Loans for Low Credit Scores in India 2026: Options & Tips

Getting a loan with a low credit score feels like hitting a wall. Banks see anything below 750 and the door slams shut. But here's the thing: a low score doesn't mean you're out of options. It just means you have to look in different places.

The Reality of Credit Scores in India

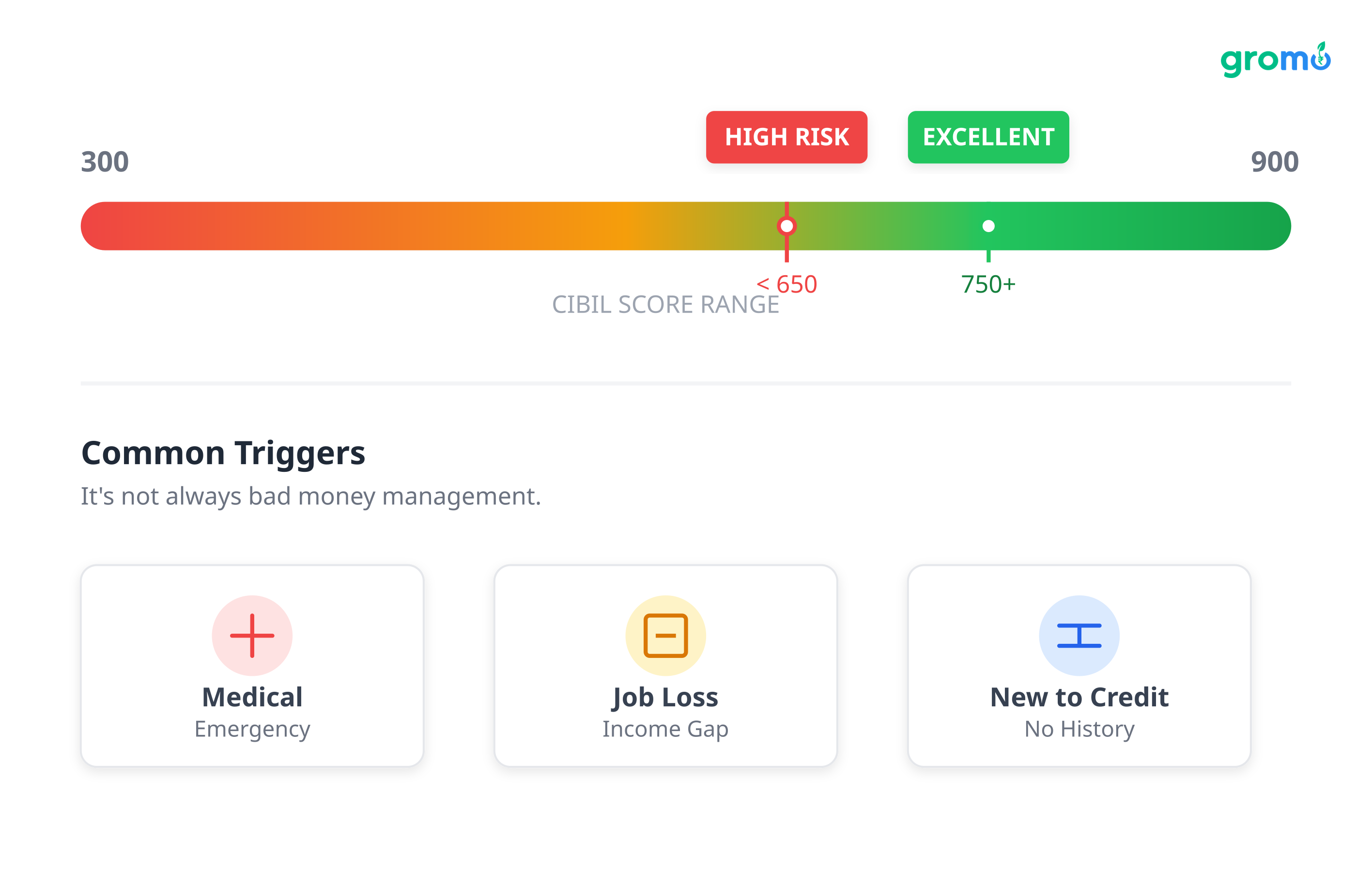

Think of your credit score as a financial report card. In India, CIBIL scores run from 300 to 900. Lenders love 750+. Anything below 650 gets stamped "high risk."

This doesn't mean you're bad with money. A medical emergency, a job loss, or just being new to credit can wreck your score almost overnight.

Why Scores Tank

Usually, it's one of these:

Late payments. Missing an EMI hurts. A single 30-day delay can shave off 50-80 points.

High utilization. If you're using more than 70% of your credit card limit, lenders get nervous. A ₹80k balance on a ₹1 lakh limit is a red flag.

Too many applications. Every time you apply for credit, there's a "hard inquiry." Four to seven of those in six months makes you look desperate.

Thin history. Being new to credit means you have no track record. Lenders hate guessing.

Settlements. Settling a debt for less than you owe? That stays on your report for years.

Where to Actually Get a Loan in 2026

Fintech has changed the game. You won't get prime rates, but you can get money.

Small Loans (₹5,000 - ₹30,000)

For immediate needs, RBI-regulated NBFCs are focusing on micro-loans:

PaapaPay: They lend ₹500 to ₹20,000 with just PAN and Aadhaar. They look at your current income, not your past mistakes. Money lands in your account in 10 minutes.

My Money Bazaar: Goes up to ₹30,000. They're lenient on scores and don't make you jump through hoops.

Smartcoin: Offers up to ₹1 lakh. They work with self-employed people and those without salary slips useful if your income is steady but your credit history isn't.

Mid-Range Loans (₹50,000 - ₹2,50,000)

Need more? These platforms have wider criteria:

Tez Credit: Accepts a minimum salary of just ₹18,000. They cover 8,000+ pincodes. You need PAN, Aadhaar, and salary proof.

Ram Fincorp: Flexible repayment up to 3 months, no foreclosure charges. They do a video KYC and disburse within 24 hours.

Moneyview: They're known for working with people in the 600-700 range.

The Cost of Borrowing

Let's be honest: these loans are expensive. A 780 score might get you 11% interest. A 600 score? You're looking at 18-24%. Lenders charge more because they're taking a risk.

To survive this:

Borrow the minimum, not the maximum.

Pick the shortest tenure you can handle.

Never miss a payment. One slip-up can undo months of work.

Read the fine print. Hidden fees add up.

When Unsecured Isn't an Option

If even the flexible lenders say no, try secured loans.

Loans Against FD: Borrow against your Fixed Deposit. The rate is low (1-2% above your FD rate), and your credit score barely matters because the deposit secures the loan.

Gold Loans: The classic fallback. You get liquidity fast (usually 75% of the gold's value) without a credit check.

Peer-to-Peer Lending: P2P sites match you with individuals willing to lend. Some are okay with higher risk for a better return.

Watch Out for Sharks

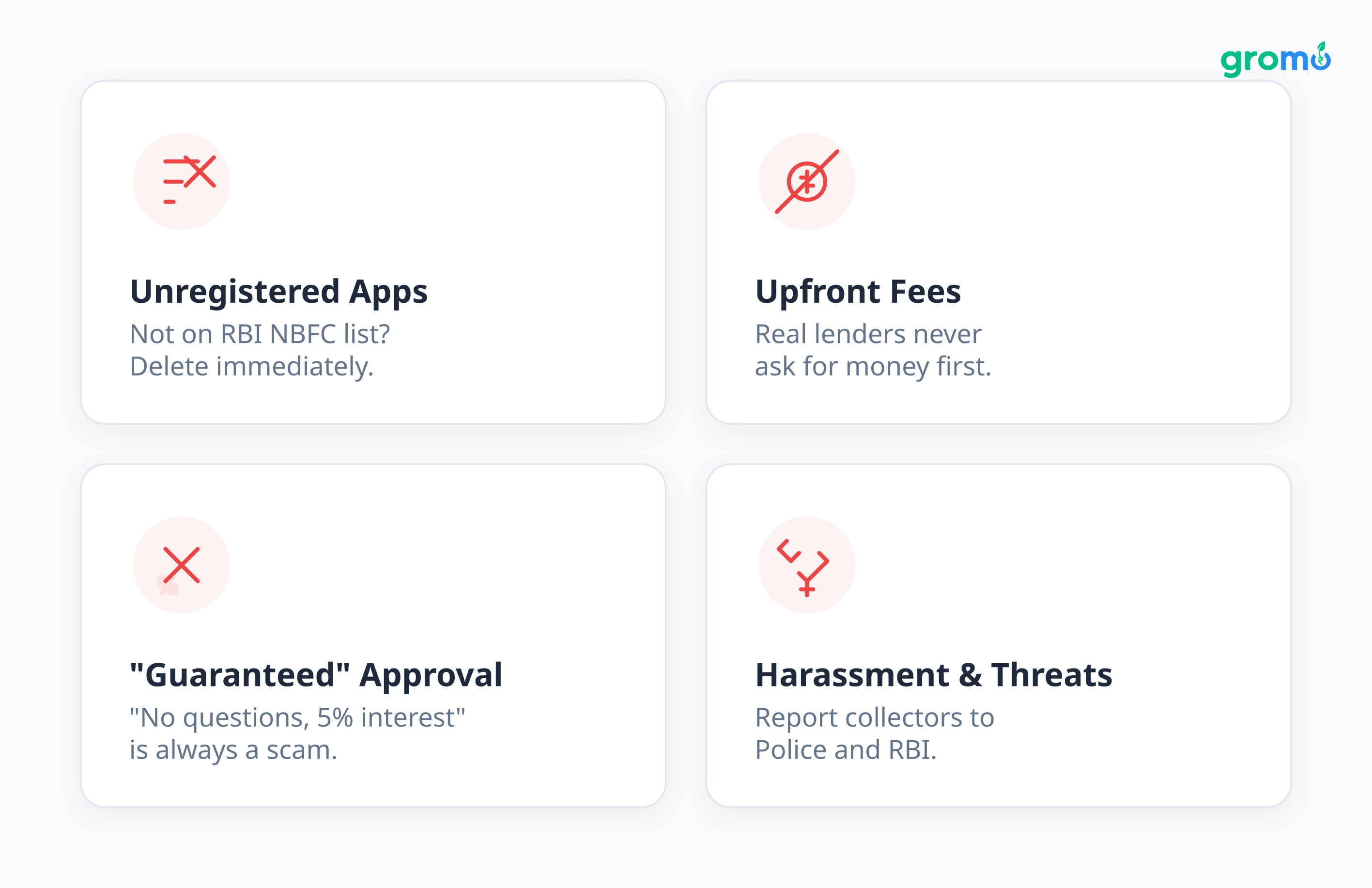

Desperate borrowers get targeted. Avoid these traps:

Unregistered apps: Check the RBI's NBFC list. If the app isn't there, delete it.

Upfront fees: Real lenders don't ask for money before giving you a loan.

"Guaranteed" approvals: "No questions asked, 5% interest" is a scam. Real lenders verify everything.

Threats: If collectors harass you or call your family, report them to the police and RBI.

We've written a full guide on RBI-approved loan apps to help you sort the legit ones from the predators.

The Strategy: Use the Loan to Fix the Score

Don't just take the money use it to rebuild trust.

Borrow small. Take ₹50,000 even if you qualify for ₹2 lakh. It's easier to manage.

Automate. Set up auto-debit so you never forget an EMI.

Lower utilization. Get your credit card balance below 30% of the limit.

Stop applying. Don't apply for new credit for at least 3-6 months.

Check your report. Errors happen. Dispute them immediately.

If you want the step-by-step, our post on how to improve your credit score breaks it down with timelines.

Earning While You Repair

Here's a thought: while you're fixing your credit, why not make more money?

More income means faster repayment. But if you're already working, "get a second job" is useless advice. That's where selling financial products comes in.

GroMo lets you earn commissions by helping people get credit cards, loans, and savings accounts. You do it from your phone, on your own time. No investment needed.

You're already learning about loans to help yourself. That knowledge is valuable. Why not share it? If your friends need a credit card or a savings account, refer them.

The math is simple:

Credit card referrals: ₹500-₹1,700 per approval.

Personal loan referrals: 0.5%-3.5% of the loan amount.

Demat/Savings accounts: ₹100-₹1,400 per account.

Help 10 people get a credit card this month? That's an extra ₹5,000-₹17,000. Put that straight into your EMI. We break down the numbers in our guide on earning ₹10K-₹1L monthly.

What the Market Actually Looks Like

GroMo partners have earned over ₹100 crores collectively. These aren't finance bros they're students, homemakers, and shop owners who figured out how to share links.

Payouts in 2026 are solid:

Personal Loans: Tez Credit and My Money Bazaar pay 3.5%. KreditBee pays 3.1%.

Credit Cards: IDFC WOW pays ₹2,000. YES Prosperity pays ₹1,800.

Help someone get a ₹2 lakh Tez Credit loan? You earn ₹7,000. That’s not side-hustle pocket money; that’s a significant chunk of debt cleared.

A 12-Month Recovery Blueprint

Months 1-3: Stabilize.

Take a small loan if you must. Automate the EMI. Start the GroMo training. Target ₹5,000-₹10,000 in side income.

Months 4-6: Build Momentum.

Your score should nudge up 10-30 points. Push for ₹15,000-₹25,000 monthly income. Build a tiny emergency fund so a bad week doesn't mean a missed payment.

Months 7-9: Accelerate.

You might see a 50-80 point jump. Maybe grab a secured credit card to show you can handle different types of credit. Scale up the referrals.

Months 10-12: Transform.

If you haven't missed a payment, you should be flirting with 650-700. You now qualify for better rates. Your side income is real.

The Mental Game

Bad credit feels shameful. It feels like a permanent mark. It isn't. Plenty of people have crawled out of the sub-500 hole. The stress evaporates once you see the numbers moving in the right direction.

For more on generating cash flow, check our piece on making money online in India.

Beyond the Score

Fixing your credit is step one. The end goal is stability:

Multiple income streams.

6-12 months of expenses saved.

Using credit for leverage, not survival.

It's possible. The tools are there. You just have to start.

Our guide on zero-investment business models has more ideas if you want to diversify.

FAQs

Q: Can I get a personal loan with a credit score of 600 in India?

A: Yes. Tez Credit, Smartcoin, and PaapaPay work with this range. They prioritize current income over history. Expect 18-24% interest and smaller loan amounts.

Q: How long to go from 600 to 750?

A: Plan on 6-9 months to hit 700, and another 6-12 to reach 750. You need perfect payments and low card utilization.

Q: Are small-ticket loan apps safe?

A: Only use RBI-registered NBFCs. Verify the license number on their site. If they ask for fees upfront or access to your contacts, walk away.

Q: Does GroMo income count for loan applications?

A: Yes. Consistent monthly deposits in your bank statement prove income stability, which lenders like to see.

Q: Fastest way to gain 100 points?

A: Pay down credit cards to under 30% utilization immediately. Automate all payments. Don't apply for new credit. Dispute any report errors.

Q: Should I take a loan to build credit or just wait?

A: If you need the funds, take a small loan and pay it perfectly. Active positive payment history builds a score faster than doing nothing.