Motor Insurance Meaning: Exhaustive Guide

Motor insurance meaning is a crucial aspect of vehicle ownership, providing financial protection against potential damages or losses

Motor insurance meaning is a crucial aspect of vehicle ownership, providing financial protection against potential damages or losses. In this comprehensive guide, we'll cover the essentials of motor insurance, including types, coverage, factors affecting premiums, and claims process.

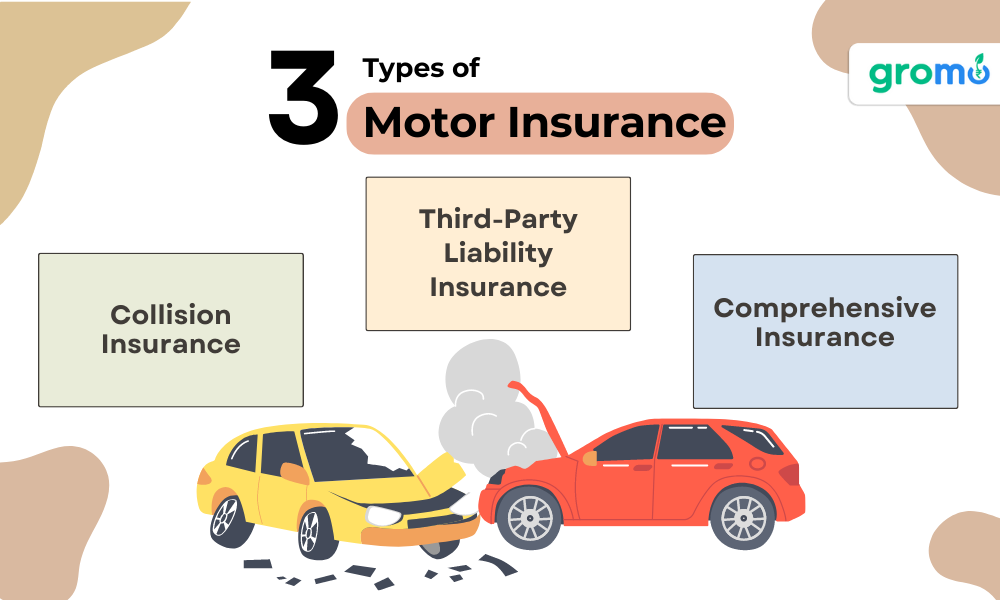

Types of Motor Insurance

There are three main types of motor insurance:

Third-Party Liability Insurance: This type of insurance covers the policyholder's legal liability for damages caused to a third party, including bodily injury, death, or property damage.

Collision Insurance: Collision insurance covers the costs of repairing or replacing the policyholder's vehicle following an accident, regardless of fault.

Comprehensive Insurance: Comprehensive insurance offers the broadest coverage, including third-party liability, collision, and additional coverage for damages resulting from events such as theft, vandalism, fire, or natural disasters.

Third-Party Liability Insurance

Third-Party Liability Insurance is mandatory in most countries and offers the following coverage:

-

Bodily Injury Liability: Covers medical expenses, lost wages, and other costs related to injuries sustained by a third party in an accident caused by the policyholder.

-

Property Damage Liability: Covers the cost of repairing or replacing a third party's property damaged in an accident caused by the policyholder.

Collision Insurance

Collision insurance coverage includes:

Vehicle Repair: Covers the cost of repairing the policyholder's vehicle after an accident, up to its actual cash value.

Vehicle Replacement: Provides compensation for a total loss, based on the vehicle's actual cash value.

Comprehensive Insurance

Comprehensive insurance offers extensive coverage, including:

-

Theft: Covers the cost of replacing the policyholder's vehicle if it is stolen.

-

Vandalism: Covers the cost of repairing damages caused by vandalism.

-

Fire: Covers the cost of repairing or replacing the policyholder's vehicle in case of fire damage.

-

Natural Disasters: Covers damages caused by events such as floods, storms, or earthquakes.

Factors Affecting Motor Insurance Premiums

Several factors can influence the cost of motor insurance premiums, including:

Vehicle Make and Model: High-value or high-performance vehicles typically have higher insurance premiums due to their increased repair or replacement costs.

Driver's Age: Younger drivers may face higher premiums due to their lack of driving experience and increased risk of accidents.

Driving Record: Drivers with a history of accidents, violations, or claims may be considered high-risk and face higher insurance premiums.

Location: Areas with higher crime rates or greater exposure to natural disasters can result in higher insurance premiums.

Deductibles: Choosing a higher deductible, which is the amount the policyholder pays out-of-pocket before the insurance coverage kicks in, can lower the premium.

Sell financial products with the help of the GroMo app and earn as much as you can with each product

Motor Insurance Claims Process

The motor insurance claims process typically involves the following steps:

Report the Accident: Immediately contact your insurance provider to report the accident and provide relevant details, such as the date, time, location, and parties involved.

Gather Documentation: Collect necessary documents, such as a police report, photographs of the accident scene, and repair estimates.

File a Claim: Complete and submit the required claim forms to your insurance provider, along with the supporting documentation.

Claim Investigation: The insurance provider will investigate the claim to verify the details, assess liability, and determine the compensation amount.

Claim Settlement: Once the claim is approved, the insurance provider will issue the compensation payment, either directly to the policyholder or to the repair facility.

By understanding the various types of motor insurance, coverage options, factors affecting premiums, and the claims process, vehicle owners can make informed decisions and ensure they have adequate protection against potential risks and financial losses associated with vehicle ownership.

Tips for Choosing the Right Motor Insurance Policy

Selecting the right motor insurance policy is essential for securing the best coverage at an affordable price. Consider these tips when choosing a motor insurance meaning policy:

-

Assess Your Needs: Determine the level of coverage you require based on factors such as the value of your vehicle, the likelihood of theft or damage, and your financial situation.

-

Compare Policies: Research and compare different motor insurance policies, taking note of their coverage, premiums, and any additional benefits or discounts.

-

Read the Fine Print: Carefully review the policy's terms and conditions, exclusions, and limitations to ensure you fully understand the coverage and your responsibilities as a policyholder.

-

Choose a Reputable Insurer: Select a reputable insurance provider with a strong financial rating and a history of reliable customer service.

-

Review Your Policy Regularly: Regularly review your motor insurance policy and update your coverage as needed, particularly when your circumstances change, such as purchasing a new vehicle or relocating.

Ways to Lower Your Motor Insurance Premiums

Reducing motor insurance premiums can result in significant cost savings. Here are some strategies to lower your motor insurance premiums:

-

Maintain a Clean Driving Record: A history of safe driving can lead to lower premiums, as insurers view responsible drivers as less likely to file claims.

-

Increase Your Deductible: Opting for a higher deductible can result in lower insurance premiums, but ensure you can afford the out-of-pocket expenses in the event of a claim.

-

Bundle Insurance Policies: Combining your motor insurance meaning with other insurance policies, such as homeowners or renters insurance, can result in discounts from your insurance provider.

-

Take Advantage of Discounts: Look for discounts offered by insurers, such as safe driver, low mileage, or multi-vehicle discounts, and ensure you meet the eligibility requirements.

-

Improve Your Vehicle's Security: Installing anti-theft devices, such as alarms or tracking systems, can reduce the risk of theft and potentially lower your insurance premiums.

GO CHECK OUT!!

- 7 Guaranteed Ways To Improve Your CIBIL Score

- How To Apply For A Personal Loan With Low CIBIL Score?

- How To Apply For A Home Loan With Low CIBIL Score?

- Earn Commission By Selling Credit Cards Online

Importance of Motor Insurance for Legal Compliance and Financial Protection

Having motor insurance is not only a legal requirement in most jurisdictions but also crucial for protecting your financial well-being in the event of an accident or loss. Motor insurance provides:

-

Legal Compliance: Adhering to the mandatory insurance requirements in your area can help you avoid fines, penalties, or license suspension.

-

Financial Protection: Motor insurance can cover the costs of vehicle repair, replacement, or third-party liability, preventing significant financial strain or debt.

-

Peace of Mind: Knowing you have adequate motor insurance coverage can alleviate stress and provide peace of mind while driving.

Understanding motor insurance is essential for vehicle owners to make informed decisions about their coverage and protect themselves against potential financial losses. By assessing your needs, comparing policies, and taking advantage of cost-saving strategies, you can secure the right motor insurance policy at an affordable price.

Motor Insurance Exclusions and Limitations

It's important to be aware of common exclusions and limitations in motor insurance policies, as these can affect your coverage and claims. Some typical exclusions and limitations include:

-

Intentional Damage: Motor insurance policies generally do not cover damages resulting from intentional acts, such as vandalism or arson, committed by the policyholder.

-

Driving Under the Influence: Accidents or damages caused while the policyholder is driving under the influence of alcohol or drugs are typically not covered.

-

Unlicensed or Unauthorized Drivers: Coverage may not apply if the vehicle is driven by an unlicensed driver or someone not authorized under the policy.

-

Commercial Use: If the insured vehicle is used for commercial purposes, such as ride-sharing or delivery services, standard motor insurance policies may not provide coverage.

-

Wear and Tear: Regular wear and tear, mechanical breakdowns, or tire damage are generally not covered under motor insurance policies.

Understanding these exclusions and limitations can help you make informed decisions about your coverage and avoid surprises during the claims process.

Navigating the Motor Insurance Claims Process Effectively

To ensure a smooth motor insurance claims process, follow these tips:

Know Your Policy: Familiarize yourself with your motor insurance policy's coverage, exclusions, and limitations to understand what is covered and your responsibilities during the claims process.

Document the Accident: Take photographs of the accident scene, damages, and any relevant documents, such as police reports or witness statements, to support your claim.

Stay Organized: Keep all claim-related documents and correspondence organized and easily accessible.

Communicate with Your Insurer: Maintain open communication with your insurance provider and promptly respond to their requests for information or documentation.

Monitor the Claim Status: Regularly check the status of your claim and follow up with your insurer if necessary to ensure timely resolution.

By following these tips, you can navigate the motor insurance claims process more effectively and increase the likelihood of a successful outcome.

The Role of Motor Insurance in Accident Recovery

Motor insurance plays a vital role in accident recovery by providing financial assistance for vehicle repairs, medical expenses, and other costs associated with an accident. The benefits of motor insurance in accident recovery include:

-

Vehicle Repair or Replacement: Motor insurance can cover the costs of repairing or replacing your vehicle, helping you get back on the road faster.

-

Medical Expense Coverage: If your motor insurance policy includes personal injury protection or medical payments coverage, it can help cover medical expenses for you and your passengers after an accident.

-

Legal Protection: In the event of a lawsuit resulting from an accident, motor insurance can provide legal defense and cover any court-ordered judgments or settlements.

-

Third-Party Liability Coverage: Motor insurance can protect you from the financial consequences of damages or injuries caused to third parties in an accident.

By offering financial protection and support during accident recovery, motor insurance can alleviate some of the burdens associated with vehicle accidents and help you regain your footing more quickly.

Motor insurance is an essential component of responsible vehicle ownership, providing financial protection and peace of mind in the event of accidents or losses. By understanding the various types of motor insurance, coverage options, factors affecting premiums, and the claims process, vehicle owners can make informed decisions and ensure they have adequate protection against potential risks and financial losses associated with vehicle ownership.

Importance of Motor Insurance for Road Safety

Motor insurance not only offers financial protection but also promotes road safety by encouraging responsible driving habits. Here's how motor insurance contributes to road safety:

-

Incentivizing Safe Driving: Since a clean driving record can result in lower insurance premiums, policyholders are incentivized to maintain safe driving habits and avoid accidents or traffic violations.

-

Encouraging Vehicle Maintenance: Properly maintaining a vehicle can prevent accidents caused by mechanical failures. Some motor insurance policies offer discounts for well-maintained vehicles or those equipped with safety features, encouraging vehicle owners to prioritize maintenance and safety.

-

Supporting Accident Recovery: Motor insurance can help cover the costs of medical treatment and vehicle repair after an accident, ensuring that injured parties receive proper care and that damaged vehicles are repaired or replaced, reducing the risk of further accidents caused by unsafe vehicles.

-

Promoting Financial Responsibility: By requiring vehicle owners to have motor insurance, governments promote financial responsibility and ensure that drivers can cover the costs associated with accidents, reducing the likelihood of disputes or uninsured drivers on the road.

By encouraging responsible driving, vehicle maintenance, and financial responsibility, motor insurance plays a critical role in promoting road safety and reducing the risk of accidents.

The Role of Motor Insurance in Economic Stability

Motor insurance plays a significant role in maintaining economic stability by providing a safety net for individuals, businesses, and the broader economy. The economic benefits of motor insurance include:

-

Reducing Financial Burdens: By covering the costs associated with accidents or losses, motor insurance prevents individuals and businesses from facing significant financial strain, ensuring they can continue to contribute to the economy.

-

Supporting the Auto Industry: Motor insurance claims often result in vehicle repairs or replacements, which generates revenue for the auto industry, including manufacturers, dealerships, and repair shops.

-

Promoting Employment: The motor insurance industry provides employment opportunities in various sectors, such as sales, customer service, claims management, and underwriting, contributing to overall employment levels and economic growth.

-

Facilitating Economic Activity: Motor insurance allows individuals and businesses to use their vehicles with confidence, knowing they are protected against potential losses. This enables the transportation of goods, services, and people, promoting overall economic activity.

-

Risk Management: Motor insurance helps individuals and businesses manage the risks associated with vehicle ownership, promoting economic stability by reducing the likelihood of unforeseen financial losses.

By providing financial protection, supporting various industries, and facilitating economic activity, motor insurance plays a crucial role in maintaining economic stability at both the individual and macro levels.

CHECK OUT!

- Best Selling Credit Cards in India

- Earn Commission By Selling Credit Cards Online

- Are You Aware Of The Benefits That Come Along With A High CIBIL Score?

- 7 of the Best Money-Making Apps of 2022

Motor Insurance Policy Renewal: Factors to Consider

When it's time to renew your motor insurance policy, consider the following factors to ensure you have adequate coverage at the best possible price:

Review Your Coverage: Assess your current coverage to determine if it still meets your needs, considering any changes in your circumstances, such as purchasing a new vehicle or relocating.

Compare Quotes: Obtain quotes from multiple insurance providers to compare coverage options, prices, and potential discounts.

Check for Discounts: Inquire about any discounts you may be eligible for, such as safe driver, low mileage, or multi-policy discounts, and ensure they are applied to your policy.

Examine Customer Reviews: Research customer reviews and ratings for the insurance providers you are considering to gain insight into their customer service, claims handling, and overall satisfaction.

Evaluate Payment Options: Consider the available payment options, such as monthly or annual payments, and select the one that best suits your budget and financial situation.

By taking these factors into account when renewing your motor insurance policy, you can ensure you have the right coverage at a competitive price.

Motor insurance is an essential aspect of responsible vehicle ownership, providing financial protection, promoting road safety, and supporting accident recovery. By understanding the various types of motor insurance, coverage options, factors affecting premiums, and the claims process, as well as the broader economic implications of motor insurance, vehicle owners can make informed decisions and secure adequate protection against potential risks and financial losses.

KEY TAKEAWAYS

-

Motor insurance meaning offers financial protection against damages, injuries, and liabilities arising from vehicle-related incidents.

-

Coverage types include comprehensive, third-party, and third-party fire and theft, each providing varying levels of protection.

-

Premiums are influenced by factors like vehicle type, driver's age, driving history, and location.

-

No-claims bonuses reward safe drivers with reduced premiums over time, promoting responsible driving.

-

Understanding policy exclusions and comparing plans helps ensure the best possible coverage for your unique needs and budget.