2026 Investment Plan: GroMo Referrals & Safe Income Strategies

If you're looking for the single "best" investment plan in India for 2026, you can stop. It doesn't exist. A good plan mixes boring, safe stuff like FDs and bonds with a way to actually generate cash like GroMo so you aren't just parking money and waiting.

Most financial advice obsesses over where to park your money. It skips the harder part: how to get more of it. In your 20s and 30s, your ability to earn usually matters more than your ability to pick stocks. Here's what a realistic plan actually looks like this year standard investing plus commission income, because "save and invest" is useless if you don't have enough to save.

What a "Best" Plan Actually Looks Like

A plan needs three things: accessible cash, returns that beat inflation, and more than one income source. No single product hits all three.

Fixed deposits are safe but lose to inflation after tax. Bonds via Jiraaf pay 8-15%, which beats most FDs. Demat accounts on AngelOne or 5paisa get you into the market cheap. But they all require you to have money first. This is where the conversation usually dies. It shouldn't.

If you want real numbers on splitting ₹10 Lakh across these, we did the math here: maximizing ₹10 Lakh returns with FDs, bonds, and GroMo side income.

Why Capital Alone Fails Many Investors

If you don't have ₹5-10 lakh sitting idle, standard advice ignores you. That's most working professionals, students, and homemakers. For this group, the "best" plan starts with earning, not investing.

GroMo works differently. You don't put money in. You help people open demat accounts or apply for credit cards, and you get paid. You aren't risking capital you're using your network. Earning ₹800-₹3,500 per referral on products like Kotak 811 or SBM Novio cards gives you real seed money to start investing.

This isn't hypothetical. We showed how ₹50k can grow to ₹1 lakh in a year with GroMo.

Building a Portfolio: The Allocation

Split your money four ways: emergency cash, growth investments, market exposure, and active earning. This covers your downside while letting you chase better returns.

Bucket | Allocation | Example Instruments | Purpose |

|---|---|---|---|

Emergency Fixed Income | 20-25% | FDs, Jiraaf FD marketplace | Safety, liquidity |

Growth Bonds | 15-20% | Jiraaf Bonds (8-15% p.a.) | Predictable higher return |

Market Exposure | 25-30% | AngelOne, 5paisa, Motilal Oswal Demat | Long-term wealth |

Active Income | 25-30% | GroMo commissions | Cash flow, no capital lock-in |

See GroMo in that table? It's not a footnote. It's a real income category. Traditional planning ignores this completely. For millions without savings, it's often the only accessible option.

We go deeper on mixing active and passive income here: Active & Passive Income: GroMo Merges Both for Indians 2026.

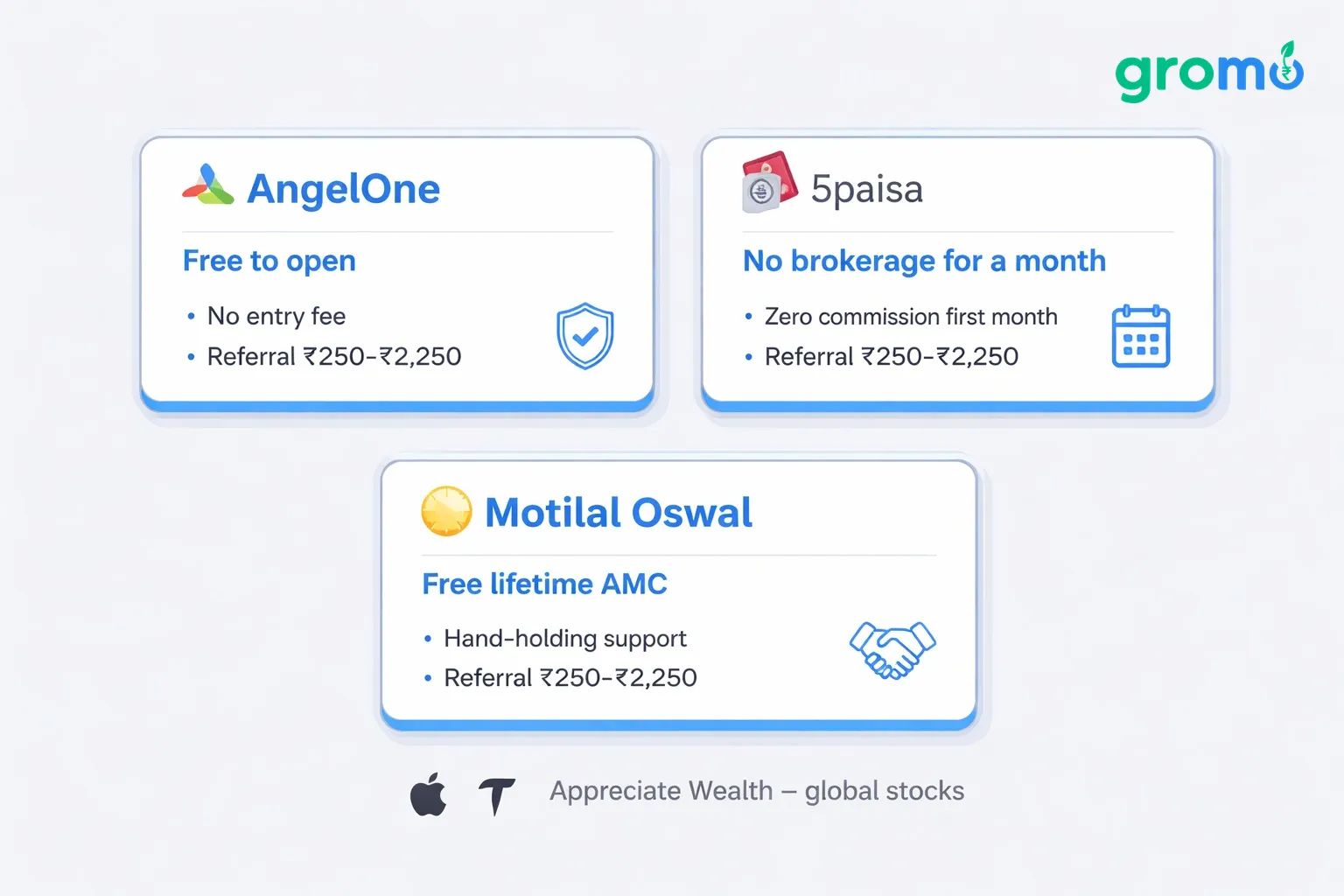

Demat Accounts: Getting Started

Demat accounts get a bad rap. People are scared to open them, or they open five and drown in AMC fees.

They aren't all the same. AngelOne is free to open. 5paisa has no brokerage for a month. Motilal Oswal is an old-school firm with free lifetime AMC if you want hand-holding. Appreciate Wealth lets you buy Apple and Tesla if you want global stocks.

Also, all of these are GroMo products. You can use them, or refer them to earn ₹250-₹2,250 per account. You rarely hear that in standard advice.

Our guide on Top Indian Investments 2026 & Zero-Capital Earnings with GroMo covers this shift.

Fixed Income vs Market Risk

Fixed income is for the cautious. Market-linked is for people with time and patience. A 2026 plan doesn't choose one. It uses both, based on how old you are and how steady your paycheck is.

Young and employed? Take market risk. Older or irregular income? Stick to bonds and FDs for the 8-15% returns. GroMo fits both. The extra cash funds your investments regardless of your risk appetite.

Read our comparison: Fixed Income vs GroMo: Hybrid Earnings Strategy 2026.

Common Mistakes

People chase returns they can't afford. They invest in risky assets without an emergency fund. Or they never start because they think they need a lakh to "start properly."

The usual suspects:

Opening too many demat accounts and paying useless fees

Forgetting lock-in periods and getting stuck

Ignoring credit scores before applying for cards

Treating earning and investing as separate sports

Waiting for a big lump sum to begin

You don't need a lakh. You need ₹100 for an SIP. Or you start earning on GroMo with zero down and fund your investments from there.

For a longer roadmap, see the Realistic ₹1 Crore Investment Plan with Zero Capital.

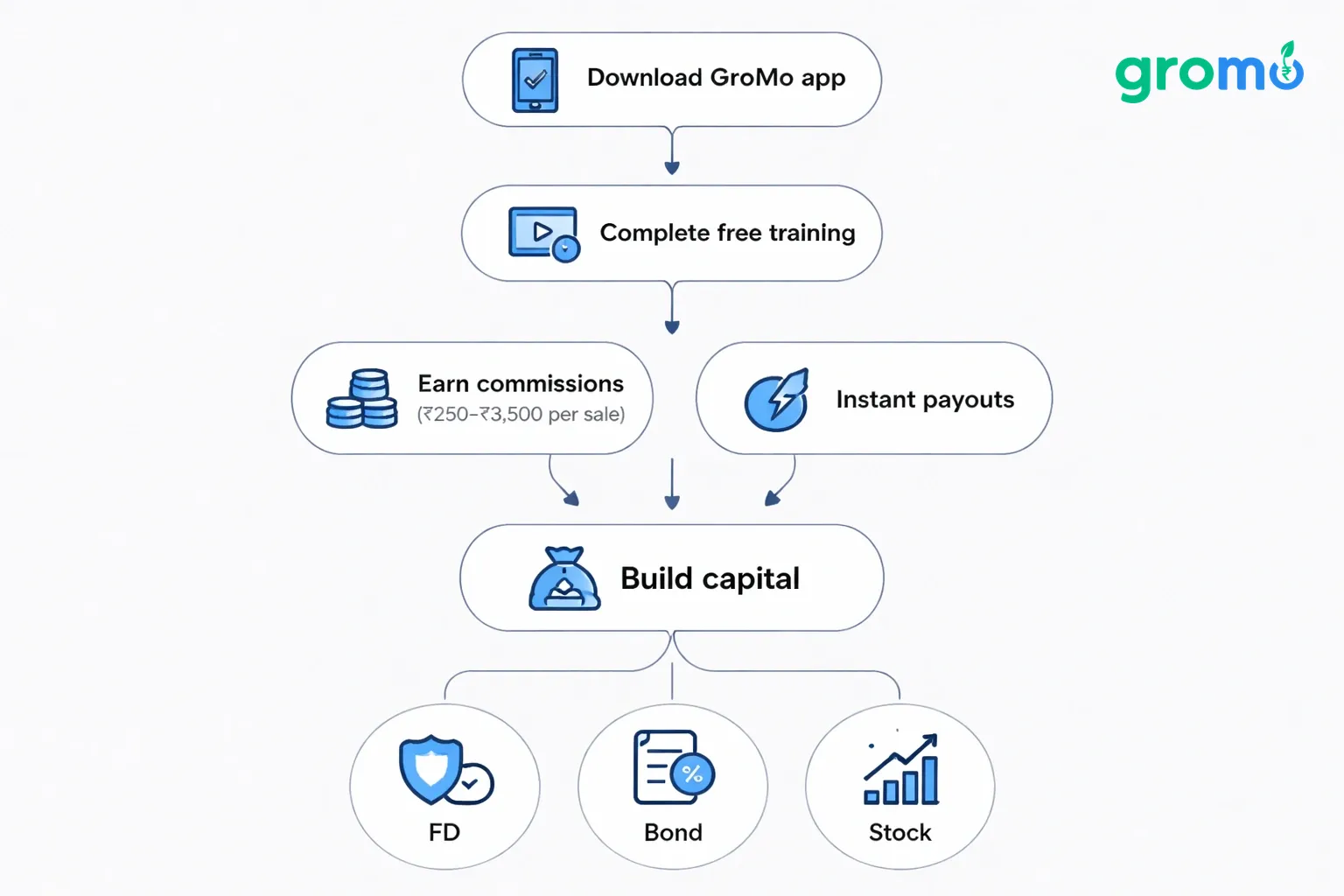

How GroMo Fits

GroMo is the income engine, not the investment. You build capital through commissions, then shove that capital into FDs, bonds, or stocks. No savings required.

It's straightforward. Download the app, do the free training, share links. You get paid per sale ₹250 for a Motilal Oswal Demat, up to ₹3,500 for an SBM Novio Credit Card. No inventory. No office. Payouts are instant.

This removes the biggest wall: not having money. You can generate your investment starter kit in weeks, not years.

Check out Multiple Income Streams in 2026: GroMo Referrals & More. Or bookmark our main guide: Passive Income 2026: GroMo Earnings Without Clocking In.

The Bottom Line

The best investment plan in 2026 isn't a magic product. It's a system. Safe fixed income, market access via demats, and GroMo income that costs nothing to start.

Start small. Pick one fixed-income option and one market account. Commit to GroMo for 90 days. Watch your numbers. Reinvest a chunk. That's how wealth gets built not by hunting for the one "best" product.

Frequently Asked Questions

Q: What is the best investment plan for someone with no savings in 2026?

A: Start with GroMo. Zero investment required. Use the commissions to fund small SIPs or bonds later.

Q: Are bonds better than fixed deposits in 2026?

A: Bonds on Jiraaf offer 8-15% returns, usually beating FDs. But they carry market risk. FDs are guaranteed. It depends on your comfort with risk.

Q: Do I need a large amount to open a demat account?

A: No. AngelOne, 5paisa, and Motilal Oswal offer free or near-free opening. You might need a small first trade, but no large capital.

Q: How does GroMo help without capital?

A: You earn commissions by referring products like credit cards and demat accounts. That income becomes your starting capital.

Q: Is relying on referral income risky?

A: GroMo income isn't market-linked, so it has no investment risk. It's supplementary income best used alongside traditional investments.

Q: How much can I realistically earn monthly with GroMo?

A: Depends on effort. Active partners moving cards and accounts regularly can earn from ₹10,000 to over ₹1 lakh monthly.