Earn ₹1000 Daily with GroMo: Zero Investment Commission Income

Earning apps without investment usually promise the world and deliver pennies. GroMo is a bit different. It lets you generate income by selling financial products on commission, and it’s a model that has actually paid out ₹100 crores to a network of 6 million partners in India. You don't need capital, just a smartphone and the willingness to talk to people about credit cards, loans, and investment accounts.

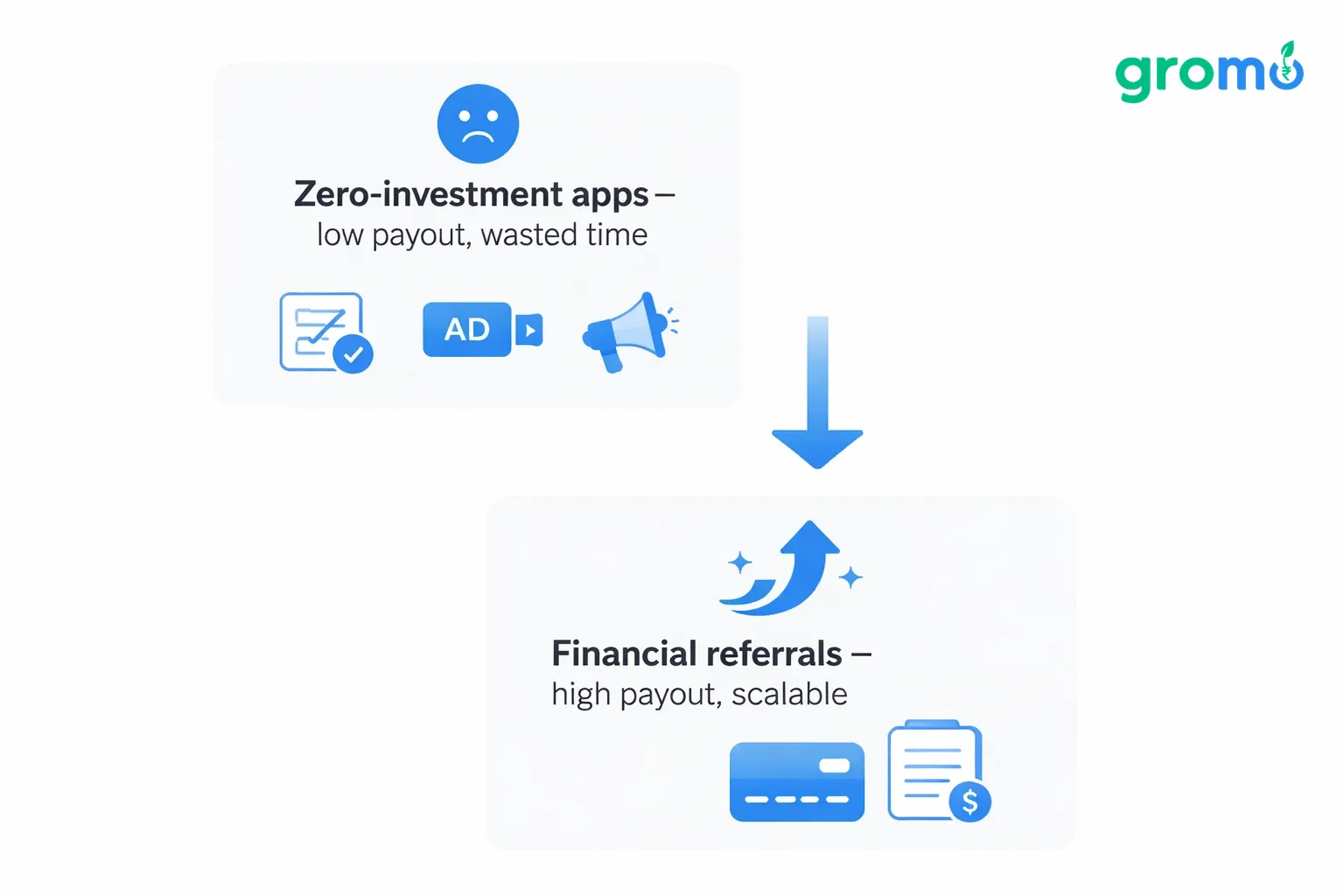

Most side hustles demand money upfront for inventory or specialized skills. These apps remove that barrier, but the trade-off is usually terrible pay. You end up watching 50 ads for ₹10 or answering surveys for hours to make less than minimum wage. GroMo skips the micro-task drudgery and pays market-rate commissions for actual transactions. You aren't watching ads; you're effectively a freelance agent for banks.

Why most zero-investment apps are a waste of time

Survey and task-based platforms are often brutal. You might spend an hour answering questions only to get disqualified, or watch ads for a payout that wouldn't buy a coffee.

Referral-only apps have a different problem: they collapse once you run out of friends to invite. Gambling apps disguised as games are arguably worse you deposit money to play, and the platform skims a percentage off the top. Most people lose money on those.

Financial product distribution avoids these issues. Banks have customer acquisition budgets, and they pay out whether you have capital or not. Your earning potential scales with your effort, not an arbitrary point cap. Because there's a constant cycle of new credit cards, loans, and accounts, the inventory doesn't run dry. The math is pretty stark: one credit card referral can pay out as much as 200 ad-watching sessions, as detailed in this comparison on GroMo vs Ad-Watching.

Start Earning Without Investment Today

How GroMo actually works

GroMo partners with over 40 financial institutions including HDFC, Axis, Kotak, and Bajaj Finserv. Banks typically spend ₹3,000–₹5,000 to acquire a single credit card customer through traditional channels. GroMo captures a portion of that acquisition cost and shares 60–70% with you.

The process is straightforward. You get a unique link for a product. When someone clicks, applies, and gets approved, the bank confirms it. GroMo credits your wallet within 24–72 hours. There are no monthly thresholds or 45-day holding periods.

Here is a breakdown of typical payouts:

Category | Example Payout | Typical Conversion Time |

|---|---|---|

Credit Cards | ₹300–₹2,500 | 5–7 days approval |

Savings Accounts | ₹150–₹500 | 2–3 days |

Demat Accounts | ₹250–₹500 | 7 days + first trade |

Personal Loans | ₹1,000–₹3,000 | 3–5 days disbursal |

Business Loans | ₹2,000–₹10,000 | 7–14 days |

Mutual Funds | ₹200–₹600 | First SIP activation |

Your customers don't pay extra. Banks factor these costs into their existing fee structures. You are simply claiming a finder's fee that would otherwise go to a direct sales agent. The GroMo app includes training modules on eligibility and documentation, and a success-rate predictor to help you avoid pitching to people who won't qualify.

Getting your first ₹1,000

It usually takes about a week to see your first real earnings.

Day 1: Download the app and register. You will need your mobile number and PAN for KYC verification via Aadhaar OTP. The Play Store listing shows a 4.3-star rating.

Day 2: Pick a product. Credit cards are often the best starting point because approval criteria are transparent. Look for cards that match your network salaried employees might prefer cashback cards, for instance.

Day 3: Do the training. The certification modules take about 15–20 minutes. They cover the essentials: never promise guaranteed approval, never ask for processing fees, and never share fake documents.

Days 4–6: Start reaching out. Share your link with 10–15 contacts who actually meet the criteria. The app has templates you can use, but a personal message works better. Follow up if they start an application but don't finish.

Day 7: Get paid. If you get two approvals a typical conversion rate for targeted outreach you're looking at ₹600–₹1,200. Once the bank confirms, the money hits your wallet. You can withdraw it via NEFT, usually within four hours.

Case studies on daily online earnings with GroMo show partners consistently earning ₹300–₹800 daily once they figure out how to match products to the right customers.

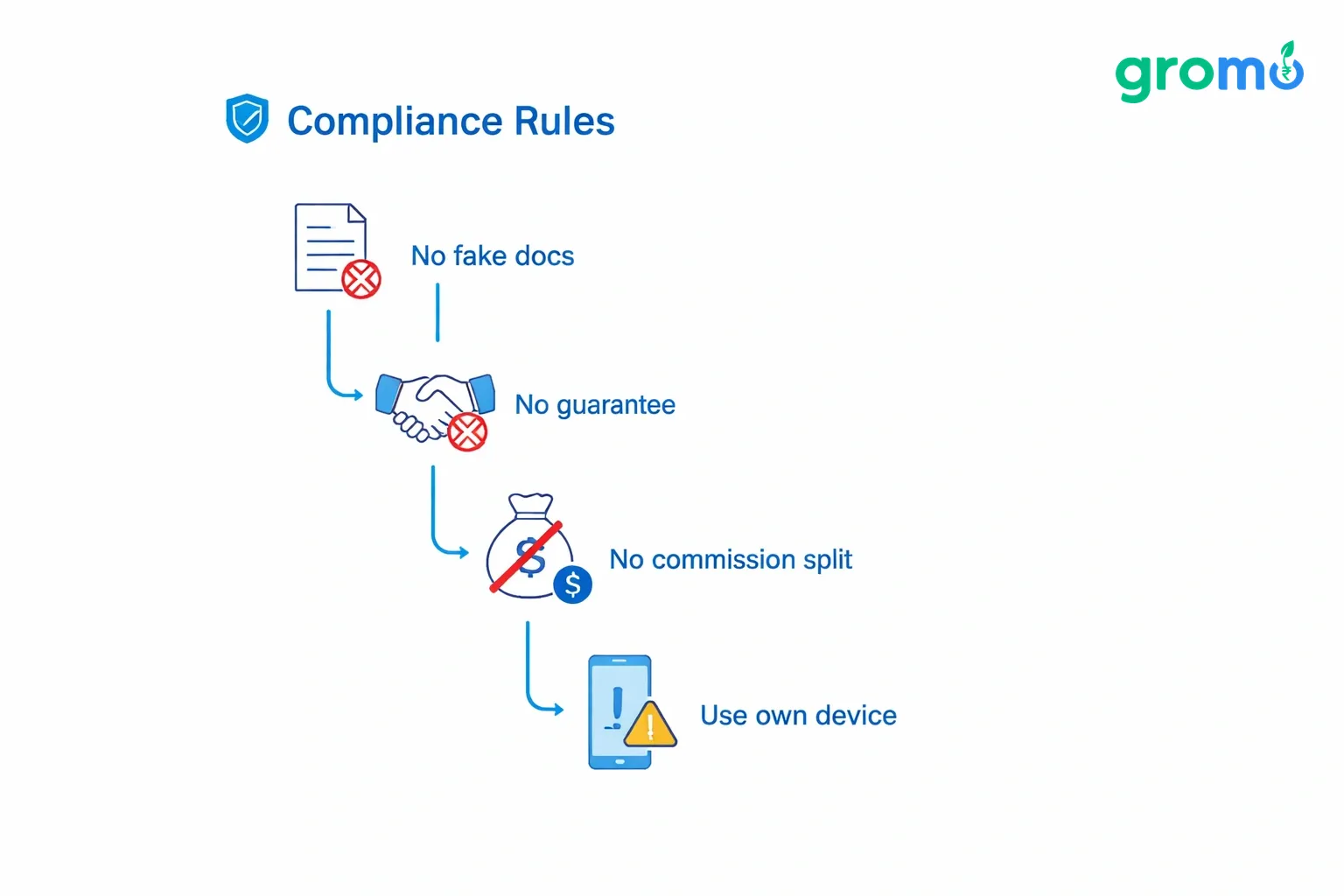

Compliance rules you can't ignore

This isn't like sharing a referral code for a shopping app. RBI and SEBI regulate financial product distribution. Violations can get your account suspended and payouts reversed.

Do not fake documents. Uploading fake salary slips is fraud. Banks verify this stuff, and getting caught can blacklist you across partner banks.

Do not promise approval. You are a facilitator, not a guarantor. Underwriting is complex, and even eligible candidates get rejected.

Do not split your commission. Offering a customer ₹200 back from your earnings violates RBI inducement guidelines. It attracts the wrong kind of customer and hurts your credibility.

Do not apply for others from your phone. Multiple applications from the same device raise red flags for fraud. Customers need to use their own devices.

If you mis-sell a card to someone who can't afford it, defaults and complaints will reflect on your record. Three complaints can lead to a permanent ban. For more on the regulatory side, see this list of RBI-Approved Loan Apps in India 2026.

Join 6 Million GroMo Partners Now

Turning this into a real income

Active partners typically earn ₹3,000–₹8,000 in their first month. To scale that up to ₹50,000, you have to stop treating it like a casual referral program.

Volume: You need to convert 40–60 leads a month, not just 10. This means looking beyond your immediate circle. Join local community groups on WhatsApp. Offer to help people find the right card for their spending habits. Don't just drop links; offer value.

Product mix: Credit cards are easy, but loans pay more. One personal loan approval can net you ₹1,000–₹3,000 the equivalent of four credit card approvals. Focus on people with actual borrowing needs. Loans Without Credit Score 2026 has details on products with flexible criteria.

Team building: GroMo pays you for recruiting successful partners. You earn when they hit milestones. If you recruit 20 active people who each earn ₹15,000 a month, you can generate a solid passive income stream on top of your own sales.

Your time allocation changes as you grow. Initially, you spend most of your time selling. Eventually, you spend more time training the people you've recruited.

How it compares to other apps

Platform | Income Model | Average Monthly Earning | Withdrawal Time | Scalability |

|---|---|---|---|---|

GroMo | Product commissions | ₹5,000–₹50,000 | 24–72 hours | High (team building) |

Google Opinion Rewards | Surveys | ₹200–₹500 | 7 days | Low (capped tasks) |

MPL/Dream11 | Gaming contests | -₹500–₹2,000 | 24 hours | Negative (loss risk) |

Meesho Reselling | Product markup | ₹2,000–₹15,000 | 7 days | Medium (inventory limits) |

YouTube Affiliate | Ad revenue share | ₹0–₹10,000 | 60 days | High (viral potential) |

Survey apps are capped by design. Gaming platforms are risky. Reselling requires managing inventory and returns. GroMo’s model is distinct because it avoids inventory and house edges. The limit is really just the size of your network and your conversion rate. More details on hitting four-figure daily numbers are available here: Earn ₹5,000 Daily from Home via GroMo.

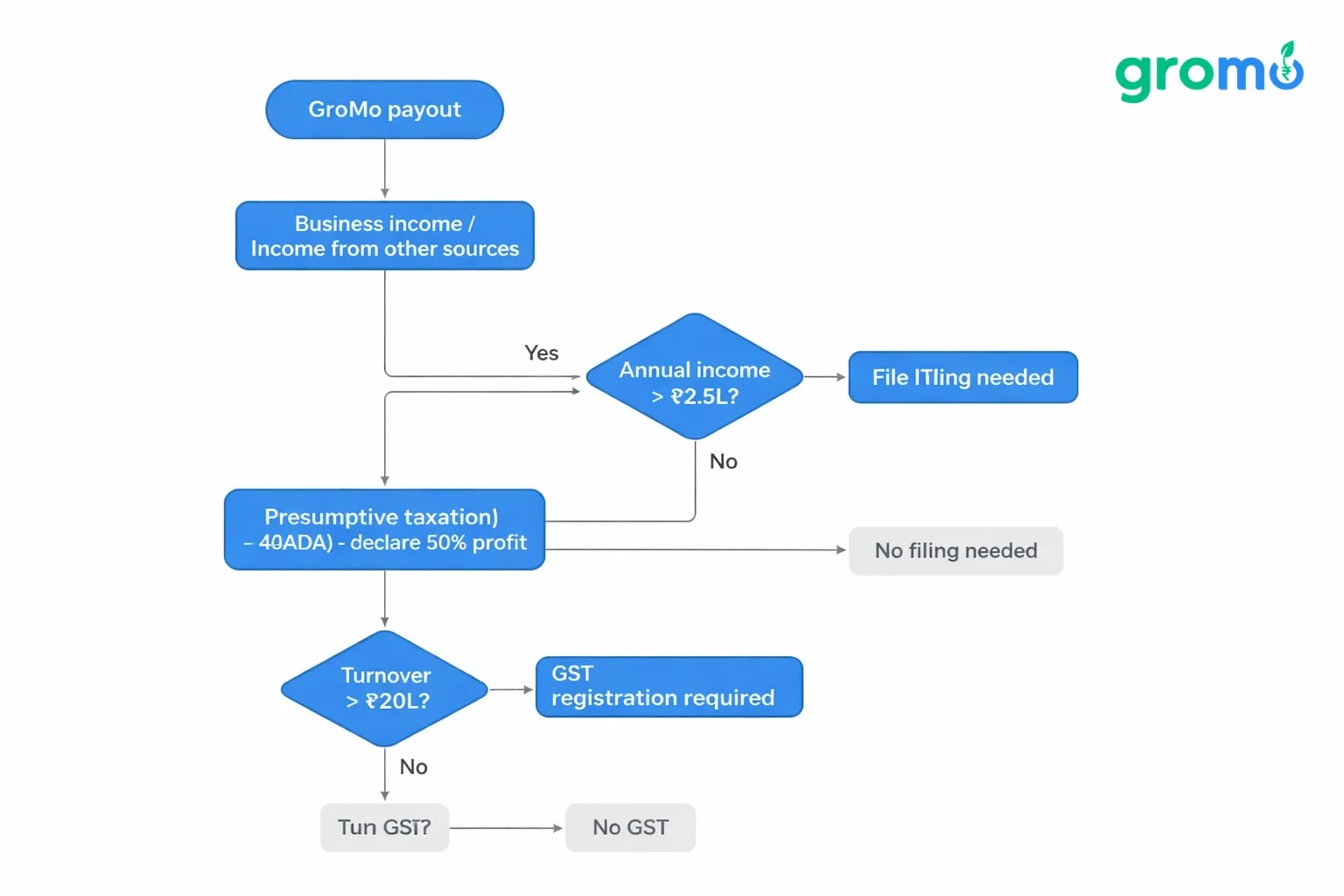

The tax angle

This income isn't tax-free. The Income Tax Act treats these payouts as "business income" or "income from other sources." If you earn over ₹2.5 lakh a year, you need to file ITR-3 or ITR-4.

You can use presumptive taxation (Section 44ADA) to declare 50% of your receipts as profit, paying tax only on that amount. This is often simpler than tracking every expense for internet or phone bills.

If your annual turnover crosses ₹20 lakh, GST registration becomes mandatory. You would need to file quarterly returns. Currently, TDS doesn't apply to GroMo payouts, but you should keep records of your earnings for tax filing. For a deeper look, Financial Product Distribution in India covers the tax specifics.

Mistakes that kill your earnings

Spamming: Posting links in unrelated groups gets you banned by admins and ignored by users. Context matters. Share links where finance is relevant.

Ignoring eligibility: Pitching a premium card to someone who doesn't meet the income threshold is a waste of time for everyone. Use the success-rate tool.

Poor follow-up: Most people won't apply immediately. A gentle reminder the next day can convert drop-offs.

Chasing only big payouts: Business loans pay well but convert rarely. Savings accounts pay less but convert often. A mix is safer.

Not educating customers: If a customer doesn't understand the fees, they will blame you when the charge hits. Explain the terms upfront.

Fintech trends in 2026

Digital lending grew 40% last year. UPI-linked credit is massive now HDFC and Tata Neu cards let people scan and pay with credit. This expands your potential market to anyone using UPI.

Neo-banking is also taking off, with zero-balance accounts attracting younger users. The India Fintech Revolution 2026 overview predicts neobank accounts will soon outnumber traditional ones.

Regulations are tightening, though. NBFCs now require higher credit scores for personal loans. This pushes demand toward secured loans or products for lower scores, covered in Loans for Bad CIBIL Scores 2026. GroMo has also introduced AI-powered lead scoring to help partners predict which products will convert best.

Who should try this

Salaried professionals: Use lunch breaks for follow-ups and evenings for outreach. It fits around a 9–6 job. See Earn ₹1 Lakh Monthly While Working Full-Time.

Stay-at-home parents: The 10 AM–3 PM window is ideal. School WhatsApp groups provide a natural network.

College students: Campus networks are full of potential leads final year students with internships, for example.

Small business owners: You can cross-sell to existing customers. A mobile shop owner can suggest cards with phone insurance benefits.

Retired professionals: Ex-bankers or insurance agents already know the products and can work from home without sales targets.

Frequently Asked Questions

Q: How to earn ₹1000 daily in India?

A: You can hit ₹1,000 daily by closing 1–2 sales. One credit card approval (₹300–₹800) plus a savings account (₹200–₹400) gets you there. Focus on pre-qualified leads to maintain consistency.

Q: Who is no 1 earning app without investment?

A: GroMo is a top contender with 6 million partners and ₹100 crore in payouts. Unlike survey apps, its commission model allows for significant scaling.

Q: What is the No. 1 money earning app?

A: GroMo ranks highly due to fast payouts (24–72 hours) and high commissions per transaction (₹300–₹10,000). Its reliability is reflected in its user reviews.

Q: How to earn 500 rupees per day?

A: Earning ₹500 daily is feasible with a single conversion. Identify 2–3 potential customers, check their eligibility, and follow up to keep the numbers consistent.