Best Investment Plans 2026: Earn with GroMo

Most "best investment plan" lists for 2026 ignore one option: becoming a distributor instead of just an investor. GroMo lets you earn commissions by helping others invest in mutual funds, demat accounts, and bonds. You turn financial literacy into income without locking up your own capital.

Standard investment plans ask you to park money and wait years. That works for wealth building, but it doesn't help your monthly cash flow right now. You can actually combine traditional investment plans with GroMo's zero-investment earning model to get both immediate income and long-term wealth you don't have to choose.

What Makes an Investment Plan "Best" in 2026?

There isn't one "best" plan. It depends on whether you need money in 6 months or 6 years. Inflation, shifting RBI policies, and better financial literacy have changed what "good returns" look like. A plan that worked in 2020 might underperform in 2026.

The conversations today usually revolve around these instruments:

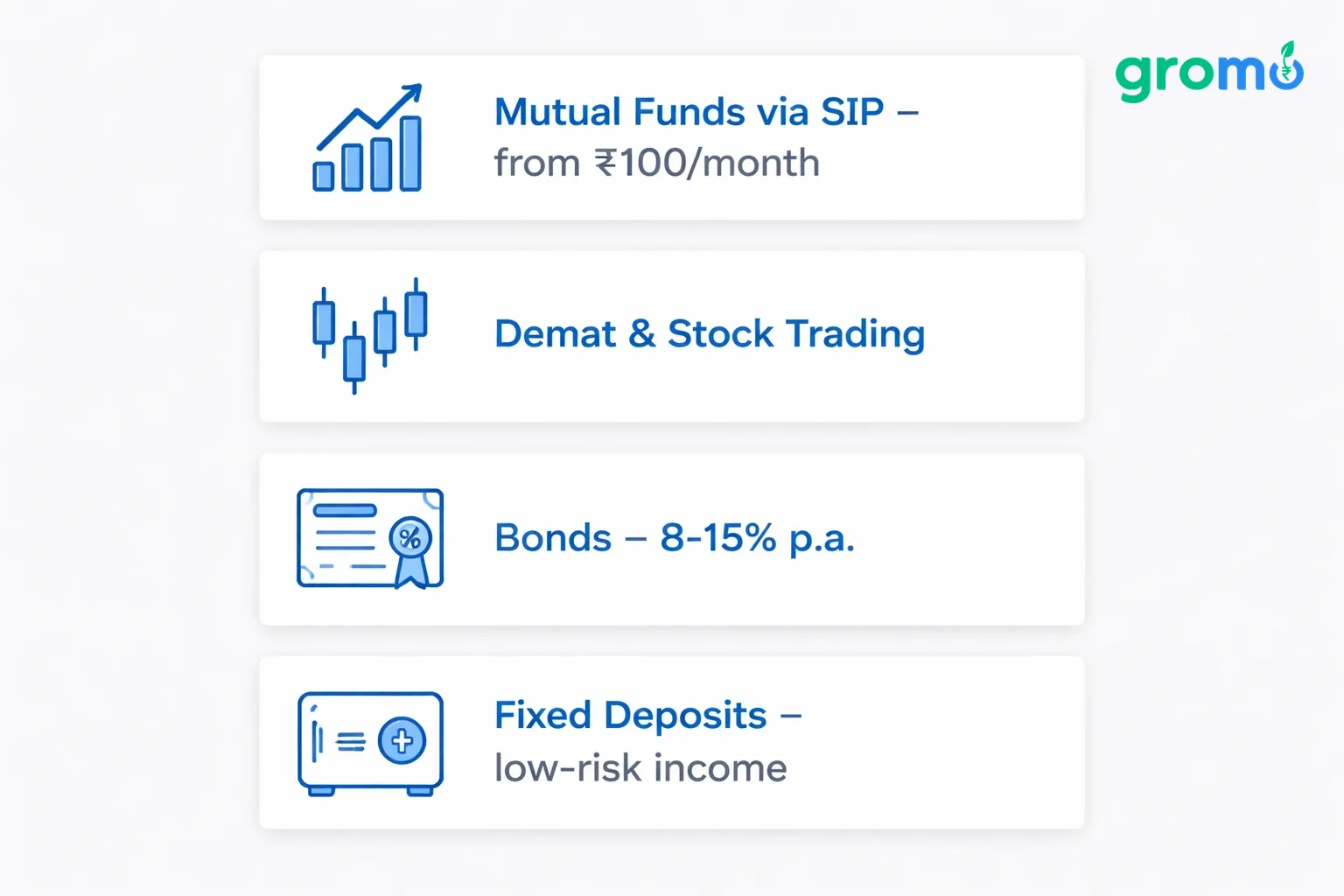

- Mutual Funds via SIP – Start from ₹100/month, good for beginners

- Demat & Stock Trading – For those comfortable with market volatility

- Bonds – Fixed returns between 8-15% p.a., safer than equities

- Fixed Deposits (via marketplaces) – Predictable, low-risk income

- Digital Gold/Silver – Hedge against inflation

If you're new to this, our guide on digital silver investment in India 2026 breaks down one popular low-entry option in detail.

Investment Options You Can Actually Distribute (And Earn From)

GroMo lets you become the bridge between financial platforms and everyday investors. Partners earn commissions by helping people open demat accounts, invest in bonds, or start SIPs without spending a rupee themselves.

GroMo's product documentation lists real payout structures across dozens of investment products:

| Product | Payout Range | Ideal Customer |

|---|---|---|

| Jiraaf Bond Investment | ₹1,500 - ₹2,250 | Mass-affluent seeking fixed income |

| Appreciate Wealth (US Stocks) | ₹1,400 - ₹2,250 | Investors wanting FAANG exposure |

| AngelOne Demat | ₹300 - ₹500 | Retail investors, full-feature broker |

| 5paisa Demat | ₹300 - ₹500 | First-time traders |

| Jiraaf FD | ₹1,500 - ₹2,250 | Conservative, FD-style investors |

Each product has its own eligibility rules and compliance steps. The pitch is simple: help someone start investing, earn a commission instantly. For a deeper dive, check out mutual fund distribution commissions in India 2026.

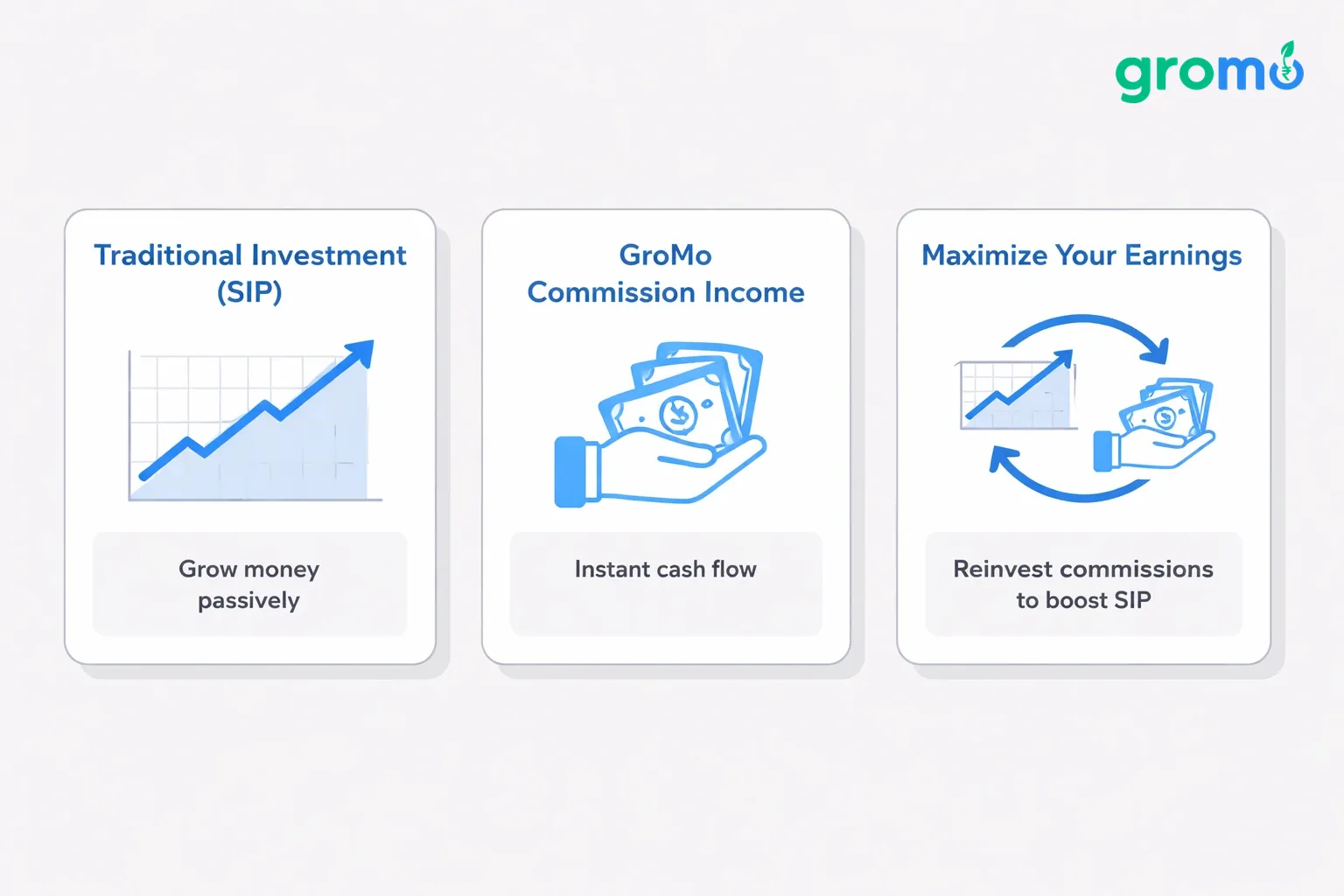

Why Combine Investment Plans with Commission Income?

Why bother with both? Because they solve different problems. Your investments grow passively, while GroMo earnings provide active cash flow you can reinvest or spend immediately.

Think about it this way. A ₹5,000 SIP takes years to show meaningful growth. But referring five people to open demat accounts this month could earn you ₹1,500-₹2,500 instantly. That is real money you can use to increase your own SIP contributions.

This works well because you aren't risking capital to earn the commission. Payouts are instant, unlike investment returns. You also learn financial products deeply, which makes you a smarter personal investor, and your network benefits from products you actually understand.

Our related post on active and passive income how GroMo merges both for Indians in 2026 explains this dual-income philosophy in more depth. It's worth reading if you're serious about building wealth from multiple directions.

Building a ₹1 Crore Corpus: Where GroMo Fits

Building a ₹1 crore corpus takes consistent contributions over time. GroMo's zero-capital commission model can fund your SIPs, bond purchases, or FD investments without touching your salary.

Let's look at the math. Say you refer 10 people monthly to open demat accounts, averaging ₹400 payout each. That's ₹4,000 monthly enough to fund a decent SIP without dipping into your own savings. Scale this to 30-40 referrals monthly across bonds, credit cards, and savings accounts, and you're looking at ₹15,000-₹25,000 in pure commission income.

For a full breakdown of how zero-capital earnings can snowball into serious wealth, read our detailed guide: Realistic ₹1 Crore Investment Plan with Zero Capital. It walks through the exact math and timelines.

This is also connected to the broader idea explored in Passive Income 2026: GroMo Earnings Without Clocking In, the parent guide covering how commission-based income can function like passive income once your network is established.

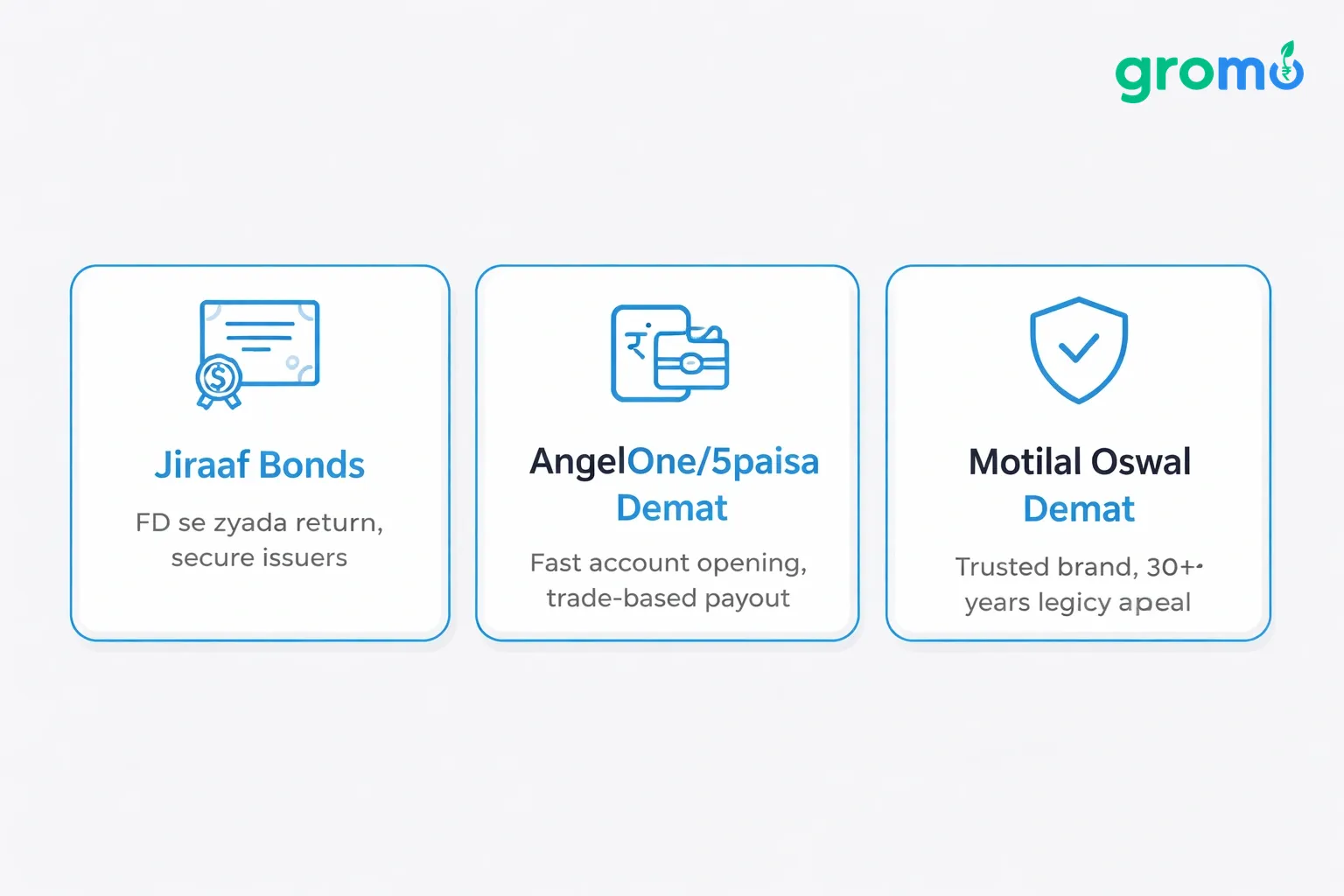

Which Investment Products Are Easiest to Distribute?

Bonds and demat accounts are the easiest investment products to distribute in 2026. They have straightforward onboarding, digital KYC, and clear payout triggers tied to first transactions.

Compare that to insurance-linked investment products, which involve longer compliance cycles (note: GroMo no longer offers insurance products). Instead, focus on:

- Jiraaf Bonds – Simple pitch: "FD se zyada return, secure issuers"

- AngelOne/5paisa Demat – Fast account opening, trade-based payout

- Motilal Oswal Demat – Trusted brand, 30+ years legacy appeal

Each product requires you to understand basic eligibility (age 18+, PAN, Aadhaar-linked mobile) and compliance windows (usually 7-30 days for first trade). GroMo's in-app training covers this, so you're never pitching blind.

Common Mistakes People Make with Investment Plans

Investment mistakes usually come from chasing returns without understanding risk or liquidity needs. The best investment plan isn't the one with the highest returns it's the one that matches your timeline and risk tolerance.

Watch out for these patterns:

- Putting everything into one instrument – Diversify across bonds, equity, and FDs

- Ignoring lock-in periods – Some products penalize early withdrawal

- Skipping KYC compliance – Incomplete KYC delays payouts and account activation

- Believing "guaranteed returns" claims – Legitimate products disclose risk clearly

If you're also exploring credit-building alongside investing, our post on how to improve your credit score in India (2026 guide) pairs well with this strategy since better credit often unlocks better investment terms.

How to Get Started This Month

Getting started requires three things: a GroMo account, basic product knowledge, and a network willing to listen. None of these require capital investment.

Follow this sequence:

- Download the GroMo app and complete free certification training

- Pick 2-3 investment products matching your network's profile (students vs. salaried professionals)

- Share personalized links via WhatsApp, social media, or in-person conversations

- Track leads and payouts directly in-app

- Reinvest early commissions into your own SIP or bond portfolio

This approach mirrors what's covered in our broader guide on zero-investment business models in 2026, which explains why commission-based models outperform traditional franchise or retail setups for beginners.

Frequently Asked Questions

Q: What is the best investment plan for beginners in 2026? A: SIPs starting at ₹100/month through platforms like Aditya Birla MF offer the lowest entry barrier. Bonds via Jiraaf suit those wanting higher fixed returns (8-15% p.a.) with moderate risk.

Q: Can I earn money by helping others invest without investing myself? A: Yes. GroMo lets you distribute investment products like demat accounts and bonds, earning commissions ranging from ₹300 to ₹2,250 per successful referral, without any capital investment.

Q: How quickly are GroMo investment referral payouts credited? A: Payouts typically process within days of the customer completing KYC and their first qualifying transaction. Exact timelines vary by product, usually 7-30 days.

Q: Is combining SIP investing with GroMo commission income a good strategy? A: It works well. Commission income from referrals can fund your own SIP contributions without touching your salary, effectively accelerating your personal investment goals using zero-risk earnings.

Q: What documents do I need to distribute investment products on GroMo? A: You need a smartphone, PAN, and Aadhaar-linked mobile number to get certified. Your customers will need similar documents (PAN, Aadhaar) to open their own accounts.

Q: Are bond investments through Jiraaf safe for first-time investors? A: Jiraaf curates issuers and discloses securities market risks upfront. Returns of 8-15% p.a. are higher than FDs but carry more risk than government-backed instruments, so read disclosures carefully.