Earn ₹1000+ Daily with GroMo – Zero Investment Side Hustle

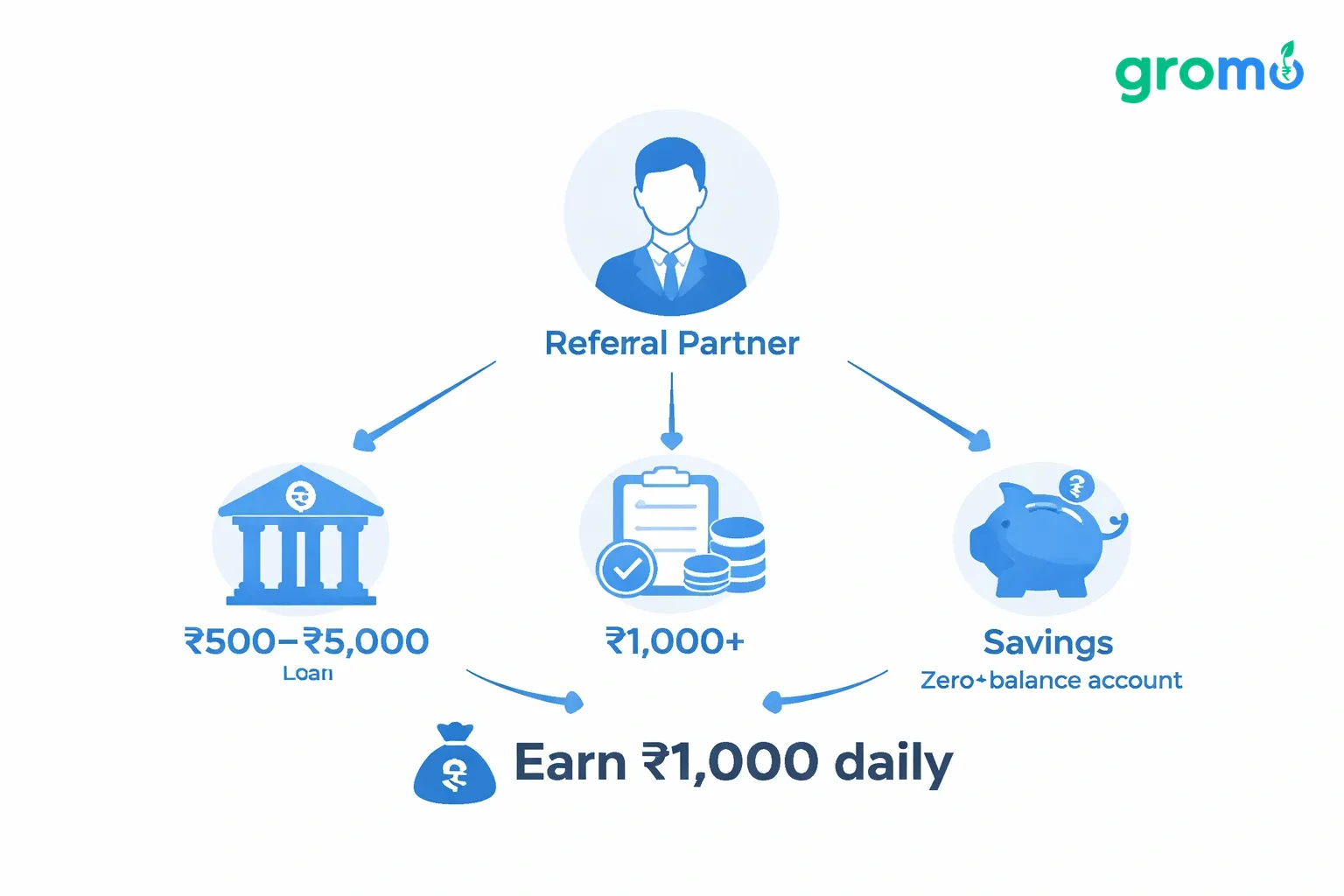

Making extra money in India used to mean taking on a second job or investing in inventory. That's changed. GroMo, a platform with over 60 lakh partners, lets people earn ₹1,000 to ₹5,000 daily by referring friends and contacts for credit cards, loans, and savings accounts. You don't need capital, just a phone and a network.

Most Indian households feel the squeeze education, healthcare, and housing costs keep climbing. A side hustle helps, but the usual options (reselling products, gig work) require upfront investment or specific skills. Financial product distribution is different. Banks pay commissions to acquire customers. GroMo handles the backend paperwork and compliance. You just share the links.

Explore how GroMo partners have collectively earned ₹100 crores through this model.

Why this works

You turn your existing contacts friends, family, social media connections into income. You aren't selling physical products or managing inventory. Banks pay ₹500 to ₹5,000 per approved credit card and ₹1,000+ for savings accounts. If you close two or three referrals a day, you hit ₹1,000.

GroMo partners with Axis Bank, Kotak 811, Upstox, Paytm Money, Bajaj Finserv, and 50+ institutions. A college student might need a zero-balance account; a business owner needs a loan. You match the person to the product.

It scales, too. Your first week might bring ₹3,000 from five referrals. By month two, once you've set up templates and follow-up routines, you might see daily earnings of ₹2,000 to ₹4,000. Top partners earn ₹1 lakh monthly by recruiting other sellers and taking a cut of their commissions.

Getting started

Download the app and get certified. Install GroMo from Google Play or the App Store. The free certification courses take 15 to 20 minutes each. They teach you the product details you need to answer customer questions.

Find your first prospects. Look at your contact list. Who recently changed jobs, got married, or started a business? These life events create financial needs. Warm leads convert much faster than cold messages.

Share links that actually work. GroMo gives you unique referral links. Don't just send "Here's a card." Send: "Hey [Name], Axis has a card with a ₹500 bonus and no joining fee. Takes 3 minutes. [link]." Personalization triples clicks.

Track your applications. The dashboard shows who clicked, started, and finished. If someone drops off, a nudge like "Need help with the Kotak KYC?" recovers about 30% of lost applications.

Get paid quickly. Commissions hit your bank within hours of approval. Credit cards pay at dispatch; loans pay at disbursal. It's one of the fastest payout cycles in the Indian market.

Which products pay the most?

Credit cards: ₹500 to ₹5,000. Premium cards (Axis Magnus, HDFC Infinia) pay ₹3,000 to ₹5,000 but need higher income proof. Mass-market cards (IDFC FIRST UPI, Jupiter RuPay) pay ₹500 to ₹1,500 and approve faster. Target 2–3 approvals a day.

One partner in Bangalore targets software engineers on LinkedIn with comparison posts like "Best cashback cards for online shoppers." He drives 15 to 20 applications a week and earns ₹80,000 monthly just from cards.

Personal loans: 2–3% of the amount. A ₹2 lakh loan at 2.5% commission pays ₹5,000. Loans take a day or two to disburse, so one approval every other day keeps income steady. Look for salaried customers with CIBIL scores over 700 who have immediate needs.

MyFlot and Hero Fincorp on GroMo approve ₹50,000 to ₹5 lakh for salaried staff. Avoid cash-salary customers; they face more rejections.

Savings and demat accounts: ₹500 to ₹1,000. IndusInd pays ₹650 per funded account. Jupiter and Kotak 811 pay ₹300 to ₹800. Demat accounts (Upstox, Aditya Birla Money) pay ₹800 to ₹1,200 after the first trade. These are low-friction products instant opening, minimal docs perfect for volume.

Learn advanced strategies for financial product distribution in India.

What partners actually make

Part-time (1–2 hours daily): ₹15,000 to ₹30,000 monthly. Professionals and students who spend evenings on GroMo typically close 10 to 15 referrals a month. A Mumbai marketing executive spends 90 minutes after work messaging contacts and posting Instagram Stories. She earns ₹22,000 monthly enough to cover rent.

Full-time (5–6 hours daily): ₹50,000 to ₹80,000 monthly. Partners who treat this as a job close 40 to 60 referrals. They use WhatsApp Business, content calendars, and CRMs. A Pune housewife with no sales background earns ₹65,000 monthly by focusing on her housing society and local groups.

Team builders: ₹1 lakh+ monthly. You can earn overrides by recruiting other partners. Refer 10 active partners earning ₹20,000 each, and you get 5–10% of their commissions. Top earners mix direct sales with team commissions.

See how students earn ₹300 to ₹5,000 daily.

Where people mess up

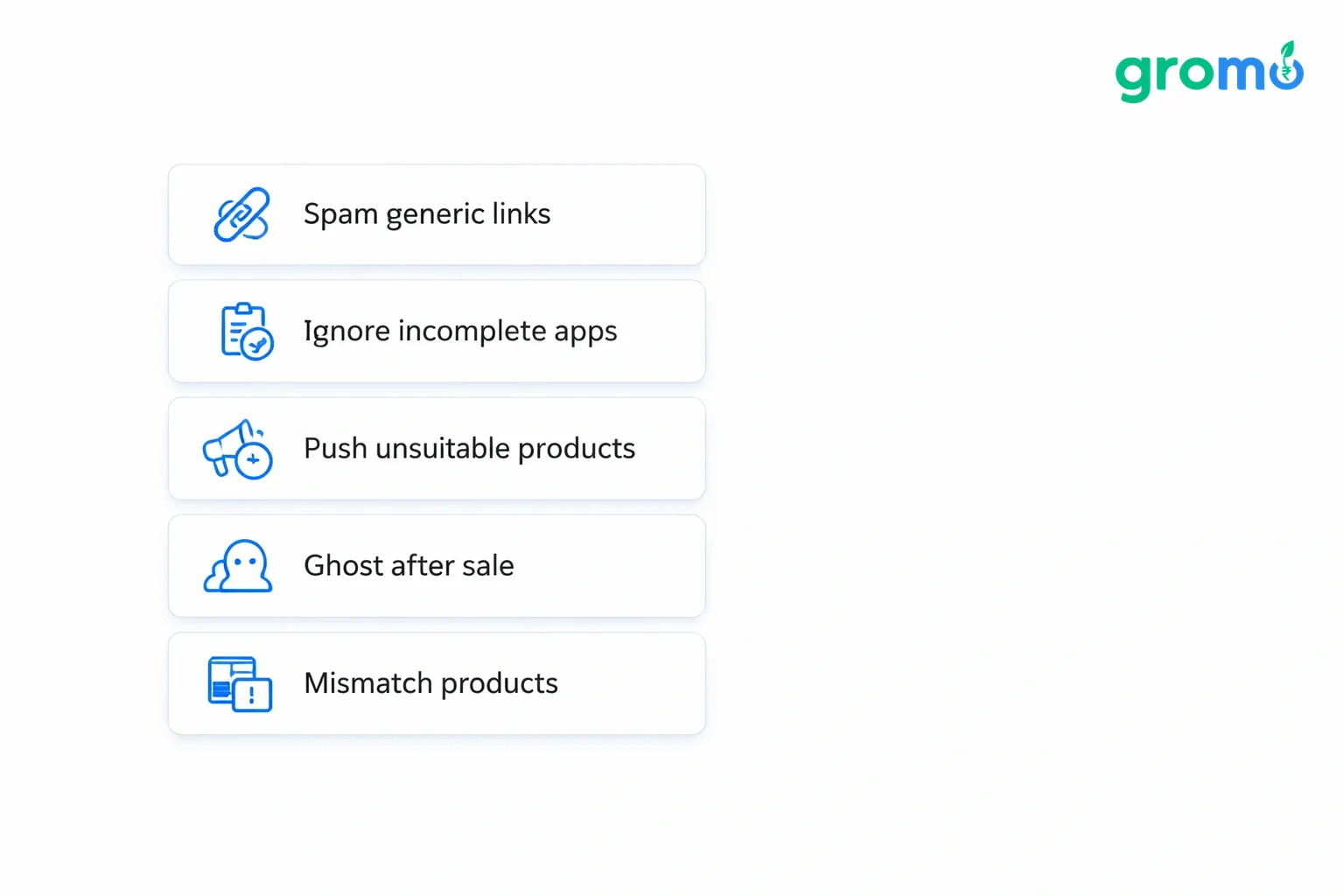

Spamming generic links. "Here's a credit card link" gets ignored. "Rohit, you mentioned travel this HDFC card gives lounge access and points on spends" gets clicks.

Ignoring incomplete applications. Half of applicants start but don't finish. A follow-up message recovers 30% of drop-offs.

Pushing products you don't get. If you can't explain the interest-free period, you lose trust. Do the certification courses.

Ghosting after the sale. Help customers activate cards. Satisfied customers refer others. One partner gets 40% of leads from repeat referrals because he supports post-approval.

Mismatching products. Don't pitch a ₹1 lakh loan to someone earning ₹18,000. It wastes time and hurts your credibility.

Avoid online game scams and earn real income.

Scaling to ₹5,000 daily

Build a content engine. Post 5 to 7 WhatsApp Status updates weekly on benefits and offers. Put carousels on Instagram "Top 3 Cards for Freelancers." Content brings leads to you.

Segment your network. New grads need demat accounts. Mid-career pros need premium cards. Targeted pitches convert better.

Run micro-campaigns. Partner with RWAs or alumni groups. Host a 30-minute Zoom "financial clinic." One webinar can generate 10 to 15 leads.

Follow the seasons. Credit card applications spike during festivals (Oct–Nov). Loans surge before wedding season. Time your outreach.

Master the follow-up. Day 1: Send link. Day 3: Share testimonial. Day 7: Highlight offer. Day 14: Offer a call. Sequences convert 40% more than single touches.

Taxes

Commission income from GroMo is taxable. If you earn over ₹50,000 annually, file ITR-3 or ITR-4. GroMo provides monthly payout statements for your CA. No TDS is deducted, so set aside 10–15% for advance tax if your income exceeds ₹2.5 lakh.

Most full-timers register as sole proprietors to deduct expenses like internet and phone bills.

Explore zero-investment business ideas.

Why this beats freelancing

No skill barrier. Freelancing needs design or coding skills. GroMo needs communication skills, which are trainable in days.

Faster payouts. Freelance platforms hold money for weeks. GroMo pays in hours.

Recurring income. A freelance project pays once. A referral who opens an account, takes a loan, then gets a card pays you three times.

Lower rejection. Freelance proposals face 95% rejection. GroMo links convert at 10–20% because you're solving a real need for people you know.

Compare GroMo with ad-watching apps.

Who this is for

Salaried professionals. Want an extra ₹15,000 to ₹30,000? Do this in the evenings.

Students. College networks are gold for demat accounts and entry-level cards.

Homemakers. No commute, flexible hours. One partner earns ₹65,000 monthly from her housing society.

Business owners. You already see customers daily. Add financial referrals as a value-add.

Retirees. Monetize your network of former colleagues and community contacts.

See how housewives earn ₹15,000 to ₹50,000 monthly.

What you need

Smartphone and internet. A basic ₹8,000 Android phone works.

Social presence. WhatsApp Business and Instagram help. Consistency 5 posts a week beats virality.

Willingness to learn. Your first 10 referrals teach you what works. Track click rates and approvals.

Financial literacy. Understand credit scores and interest rates (the GroMo course covers this).

Follow-up discipline. Spend 30 minutes every morning checking statuses. This habit lifts earnings significantly.

Compare GroMo with traditional remote jobs.

How GroMo keeps it fair

Instant payouts. Banks take 30–45 days? GroMo pays in hours.

Transparent commissions. You see the payout upfront: ₹1,000 for Kotak 811, ₹2,500 for Axis Flipkart. No hidden cuts.

Full tracking. You see who clicked, started, or got approved. No guessing.

Compliance handled. GroMo manages RBI and SEBI rules. You just sell.

Support. In-app chat and relationship managers for active partners.

Understand why GroMo beats money-earning games.

Legal basics

Register if needed. Earning ₹20 lakh+? Register as a sole proprietor to deduct expenses.

Keep records. Download monthly statements. Use accounting software.

Watch GST. Turnover over ₹20 lakh may need GST. Check with a CA.

Don't mis-sell. No false promises. GroMo monitors this; violations mean suspension.

Privacy. Don't spam. Respect "no."

Learn about legitimate refer-and-earn apps.

FAQs

Q: How to earn ₹1,000 per day?

A: Share 2–3 credit card or savings account links daily via GroMo. Commissions are ₹500–₹5,000 per product. No investment needed.

Q: Is ₹70,000 a good salary?

A: It's above median. Adding ₹20,000 via GroMo helps with savings or EMIs.

Q: Easiest way to earn?

A: Financial distribution via GroMo. No skills or inventory. Share links, earn ₹300–₹5,000 per referral.

Q: How to get ₹10,000 fast?

A: Close 5–7 credit card/savings referrals in 7–10 days. Focus on warm leads colleagues, family who have a need.