Fixed Income vs GroMo: Hybrid Earnings Strategy 2026

Fixed income plans are the boring part of a portfolio. That's the whole point. You put money in, you know exactly what comes out, and you don't check the markets every morning. But in 2026, the options aren't just bank FDs and bonds anymore. GroMo’s referral commissions pay out immediately. You don’t lock away capital for years to see results.

Most fixed income plans reward patience. GroMo rewards action. You earn commissions right after a successful referral. I’ll walk through the traditional options, compare them to GroMo, and show how mixing both actually works.

What Is a Fixed Income Plan?

Fixed income plans are financial instruments that pay predetermined returns over a set period. Unlike equities, which fluctuate with market sentiment, these plans prioritize capital safety. Bonds, fixed deposits, and government schemes fall under this umbrella.

In India, the FD is almost sacred. Banks offer 6-7% annual returns on standard FDs. Curated platforms now offer more Jiraaf, for instance, connects investors to bond investments yielding 8-15% p.a. It’s a blend of safety and better returns than the legacy FDs your parents used.

The appeal is simple: you know what you're getting. No guessing games. For risk-averse investors, especially those nearing retirement, fixed income is the anchor.

Why Fixed Income Alone Isn't Enough in 2026

Fixed income plans alone rarely beat inflation. Real returns after tax and inflation often hover in low single digits. This makes fixed income a foundation, not a complete strategy.

Think about it: if inflation runs at 5-6% annually, a traditional FD returning 6.5% barely keeps pace after tax deductions. That’s why financial planners suggest layering fixed income with active or semi-passive income streams that can outpace inflation.

This is where GroMo comes in. Instead of just parking money, you generate income by helping others access financial products credit cards, loans, investment accounts and earn commissions instantly. It's a side strategy, not a replacement.

For a deeper dive into how passive earnings work without daily clocking in, check out the parent guide: Passive Income 2026: GroMo Earnings Without Clocking In.

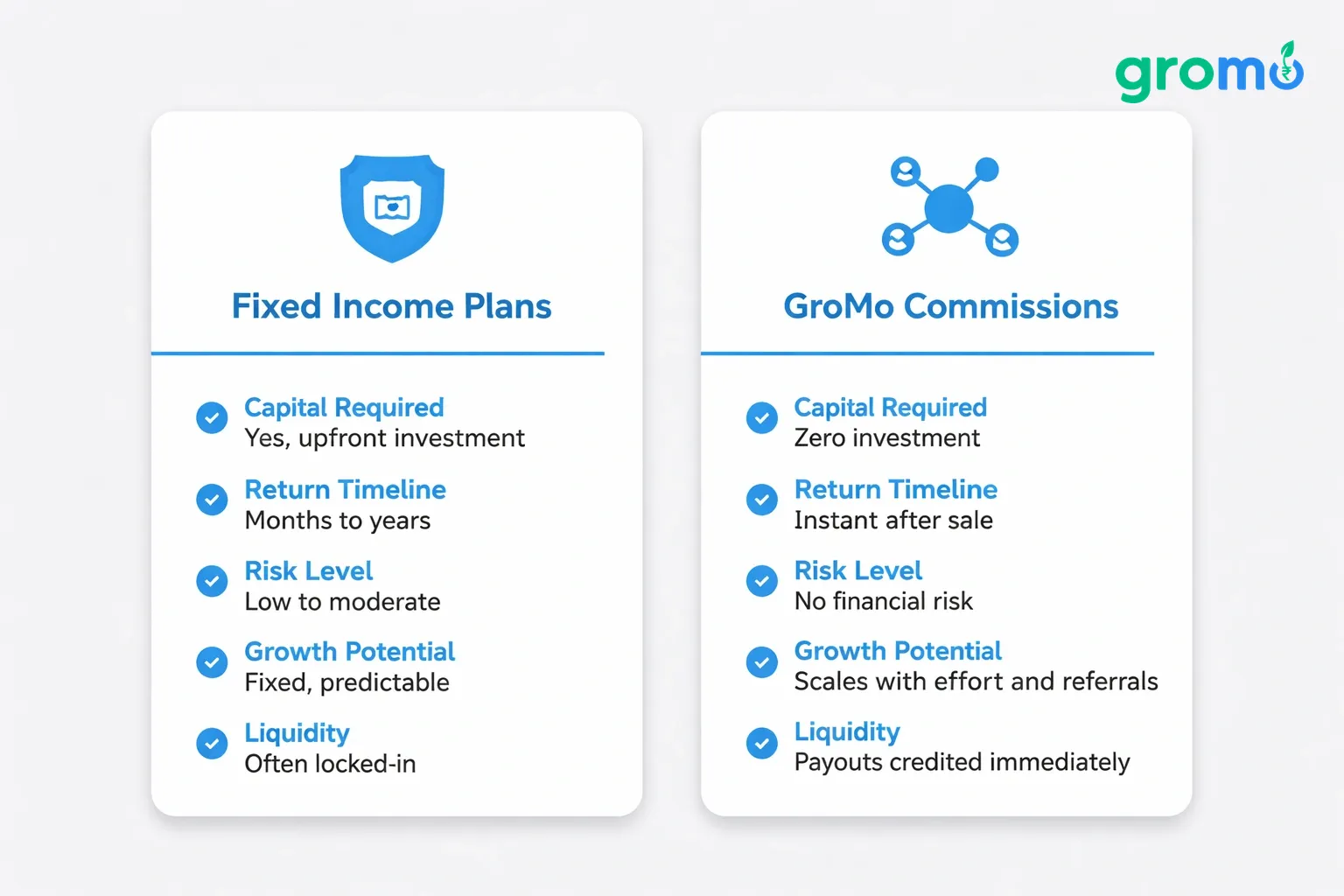

Comparing Fixed Income Plans vs GroMo Commissions

Fixed income plans and GroMo commissions serve different purposes. Fixed income protects capital. GroMo generates active-to-passive income by monetizing your network, often with faster payout cycles.

Here's the breakdown:

Feature | Fixed Income Plans | GroMo Commissions |

|---|---|---|

Capital Required | Yes, upfront investment | Zero investment |

Return Timeline | Months to years | Instant after sale |

Risk Level | Low to moderate | No financial risk (no capital at stake) |

Growth Potential | Fixed, predictable | Scales with effort and referrals |

Liquidity | Often locked-in | Payouts credited immediately |

Bond investments through Jiraaf require a minimum investment of ₹1,000 and lock-in periods depending on tenure. GroMo requires zero capital you share product links and earn when someone completes a transaction.

Building a Hybrid Fixed Income Plan for 2026

A hybrid fixed income plan mixes traditional guaranteed-return instruments with commission-based earning. You get safety and some growth potential without exposing your savings to market risk.

Here's a practical split:

40% in Fixed Deposits or Bonds: Use platforms offering curated bond investments with 8-15% returns for stable growth.

30% in Mutual Fund-Linked Loans: Products like Abhiloans let you borrow against mutual funds without selling them, keeping your investments compounding while you access cash.

30% Active Income via GroMo: Selling financial products like credit cards, personal loans, and investment accounts adds a flexible income layer with zero capital lock-in.

The goal isn't to replace safety with risk. It's to diversify so one underperforming asset class doesn't derail your plan. Housewives, students, and working professionals across India are already using this model read more in Earn ₹15k-50k/Month as a Housewife Selling Financial Products.

How GroMo Fits into Your Fixed Income Strategy

GroMo complements fixed income by adding a commission-based income stream. It works alongside your existing investments. You earn while your fixed income assets mature.

It works like this: Download the GroMo app, complete the free certification training, and start sharing product links for credit cards, loans, savings accounts, and investment products from partners like Axis Bank, Kotak 811, Upstox, and Bajaj Finserv. Each successful referral pays a commission sometimes within hours.

Referring someone for a personal loan through Smartcoin can earn 2.75% to 4.5% of the loan value. Referring for bond investments through Jiraaf can net ₹1,500 to ₹2,250 per successful lead. These payouts happen fast compared to waiting years for an FD to mature.

Over 60 lakh partners have collectively earned ₹100 crores using this model. Many use the income to fund their fixed income investments, using GroMo earnings to grow their bond or FD portfolios faster than salary alone would allow.

For more on how active and passive income streams work together, read Active & Passive Income: GroMo Merges Both for Indians 2026.

Practical Steps to Start Today

Getting started doesn't require much. First, look at your existing savings and move a portion toward guaranteed-return instruments. Then add GroMo as your active income layer.

Here’s a simple roadmap:

Check your savings: See how much sits in low-yield savings accounts versus fixed income instruments.

Look beyond your bank: Research bond platforms offering better returns than traditional FDs. Check the lock-in periods.

Download the GroMo app: Complete the free training to become a certified financial product distributor.

Share product links: Focus on categories you know credit cards, loans, or investment accounts.

Reinvest the earnings: Put commission income back into fixed income instruments to compound returns.

Check in quarterly: Review your fixed income maturity dates and GroMo referral income to see if you need to rebalance.

This works for students building early habits, housewives seeking flexible income, and professionals wanting a side hustle that doesn't interfere with their day job. For students, check out Students Earn ₹300-5,000 Daily via GroMo's Zero-Investment Biz for tailored strategies.

Common Mistakes to Avoid

Don't treat fixed income plans as a set-it-and-forget-it solution. Inflation eats away at stagnant money. Combining fixed income with an active income stream like GroMo helps avoid that stagnation.

Another common error is locking up too much capital in long-term bonds without keeping liquidity. Always keep an emergency fund separate. GroMo's instant payout structure can serve as a liquidity buffer earnings hit your account immediately after a qualifying sale.

Also, don't fall for unregulated schemes promising unrealistic fixed returns. Stick to RBI-approved lending partners and verified investment platforms. For guidance on identifying safe options, read RBI-Approved Loan Apps in India 2026: Safe Borrowing & Earnings.

Final Thoughts

Fixed income plans are essential for stability. But they work best when paired with an active income source. GroMo offers that zero-investment earning potential that complements your savings without adding risk to your capital.

Whether you're a professional, student, or homemaker, blending traditional fixed income instruments with GroMo's commission model creates a more resilient financial plan for 2026 and beyond.

Frequently Asked Questions

Q: What is the safest fixed income plan for beginners in 2026?

A: Bank fixed deposits are the safest starting point, offering guaranteed returns around 6-7% annually. For slightly higher returns with managed risk, curated bond platforms offering 8-15% p.a. are worth exploring once you understand the lock-in terms.

Q: Can GroMo earnings replace a fixed income plan entirely?

A: No. GroMo earnings depend on referral activity and aren't guaranteed like fixed income instruments. They work best as a complementary stream that helps you fund and grow your fixed income investments.

Q: How quickly can I start earning through GroMo alongside my fixed income investments?

A: Immediately after downloading the app and completing the free certification training. Payouts are credited instantly after a qualifying sale, unlike fixed income plans that require months or years to mature.

Q: Is there any investment required to start with GroMo?

A: No. GroMo requires zero investment. You share product links and earn commissions on successful referrals, regardless of your current portfolio size.

Q: What's the minimum amount needed to start a fixed income plan in 2026?

A: Many bond investment platforms allow entry with as little as ₹1,000. Bank FDs often require ₹1,000 to ₹5,000 minimum deposits depending on the institution.

Q: How does loan-against-mutual-fund fit into a fixed income strategy?

A: Products like Abhiloans let you access cash without selling your mutual fund holdings. Your investments keep compounding while you cover short-term needs, making it a smart add-on to your fixed income plan.