Start Earning ₹50K+ Monthly with Zero Investment in 2026

start-earning-50k-monthly-zero-investment-2026

The gig economy in India has gotten big. You're probably here because you want to make extra money without quitting your job could be you're a student, working professional, at home during the day, running something already. The digital shift has created options that simply didn't exist ten years ago.

Here's what most guides won't mention: most side hustles need upfront money, inventory, or skills you might not have. Financial product distribution is different because you can start fairly quickly, with zero investment, while keeping your current job.

What's actually happening

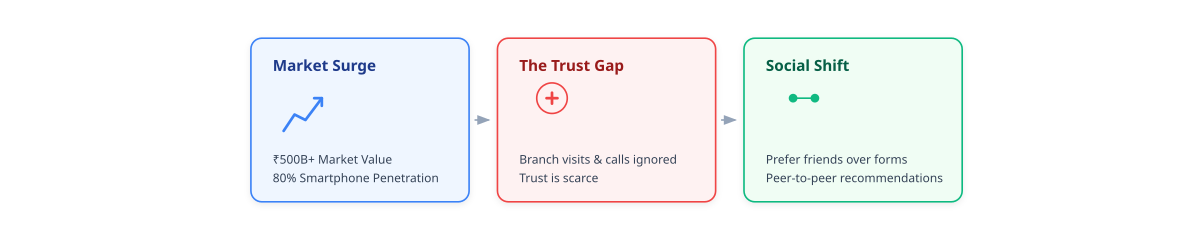

India's digital financial services market crossed ₹500 billion in 2026. Smartphone penetration sits around 80%. Financial literacy is creeping up. People are looking for credit cards, savings accounts, loans, investment options.

Two things are colliding at once.

Banks can't reach people the old way. Branch visits are down. Cold calls get ignored. Unknown numbers don't get picked up.

Trust has become scarce. When someone needs a credit card or loan, they'd rather talk to someone they know a friend, cousin, colleague than fill out a form after a random phone call.

This gap is where individual distributors fit. You become the bridge.

What you can earn

Credit cards run ₹200 to ₹1,000+ per successful card. Savings accounts: ₹50 to ₹500. Demat/trading accounts: ₹300 to ₹1,200. Personal loans: 0.5% to 2% of the loan amount. Business loans: 1% to 3% of sanctioned amount.

Help 10 people get credit cards in a month and you're at ₹5,000 to ₹10,000. Add loan applications, demat accounts, maybe a business loan or two. That's ₹30,000 to ₹50,000 monthly territory. People who treat this like an actual business not an experiment regularly cross ₹1 lakh.

The difference between ₹10,000 and ₹1 lakh isn't luck. It's consistency.

Why there's no investment needed

Most business ideas have catch-22s. Buy inventory first. Rent space before you have customers. Spend on ads before you know what works.

This is different. You need a smartphone, internet, and time. That's genuinely it. No inventory. No delivery logistics. No customer service after the sale. Financial institutions handle everything once you've made the connection.

Platforms like GroMo provide training, product links, customer tracking, and payouts. They make money when products get sold, so helping you succeed is aligned with their interests.

Who this works for

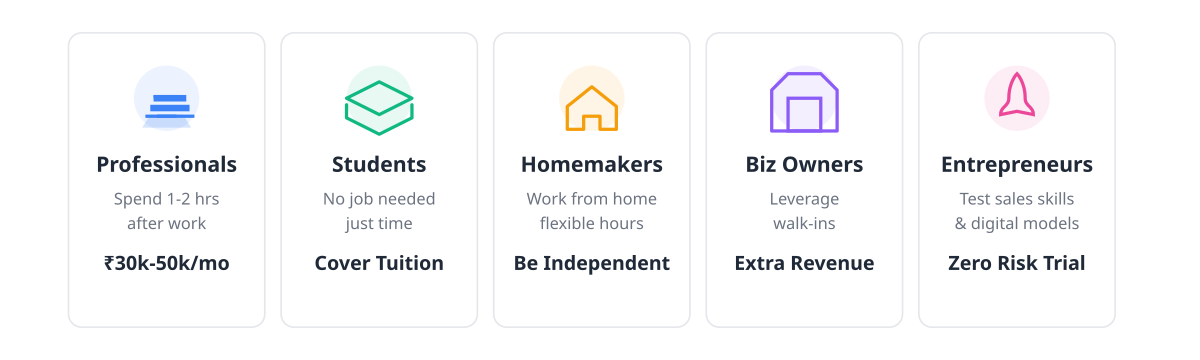

Working professionals can spend an hour or two after work and hit ₹30,000-₹50,000 monthly. Your network is already there.

Students often don't have job options but do have time. Some earn enough to cover tuition.

Homemakers can work from home with flexible hours. Financial independence without trading off family responsibilities.

Small business owners already have customers walking in. Offering financial products is an extra revenue stream.

Aspiring entrepreneurs can test sales skills, understand digital business models, and build a customer base without risking money.

How to actually start

Day one: sign up. Pick a platform with quick payouts (same-day or next-day, not 30-60 day cycles), multiple product categories, known financial partners, free training, and responsive support. Download the app, do your KYC with PAN and Aadhaar.

Days two and three: learn. Most platforms have training modules. Don't skip them. You need to understand what you're selling so you can answer questions without fumbling. Spend 2-3 hours. Some platforms offer certifications they help credibility but aren't necessary.

Day four: list prospects. Write down 20 people in your network who might need financial products. Friends starting jobs. Family thinking about investments. Colleagues comparing loan rates. Business owners who need working capital. Your first customers are people who already trust you.

Days five and six: reach out. WhatsApp, call, meet in person. Something simple: "I'm helping people get credit cards and loans through [Bank]. If you're looking, I can walk you through the application and make sure you get the current offers." Share the link. Follow up if they don't respond. Most people need a nudge.

Day seven: follow up. Applications get abandoned halfway all the time. Check status. Answer last-minute questions. Help them finish. Your involvement increases approval rates. Commissions usually land within 24-48 hours after approval.

Why people quit

I've seen enthusiastic starters quit in weeks.

Treating it like a lottery ticket. This takes consistent effort. An hour a day, most days, adds up.

Skipping training. If you can't explain the difference between two credit cards, conversations get awkward fast.

Being pushy. You're helping people find products that fit. Trust is everything. Lose it and you're done.

Not tracking. Notice which products convert, which messages work. Optimize. Don't just throw things at the wall.

Quitting too early. Month one might be ₹5,000. Month three could be ₹15,000 or more. The curve is real. Most people never see it because they leave early.

The long game

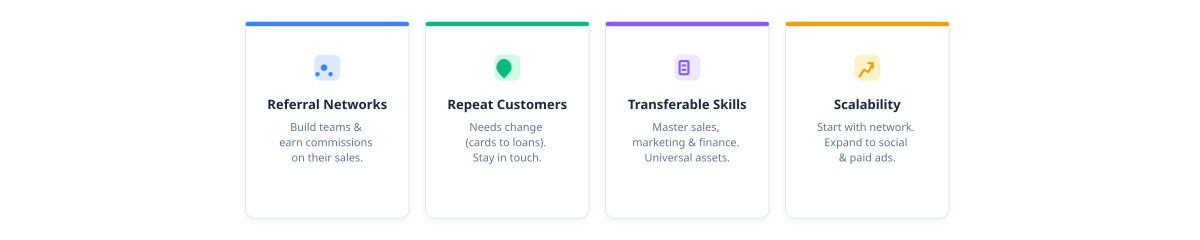

Referral networks. Some platforms let you build teams. When people you refer make sales, you get additional commissions. That's passive income starting.

Repeat customers. Someone who gets a credit card from you today might need a home loan in two years. Stay in touch.

Transferable skills. You're learning sales, digital marketing, financial products. These matter across careers.

Scalability. Start with your network. Expand to social media. Maybe content creation or paid ads later. Grows with your ambition.

Why 2026 is different

AI matching. Platforms suggest products based on customer profiles. You're not guessing.

Real-time tracking. Application status, approval rates, commissions all visible.

Automated marketing. Pre-made content, personalized landing pages, digital business cards. You don't design anything.

Fast payments. UPI integration means hours, not weeks.

Mobile-first. Everything on your phone. No laptop needed.

Is this worth your time?

Honest answer: this isn't passive income at the start. You work for what you earn.

But look at the alternatives.

Traditional part-time job: fixed hours, fixed pay, commute, capped earnings.

Delivery or ride-sharing: vehicle wear, fuel costs, physical strain, safety issues, earnings ceiling.

E-commerce or dropshipping: inventory headaches, returns, customer complaints, ad spend, platform fees eating margins.

Financial distribution: zero investment, flexible timing, uncapped earnings, skill development, no physical risk.

For most people wanting side income, the math works.

How to start today

Pick a platform GroMo is one verified option. Download the app, complete KYC with PAN and Aadhaar. Finish the training, 2-3 hours. Make your first pitch to someone you know.

Yesterday would've been better. Today works.