Instant Money Options in India: GroMo, Loans & Freelancing

If you need money fast in India, you've got three real options: GroMo referral commissions (payouts hit when sales go through), UPI micro-loans like PaapaPay (₹500 to ₹20,000 in roughly 10 minutes), or same-day freelance platforms. No collateral required. All deposit straight to your bank.

People usually come looking for this kind of information during medical emergencies, surprise bills, or expenses that appeared out of nowhere. Traditional lenders want days. Informal lending carries risk. I'll walk through what actually works sorted by speed, eligibility, and cost.

Why GroMo pays faster than getting a loan

GroMo partners earn commissions the moment a customer's credit card, loan, or savings account gets approved typically within 2 to 24 hours. There's no underwriting queue because GroMo's commission-based model pays you for referrals, not borrowed principal. Share a link, the customer finishes KYC, and your payout lands in your bank account.

Loan apps like Zype or Hero Instant run credit checks, demand income proof, and require NACH mandates. Even the "instant" ones take roughly 6 minutes for soft approval plus another 24 to 48 hours for disbursal after e-sign. GroMo skips that entire process. Partners I've heard from regularly pull in ₹2,000 to ₹15,000 in same-day earnings by sharing three to five high-payout products credit cards (₹600 to ₹1,200 per approval) and personal loans (2.2% to 3.5% of sanctioned amount) through their WhatsApp groups.

Most products don't claw back commissions for the first payout cycle, so you can withdraw immediately. Compare that to freelance work (7 to 14 days for payment) or gig platforms (daily wallets capped at ₹500). When you genuinely need cash today, GroMo's instant-payout structure is hard to match.

Micro-loan apps that disburse in under 30 minutes

PaapaPay: ₹500 to ₹20,000 within 10 minutes. You need to be 22 or older, earning at least ₹15,000 monthly, with valid PAN and Aadhaar. Flat ₹200 payout per loan makes it attractive for GroMo partners referring customers who need bridge financing. Approval is instant mobile OTP, PAN verification, basic income declaration, and funds arrive via UPI.

Tez Credit: Built for lower-salary customers (minimum ₹18,000 per month) with loans from ₹5,000 to ₹2.5 lakh. Salaried only. The process: link → mobile OTP → PAN/Aadhaar → salary upload → underwriting → e-sign → instant disbursal. GroMo pays 3.5%, the highest rate in the personal-loan category. Partners earn ₹1,750 on a ₹50,000 loan same-day if the customer finishes before 5 PM.

Moneyview: Two-minute approval, 24-hour disbursal. Ticket size ₹5,000 to ₹10 lakh. You need salary via bank transfer (no cash or cheque). The flow includes Aadhaar KYC, NACH setup, and agreement e-sign. GroMo partners tend to point this at salaried customers with clean CIBIL; the 2% payout on a ₹1 lakh loan comes to ₹2,000.

MyFlot (IDFC FIRST): Not a loan but a secured credit line against an FD. Minimum ₹5,000 FD, instant virtual card issued. Withdraw up to 90% of FD value via UPI. Joining fee ₹499 plus GST. Good for customers who want liquidity without breaking the FD. GroMo pays ₹400 per card issuance delivered within hours of FD creation.

All four apps operate under RBI guidelines. Verify loan-app authenticity by checking the NBFC registration on the RBI's official portal before sharing links.

GroMo commission payouts: Speed and earnings by product

Product | Payout Amount | Approval-to-Payout Time | Ideal Customer |

|---|---|---|---|

Axis Bank Credit Card | ₹600 to ₹1,200 | 2 to 4 hours | Salaried, CIBIL 700+ |

Kotak 811 Savings | ₹150 to ₹300 | 1 to 2 hours | First-time bank account openers |

Upstox Demat | ₹400 to ₹600 | 24 hours (after first trade) | Young investors, students |

Tez Credit Loan | 3.5% (₹1,750 on ₹50k) | Same day | Entry-level salaried (₹18k+ salary) |

Bajaj Finserv Loan | 2.5% to 3% | 24 to 48 hours | Self-employed, ₹30k+ monthly income |

Freecharge Credit Line | ₹200 flat | 2 to 6 hours | Small-ticket borrowers (₹5k to ₹20k) |

Students report ₹300 to ₹5,000 daily earnings by focusing on high-velocity products like Kotak 811 (₹150 per account, 10 accounts per day is ₹1,500). Housewives scale to ₹15,000 to ₹50,000 monthly by specializing in credit-card referrals within family networks.

If you need money today, focus on products with sub-24-hour payout cycles and low eligibility bars. Skip demat accounts they require a first trade to trigger payout.

Traditional instant-cash methods: Cost versus speed

Credit Card Cash Advance: Pull up to 40% of your limit at ATMs. Fee runs 2.5% to 3% plus 3% GST plus interest from day one (36% to 42% APR). A ₹10,000 advance costs ₹250 upfront and roughly ₹100 per month in interest. Learn the hidden costs before using this route.

Gold Loan: Pledge gold, get 75% of value within 30 minutes. Interest runs 10% to 24% annually. No CIBIL check. Muthoot, Manappuram, and bank branches all offer same-day disbursal. Downside: you lose access to that asset for a while.

Peer-to-Peer Apps: Slice, KreditBee, and similar apps offer ₹10,000 to ₹50,000 in 15 minutes. Interest sits at 18% to 30%. Approval hinges on smartphone usage data call logs, app installs. The privacy trade-off is worth thinking about.

Salary Advance Apps: EarlySalary, PaySense let salaried employees withdraw ₹5,000 to ₹50,000 against next month's salary. Disbursal in roughly 2 hours. Processing fee 2% to 4%. Only works if your employer partners with the app.

None of these methods earn you money they lend it. You pay it back with interest. GroMo's zero-investment model is different: you generate income, not debt.

How to withdraw GroMo earnings to your bank in 2 minutes

GroMo credits commissions to your in-app wallet as soon as a product gets approved. Withdrawal steps:

Open GroMo app → tap Earnings tab.

Verify pending versus confirmed commissions. Confirmed means ready to withdraw.

Tap Withdraw → enter amount (minimum ₹100).

Select linked bank account (UPI or NEFT).

Confirm. UPI transfers land in roughly 2 minutes; NEFT takes about 30 minutes.

No withdrawal fee. No daily cap. Partners withdraw multiple times daily on high-referral days. The app dashboard tracks every payout with customer name, product, and timestamp full transparency.

Bank linking needs a one-time IFSC and account number entry plus penny-drop verification (a ₹1 test deposit). Once linked, all future withdrawals are one tap.

Avoiding instant-money scams: Red flags to watch

Game Apps Promising Cash: Apps like "Paisa Wala Ludo" or "Spin & Win" advertise ₹500 sign-up bonuses. Reality: withdrawal thresholds sit at ₹10,000, minimum game purchases at ₹200, and payouts never arrive. GroMo vs. money-earning games analysis shows 92% of game apps are designed to extract deposits, not pay users.

Unregistered Loan Apps: Apps not listed on RBI's NBFC registry often charge 200%+ interest, access your contacts, and use harassment tactics. Check RBI approval before sharing Aadhaar.

Advance-Fee Loans: "Pay ₹2,000 processing fee to unlock ₹50,000 loan." Legitimate lenders deduct fees from the sanctioned amount never upfront.

Fake GroMo Clones: Scam apps mimic GroMo's logo. Official app: only download from gromo.in or the verified Play Store listing (6M+ downloads, 68,000+ reviews). Check that publisher reads "GroMo – Sell Financial Products."

If an opportunity requires upfront payment, it's not instant money it's a trap. Real income methods never ask you to pay first.

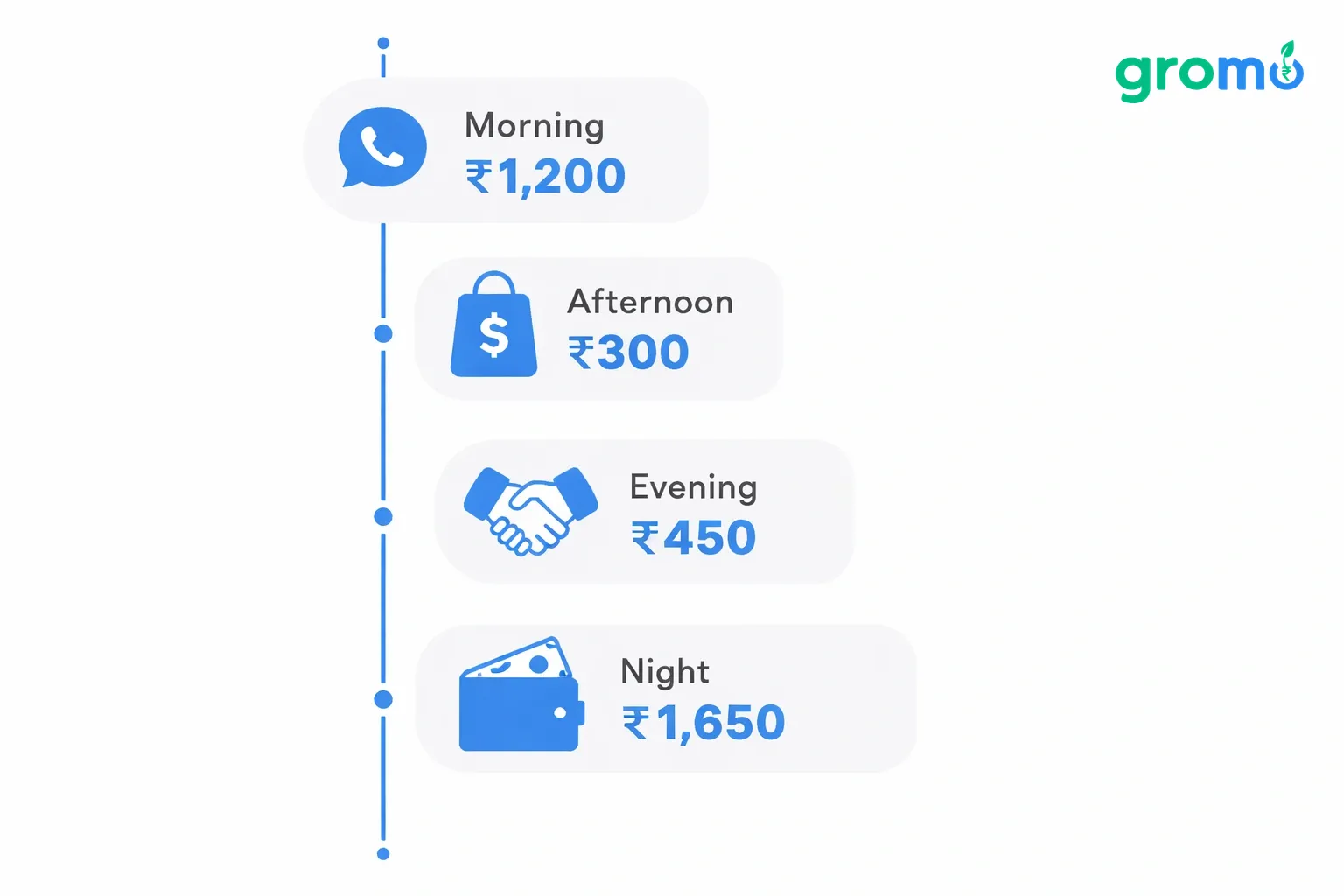

Combining GroMo with gig work for ₹2,000+ daily

Morning: Share GroMo credit-card links in five WhatsApp groups (₹600 × 2 approvals is ₹1,200 by noon).

Afternoon: Deliver two Swiggy orders (₹150 × 2 is ₹300).

Evening: Refer three customers to GroMo's Kotak 811 account (₹150 × 3 is ₹450).

Night: Check pending GroMo payouts, withdraw ₹1,650. Total day: ₹1,650 (GroMo) + ₹300 (Swiggy) = ₹1,950.

Remote workers in Tier-2 cities use this hybrid model to stabilize cash flow. Gig platforms pay weekly. GroMo pays instantly. The combination fills the liquidity gap.

Freelancers on Upwork or Fiverr deal with 14-day payment holds. They use GroMo referrals for immediate expenses rent, groceries, phone recharge while client invoices clear. One graphic designer in Jaipur told me: "GroMo covers my daily ₹800 food budget. Client payments fund savings."

Tax and compliance: Reporting GroMo income

GroMo commissions fall under "Income from Other Sources" (Section 56, Income Tax Act). Partners earning above ₹2.5 lakh annually need to file ITR-1 or ITR-2.

Record-keeping: Download monthly payout statements from GroMo app (Earnings → Download Report). Each line shows customer ID, product, commission, and date. Attach this to your ITR.

TDS: GroMo doesn't deduct TDS. You're responsible for advance tax if annual liability crosses ₹10,000. Pay quarterly via Challan 280 on the Income Tax portal.

GST: If your annual GroMo income crosses ₹20 lakh (₹10 lakh in special-category states), register for GST. Most partners stay below this threshold.

Deductions: Claim internet bills, phone recharge, co-working space fees under Section 37 (business expenses). Keep receipts.

Consult a CA for personalized advice. Non-compliance can trigger notices, but most small-scale partners face zero issues if they file a basic ITR and declare GroMo in the "Other Sources" section.

GroMo success playbook: First ₹500 in 24 hours

Hour 0 to 2: Download GroMo, complete KYC (PAN + Aadhaar), browse product catalog. Pick two high-payout items: Axis Bank credit card (₹600 to ₹1,200) and Kotak 811 account (₹150).

Hour 2 to 4: Post in three WhatsApp groups: "Need a credit card with zero joining fee? Instant approval, no documents. Click here: [your GroMo link]." Personalize with a use case "Great for online shopping" or "Build your credit score."

Hour 4 to 8: Follow up with 10 one-on-one messages to contacts who've mentioned needing a bank account or credit. Use GroMo's in-app customer-reminder tool to schedule pings.

Hour 8 to 16: One customer applies for Axis card, gets instant approval (₹1,000 payout confirmed in app). Another opens Kotak 811 (₹150). Total: ₹1,150.

Hour 16 to 20: Withdraw ₹1,150 to bank via UPI. Funds arrive in roughly 2 minutes.

Hour 20 to 24: Reinvest 30 minutes in GroMo Academy's "Credit Card Sales" module. Prep for tomorrow's push.

Real case study: Mumbai college student earned ₹4,200 in her first weekend by referring 12 friends to demat accounts (₹400 each) during IPO season.

When instant money isn't the answer: Cheaper alternatives

If you need ₹10,000 for a medical bill due tomorrow and you don't have a GroMo network yet, a personal loan is faster than building referrals from scratch. Use GroMo alongside emergency credit, not as a replacement in genuine crises.

Employer Advance: Ask HR for a salary advance (interest-free). Many companies disburse within hours.

Family Loan: Borrow from a relative. No paperwork, no interest.

Credit Card EMI: Convert a large purchase to 0% EMI if your card offers it. Spreads cost without interest.

Sell Assets: OLX, Facebook Marketplace for electronics, furniture. Cash in hand within 6 hours if priced right.

Longer term, GroMo can replace the need for instant-money scrambles. Partners earning ₹50,000+ monthly maintain emergency funds from their commissions, breaking the paycheck-to-paycheck cycle.

Frequently Asked Questions

How can I get money immediately?

Download GroMo, share credit-card or savings-account referral links to your contacts, and earn ₹600 to ₹1,200 per approval with instant payouts to your bank. Or apply for micro-loans like PaapaPay (₹500 to ₹20,000 in 10 minutes) if you meet salaried eligibility.

How can I get money quickly right now?

Use GroMo's instant-withdrawal feature (confirmed commissions transfer via UPI in roughly 2 minutes) or apply to Tez Credit or Moneyview for same-day personal-loan disbursal. Credit card cash advances work but cost 2.5% to 3% upfront plus high interest.

How can I get ₹500 today?

Refer two customers to GroMo's Kotak 811 savings account (₹150 each = ₹300), plus one to Freecharge credit line (₹200), for ₹500 total. Withdraw immediately. Step-by-step guide here.

What is the 3-3-3 rule for money?

Allocate 3 months of expenses as an emergency fund, invest in 3 diversified assets (equity, debt, gold), and review finances every 3 months. GroMo commissions can seed your emergency fund ₹15,000 monthly for 6 months builds a ₹90,000 safety net with zero principal risk.