Earn ₹2,400 Per GroMo Credit Card Referral – Zero Investment

Referral money-earning apps let users earn commissions by sharing product links with their network. No upfront capital, no inventory, and payouts land directly in your bank account after every successful conversion. GroMo leads this category in India with instant payments, 80+ financial products, and ₹2,400 per credit card sale.

Traditional side hustles demand time blocks you don't have. Referral platforms flip that model: share a link during lunch, earn while you sleep, scale income by building a customer list you own. This guide explains how referral apps generate real money, which mechanics separate scams from legitimate platforms, and why financial-product distribution outearns cashback gimmicks by 20× in 2026.

How referral money-earning apps actually work

Referral money-earning apps operate on affiliate commission logic. You register for free, receive a unique tracking link for each product, and share it via WhatsApp, Instagram, or face-to-face conversations. When someone clicks your link and completes a qualifying action card approval, loan disbursal, demat account funding the brand pays the platform, and the platform credits your wallet.

GroMo processes this cycle in real time. You see lead status updates inside the Leads section, watch funding confirmations arrive, and withdraw earnings above ₹100 instantly. No monthly cheque cycles, no 45-day payment holds money moves the moment the bank confirms activation.

Three structural pillars separate working referral apps from time-wasters:

Commission transparency exact payout figures published per product, not vague "up to" promises

Zero joining fees legitimate platforms earn from brand partnerships, not recruiter deposits

Instant withdrawal thresholds ₹100 minimums instead of ₹5,000 lockups that trap small earners

Cashback apps pay ₹10–₹50 after you spend ₹500. Referral income apps pay ₹300–₹2,400 when your contact makes a decision they already needed. The unit economics favor referral models because brands assign higher customer-acquisition budgets to considered purchases than impulse transactions.

Top referral money apps in India that pay real cash

GroMo has India's fastest payout cycle and widest financial product catalog. Fourteen lakh active partners across 19,000 PIN codes earn from credit cards (SBI ₹2,400, HDFC Millennia ₹1,600), savings accounts (Kotak 811 ₹300), demat accounts (Upstox ₹600), personal loans (Fibe ₹2,000), and fixed deposits via Stable Money with zero convenience fees. The My Customers dashboard uses AI to recommend which product fits each contact's profile, so you pitch relevance, not randomness.

Google Pay, PhonePe, and Paytm run tactical referral campaigns ₹51 when a friend completes their first UPI transaction, ₹201 for bill payments during festival windows. These work for quick pocket money but cap total earnings because UPI saturation is 80%+ in urban India; your network already uses these apps. Conversion rates collapse after your first ten referrals.

Amazon Pay and Flipkart offer affiliate programs that reward product link shares. You earn 1–8% of order value, which sounds attractive until reality sets in: a ₹2,000 electronics sale nets you ₹40, while a single GroMo credit card referral pays ₹1,600–₹2,400 with no dependency on the customer's shopping cart size.

Freelance-platform referral schemes like Upwork and Fiverr pay you when referred users complete billable projects. Strong concept, weak execution payouts arrive only after the freelancer crosses revenue thresholds ($100–$500), timelines stretch to 60–90 days, and your ability to influence whether a stranger succeeds on the platform is zero.

EarnKaro and CashKaro aggregate cashback deals and pay you a share when referrals shop through their links. Middleman economics compress margins; you earn ₹5–₹15 per transaction because the platform already takes its cut from brand commissions before passing residuals to you.

Comparison snapshot:

Platform | Payout per Referral | Withdrawal Minimum | Payment Speed | Product Range |

|---|---|---|---|---|

GroMo | ₹300–₹2,400 | ₹100 | Instant | 80+ financial products |

Google Pay | ₹51–₹201 | ₹0 | 2–3 days | UPI, bill payments |

Amazon Associates | 1–8% of order | ₹1,000 | 60 days | E-commerce catalog |

EarnKaro | ₹5–₹50 | ₹100 | 7–10 days | Aggregated deals |

Upwork Referral | $100–$500 | $100 | 30–90 days | Freelance gigs |

Zero-investment business models thrive when high-ticket products meet low-friction sharing. Financial services hit both criteria everyone needs credit, savings, or loans, and sharing a link takes fifteen seconds.

Why financial-product referrals beat cashback apps 20×

Cashback apps incentivize spending you hadn't planned. Referral apps monetize decisions people already researched. That psychological difference explains why GroMo partners earn ₹10,000–₹1,00,000 monthly while cashback junkies scrape together ₹500 after dozens of transactions.

Average order value governs commission size. A Myntra cashback of ₹50 on a ₹2,000 dress represents 2.5% of transaction value. A Kotak 811 savings account referral pays ₹300 on a zero-rupee product because banks assign ₹800–₹1,200 customer-acquisition costs to new accounts. You capture one-third to half of that budget.

Repeat business mechanics separate sustainable income from one-time windfalls. Cashback expires once your friend buys the discounted toaster. Financial products unlock cross-sell loops the contact who opened a savings account qualifies for a credit card next month, then a personal loan in six months when they plan a wedding. GroMo's My Customers section surfaces these opportunities automatically, turning single transactions into annuity streams.

Time investment flips the cashback equation. Hunting ₹10 offers across five apps for an hour yields ₹50 ₹50/hour effective wage. Sharing one GroMo credit card link during a coffee chat earns ₹1,600 in fifteen minutes ₹6,400/hour effective rate.

Behavioral data from 14 lakh GroMo partners shows the top 10% earn 40× more than casual users. The difference isn't talent or connections it's treating referrals as commission-based business with customer lists, follow-up systems, and product-match logic, not random WhatsApp spam.

Step-by-step: Earning your first ₹1,000 in 48 hours via GroMo

Download the GroMo app from gromo.in and complete mobile-number verification. No documents required at signup KYC happens only when you withdraw, keeping onboarding friction at zero. The home screen loads your product catalog immediately; scroll to credit cards and tap "SBI Card."

Read the product brief in sixty seconds: SBI pays ₹2,400 per approval, requires Aadhaar + PAN, suits salaried customers with ₹25,000+ monthly income, and approves within 7–10 days. Tap "Share Link" to generate your unique tracking URL and copy it.

Open WhatsApp and message three contacts who mentioned needing a credit card in recent conversations. Paste the link with context: "You asked about reward cards last week this SBI option gives fuel discounts + lounge access. Takes 5 minutes to apply, no charges." Personalization doubles open rates compared to generic blasts.

When your contact clicks, they land on a GroMo co-branded page that collects basic details name, mobile, PAN, city and routes them to the bank's native application flow. Your Leads dashboard updates in real time: "Application started," "Documents uploaded," "Bank reviewing," "Approved," "Card dispatched."

Approval triggers instant commission credit. ₹2,400 appears in your GroMo Wallet within sixty seconds of dispatch confirmation. Tap "Withdraw," enter your bank account number and IFSC (stored for future payouts), and funds hit your account in 2–4 hours via IMPS.

Scale the model by adding five new contacts daily to your customer list. GroMo's AI recommends which product suits each profile students get Fi Money accounts, freelancers see OneCard, business owners receive Tide offers. Relevance lifts conversion from 5% (spray-and-pray) to 25% (targeted matching).

Red flags that expose fake referral apps

Upfront registration fees signal pyramid schemes, not referral platforms. Legitimate apps earn by taking spreads from brand payouts if they demand ₹500 "activation charges" or ₹2,000 "premium membership," the business model is recruiting you, not serving brands.

Vague commission structures hide unpayable earnings. "Earn up to ₹50,000 monthly" without product-wise payout tables means the platform manipulates rates post-facto. GroMo publishes exact figures ₹2,400 for SBI Card, ₹600 for Upstox, ₹300 for Kotak 811 so you calculate income before investing time.

Withdrawal minimums above ₹5,000 trap small earners in perpetual accumulation. By the time you hit the threshold, the app folds or changes terms. GroMo's ₹100 floor lets part-time users withdraw weekly, testing platform reliability before scaling effort.

Gaming mechanics disguised as income spin wheels, scratch cards as primary revenue, ad-watching tasks monetize your attention, not your referrals. Money-earning games pay ₹2–₹5 per hour because advertisers fund those pennies, and advertiser budgets cap at ₹10 per user. Financial-product commissions come from ₹1,200–₹3,000 acquisition budgets, completely different economics.

Delayed payout horror stories litter Google Play reviews for marginal apps "Withdrawal pending 90 days," "Customer care not responding," "Account suspended without reason." Check one-star reviews before joining any platform; patterns repeat across scams.

Tax, legal, and compliance realities for referral income

Referral commissions classify as "income from other sources" under Section 56 of the Income Tax Act. You report annual earnings in your ITR-1 or ITR-2, and if total income exceeds ₹2.5 lakh (₹3 lakh for senior citizens), you pay tax at slab rates. GroMo doesn't deduct TDS because payments go to individuals, not businesses, but you're responsible for declaring earnings.

PAN linking becomes mandatory when cumulative withdrawals cross ₹50,000 in a financial year. The app prompts you to submit PAN details before processing the transaction this isn't overreach, it's RBI's Know Your Customer (KYC) protocol that applies to all digital wallets and payment aggregators.

GST registration isn't required for individual referral partners. You're acting as a commission agent, not a service provider issuing invoices, so the 18% GST burden doesn't apply unless you incorporate as a business entity and cross ₹40 lakh annual turnover (₹20 lakh in special-category states).

Bank account verification happens at first withdrawal. GroMo requests account number, IFSC, and beneficiary name matching your registered mobile number to comply with RBI's digital lending guidelines. This prevents money laundering and ensures payouts reach legitimate users, not mule accounts.

IRDAI licensing isn't required for financial product distribution via GroMo. The platform holds institutional partnerships with banks and NBFCs; you're sharing pre-approved links, not underwriting credit or collecting applications manually. Insurance sales previously required IRDAI certification, but GroMo no longer offers insurance products, so that barrier doesn't apply to current partners.

Advanced strategies: Scaling from ₹10K to ₹1L monthly

Customer segmentation multiplies conversions without increasing reach. Tag contacts by life stage college students need demat accounts for first investments, young professionals want travel credit cards, parents aged 35–50 seek education loans. Send Upstox links to the first group, HDFC Millennia to the second, and Fibe personal loans to the third. GroMo's product filters let you save these segments as lists inside My Customers, automating match logic.

Success Rate scoring eliminates wasted pitches. Green indicators flag customers with 70%+ approval probability based on their profile data income bracket, city, existing credit history. Focus on green-rated leads first; you'll close 4× more deals per 100 conversations than scattering effort across red and yellow profiles.

Referral program layering adds ₹10,000 per recruit. GroMo pays up to ₹10,000 when you refer another partner who hits sales milestones: ₹100 at first sale, ₹1,000 at Gold tier, ₹1,500 at Platinum, ₹7,400 at Elite. Build a five-person team, guide them through free training webinars, and your monthly income includes both direct commissions and recruitment bonuses.

Content-led distribution beats link dumping by 6×. Record a 60-second Instagram Reel explaining "3 credit cards for online shopping cashback," embed your GroMo link in bio, and watch passive clicks roll in. WhatsApp Status updates work similarly post a screenshot of your latest ₹2,400 payout with caption "Earned this by sharing one link," and curiosity drives inbound questions.

Cross-sell automation converts one-time buyers into ₹15K lifetime value. After a contact opens a Kotak 811 account (₹300 earned), GroMo's AI suggests pitching an Upstox demat account (₹600) the following month, then an SBI credit card (₹2,400) after three months. Sequence these touches in your calendar customer lifetime value jumps from ₹300 to ₹3,300 with three conversations spread over 90 days.

Elite GroMo partners track five metrics weekly: leads shared, conversion rate, average payout per lead, customer reactivation rate, and referral-program earnings. What gets measured gets managed spending thirty minutes on Sunday reviewing these numbers identifies which products to push harder and which contacts need follow-up nudges.

Comparing GroMo to peer referral platforms feature-by-feature

GroMo's instant payout infrastructure beats 90% of competitors. Most affiliate networks batch payments weekly or monthly; GroMo credits your wallet within sixty seconds of lead conversion and lets you withdraw above ₹100 anytime. Cash flow flexibility matters when you're scaling waiting 30 days for a ₹10,000 payout locks working capital that could fund WhatsApp Business API subscriptions or paid ads.

Product diversity separates distribution businesses from single-trick platforms. GroMo offers 80+ products across eight categories credit cards, savings accounts, demat accounts, loans, credit lines, FDs, neobanking cards, and bill-payment cashback. Compare that to PhonePe's referral program (UPI signups only) or Groww's affiliate scheme (investment products only). Narrow catalogs exhaust your network in weeks; wide selection keeps conversations fresh for years.

Training infrastructure determines partner success rates. GroMo Academy runs daily webinars in Hindi, English, Tamil, Telugu, and Bengali covering product knowledge, objection handling, and digital marketing tactics. Attendance earns GroMo Coins redeemable for premium features. Competitors hand you a link and expect magic; GroMo builds competence systematically.

Customer-management tools distinguish professional operations from hobby-level sharing. GroMo's AI recommends products per contact, sets follow-up reminders, tracks application status in real time, and flags cross-sell opportunities. You get a CRM embedded in the referral app most alternatives offer a dumb link shortener and call it a "platform."

Elite referral tiers unlock higher payouts as you prove volume. Hit Gold (₹50,000 total earnings) and GroMo grants access to exclusive products with ₹3,000–₹5,000 commissions. Platinum and Elite tiers follow at ₹1,00,000 and ₹2,00,000 cumulative earnings, each unlocking premium rates and dedicated partner managers. Flat-rate platforms cap your income growth regardless of performance.

Network effects through team building let you earn from others' sales. GroMo's refer-a-partner program pays milestone bonuses when recruits hit sales targets up to ₹10,000 per successful referral. Traditional affiliate programs pay you only for your direct sales; multi-tier commission structures multiply income without multiplying your hours.

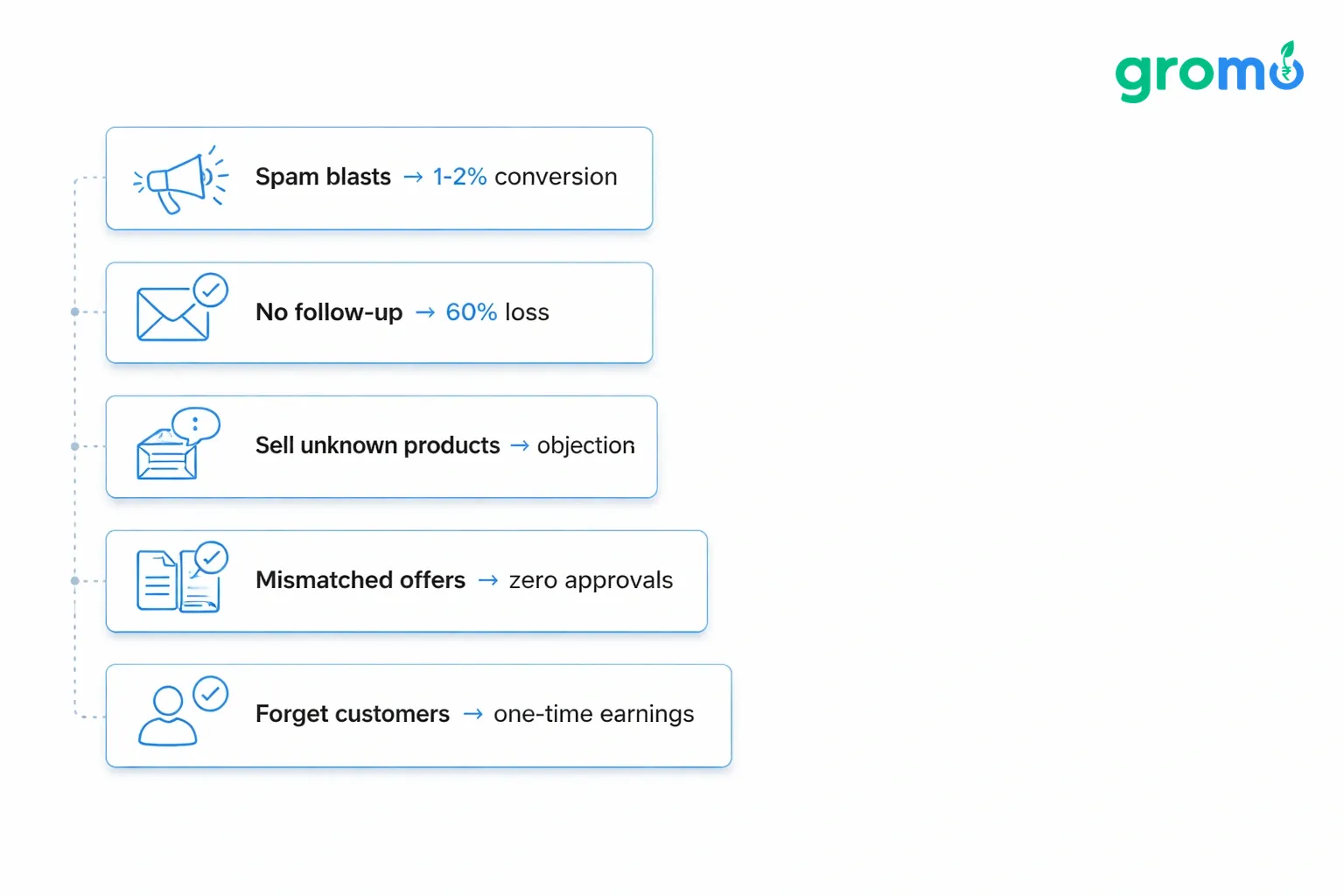

Common mistakes that kill referral earnings

Generic link blasts to 100 WhatsApp contacts produce 1–2% conversion. Recipients flag you as spam, mute your Status updates, and ignore future shares. Personalized one-on-one messages with context "You mentioned credit card interest rates last week; this option has 0% forex markup for your Dubai trip" convert at 20–30% because you're solving a stated problem.

Ignoring follow-up kills 60% of potential earnings. Someone clicks your link, starts the application, gets distracted, and forgets. GroMo's Leads dashboard shows which contacts dropped off at which stage document upload, address verification, video KYC. A simple nudge message "Saw your SBI Card application is 80% done, need help with the video KYC step?" recovers 40% of abandoned leads.

Selling products you don't understand breeds objections you can't answer. Spend fifteen minutes reading each product brief in the GroMo app before sharing links. Know eligibility criteria, approval timelines, fees, and top benefits. When your contact asks "What's the joining fee?" and you fumble, credibility evaporates and the sale dies.

Chasing high payouts without matching customer profiles wastes time. The ₹2,400 SBI Card requires ₹25,000+ monthly income pitching it to college students yields zero approvals. The ₹300 Kotak 811 account has near-universal eligibility but lower payout. Match product to profile using GroMo's Success Rate feature; green-lit leads close 4× faster than yellow or red.

Neglecting the customer database turns you into a one-hit vendor. After earning ₹1,600 from a friend's credit card signup, most beginners move to the next contact and forget the first. Elite partners revisit each customer quarterly with new offers demat accounts, FDs, personal loans building ₹10,000–₹15,000 lifetime value per relationship instead of ₹1,600 one-time income.

Real income benchmarks: What GroMo partners actually earn

Beginner tier (first 30 days): ₹3,000–₹8,000. New partners typically convert 2–3 credit card leads and 3–5 savings accounts from immediate family and close friends. Total effort: 10–15 hours spread across the month, effective rate ₹200–₹500/hour.

Intermediate tier (months 2–6): ₹15,000–₹40,000 monthly. Active partners expand to college networks, office colleagues, and social media followers. Weekly rhythm emerges 20 new leads shared, 4–6 conversions, 15 follow-up messages. Monthly time investment: 40–50 hours, effective rate ₹300–₹800/hour.

Advanced tier (months 7–12): ₹60,000–₹1,00,000 monthly. Top 5% partners build customer lists of 200–300 contacts, run Instagram/YouTube channels teaching financial literacy with embedded GroMo links, and recruit 5–10 sub-partners via the refer-a-partner program. Combined earnings from direct sales + team bonuses. Time investment stabilizes at 50–60 hours monthly as systems automate lead nurturing.

Elite tier (year 2+): ₹1,50,000–₹3,00,000 monthly. These outliers treat GroMo as primary income, manage teams of 20–50 partners, run paid Facebook/Google ads targeting "best credit card India" keywords, and leverage WhatsApp Business API for automated follow-ups. They've crossed ₹10,00,000 cumulative earnings and unlocked Platinum/Elite tier rates (₹3,000–₹5,000 per premium product).

Part-time bracket: ₹5,000–₹12,000 monthly. Working professionals and housewives dedicating 10–15 hours weekly share links during lunch breaks, family gatherings, and weekend meetups. Focus on credit cards and savings accounts yields consistent ₹300–₹2,400 payouts without disrupting primary commitments.

Geography plays minimal role tier 2/3 cities show similar earnings to metros because financial products have pan-India demand. A partner in Jaipur earns the same ₹2,400 SBI Card commission as a Mumbai counterpart; the product catalog and payout structure don't discriminate by PIN code.

Why GroMo outlasts fad apps and gig platforms

Business model durability matters more than viral growth. Money-earning games burn venture capital paying unsustainable ₹100 signup bonuses, acquire 10 lakh users in six months, then collapse when funding dries up. GroMo earns spreads from billion-dollar banks and NBFCs with 50-year operating histories the revenue source isn't going anywhere.

Regulatory moats protect GroMo's model. RBI-approved banks and SEBI-registered brokers can't sell directly to 1.4 billion Indians cost-effectively; they need distribution partners. GroMo aggregates that demand, vets partners through KYC processes, and provides compliance infrastructure banks trust. New entrants face 18–24 month partnership negotiations; GroMo's existing contracts create barriers competitors can't replicate quickly.

Network effects compound over time. As more partners join, brands increase product listings to capture the distribution 80 products today versus 20 in 2021. As product variety grows, partner earnings rise, attracting more partners in a self-reinforcing loop. Gig platforms like task-completion apps lack these dynamics because one delivery rider doesn't make the platform more valuable to the next rider.

Y Combinator backing and Shark Tank India validation signal institutional quality. While not guarantees, these endorsements mean GroMo survived Silicon Valley's toughest startup accelerator and convinced seasoned investors to deploy capital. Fly-by-night apps lack this scrutiny; their founders often remain anonymous and operating companies unregistered.

Long-term incentive alignment between platform and partners separates GroMo from exploitative models. GroMo earns only when partners earn if payout cycles delay or commission rates drop, partner churn kills the platform. Compare this to ad-watching apps that profit regardless of whether you ever withdraw, or game apps that monetize your time via ads while paying ₹2 consolation prizes.

Frequently asked questions

Q: Which app pays for referrals?

A: GroMo pays ₹300–₹2,400 per referral for financial products like credit cards, savings accounts, and loans. Google Pay, PhonePe, and Paytm offer ₹51–₹201 for UPI signups and bill payments, while Amazon Associates pays 1–8% of product order value. GroMo delivers the highest per-referral payout with instant withdrawals above ₹100.

Q: How to get 100 RS in Google Pay?

A: Google Pay occasionally runs promotional referral campaigns where both referrer and referee earn ₹51–₹101 when the new user completes their first UPI transaction or bill payment. These offers are time-limited and region-specific. Check the "Rewards" section in the Google Pay app for active campaigns, but note that financial product referrals via GroMo pay 10–20× more per conversion.

Q: How to earn ₹201 cashback?

A: PhonePe and Paytm offer ₹201 cashback during festival seasons when referred users complete specific actions like recharges, bill payments, or gold purchases above threshold amounts (typically ₹500–₹1,000). These promotions appear in the app's "Offers" tab. For consistent earnings beyond one-time cashback, GroMo's commission model generates ₹300–₹2,400 per sale without requiring the customer to spend money.

Q: How to get $600 on Greenlight?

A: Greenlight is a US-based kids' debit card with a referral program paying $10–$30 per signup, not $600. That figure likely refers to cumulative earnings after 20–60 referrals. Indian residents cannot access Greenlight; for rupee-based referral income, GroMo's financial product distribution offers localized earning potential up to ₹1,00,000 monthly across credit cards, savings accounts, and investment products.