Realistic ₹1 Crore Investment Plan with Zero Capital

Everyone searching for a "1 crore investment plan" wants the same thing: a realistic path to seven-figure wealth without gambling their savings. GroMo offers a different angle using commission income to fund your investments so you aren't pulling from your salary. You start with zero capital.

Most Indians chasing ₹1 crore focus only on where to invest. They ignore the harder question: where does the money actually come from? This post covers both sides smart investment vehicles and a way to generate the cash to fill them so your 2026 crorepati plan isn't just a spreadsheet fantasy.

What Does a Realistic ₹1 Crore Investment Plan Actually Require?

You need consistent monthly capital, a long time horizon, and instruments that compound reliably. Most plans don't fail because of bad instruments. They fail because the "consistent capital" part falls apart within a year.

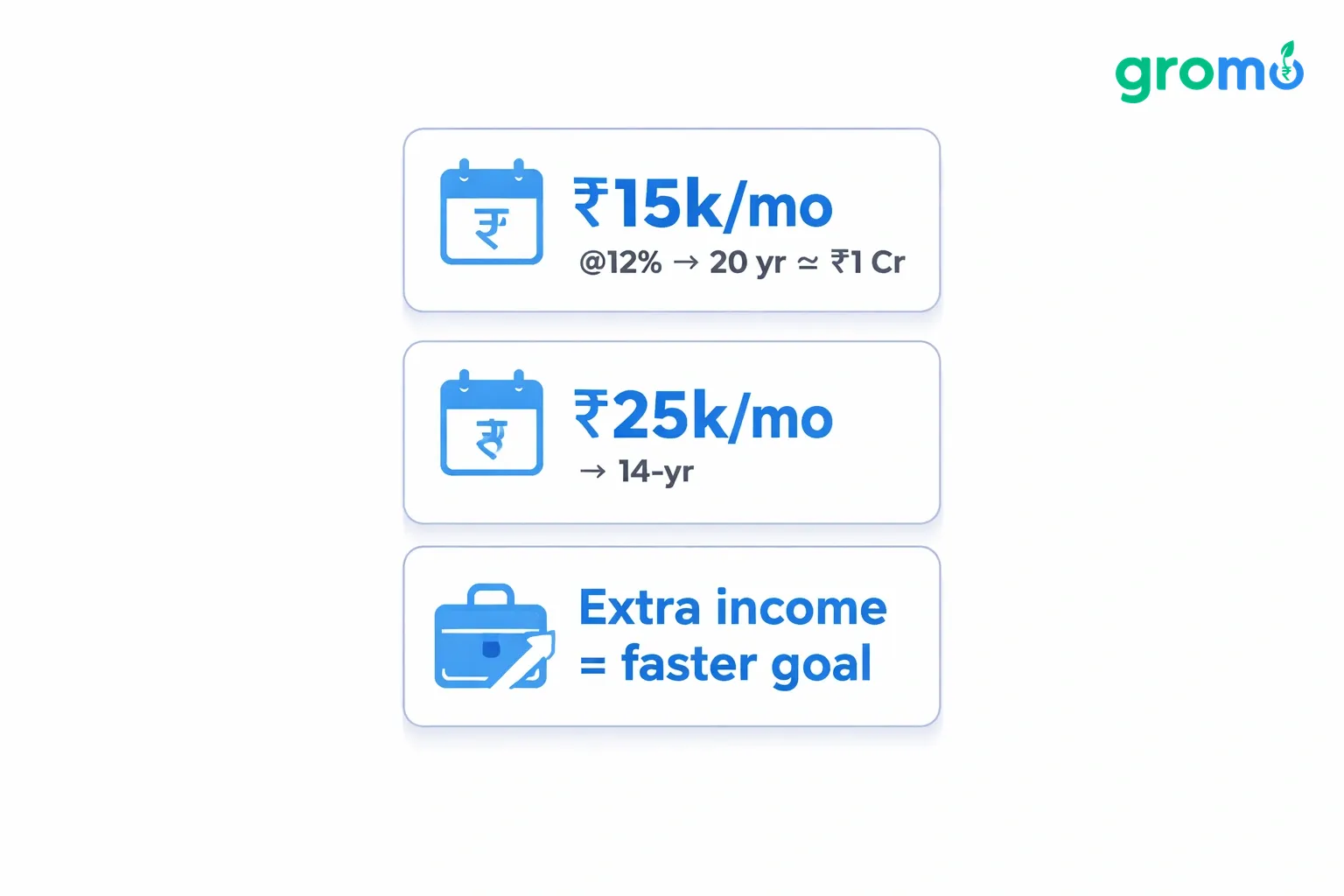

Look at the math. Invest ₹15,000 monthly at 12% annual return and you hit roughly ₹1 crore in 20 years. Push it to ₹25,000 monthly and you cut that down to 14-15 years. The variable most people can't control is their salary hike schedule. But they can control a second income stream that funds the difference.

That's usually where the gap kills the plan. Salaried professionals often can't increase their SIP contributions fast enough because their fixed income barely covers rising expenses. A commission-based side income like what GroMo offers becomes the lever that accelerates the timeline without needing a raise or a loan.

How Much Monthly Investment Is Needed to Reach ₹1 Crore?

Monthly investment needs vary wildly based on your timeline and expected returns. Here's a quick reference table using standard compounding assumptions at 12% annual returns a reasonable long-term equity mutual fund benchmark.

Time Horizon | Monthly SIP Needed | Total Invested | Wealth Gained |

|---|---|---|---|

10 years | ₹43,000 | ₹51.6 lakh | ₹48.4 lakh |

15 years | ₹19,800 | ₹35.6 lakh | ₹64.4 lakh |

20 years | ₹10,000 | ₹24 lakh | ₹76 lakh |

25 years | ₹5,300 | ₹15.9 lakh | ₹84.1 lakh |

Starting early cuts your required monthly commitment dramatically. But most Indians in their late 20s and 30s don't have an extra ₹15,000-₹40,000 sitting idle every month. That's the real constraint not the mutual fund choice, not the market, but disposable income.

Building a side income isn't optional for most crorepati plans it's structural. Without it, the required monthly SIP simply doesn't fit inside a typical salary after rent, EMIs, and household expenses.

Where Should the ₹1 Crore Investment Plan Actually Go?

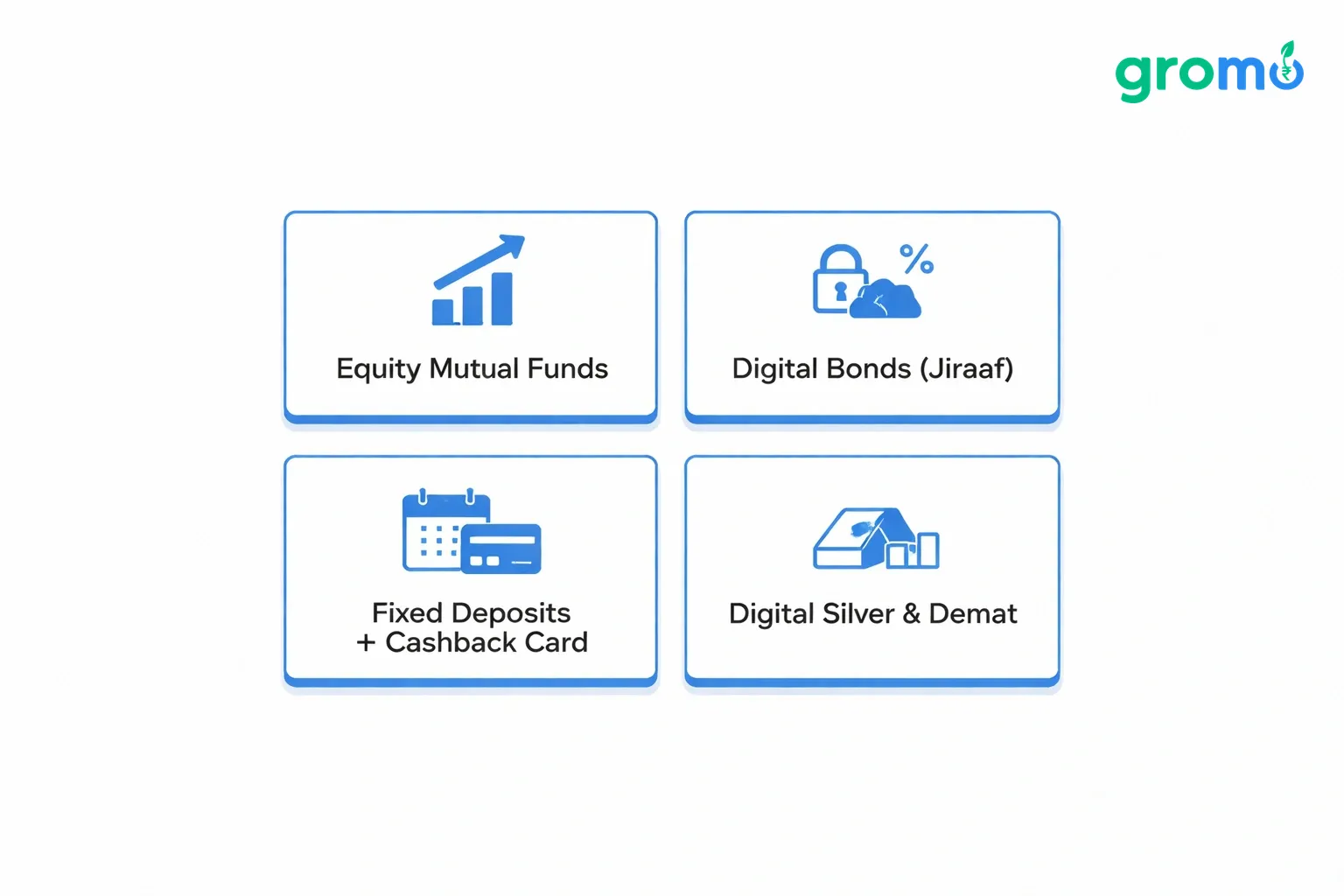

Diversified options work best. You spread risk across equity, fixed income, and alternatives. No single product should carry the entire weight of a multi-decade goal.

Equity mutual funds remain the backbone for most Indian investors chasing long-term wealth, given their historical 10-14% annualized returns. But 2026 investors also have access to instruments that didn't exist mainstream a decade ago.

Bond investments through platforms like Jiraaf offer fixed-income options with 8-15% p.a. returns a solid ballast against equity volatility, especially for investors nearing their goal timeline. Since these are 100% digital and start at just ₹1,000, they're accessible even for first-time fixed-income investors.

Fixed deposits still matter, particularly for building emergency buffers before aggressive investing begins. Products bundling FDs with cashback-linked virtual cards (check our RBI-approved loan apps guide for related credit-building context) let your parked capital do double duty.

Digital silver and demat accounts round out a diversified approach, letting investors dip into commodities and direct equity without heavy paperwork. Our digital silver investment guide covers how this fits into a broader wealth plan.

Most first-time crorepati planners put 100% into one instrument out of fear or unfamiliarity. Spreading ₹1 crore ambitions across 3-4 vehicles reduces risk without sacrificing much return.

Can Side Income Actually Speed Up a ₹1 Crore Goal?

Side income can accelerate a ₹1 crore goal by increasing your monthly investable surplus without cutting lifestyle expenses. An extra ₹15,000-₹30,000 monthly, redirected entirely into SIPs or bonds, can shave 5-8 years off a typical timeline.

GroMo's model fits this need precisely because it requires zero upfront investment. Partners earn commissions by helping others access credit cards, loans, demat accounts, and investment products the same categories that make up a healthy financial portfolio. No inventory, no office, no fixed hours.

The math changes significantly with a functioning side income:

Base salary SIP: ₹10,000/month → ₹1 crore in ~20 years

Salary SIP + ₹15,000 GroMo side income (partially invested): ₹18,000/month → ₹1 crore in ~15 years

Salary SIP + ₹30,000 GroMo side income: ₹28,000/month → ₹1 crore in ~13 years

These aren't hypothetical numbers. GroMo has facilitated over 60 lakh partners who've collectively earned ₹100 crores through commission-based selling proof that this income stream is real, not speculative. Read the full breakdown in Earn Online with GroMo: ₹100 Crore in Payouts.

What Financial Products Can You Sell to Fund Your Investment Plan?

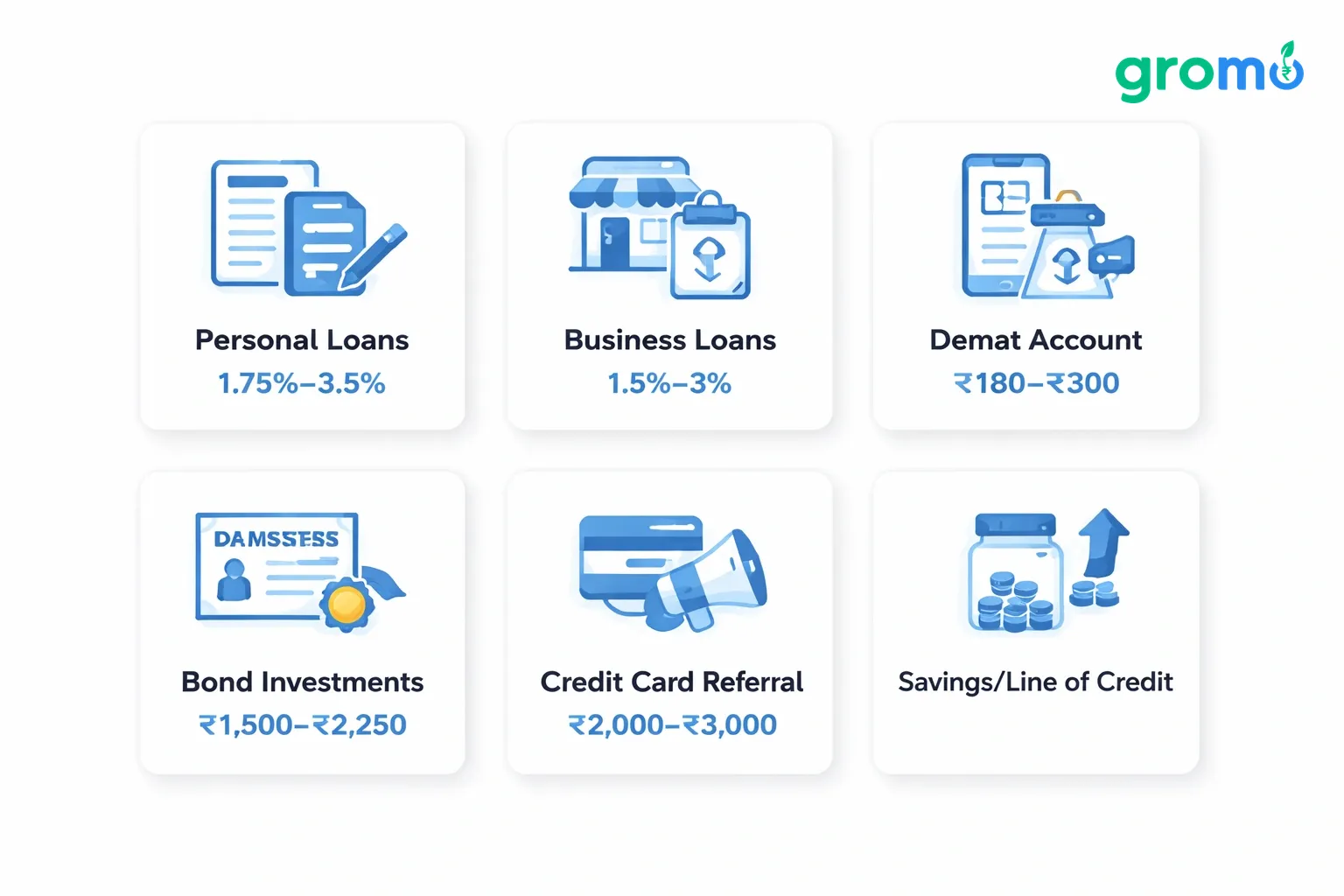

GroMo partners earn commissions across six major categories: credit cards, loans, savings accounts, demat accounts, lines of credit, and investment products. Each sale generates instant payouts that can go straight into your ₹1 crore SIP.

Current partner network examples show the potential:

Personal loans (Moneyview, Hero Fincorp) pay 1.75%-3.5% commission per disbursed loan

Business loans (ClickPe by Muthoot, Poonawalla Fincorp) pay 1.5%-3% on loans up to ₹50 lakh

Demat account openings (Aditya Birla Money, Indiabulls) pay ₹180-₹300 per activation

Bond investments via Jiraaf pay ₹1,500-₹2,250 per first-time investor

Credit card referrals (Axis Flipkart Card) pay ₹2,000-₹3,000 per approved card

If you're active on social media or have a wide personal network, selling even 5-6 products monthly across these categories can generate ₹15,000-₹40,000 money that goes directly toward funding your own crorepati SIP. Our detailed guide on credit card referral earnings shows exactly how this works in practice.

The model compounds on two fronts: your investments grow through market returns, while your side income compounds through referral networks and repeat customers.

How Do You Build a Sustainable Passive Income Layer for This Plan?

Sustainable passive income comes from combining active commission work with genuinely passive elements like referral team-building. GroMo's referral program lets partners earn from the sales activity of people they onboard, creating income that doesn't require constant personal selling.

This layered approach mirrors what serious investors already understand: multiple income streams beat single-source dependency. Our companion post, Passive Income 2026: GroMo Earnings Without Clocking In, goes deeper into how partners structure this for long-term, low-effort earnings. It's worth reading if you want your side income to outlast your initial motivation.

Building this layer typically follows a sequence:

Months 1-3: Learn the app, complete free certification training, make your first few sales

Months 4-6: Identify your best-performing product categories, build a customer pipeline

Months 7-12: Start referring other partners, building a small team for passive commission

Year 2 onward: Redirect 70-80% of side income directly into your ₹1 crore investment plan

This isn't a get-rich-quick framework. It's a get-rich-steadily framework which is exactly what a genuine ₹1 crore goal demands.

What Mistakes Derail Most ₹1 Crore Investment Plans?

Most plans fail due to inconsistency, not bad investment choices. People start SIPs enthusiastically, then pause during expensive months effectively resetting their compounding clock.

Common derailment patterns:

Stopping SIPs during market dips exactly when disciplined investors should continue or increase contributions

Chasing high-return schemes without checking RBI registration our guide on identifying RBI-registered loan apps helps spot red flags in adjacent lending products

Relying solely on salary hikes to increase investment capacity, ignoring side income entirely

Ignoring credit score maintenance, which affects loan and credit card eligibility for wealth-building tools (see our credit score improvement guide)

Treating side income as spending money instead of redirecting it into the investment plan

Avoiding these mistakes matters more than picking the "perfect" mutual fund. Discipline compounds; perfection doesn't.

Frequently Asked Questions

Q: How long does it realistically take to build a ₹1 crore investment plan in India?

A: With disciplined monthly SIPs at 12% average returns, timelines range from 10 years (₹43,000/month) to 25 years (₹5,300/month). Adding side income typically shaves 5-8 years off these timelines.

Q: Is GroMo a genuine way to fund a ₹1 crore investment goal?

A: Yes. GroMo is a zero-investment commission platform where partners earn by helping others access financial products. Over 60 lakh partners have collectively earned ₹100 crores, making it a legitimate, low-risk income supplement.

Q: What's better for a ₹1 crore plan mutual funds or bonds?

A: A mix works best. Equity mutual funds drive long-term growth, while bond investments like those on Jiraaf offer stable 8-15% returns that balance portfolio volatility especially closer to your goal date.

Q: Do I need any investment to start earning with GroMo?

A: No upfront capital needed. Partners download the free app, complete free certification training, and start earning commissions immediately after their first successful referral.

Q: Can side income really replace the need for a salary hike to reach ₹1 crore faster?

A: Yes, in many cases. A consistent ₹20,000-₹30,000 monthly side income redirected into SIPs can outpace waiting years for salary increments, especially in slow-growth job markets.

Q: What financial products offer the highest commissions on GroMo for funding investment goals?

A: Business loans (1.5%-3% on amounts up to ₹50 lakh) and bond investments via Jiraaf (₹1,500-₹2,250 per lead) currently offer some of the strongest payout ranges for active partners.