Identify RBI-Registered Loan Apps in India 2026 | GroMo

Digital lending in India has exploded. So has the fraud. Thousands of unregistered apps sit in the Play Store, waiting to trap borrowers with absurd interest rates and harassment tactics. Whether you need to borrow safely or want to earn by distributing legitimate financial products, knowing which apps are actually RBI-registered is the only thing that matters in 2026.

Here is how to tell the real ones from the scams, and how platforms like GroMo let you earn by connecting people to safe credit.

What "RBI-Registered" Actually Means

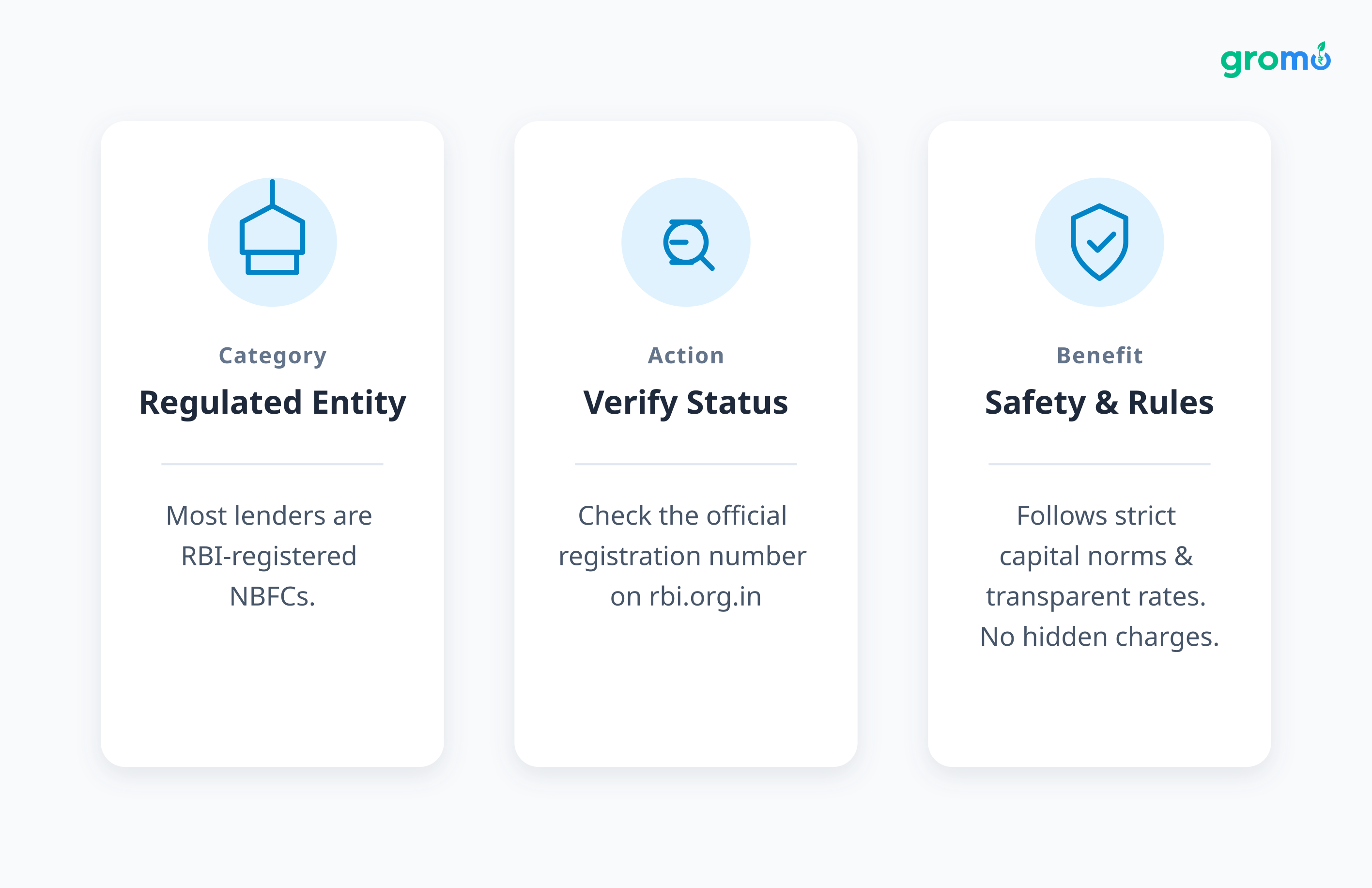

The Reserve Bank of India (RBI) regulates every legitimate lender in the country. An RBI-registered app operates under rules that exist to keep you from getting scammed.

In practice, this is what separates a real lender from a fake one:

Most digital lenders are Non-Banking Financial Companies (NBFCs). You can verify their registration number on the RBI website (www.rbi.org.in).

They follow the rules. This means minimum capital requirements, strict lending guidelines, and regular audits.

Rates are transparent. There is no interest rate cap for NBFCs, but the RBI forces them to disclose every charge upfront. Hidden penalties are a violation.

Your data stays safe. Illegal apps steal your contacts and photos. RBI guidelines ban this lenders only access what is necessary for verification.

Collection agents have rules. Registered lenders follow the Fair Practices Code. No harassment, no threats, no calling your family.

The biggest difference? If an RBI-registered app violates the rules, you can complain to the RBI Ombudsman. With an illegal app, you have no protection at all.

Red Flags: How to Spot the Scams

Before we get to the good apps, here is how to filter out the bad ones:

Too good to be true. Apps promising "₹5 lakh loan, no documents" or "loans for CIBIL score below 300" are traps. Real lenders always check your ability to repay.

Creepy permissions. If a loan app demands access to your photos, contacts, SMS, and call logs, delete it. Genuine apps only need KYC info.

No address. Real NBFCs list their registered office, GSTIN, and customer care details prominently. Fraudulent apps hide behind generic email IDs.

Upfront fees. No legitimate lender asks for "registration fees" or "insurance deposits" before approval. That is a scam.

Harassment. If agents call your contacts or threaten you days after a missed payment, you are dealing with an illegal operator.

No agreement. Legit lenders give you a detailed agreement with APR, EMI schedule, and prepayment terms. Shady apps skip this entirely.

The RBI has cracked down hard as of April 2026, blocking thousands of these apps. Google and Apple have tightened vetting, but new scams still appear.

Start Earning by Distributing Safe Loans →

Legit Loan Apps in 2026

These platforms are either RBI-registered NBFCs or partner with registered banks.

Personal Loan Apps

Moneyview Personal Loan

Moneyview is a solid NBFC. They offer loans from ₹5,000 to ₹5 lakhs. What makes them different is that they look at your bank statement, not just your credit score. This helps if you have a thin credit file.

Tenure goes up to 60 months. Interest starts at 1.33% monthly, with processing fees from 2%. You will need your mobile number, PAN, Aadhaar, and bank statement. Disbursal usually happens within 24 hours.

You do need a bank-transfer salary (NEFT/RTGS/UPI). Cash salaries don't work.

Ring Personal Loan

Ring is for salaried people aged 21-59 earning over ₹15,000 a month. They want a CIBIL score of at least 650.

The process is entirely digital. You link your bank account, set up NACH for repayment, and withdraw instantly. Loans range from ₹5,000 to ₹5 lakhs.

You have to apply from your own phone. Applications from a third-party device get rejected immediately.

Kissht Personal Loan

Kissht works similarly to Ring but with different interest structures. It is popular with younger borrowers because the app is easy to use and approvals are quick.

They look at alternative data points beyond CIBIL, which helps if you lack a credit history.

IDFC First Bank Personal Loan

If you need more money up to ₹10 lakhs IDFC First Bank is a proper bank with proper rates, starting at 9.99% annually.

The best part? Zero foreclosure charges. You can prepay whenever you want. But they are picky. They generally want new customers with CIBIL scores above 700, no recent defaults, and credit utilization under 70%.

Expect a thorough check: address verification, e-mandate, video KYC. Once cleared, disbursal is within 24 hours.

InCred Personal Loan

InCred only serves salaried individuals. Loans go from ₹50,000 to ₹15 lakhs over 60 months. If you have zero credit history, you are out.

They verify everything: three months of bank statements, home photos, work email, references. Documents must be e-signed via Aadhaar OTP.

Business Loan Apps

ClickPe Business Loan (Powered by Muthoot Finance)

ClickPe is backed by Muthoot Finance, a massive legacy player. They offer unsecured business loans up to ₹3 lakhs for MSMEs.

They prefer Udyam-registered businesses but will look at others. The process involves PAN/Aadhaar, business info, optional bank statements for higher limits, residence proof, a selfie, shop photos, video KYC, and a call.

Money arrives the same day. No collateral needed.

If a customer defaults in the first three EMIs, the partner payout gets reversed. This keeps the quality of referrals high.

Lines of Credit

Smartcoin Personal Loan

Smartcoin offers small loans and credit lines. It works for self-employed people who do not have salary slips. The app supports multiple Indian languages.

Loans go up to ₹1 lakh with shorter tenures. Use code DADA50 for 50% off processing fees (up to ₹250).

You set a PIN, choose amount, submit bank details, do KYC (selfie, PAN, Aadhaar), provide family/business info, set up autopay, and sign.

Instant Approval Apps

Lendingplate Personal Loan

Lendingplate uses bank statements for instant approval. They are flexible if your address does not match Aadhaar you can use a gas bill, rent agreement, or electricity bill instead.

The workflow is long but fast: mobile verification, pincode, personal details, selfie, work email, bank statement, workplace ID, DigiLocker KYC, address proof, MPIN, loan offer, references, autopay, signing.

Do not upload fake bank statements. You will get blacklisted.

BharatPe Personal Loan

BharatPe is known for merchant payments, but they do personal loans too. Active merchants often get better rates.

You verify via OTP, enter details, get a recommendation, redirect to their loan portal, complete KYC, download the app to sign the agreement and set up ENACH, and get the money.

Verify It Yourself

Do not trust the app store description.

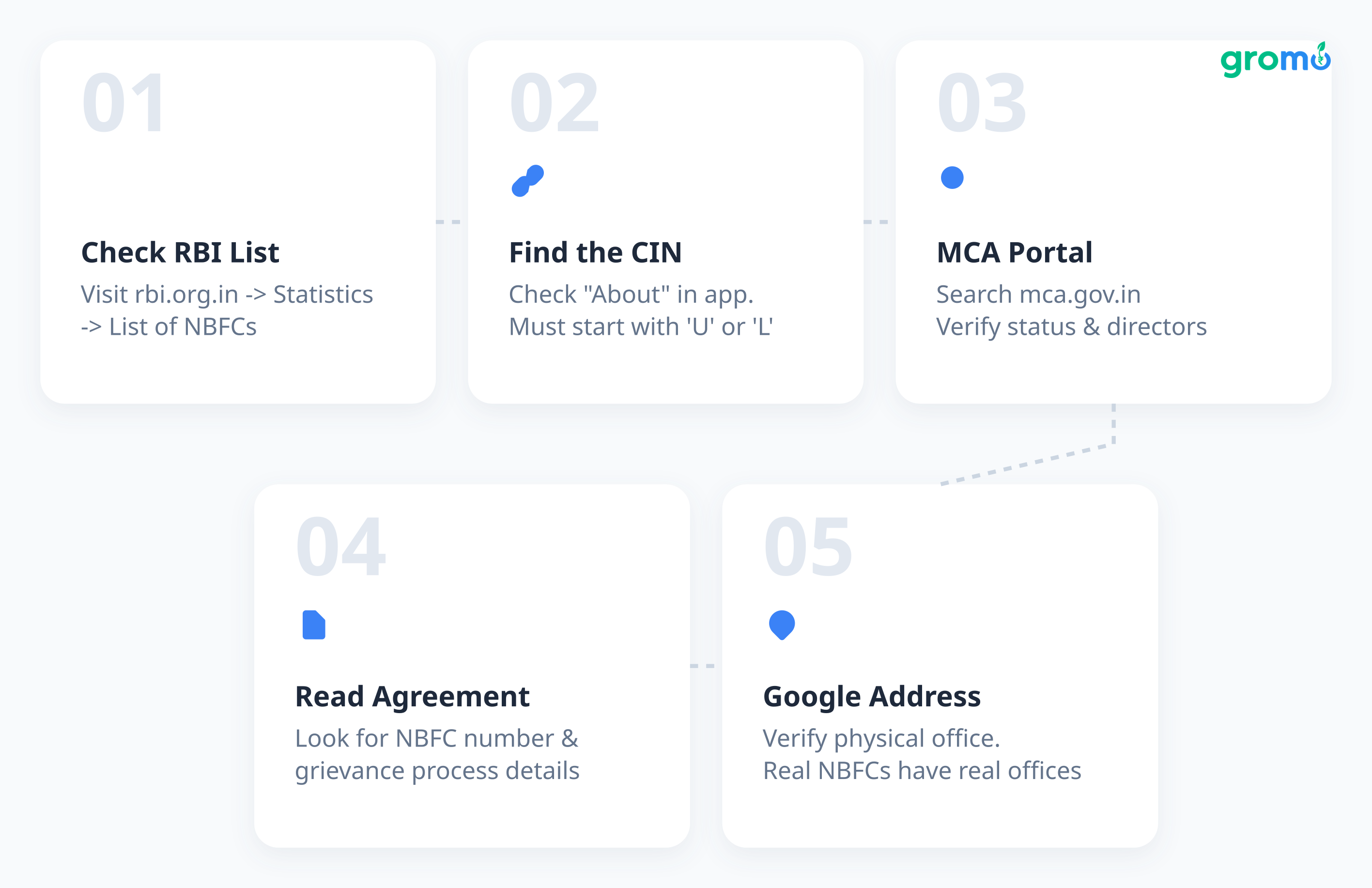

Check the RBI NBFC List. Go to www.rbi.org.in, look under "Statistics" for "List of NBFCs." It is updated monthly.

Find the CIN. Every registered company has a Corporate Identity Number (CIN) starting with 'U' or 'L'. It should be in the app's "About" section.

Search the MCA portal. Use the Ministry of Corporate Affairs site (www.mca.gov.in) to check registration status and directors.

Read the agreement. Legit lenders print their NBFC number and grievance process right in the agreement.

Google the address. Real NBFCs have real offices. If it is a virtual office or does not show up, be wary.

Email RBI. For serious doubts, contact [email protected].

Join 60L+ Partners Earning with GroMo →

Interest Rates and Charges

RBI-registered apps must show you the Annual Percentage Rate (APR) interest plus fees.

Interest Rates. Digital lenders usually charge 1.2% to 3% monthly (14.4% to 36% annually). Banks like IDFC First are cheaper, around 9.99% annually.

Processing Fees. Usually 2% to 5%. Anything over 6% is suspicious.

GST. 18% GST applies to processing fees and interest.

Prepayment. Many digital lenders let you prepay for free. Banks might charge 2-3%.

Bounce Charges. If your EMI bounces, expect a ₹500-800 penalty. This also hits your CIBIL score.

Late Fees. Usually ₹500 per missed EMI, plus interest on the overdue amount.

Illegal apps show a low rate upfront but use compounding penalties that explode a ₹10,000 debt into ₹50,000 within months.

Build Your Credit Score

Your CIBIL score changes everything.

Pay on time. Payment history is 30% of your score. A single 30-day delay can drop you 50-100 points.

Keep utilization low. If your credit limit is ₹1 lakh, stay under ₹30,000.

Mix credit types. Secured (home/car) and unsecured (personal/card) credit looks responsible.

Do not spam applications. Every application is a "hard inquiry." Too many at once looks desperate.

Check your report. You get one free report a year from each bureau. Use it.

Keep old cards. Long credit history helps.

For more, read our guide on how to improve your credit score.

The GroMo Opportunity

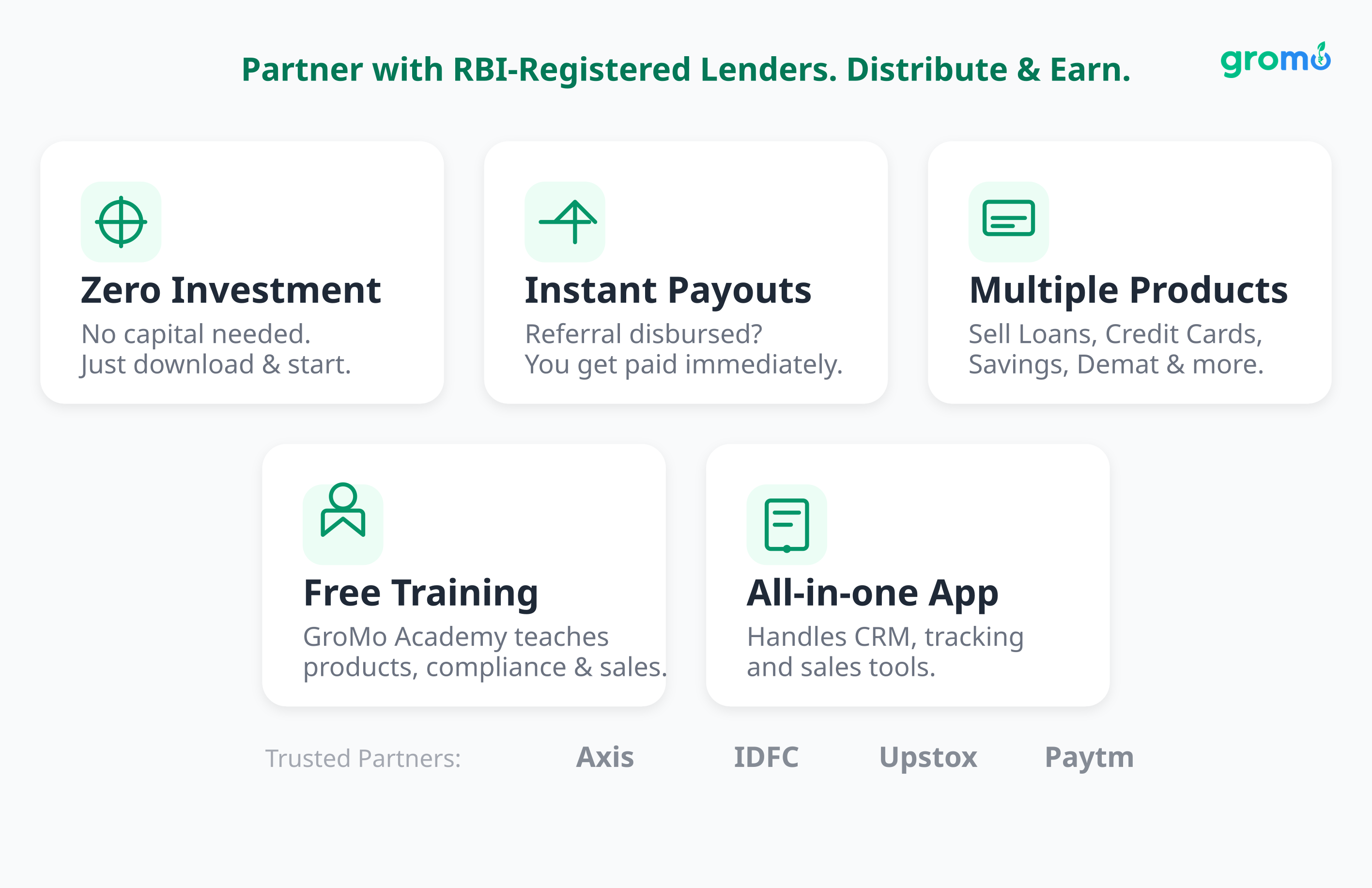

You might be here to borrow. But you can also earn by distributing these products.

GroMo partners with RBI-registered lenders. You earn commissions on personal loans, business loans, credit cards, and savings accounts.

How It Works

Zero investment. Download the app, train, and start. No capital needed.

Instant payouts. Referral disbursed? You get paid immediately.

Multiple products. Sell credit cards, savings accounts, Demat accounts, and investments from Axis, IDFC, Upstox, Paytm Money.

Free training. GroMo Academy teaches you products, compliance, and sales.

All-in-one app. It handles CRM, marketing content, security, and tracking.

What You Can Earn

Product | Payout | Ticket Size | Earnings |

|---|---|---|---|

Moneyview Personal Loan | 1.75% | ₹50,000-₹5L | ₹875-₹8,750 |

Ring Personal Loan | 2.25% | ₹5,000-₹5L | ₹113-₹11,250 |

IDFC First Bank PL | 1.20% | Up to ₹10L | Up to ₹12,000 |

ClickPe Business Loan | 1.5% | Up to ₹3L | Up to ₹4,500 |

InCred Personal Loan | Variable | ₹50K-₹15L | Up to ₹15,000+ |

Help 10 people get ₹2 lakh loans at 1.75%. That is ₹35,000. Add credit card referrals (₹500-₹1,000 each), and you are looking at ₹50,000-₹1 lakh monthly.

Over 60 lakh partners have earned ₹100 crores collectively on GroMo.

Who Should Do This?

Professionals. Flexible extra income.

Homemakers. Help your network borrow safely and earn.

Students. Learn sales and finance early.

Business owners. Cross-sell to your customers.

Advisors. Expand your product range.

Compliance

GroMo is strict:

No false promises.

Customers must apply themselves with full consent.

Data is encrypted.

Most payouts stick, though some products claw back if the customer defaults immediately.

Read more on earning ₹1 lakh monthly with referral strategies.

Safer Alternatives

If you are stuck with an illegal loan app, try these:

Bank Overdraft. Salary accounts often have this feature.

Credit Cards. 45-50 days interest-free if you pay the full bill.

Gold Loans. 7-12% annually from Muthoot or banks.

P2P Lending. RBI-regulated platforms like Faircent.

Salary Advances. Many employers offer this.

Family. Ask your personal network first.

See our guide on making money online in India in 2026.

If You Have Been Scammed

Stop paying. Do not send more money.

Document everything. Screenshots, calls, messages.

Police. File a report at the cybercrime cell.

RBI. Email [email protected].

Delete the app. Revoke permissions.

Bank. Block unauthorized mandates.

Legal help. Call National Consumer Helpline (1800-11-4000).

Courts usually rule that debts from illegal apps are not enforceable.

The Future of Digital Lending

As 2026 moves on, expect stricter rules. The RBI wants better disclosures and harsher penalties. Account Aggregators are making data sharing safer. Lenders are looking at UPI history, not just CIBIL scores. You will see loans embedded in shopping and healthcare apps, powered by regulated partners.

Regulated credit is becoming safer and more accessible. The scams are not going away overnight, but the net is tightening.

Frequently Asked Questions

Q: How can I verify if a loan app is RBI-registered?

A: Check the NBFC list on www.rbi.org.in under "Statistics." Verify the Corporate Identity Number (CIN) on the MCA website. Legit apps list their NBFC number and grievance process in the agreement.

Q: What is the difference between a loan app and an NBFC?

A: The NBFC is the lender. The app is just a tool. The app might belong to the NBFC or partner with one. Check who is actually lending the money.

Q: Can I earn money by helping people get loans through GroMo?

A: Yes. You earn commissions distributing loans and cards from registered lenders. Payouts are 1.2% to 3.5%. No investment needed.

Q: What should I do if an illegal loan app is harassing me?

A: File a police report immediately. Report to RBI at [email protected]. Save all evidence. Stop payments. The debt is not legally enforceable.

Q: What is the minimum CIBIL score required?

A: It varies. Moneyview and Smartcoin might accept 650-700. IDFC First wants 700+. Lenders also check income and job stability. Some use alternative data if you lack a history.

Q: Are processing fees refundable if my application is rejected?

A: No. Legitimate lenders deduct fees after approval or at disbursal. If they ask for money before approval, it is a scam.