Maximize ₹10 Lakh Returns with FDs, Bonds & GroMo Side Income

If you have ₹10 lakhs sitting in your savings account and want monthly income, here's what you're actually looking at: ₹6,000 to ₹12,500 a month. That's the realistic range. To get there, you'll need to spread the money across fixed deposits, bonds, and maybe debt funds. There is no magic product that pays high returns with zero risk.

Most people do one of two things: dump it all into a big corporate FD and lose sleep over whether the company will default, or leave it in a savings account earning 3.5%. Neither works well. The sweet spot is a mix of safety and yield. And honestly, even the best mix might not cover your bills. That's where side income platforms like GroMo come in they can add ₹10k-20k a month on top of your investment returns.

How Much Monthly Income Can ₹10 Lakhs Really Generate?

Ten lakh rupees isn't going to replace a salary. At best, it generates pocket money or covers a couple of utilities. Bank FDs currently pay 6.5% to 7.5%, which means ₹5,400 to ₹6,250 monthly before tax. Bonds can push that to 8-15% annually, landing you between ₹6,600 and ₹12,500 monthly. The trade-off? Bonds aren't as easy to cash out as a savings account, and you need to check who you're lending to.

Here is a comparison of what's realistically on the table:

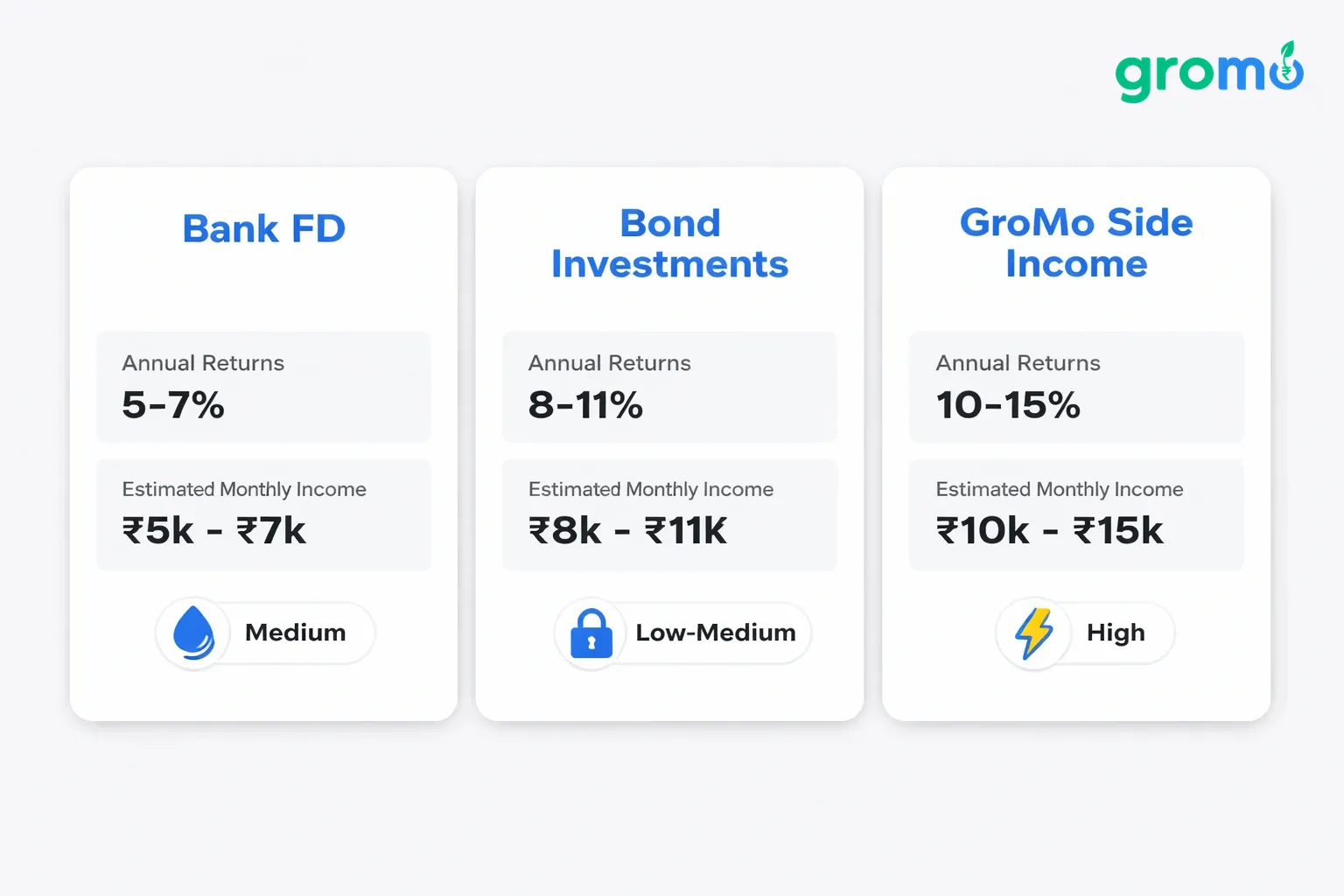

Instrument | Annual Return | Monthly Income | Liquidity |

|---|---|---|---|

Bank FD | 6.5%-7.5% | ₹5,400-₹6,250 | Medium |

Bond Investments | 8%-15% | ₹6,600-₹12,500 | Low-Medium |

Debt Mutual Funds | 6%-9% | ₹5,000-₹7,500 | High |

Senior Citizen Savings | 8.2% | ₹6,800 | Low |

Monthly Income Plans | 7%-9% | ₹5,800-₹7,500 | Medium |

If you're under 45, this income alone won't cut it. Pairing investment returns with a side hustle is becoming necessary, not optional.

Fixed Deposits: The Boring Baseline

FDs are the default option for a reason. They are simple. You park ₹10 lakhs, select the monthly payout option, and the bank credits your account. For senior citizens, rates go up to 8% or slightly more.

The safety net is real deposits are insured up to ₹5 lakhs per bank under the DICGC scheme. But the returns barely beat inflation. If you withdraw early, you lose interest and pay a penalty. It's safe, but it's a slow ride. If you want to earn from these products without locking your own cash, GroMo lets you earn commissions by helping others open FDs or demat accounts.

Bond Investments: Higher Returns, Curated Risk

This is where ₹10 lakhs can actually work harder. Digital platforms like Jiraaf let you buy bonds from established companies, often starting at just ₹1,000. Returns sit between 8% and 15% depending on the issuer's credit rating.

A smart move here is splitting your capital across 3-4 different bonds. That way, if one issuer has trouble, you aren't wiped out. The process is digital KYC, selection, and investment happen in minutes. But remember, these are securities. Returns aren't guaranteed like an FD, and you need to understand who the issuer is.

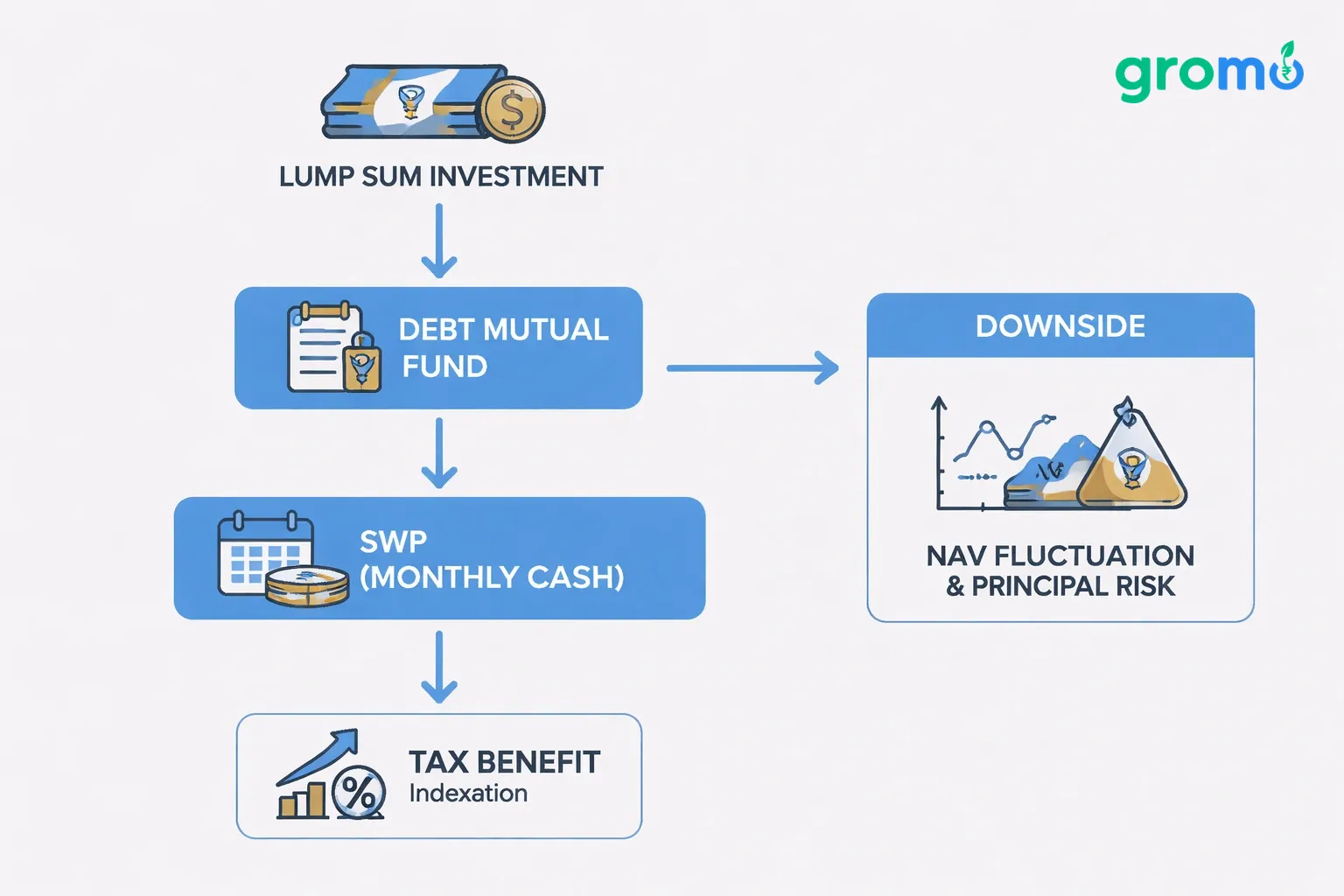

Debt Mutual Funds and SWP: Flexible Monthly Cash Flow

Debt funds with a Systematic Withdrawal Plan (SWP) work differently. You invest a lump sum, and the fund redeems a fixed number of units every month. It’s flexible you can stop or change the amount.

Taxation is the upside. If you hold debt funds for over three years, you get indexation benefits, which lowers your tax bill compared to FD interest. The downside is Net Asset Value (NAV) fluctuation. Your principal isn't guaranteed, so in a bad market cycle, you might withdraw less than you put in.

Diversification: Don't Put ₹10 Lakhs in One Basket

Putting all ₹10 lakhs in one place is risky. A standard approach might look like this: 40% in FDs for stability, 30% in bonds for yield, and 30% in debt funds or the Senior Citizen Savings Scheme for flexibility.

This mix protects you. If interest rates drop, the bond portion might gain value. If rates rise, the FD ladder helps. It's worth checking this split once a year. For more on how to balance these streams, see our guide on active and passive income merging for Indians in 2026.

Why ₹10 Lakhs Alone Isn't Enough Adding Side Income

Even if you optimize the ₹10 lakhs perfectly, hitting ₹12,500 a month is the ceiling. Inflation will eat into that fixed income every year. You need a backup plan that doesn't require capital.

This is why GroMo exists. You can earn commissions by helping people open savings accounts, apply for credit cards, or invest in bonds. You don't invest your own money; you use your phone and your network. Partners have already earned over ₹100 crores collectively through this model.

If you want to see how much difference a side income makes, read our breakdown on building a realistic ₹1 crore investment plan with zero capital.

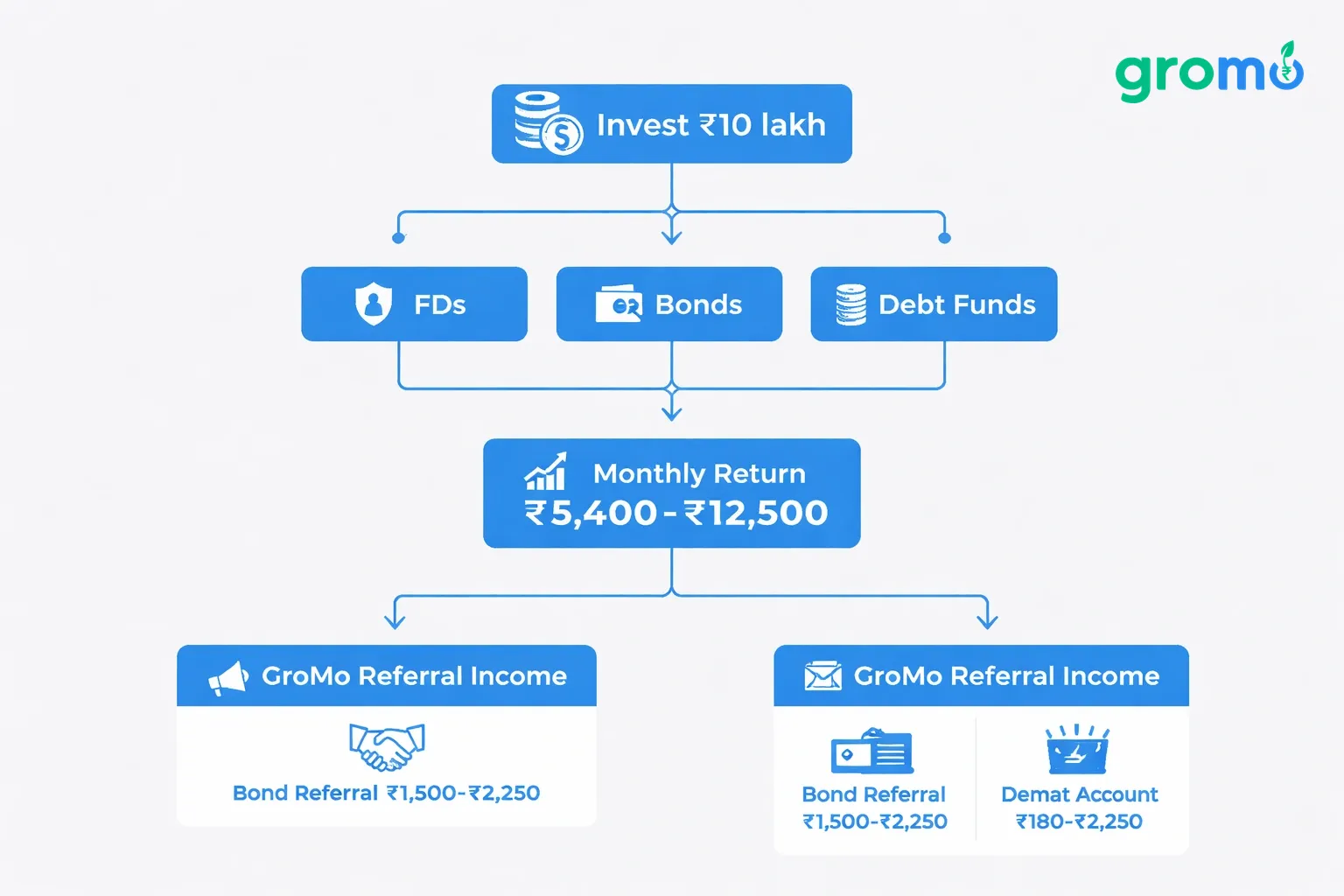

How GroMo Complements Your ₹10 Lakh Investment Strategy

If you are already looking at Jiraaf bonds or Kotak 811 accounts for your own portfolio, you know enough to recommend them. GroMo lets you do exactly that. You share a link, someone opens an account or buys a bond, and you get paid.

The numbers vary. A bond referral might pay ₹1,500 to ₹2,250. A demat account referral could be anywhere from ₹180 to ₹2,250. It fits neatly into a broader strategy of passive income in 2026 without clocking in, where your knowledge generates cash flow.

Tax Considerations for Monthly Income Investors

Tax eats returns. FD interest is fully taxable according to your income slab. If you fall in the 30% bracket, that 7% FD return is effectively 4.9% post-tax.

Bonds are similar interest is taxed as income. Debt funds held long-term get indexation benefits, which helps, but it's not a tax-free haven. This is another reason to look at commission-based income. Referral earnings are taxable income, sure, but they don't dilute your investment returns.

Building a Realistic Monthly Income Roadmap

Start by dividing your ₹10 lakhs based on how much risk you can tolerate and when you need the money. Do this first. Then, set up a GroMo account.

This isn't just about having two income streams; it's about security. If your investments have a bad year, your commissions don't necessarily drop. We've seen this work for housewives earning ₹15K-50K monthly and students earning ₹300-5000 daily.

If you have a full-time job, check how earning ₹1 lakh monthly while working is possible. There are also city-specific guides like zero-investment ideas in Mumbai or Bangalore if you want localized tips.

Final Thoughts on Making ₹10 Lakhs Work Harder

₹10 lakhs can generate decent monthly income if you stop chasing guaranteed high returns and start mixing FDs, bonds, and debt funds intelligently. But relying solely on investment returns in 2026 is a losing game. The real play is combining those passive returns with active, zero-investment earning via GroMo.

It works for salaried people, retirees, and homemakers alike. The math is simple: your money works, and you work your network. Together, they compound faster.

Frequently Asked Questions

Q: How much monthly income can I realistically get from ₹10 lakhs?

You should expect between ₹5,400 and ₹12,500 per month. FDs sit at the lower end (around 6.5-7.5%), while bonds can push higher (8-15%), but carry more risk.

Q: Are bond investments safer than mutual funds?

Bonds give fixed returns if the issuer doesn't default. Debt mutual funds fluctuate with the market. Neither is 100% safe, but they serve different purposes.

Q: Can I add income without investing more capital?

Yes. GroMo pays commissions for referring financial products like FDs, bonds, and credit cards. You need time and a phone, not money.

Q: Is FD interest taxable?

Yes. It is added to your total income and taxed according to your tax slab. This often reduces the actual return significantly.

Q: Why should an investor use GroMo?

If you understand bonds or savings accounts well enough to buy them, you understand them well enough to sell them. GroMo lets you monetize that knowledge.

Q: How should I split ₹10 lakhs?

A standard split is 40% FDs, 30% bonds, and 30% debt funds. Adjust this based on how soon you need the money and how much risk you can stomach.