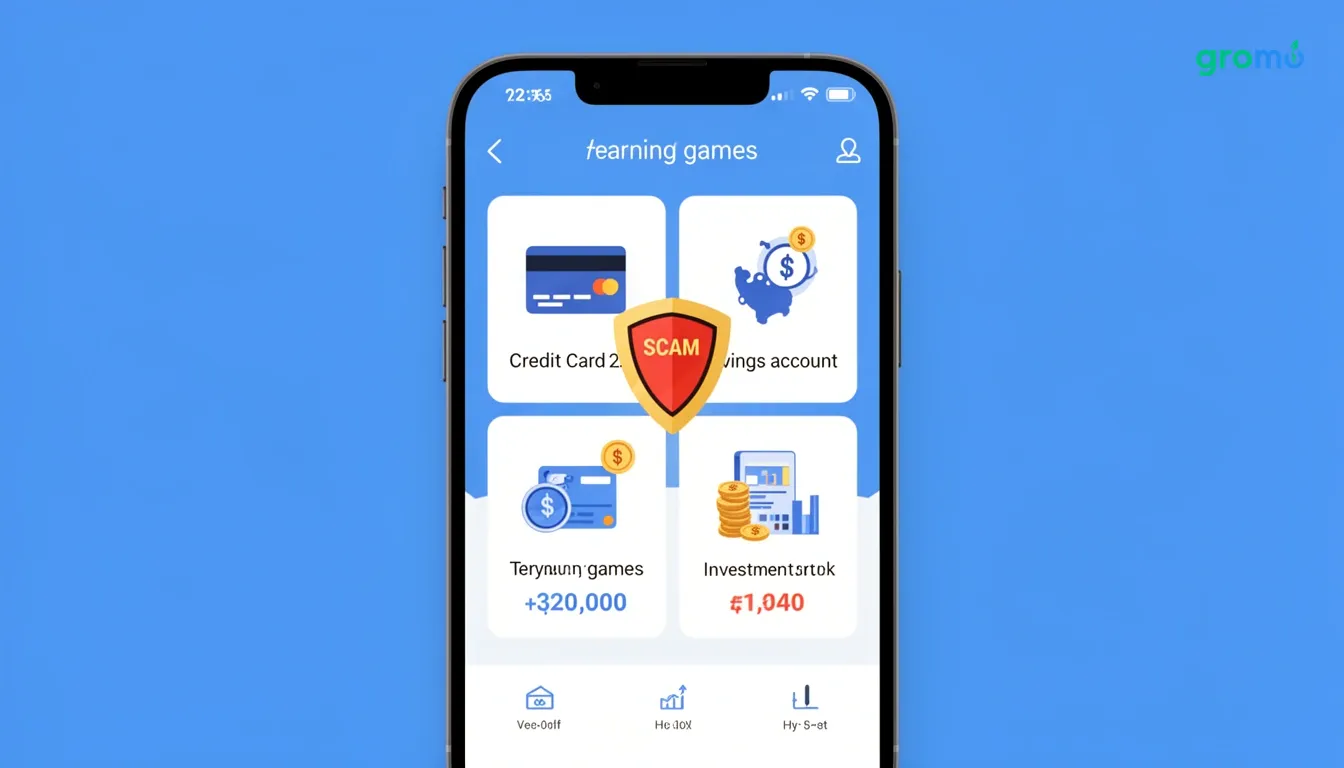

Why Earning Games Scam You & How to Earn Real Money in 2026

The internet is flooded with "earning games" that promise quick money spin a wheel, play a puzzle, watch ads, and supposedly earn real cash. If you've searched for "online earning money games," you've likely seen countless apps claiming you can make ₹500-₹1000 daily just by playing games on your phone. However, most people discover too late that these games rarely deliver on their promises. Even when they do pay out, the earnings are minimal compared to the time invested.

Consider this: while you're watching 50 ads to earn ₹5, there are people in India earning ₹10,000-₹1,00,000 monthly through legitimate online platforms. They aren't spinning lucky wheels or matching colored candies. They're leveraging actual business models instead of gamified engagement traps designed primarily to harvest your attention and data.

The reality behind money-earning games in 2026

Before exploring real alternatives, let's understand what's actually happening with most earning games. These apps operate on a simple economic principle: your attention is worth money to advertisers, and the app keeps the lion's share of that value.

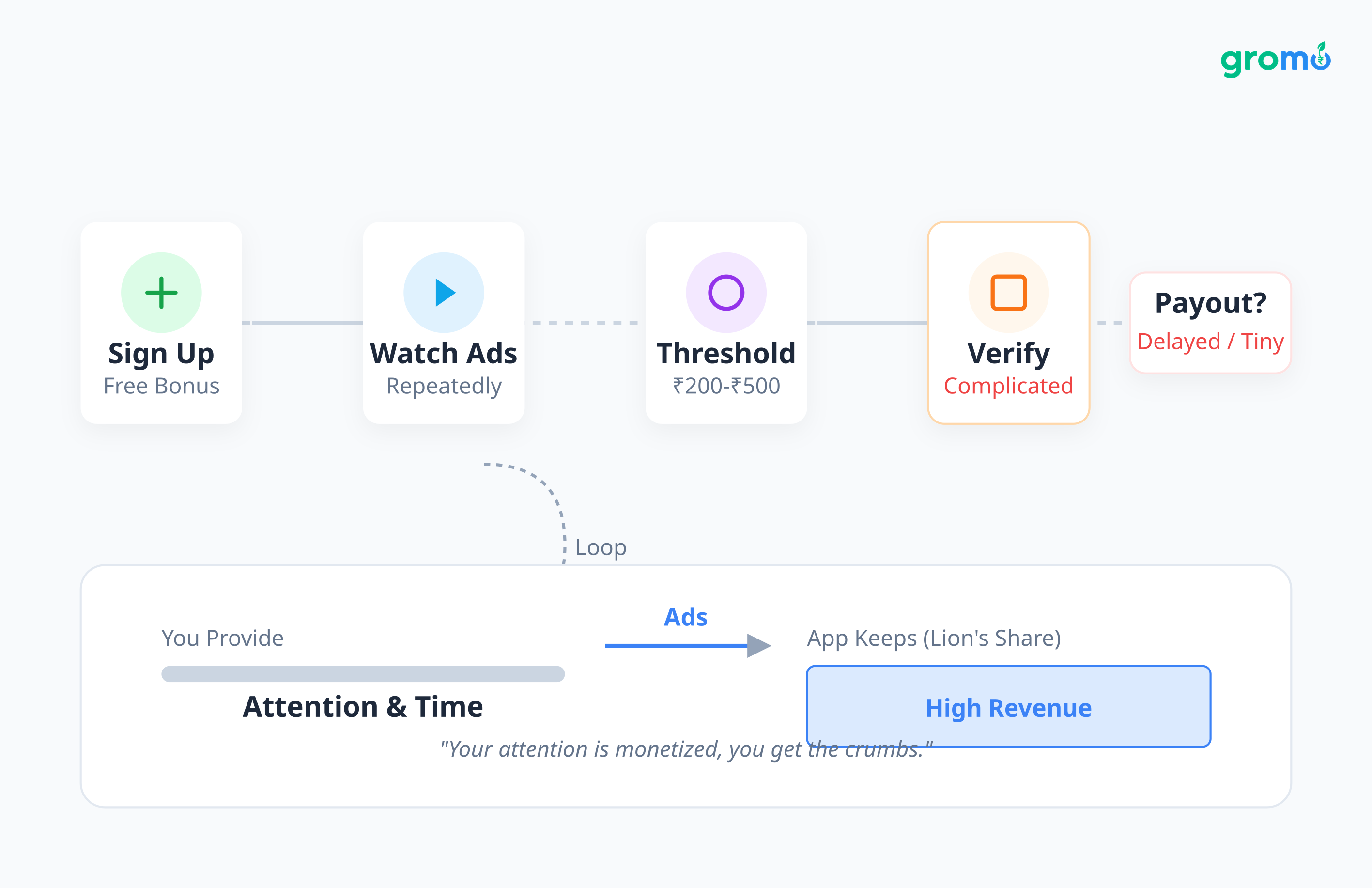

Here's how the typical money game works:

The user experience:

- Download a game promising ₹100 signup bonus

- Complete tasks, watch 30-second video ads repeatedly

- Accumulate points or virtual currency

- Reach a withdrawal threshold (often ₹200-₹500)

- Face complicated verification processes

- Wait days or weeks for tiny payouts (if they arrive at all)

The economic reality:

- Average earning: ₹2-₹15 per hour of active engagement

- Withdrawal threshold designed to maximize ad views before payout

- Many users never reach minimum withdrawal amounts

- Apps frequently change payout rates or shut down

A study of 50+ popular earning games in India found that the average hourly return was ₹8.50 far below minimum wage. More concerningly, 68% of users who reached withdrawal thresholds reported payment delays, reduced payouts, or account suspensions.

Why people search for earning games (and what they actually need)

Understanding why someone searches "online earning money game" reveals what they're truly looking for:

- Zero investment requirement – Can't afford to put money upfront

- Work from home flexibility – Need to earn around family or job commitments

- Simple, mobile-first interface – Want something easy to use on their smartphone

- Quick onboarding – Don't want complicated registration or training

- Instant gratification – Desire to see earnings accumulate immediately

The problem? Earning games satisfy these surface-level needs while failing at the fundamental requirement: meaningful income generation.

What if there was a platform that delivered all five benefits above but actually paid you real money not ₹5 after watching 100 ads, but ₹500-₹2,000 per successful transaction?

The financial product distribution alternative: real business, real earnings

Instead of playing games designed to extract maximum ad views from you, consider becoming a financial product distributor. This is exactly what platforms like GroMo enable you help people in your network get credit cards, savings accounts, loans, or investment products they genuinely need, and you earn substantial commissions for each successful transaction.

How this works in practice

Let's compare two scenarios using the same amount of time and effort:

Scenario A: Money-earning game

- Time investment: 3 hours daily

- Activities: Watching ads, completing surveys, playing puzzle games

- Monthly earnings: ₹750-₹1,500

- Withdrawal hassles: High

- Skill development: None

- Business asset created: None

Scenario B: Financial product distribution (GroMo)

- Time investment: 3 hours daily

- Activities: Sharing product recommendations with your network, helping them apply

- Monthly earnings: ₹10,000-₹1,00,000 (based on sales volume)

- Withdrawal process: Instant transfer to bank account (minimum ₹100)

- Skill development: Sales, financial product knowledge, customer relationship management

- Business asset created: Growing customer base generating repeat business

The fundamental difference? One is designed to keep you playing for negligible returns. The other is an actual commission-based business model used by 60 lakh+ partners across India who've collectively earned ₹100 crores.

Breaking down the financial distribution model

If earning games are the "illusion of income," financial product distribution is the substance. Here's exactly how it works:

Step 1: Product selection

Instead of playing games, you browse a catalog of financial products from recognized brands Axis Bank, Kotak, Bajaj Finserv, Upstox, and others. These are products people already need and search for: credit cards, personal loans, savings accounts, demat accounts.

Step 2: Customer identification

Think about your existing network friends, family, colleagues, neighbors. Someone is looking to improve their credit limit, someone needs a business loan, someone wants to start investing. Instead of sending them a game link, you share a legitimate financial product that solves their problem.

Step 3: Smart sharing

Modern platforms provide you with a unique referral link for each product. Share this via WhatsApp with a personalized message. The customer clicks, completes their application directly with the bank or financial institution (not you handling their documents), and you track the status in real-time within your app.

Step 4: Automatic commission credit

When the customer gets approved and completes the required action (card dispatch, account activation, loan disbursal), your commission is automatically credited. Unlike earning games with their arbitrary "coin conversion rates," these are real rupees ₹500 for a Kotak savings account, ₹1,000 for certain credit cards, ₹2,400 for premium products like SBI Credit Cards.

Step 5: Instant withdrawal

Once your wallet reaches ₹100 (significantly lower than most earning game thresholds), transfer money directly to your bank account instantly, not after weeks of verification drama.

The numbers that actually matter

Let's be specific about earning potential, because vague promises are exactly what earning games thrive on:

Product-wise commission structure (April 2026 rates):

| Product Category | Example Products | Commission Range | Customer Effort |

|---|---|---|---|

| Credit Cards | Axis Bank, HDFC, SBI | ₹500 - ₹2,400 per card | Medium - High (VKYC required) |

| Savings Accounts | Kotak 811, IndusInd | ₹300 - ₹500 per account | Low (fully digital) |

| Demat Accounts | Upstox, Angel One | ₹300 - ₹600 per account | Medium |

| Personal Loans | Various lenders | ₹500 - ₹3,000 per loan | High |

| Business Loans | MSME-focused products | ₹2,000+ per loan | Very High |

| Investment Products | Fixed Deposits | ₹200 - ₹1,000+ | Low - Medium |

Realistic monthly earnings scenarios:

Conservative approach (part-time, 1-2 hours daily):

- 5 credit card sales (₹1,000 average) = ₹5,000

- 3 savings account referrals (₹400 average) = ₹1,200

- 2 demat account referrals (₹450 average) = ₹900

- Monthly total: ₹7,100

Moderate approach (dedicated effort, 3-4 hours daily):

- 15 credit card sales = ₹15,000

- 10 savings accounts = ₹4,000

- 5 demat accounts = ₹2,250

- 2 personal loans = ₹1,000

- Monthly total: ₹22,250

Aggressive approach (full focus with team building):

- 30+ credit card sales = ₹30,000+

- 20+ savings accounts = ₹8,000+

- 10+ demat accounts = ₹4,500+

- 5+ loans = ₹2,500+

- Referral commissions from team = ₹5,000+

- Monthly total: ₹50,000+

Compare these numbers to earning ₹10-₹15 daily from games, and the difference becomes starkly clear.

Why this works better than earning games: the psychology and economics

1. Solving real problems Earning games create artificial tasks (watch this ad, spin this wheel) that serve only the app's business model. Financial product distribution connects people with solutions they're already searching for better credit cards, higher-interest savings accounts, investment opportunities.

2. Relationship-based, not extraction-based Games extract maximum engagement for minimum payout. Distribution builds long-term customer relationships. Someone you help get their first credit card will come back when they need a loan, investment advice, or want to open a business account.

3. Legitimate business development Every sale you make builds skills communication, understanding financial products, objection handling, follow-up discipline. You're building a real business asset. Games build nothing except perhaps faster finger-tapping reflexes.

4. Economic sustainability Banks and financial institutions have genuine customer acquisition costs ranging from ₹800-₹3,000. They're willing to share a portion of this with effective distributors. This creates sustainable economics. Earning games depend on venture funding or predatory ad models, which is why so many shut down or reduce payouts unexpectedly.

5. Success rate intelligence Advanced platforms now offer "success rate" indicators before you pitch a credit card to someone, you can check if they're likely to get approved based on their profile. This prevents wasted effort, something completely absent in the random luck mechanics of earning games.

Getting started: the practical roadmap

If you're ready to move beyond earning games to actual income generation, here's your step-by-step roadmap:

Week 1: Foundation

- Download a financial distribution platform (zero investment required)

- Complete the basic training modules (usually 2-3 hours of video content)

- Understand 3-4 flagship products thoroughly one credit card, one savings account, one investment product

- Set up your profile and personalized sharing tools

Week 2: First sales push

- List 20 people in your immediate network

- Identify which products match their likely needs

- Start conversations not sales pitches, genuine help

- Share your first 5-10 referral links

- Track applications in real-time

Week 3: Process refinement

- Analyze which products got the best response

- Follow up with pending applications

- Complete additional training on high-commission products

- Aim for 3-5 successful conversions

Week 4: Scale and systems

- Expand beyond immediate network using social media

- Create your sharing routine specific times for specific activities

- Join community groups or training sessions to learn from successful partners

- Target 10+ conversions for the month

Month 2 and beyond: Growth

- Build a referral team (some platforms offer team-building incentives)

- Specialize in 2-3 high-commission product categories

- Develop customer management habits reminders for follow-ups, cross-sell opportunities

- Set and track monthly income goals

Common objections (and honest answers)

"But I have no sales experience"

Neither did 60 lakh+ people who started. Modern platforms provide complete training recorded courses, live sessions, product specialists who answer questions. You're learning while earning. Plus, you're not doing cold sales; you're helping people you know with products they need.

"Won't people think I'm just trying to make money off them?"

Only if you approach it that way. If your friend needs a credit card and is about to apply directly through a bank's website, why shouldn't they use your link so you earn a commission? They get the same product, same terms, same approval process. You get paid for facilitating the connection. That's legitimate business.

"What if products don't get approved?"

That's exactly why success rate tools exist. Before sharing a premium credit card requiring ₹50,000 monthly income, you can check eligibility. Share products people actually qualify for. No approval = no commission, but also no wasted effort if you're strategic.

"Isn't this like those MLM schemes?"

No. MLM requires buying inventory, recruiting aggressively for your primary income, and often promotes products people don't genuinely need. Financial distribution has zero investment, commissions come primarily from direct sales (not recruitment), and you're sharing products from established banks and financial institutions that people actively search for.

"How is this different from affiliate marketing?"

It's a form of affiliate marketing, but specifically for high-commission financial products with built-in support systems. Generic affiliate marketing requires website building, SEO knowledge, and driving traffic. Financial distribution platforms give you the app infrastructure, training, customer management tools, and lead tracking everything built in.

The gamification that actually helps you earn

Interestingly, legitimate financial distribution platforms have borrowed the engaging elements from earning games but aligned them with real income generation.

For instance, GroMo runs the GroMo Premier League (GPL) a two-month contest during IPL season where your sales activities earn "runs" for IPL teams. Daily prizes (₹1,000 for top performers), impact player rewards, and team competitions make the work engaging. But here's the crucial difference: the gamification layer sits on top of real commission earnings, not instead of them.

You're earning ₹1,000+ per credit card sale AND competing for daily prizes. The game mechanics enhance the experience; they don't substitute for actual income.

Making the mental shift: from player to entrepreneur

The hardest transition isn't technical it's psychological. Earning games feel comfortable because they require minimal responsibility. Click, watch, collect tiny amounts. The risk is zero because the investment (your time) feels free.

Building a commission-based income stream requires a different mindset:

- You're building a business, not passing time

- Results vary based on effort, not on luck or algorithms

- You develop real skills that compound over time

- Initial earnings might be modest but grow as you improve

- You own customer relationships that generate repeat income

This shift from passive consumer to active entrepreneur is what separates people earning ₹500 monthly from games versus ₹50,000 monthly from distribution.

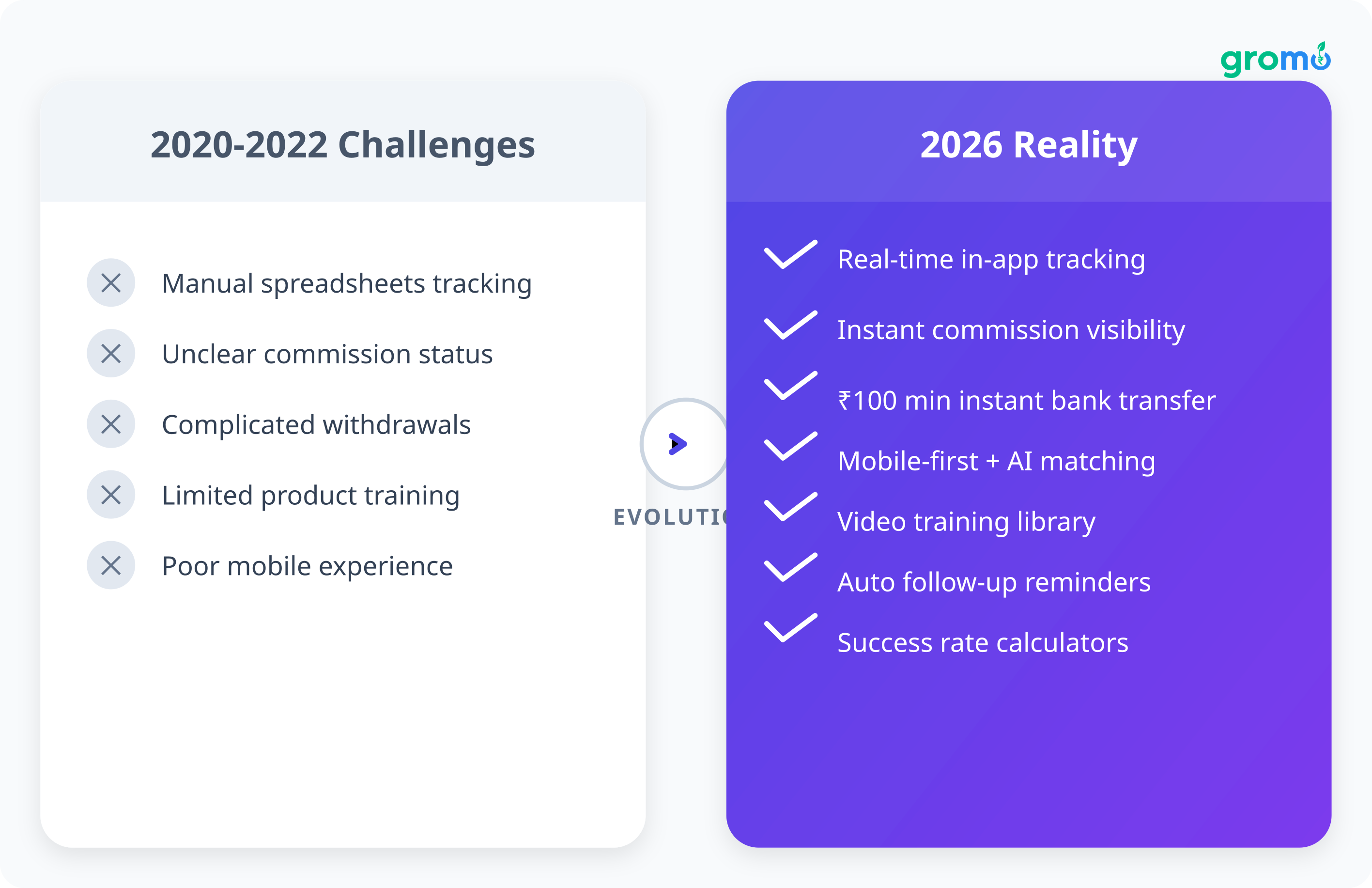

Technology advantages in 2026

If you tried financial product distribution years ago and found it cumbersome, the technology has transformed dramatically:

2020-2022 challenges:

- Manual lead tracking via spreadsheets

- Unclear commission status

- Complicated withdrawal processes

- Limited product training

- Poor mobile experience

2026 reality:

- Real-time lead tracking in-app

- Instant commission visibility

- ₹100 minimum withdrawal with instant bank transfer

- Comprehensive video training library

- Mobile-first platforms with AI-powered customer matching

- Success rate calculators

- Automated follow-up reminders

- Personalized marketing content generation

The user experience is now genuinely comparable to well-designed earning games just with payouts that are 50-100x higher per hour invested.

The compound effect: why time favors this model

Here's what happens over 12 months with each approach:

Earning games (12 months):

- Month 1: ₹800

- Month 6: ₹850 (slightly better at playing)

- Month 12: ₹900

- Total earned: ₹10,200

- Skills gained: None

- Business asset: None

Financial distribution (12 months):

- Month 1: ₹3,000 (learning phase)

- Month 3: ₹8,000 (finding rhythm)

- Month 6: ₹15,000 (established process)

- Month 9: ₹25,000 (referral team kicking in)

- Month 12: ₹35,000 (mature customer base with repeat business)

- Total earned: ₹2,10,000+

- Skills gained: Sales, financial product knowledge, customer management

- Business asset: Database of 200+ customers generating ongoing opportunities

The trajectories aren't even comparable. One is flat; the other compounds.

Specific product strategies for fast results

If you're making the switch from earning games to distribution, start with these high-conversion, beginner-friendly products:

Priority product #1: Zero-balance savings accounts

- Why: Fully digital, no documentation hassles, almost everyone qualifies

- Best options: Kotak 811, IndusInd

- Commission: ₹300-₹500

- Pitch: "Open account entirely from phone, no branch visit, no minimum balance"

- Target: Students, gig workers, anyone frustrated with traditional banks

Priority product #2: Entry-level credit cards

- Why: High demand, straightforward process, decent commissions

- Best options: Look for cards with instant digital verification

- Commission: ₹600-₹1,000

- Pitch: "Check eligibility in 30 seconds, approved cards delivered in 7 days"

- Target: Young professionals, people building credit history

Priority product #3: Investment products (fixed deposits)

- Why: Safety-conscious Indians love FDs, simple concept, low risk

- Best options: High-interest FDs from small finance banks (8-9% rates)

- Commission: ₹200-₹1,000 depending on deposit amount

- Pitch: "₹9.1% interest vs bank's ₹6.5% same safety, better returns"

- Target: Risk-averse savers, retirees, people with lump sum amounts

Master these three categories first. Once you consistently close 10+ deals monthly, expand into personal loans and premium credit cards with higher commissions.

The social proof that matters

Earning games advertise millions of downloads. But downloads are free and meaningless. What matters is actual money paid out to actual people.

Financial distribution platforms like GroMo can demonstrate tangible proof: ₹100 crores paid out to 60 lakh+ partners. That's verifiable, significant money reaching real bank accounts. Individual success stories include teachers earning ₹40,000 monthly as side income, college students making ₹15,000 during semester breaks, and homemakers building ₹60,000+ monthly income streams.

Before committing time to any platform whether earning game or distribution network demand proof of actual payouts, ideally with a transparent partner community where you can verify claims.

Your 30-day challenge

If you're currently spending 1-2 hours daily on earning games, here's a direct challenge:

For the next 30 days:

- Stop all earning games completely

- Invest that same time into learning and executing financial product distribution

- Set a target of 5 successful sales/referrals

- Track your total earnings

Predicted outcome:

- Earning games (30 days): ₹300-₹600

- Distribution (30 days with 5 sales): ₹2,500-₹5,000

That's 5-10x more money for the same time investment. And unlike earning games where month 2 looks identical to month 1, your distribution income in month 2 will likely be higher as you improve.

If after 30 days you've genuinely tried and distribution doesn't work for you, you can always go back to earning games. But give the real business model a fair shot before dismissing it.

Frequently asked questions

Q: Do I need to invest money to start financial product distribution?

A: No. Legitimate platforms like GroMo require zero investment. You don't buy inventory, pay membership fees, or purchase starter kits. You download a free app, complete free training, and start earning commissions on sales. If any platform demands upfront payment, that's a red flag.

Q: How long does it take to receive commission payments?

A: With modern platforms, commissions are credited to your in-app wallet immediately upon sale confirmation (customer approval, card dispatch, account activation, etc.). Once your wallet reaches the minimum threshold (₹100 on GroMo), you can instantly transfer to your bank account no waiting weeks like with earning games.

Q: What if I don't know anyone who needs financial products?

A: You probably know more potential customers than you think. Most Indian adults need credit cards, savings accounts, or investment options. Start with immediate family and close friends, then expand to social media connections and community groups. Platforms also provide bonus customer leads to eligible partners who demonstrate consistent effort.

Q: Is this legal, and are there any compliance issues I should worry about?

A: Yes, it's completely legal. You're acting as a referral partner for banks and financial institutions a standard distribution model. The financial institutions handle all regulatory compliance, KYC verification, and documentation. You simply facilitate the connection. Ensure you're working with a legitimate platform that partners with licensed banks and NBFCs.

Q: Can I do this alongside my full-time job?

A: Absolutely. Many successful partners treat this as side income, investing 1-2 hours daily during commute time, lunch breaks, or evenings. The flexible model means you work when convenient. Start part-time, and if earnings grow substantially, you can decide whether to scale up or continue as supplemental income.

Q: How is this different from becoming a bank DSA (Direct Selling Agent)?

A: Traditional DSA models often require significant investment (₹50,000-₹2,00,000), involve complex agreements, and demand full-time commitment. Modern financial distribution platforms are completely digital, zero-investment, and designed for part-time participants. You get similar commission structures with none of the traditional barriers to entry.