Mutual Fund Distribution Commissions in India 2026

The mutual fund industry in India is growing, and the commission structure for distributors is straightforward once you understand it. Here's how it works in 2026.

What Distributors Actually Do

Distributors connect AMCs (Asset Management Companies) with investors. You help people pick funds and complete the investment process. The AMC pays you not the investor.

This used to require AMFI certification, office space, and relationships with multiple fund houses. After 2013's direct plan regulations and the rise of apps like GroMo, the barrier to entry dropped. Now anyone with a phone can distribute.

Start Earning from Mutual Fund Distribution Today

Two Ways You Get Paid

Upfront Commission

One-time payment when someone invests a lump sum or starts a SIP. Usually 0.5% to 2.5% of the amount. Depends on the fund type (equity pays more), the AMC, and your distributor level.

Example: ₹1 lakh in an equity fund at 1.5% = ₹1,500 in your pocket immediately.

Trail Commission

This is where the money builds. You get paid annually (sometimes quarterly) as long as the investor stays in the fund. Typically 0.25% to 1% per year of AUM.

₹10 lakhs invested at 0.75% trail = ₹7,500/year

Over 10 years, that's ₹75,000 from one client

Trail is why this business compounds. Side income opportunities with recurring revenue are rare.

Commission Rates by Fund Type

Fund Category | Upfront | Trail (Annual) |

|---|---|---|

Equity | 1.0% - 2.5% | 0.50% - 1.00% |

Debt | 0.25% - 1.0% | 0.10% - 0.50% |

Hybrid | 0.50% - 1.5% | 0.30% - 0.75% |

Liquid | 0.10% - 0.25% | 0.05% - 0.15% |

ELSS | 1.0% - 2.0% | 0.50% - 1.00% |

Equity pays more because it's harder to sell and has higher expense ratios. Liquid funds are simple products with thin margins.

Realistic Earnings

I'm skeptical of income claims in most side-hustle articles, so here are grounded numbers based on typical conversion rates:

Months 1-6

20-30 clients

₹10-15 lakhs AUM

Trail: ₹625-937/month

Upfront from new SIPs: ₹2,000-5,000

Total: ₹2,600-6,000/month

Year 1-2

100-150 clients

₹1.5-2.25 crores AUM

Trail: ₹9,000-14,000/month

Upfront: ₹8,000-15,000

Total: ₹17,000-29,000/month

Year 3+

300-500 clients

₹9-15 crores AUM

Trail: ₹56,000-94,000/month

Upfront: ₹20,000-35,000

Total: ₹76,000-1,28,000/month

GroMo claims 60 lakh partners and has paid out ₹100 crores. Those numbers suggest the model works, though individual results vary wildly.

How GroMo Changed Distribution

Old model: Get AMFI certified, file paperwork, build relationships with 20+ AMCs, wait 45 days for payouts.

GroMo model: Download app, complete training, sell any fund on the platform, get paid instantly.

The app handles:

Commission tracking (real-time)

Payouts (immediate vs. traditional 30-45 days)

Multi-AMC access (Aditya Birla, others in one place)

Paperwork (fully digital onboarding)

Specific Example: Aditya Birla SIP on GroMo

Offer: ₹400 upfront per first SIP activation

Conditions:

Minimum ₹100 SIP

Must run 3 months

Clawback: If the customer cancels before 3 months, you lose the ₹400. This prevents gaming the system with fake signups.

Customer process:

Click your referral link

Download Appreciate app

Sign up (name + mobile)

KYC (PAN + Aadhaar)

Verify bank + email

Select "Indian Mutual Funds" → ABSL

Set up ₹100+ SIP

You get ₹400

Simple enough that people genuinely earn ₹10K-₹1L monthly from this flow.

Join 60L+ Partners Earning with GroMo

What Actually Works

Don't Wait for Referrals

Week 1: Find 10 prospects in your network

Week 2: Explain SIPs (use GroMo's training)

Week 3: Help them choose based on goals

Week 4: Close and follow up

Repeat. You'll land 40+ clients per quarter if you're consistent.

Push SIPs Over Lump Sums

SIPs are easier sells (₹1,000/month feels doable; ₹50,000 lump sum doesn't). They also generate ongoing trail and have better retention people set them and forget them.

Lead with Education

Customers who understand what they're buying stay invested. That means more trail for you and better referrals. Share financial planning content before you pitch products.

The Compliance Guardrails

Without SEBI RIA License, You Cannot:

Recommend specific schemes

Promise returns

Charge advice fees

Invest on someone's behalf

Split commissions with clients

You Must:

Complete KYC properly

Protect customer data

Disclose commission arrangement

Follow platform rules (like the 3-month SIP maintenance)

Violations get your wallet blocked or trigger legal issues. Platforms enforce this strictly.

Why Mutual Funds Alone Is Limiting

GroMo lets you sell other products:

Credit cards: ₹500-₹3,000 per approval (HDFC cards do well)

Savings accounts: Kotak 811 pays ₹550-₹800

Demat: ₹250-₹1,400 per account

Loans: 0.5%-3.5% of disbursed amount (business loans included)

Cards and loans pay more upfront. Mutual funds pay less now but compound. Mixing both gets you to ₹1 lakh monthly faster.

The Friction Points

Trust is hard

Reality: People are skeptical of someone suddenly pitching investments. Lead with education, not products. Share useful content first.

Markets drop

Reality: Clients will panic. Focus them on SIP discipline and long-term horizons. Rupee-cost averaging is your talking point.

First 50 clients are slow

Reality: Expect to grind for months. After ~50 clients, referrals and trail income start compounding.

Competition exists

Reality: Robo-advisors and direct plans compete with you. Your edge: availability and personalized help.

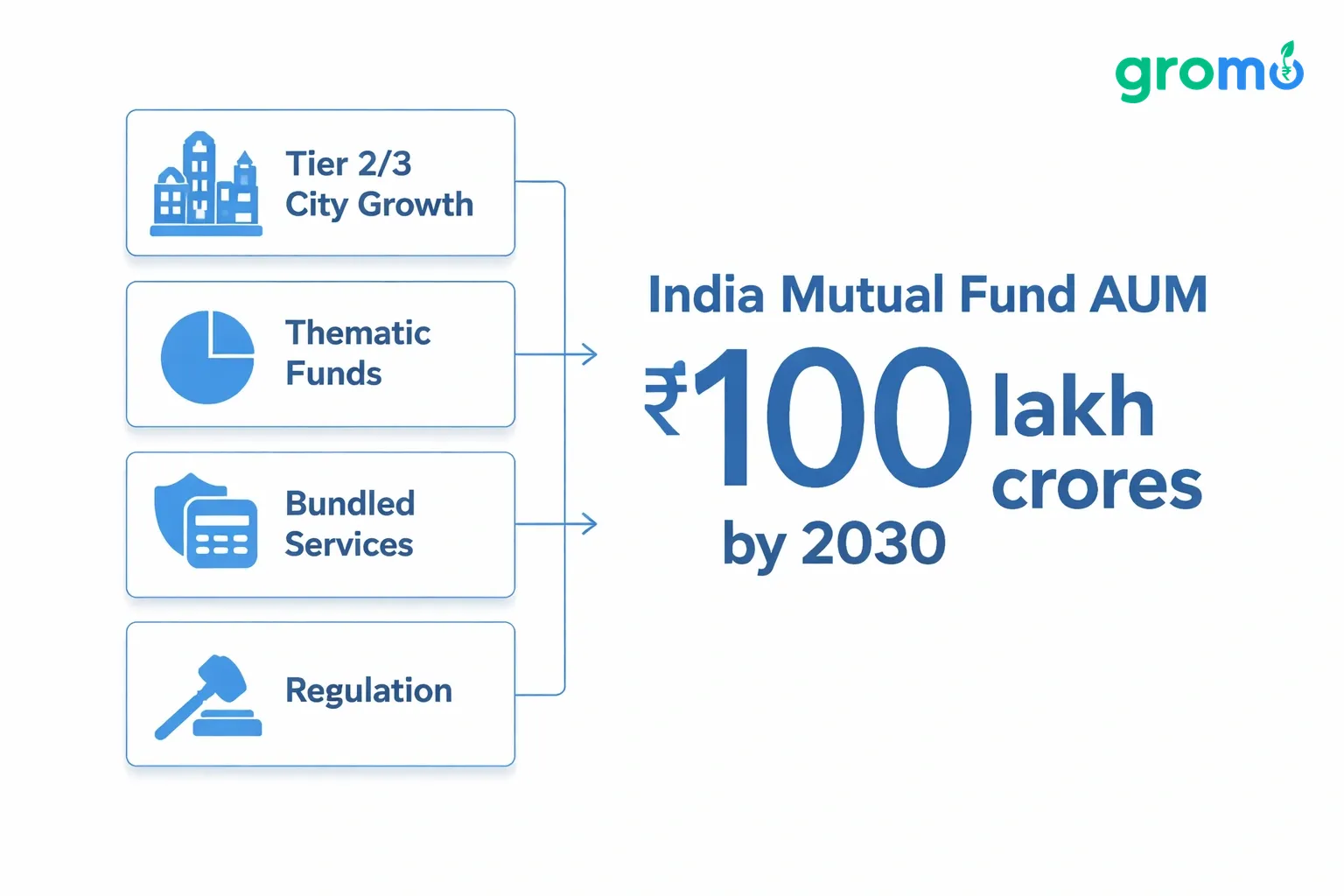

Where This Is Going

India's mutual fund AUM is projected at ₹100 lakh crores by 2030. That's the macro case for entering now.

Trends:

Tier 2/3 cities: Internet penetration is opening new markets. Rural distribution is growing.

Thematic funds: Young investors want sector-specific exposure (tech, healthcare, ESG).

Bundled services: The winning distributors offer insurance, cards, and loans alongside funds exactly what GroMo's platform enables.

Regulation: SEBI tightens rules periodically. Stay compliant or get squeezed out.

A Realistic Timeline

Month 1

Download GroMo, finish training modules

Learn the fund categories

Practice explaining SIPs to friends (badly at first, then better)

Month 2

Pitch family, friends, colleagues

Target people who save but don't invest

Start them small (₹500-₹1,000 SIPs)

Expect rejections, learn from them

Month 3

Ask satisfied clients for intros

Try social media

Aim for 20-30 active clients

Months 4-6

Add 15-20 clients monthly

Trail income starts appearing

Layer in credit cards/demat for upfront cash

Target ₹25,000-₹50,000 total

Month 6+

100+ clients

Trail grows on autopilot

Consider referral programs to scale

₹1 lakh+ monthly becomes mathematically possible

Why GroMo Specifically

60 lakh partners. ₹100 crores paid. The numbers suggest it's not a scam.

Zero entry cost: No office, no capital

Instant payouts: Cash flow matters when you're starting

Training: Free, actually useful

Brand access: Major AMCs and banks in one app

Tech stack: Mobile-first, compliance built-in

Bottom Line

Mutual fund distribution works because trail income compounds. The clients you bring in this year pay you for years.

The apps removed the old friction. You don't need an office or certification to start just consistency. The first months are slow. Then it accelerates.

If you're going to try this, download GroMo, finish the training, and help one person start a SIP. See if the process clicks. Then decide if you want to scale.

FAQs

Q: AMFI certification required?

A: No. You can facilitate and earn without it. You just can't recommend specific schemes without an RIA license. Stick to facilitation.

Q: Realistic month-one income?

A: ₹2,000-₹5,000 if you help 5-10 people start SIPs. Trail is negligible early on. By month 3-4, ₹10,000-₹15,000 is realistic.

Q: What if a client withdraws early?

A: Within the clawback period (typically 3 months), your commission gets reversed. After that, you keep it. This is why client education matters set expectations for medium to long-term.

Q: New vs. existing investments?

A: Upfront only on new. Trail continues as long as they stay invested. One good client can pay you for a decade.

Q: Mutual funds vs. cards/loans?

A: Cards/loans pay more upfront. Mutual funds build recurring income. Do both.

Q: Taxes?

A: Business income. Declare in ITR. GroMo tracks payouts, so record-keeping is easier. Talk to a CA once income grows.