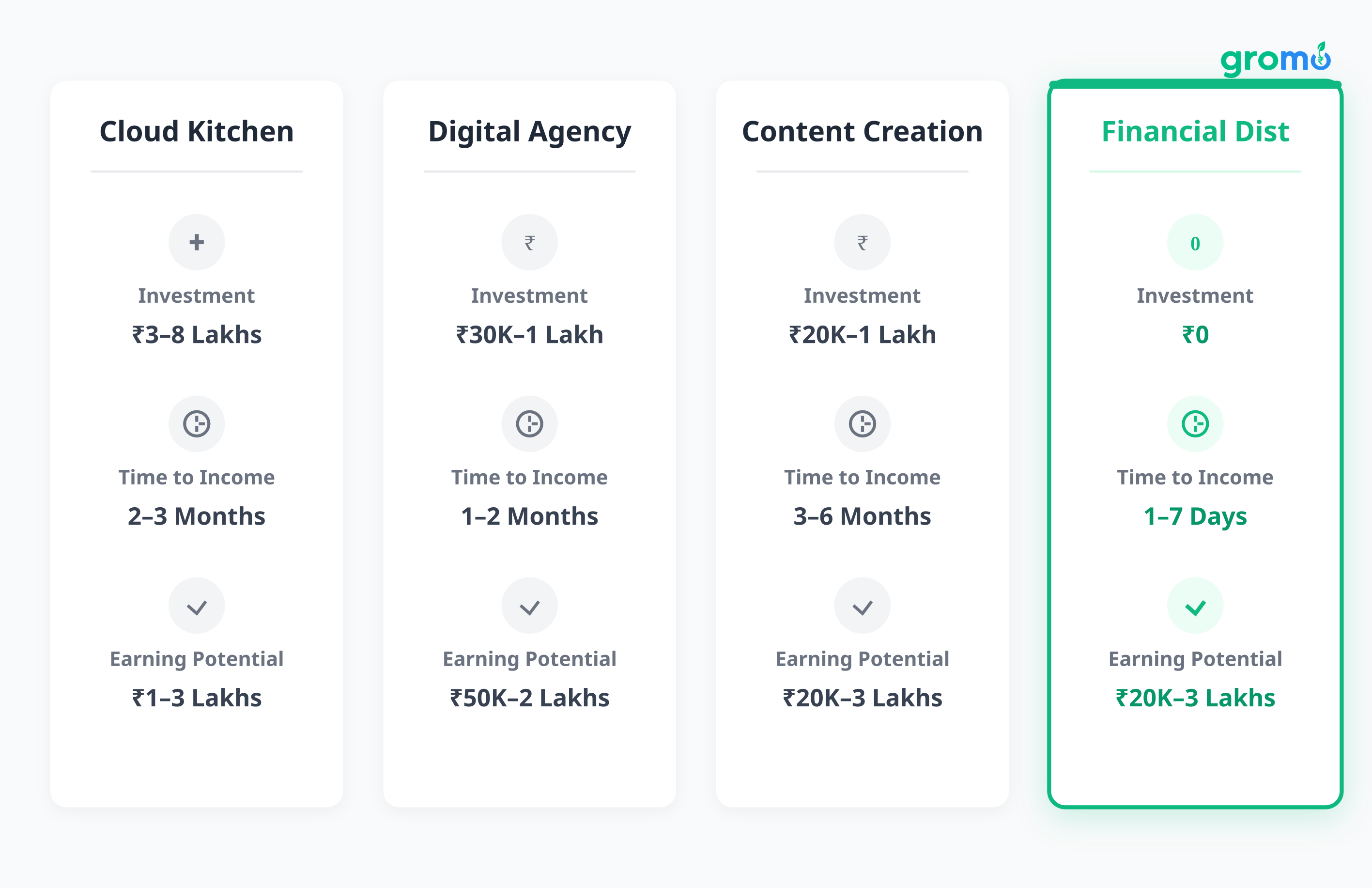

Why Financial Product Distribution Wins in 2026

Let's look at the trade-offs.

Cloud kitchen: ₹3–8 lakhs. 2–3 months before you see profit. Operational headaches. Digital agency: ₹30K–1 lakh. 1–2 months. Client management. Content creation: ₹20K–1 lakh. 3–6 months. Hit or miss.

Financial distribution via GroMo:

- Start-up cost: ₹0.

- First income: 1–7 days.

- Monthly realistic: ₹20K–3 lakhs.

| Business Type | Initial Investment | Time to First Income | Monthly Earning Potential |

|---|---|---|---|

| Cloud Kitchen | ₹3–8 Lakhs | 2–3 months | ₹1–3 Lakhs |

| Digital Agency | ₹30K–1 Lakh | 1–2 months | ₹50K–2 Lakhs |

| Content Creation | ₹20K–1 Lakh | 3–6 months | ₹20K–3 Lakhs |

| Financial Distribution | ₹0 | 1–7 days | ₹20K–3 Lakhs |

It's not just the money. It's the speed and the lack of risk.

How to Start Your Financial Distribution Business Right Now

- Download the GroMo app. Sign up.

- Watch the training videos in GroMo Academy. They're free and actually useful.

- Pick one product. Start with Kotak 811 or SBI Credit Card they convert well.

- Send your link to friends, family, WhatsApp groups.

- When they apply and get approved, you get paid. Immediately.

A rough schedule that works:

- Week 1: Savings accounts only. Easy to sell, fast approvals.

- Week 2–4: Add credit cards.

- Month 2: Loans and demat accounts.

- Month 3: Start referring other agents to earn from their sales too.

Top partners don't overthink it. They send 3 WhatsApp status updates a day. They message 10 people personally. They follow up. That's the whole secret.

Who Is This For?

Everyone.

Students have free time and a network of other students. Housewives have community groups and neighborhood contacts. Salaried professionals have colleagues. Business owners have customers. Retired people have decades of relationships.

If you have a phone and you know people, you can do this.

Mistakes That Kill Your Progress

- Selling too many products at once. Pick two. Learn them inside out.

- Pitching the wrong thing to the wrong person. Don't sell a business loan to a salaried employee.

- Quitting after 3 "no"s. It's a volume game.

- Skipping the training. The scripts work.

- Waiting to feel "ready." You won't. Just start.

What's the Best Business for YOU?

If you have cash and want to build something physical, go franchise or cloud kitchen.

If you have skills and patience, freelance or create content.

But if you want to make money this week, without spending a rupee, and without quitting your job financial product distribution is the best bet on this list.

60 lakh people are already doing it. They've earned over ₹100 crores total. The app is built. The products are ready.

Your first ₹10,000 could be two days away. Your first ₹1 lakh month could be three months away.

Or you could keep thinking about it. Up to you.

Frequently Asked Questions

Q: Can I really start a business with zero investment in 2026? A: Yes. Financial product distribution needs no capital, just a phone. You earn ₹350–₹2,400 per sale instantly. Freelancing and content creation are also low-cost, but they require skills. Financial distribution is the only one that's truly zero-risk financially.

Q: How long until I make ₹1 lakh/month? A: Most serious partners hit that in 3–6 months. Month one usually sees ₹20K–40K if you're consistent. By month three, you understand who needs what and your income scales.

Q: Do I need qualifications? A: No degree needed. The app gives you free certification training in a few hours. That's enough to start.

Q: Which business has the highest margin? A: Digital services. Financial distribution is 100% margin on commissions (no costs). Freelancing is 70–90%. Physical products like food or retail are 20–40% after expenses.

Q: Can I do this with a full-time job? A: That's how most people start. 1–2 hours a day. WhatsApp messages during lunch. Follow-ups in the evening. No meetings, no fixed hours.

Q: What about failure risk? A: Traditional businesses fail 70–80% of the time because they run out of cash. With zero-investment models, you can't lose money. You just might not make as much as you hoped. That's a very different kind of risk.