Earn in Rupees with GroMo: Zero Investment Income Guide

Many Indians want to know how to earn dollars in India without leaving home. The answer usually involves global platforms. But there's a simpler option: using Indian fintech distribution specifically selling financial products through GroMo to convert local referrals into rupee income. It often beats dollar gigs in purchasing power and simplicity.

Earning dollars sounds glamorous. But currency conversion fees, tax compliance, and payment gateway restrictions make it impractical for most people. GroMo lets you earn ₹300–5,000 daily with zero investment by distributing credit cards, loans, and savings accounts. Here's how both paths work and why GroMo often wins.

Understanding dollar-earning opportunities from India

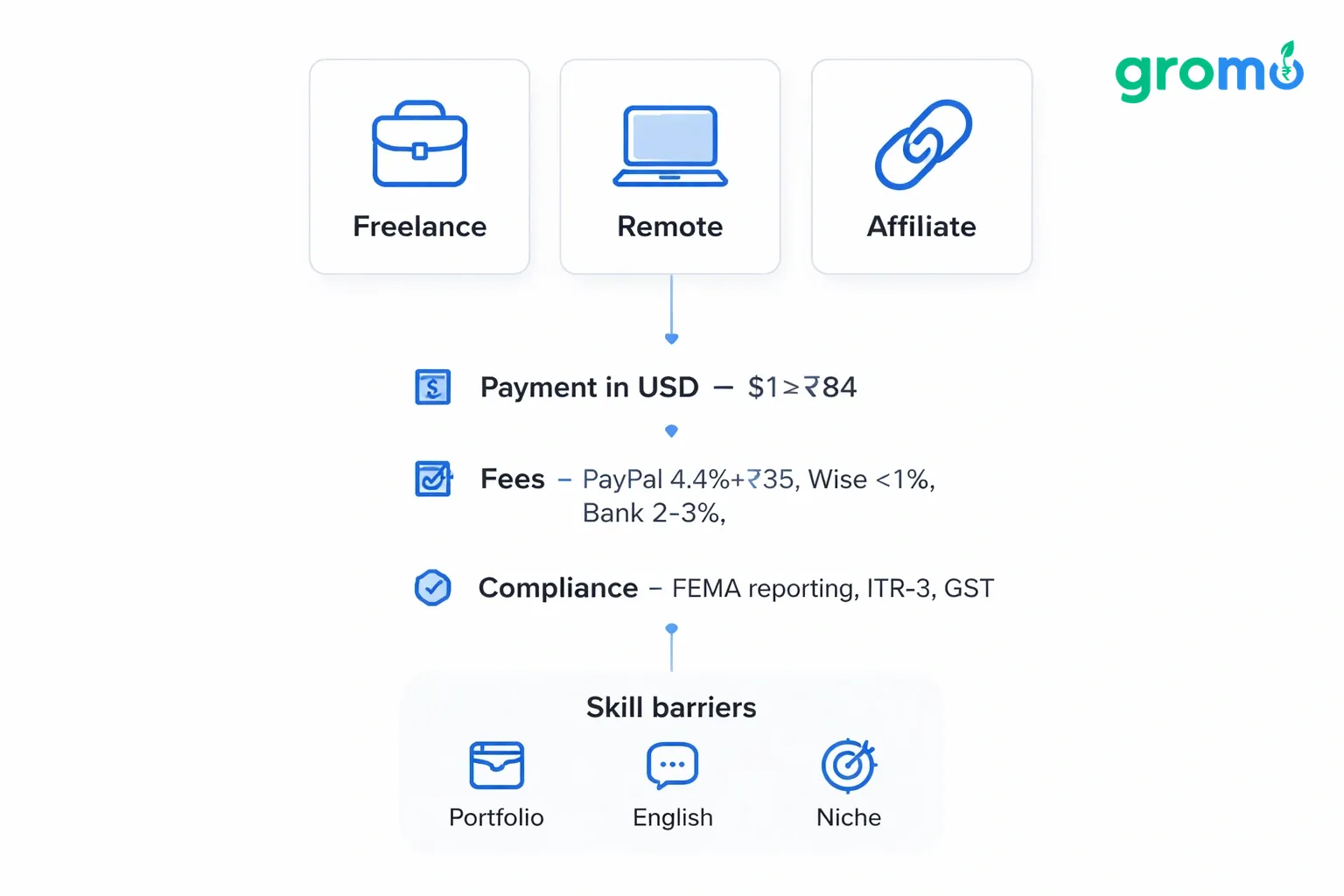

Dollar-earning from India means receiving payment in USD (or other foreign currencies) for services rendered remotely. Freelance platforms, remote jobs, and affiliate marketing are the three main channels. Freelancers on Upwork or Fiverr quote in dollars; remote employees of US/EU companies receive USD salaries; affiliates promoting global products earn commissions in foreign currency. Each route requires different skills, payment infrastructure, and tax handling.

The appeal is obvious: $1 ≈ ₹84 (May 2026), so $100 = ₹8,400. But hidden costs eat into this arbitrage. PayPal charges 4.4% + ₹35 per transaction; Wise (formerly TransferWise) takes 0.5–1%; banks add forex margins of 2–3%. A $500 invoice shrinks to ₹39,000 after deductions still decent, but not the windfall it appears.

Taxes complicate things further. FEMA regulations require reporting foreign income exceeding ₹7 lakh annually. Freelancers must file ITR-3 with full P&L statements; TDS on foreign remittances creates cash-flow gaps; and GST applies if you invoice abroad as a service exporter. Most early-stage earners skip compliance, risking penalties.

Skill barriers are equally high. Fiverr and Upwork favor established portfolios; new sellers wait months for their first order. Remote jobs demand fluent English, time-zone alignment (calls at 9 PM IST for US clients), and niche expertise data science, design, copywriting. If you lack these, dollar-earning remains out of reach.

The GroMo alternative: Earn in rupees, scale faster

GroMo offers commission-based income by letting you sell financial products credit cards, personal loans, demat accounts, savings accounts to friends, family, and social networks. You share product links; when someone applies and gets approved, you earn instant payouts. No inventory, no customer service, no foreign-currency headaches.

GroMo's model is built for India's digital-first economy. Over 60 lakh partners have collectively earned ₹100 crores. The app provides free training to become a certified financial advisor, customer-management tools to track applications, and personalized marketing content (WhatsApp templates, social-media creatives, digital visiting cards). You focus on referrals; GroMo handles compliance, payouts, and backend integrations with banks.

Payouts are immediate within hours of loan disbursal or card dispatch not the 30–60 day cycles typical of freelance platforms. A single Kotak 811 Super savings account earns you ₹800; an IDFC FIRST Ashva credit card pays ₹5,000; a Hero Fincorp personal loan can fetch ₹1,500–3,500 depending on disbursal amount. String together 5–10 conversions monthly, and you clear ₹15,000–50,000 without ever touching a dollar.

The real advantage is compounding. Refer friends to join GroMo, and you earn from their conversions too. Build a team of 20 active partners, and passive referral income flows in. This network effect works like MLM (multi-level marketing) but without upfront fees, inventory risk, or pyramid-scheme stigma because you're distributing legitimate banking products.

Real dollar-earning methods: What actually works

Freelancing platforms Upwork, Fiverr, Toptal, Freelancer.com are the default dollar-earning routes. Upwork alone has 12 million freelancers; competition is fierce. To break through, you need a niche (Python automation, Shopify theme development, medical transcription) and a portfolio showcasing past work. Expect to underbid initially: $5–10/hour for entry-level gigs. Seasoned freelancers charge $50–150/hour, but reaching that tier takes 2–3 years of consistent delivery and 5-star reviews.

Remote employment is the premium option. Platforms like Remote.co, We Work Remotely, and AngelList list full-time positions paying $40,000–120,000 annually. Indian developers at Stripe, Figma, or GitLab earn $80,000+, which converts to ₹67 lakh/year. But these jobs demand Silicon Valley–caliber skills, GitHub portfolios, and cultural fit. They're not accessible to the average college student or housewife looking for side income.

Affiliate marketing for global products Amazon Associates (US), ClickBank, CJ Affiliate pays in dollars when you drive sales through your links. A tech blog promoting VPN subscriptions or web-hosting can earn $500–2,000/month passively. However, building traffic takes 12–18 months of SEO-optimized content, email-list cultivation, and consistent posting. It's a long game, not a quick win.

Content creation on YouTube (AdSense dollars) or Medium (Partner Program) monetizes views and reads. A YouTube channel with 100,000 subscribers and 1 million monthly views earns $500–1,500/month from ads. Medium pays $0.01–0.10 per read; top writers make $1,000–5,000/month. Both require viral-ready content, audience engagement, and algorithmic luck skills that take years to hone.

Why GroMo outpaces dollar gigs for most Indians

Speed to first rupee is GroMo's killer advantage. Freelance platforms require profile setup, portfolio building, proposal writing, client vetting, project delivery, and payment release typically 30+ days for your first dollar. GroMo partners earn within 24 hours of their first successful referral. Download the app, complete 15-minute training, share a Kotak 811 link to a friend, and earn ₹550 the moment they open an account.

No specialized skills are needed. Freelancing demands coding, design, writing, or marketing expertise. GroMo requires social capital friends, family, WhatsApp groups, local community ties. If you can send a message and follow up, you can earn. The app's training modules teach you how to pitch credit cards to salaried professionals, loans to small-business owners, and demat accounts to young investors. Everything is scripted and templated.

Payment reliability is guaranteed. Freelance clients ghost, dispute invoices, or delay payments for months. Fiverr holds funds for 14 days post-delivery; PayPal disputes freeze accounts. GroMo's payouts are contractual banks pay GroMo, GroMo pays you, instantly. There's no client negotiation, no refund drama, no currency-conversion limbo.

Tax simplicity saves headaches. Foreign income triggers FEMA compliance, ITR-3 filings, and potential scrutiny. GroMo earnings are domestic business income; you file ITR-4 (presumptive taxation at 6% of turnover) or ITR-3 with straightforward P&L. TDS is deducted at source if you cross thresholds, but everything stays within Indian tax law no RBI reporting, no SWIFT codes, no forex declarations.

Scalability through referrals is unmatched. A freelancer's income scales linearly with hours worked more clients, more time, same hourly rate. GroMo's referral-commission structure lets you earn from your team's conversions. Recruit 10 active partners who each close 5 deals/month; you earn overriding commissions on their 50 deals while sleeping. This is legitimate passive income, not MLM nonsense.

Step-by-step: Earning your first ₹5,000 on GroMo

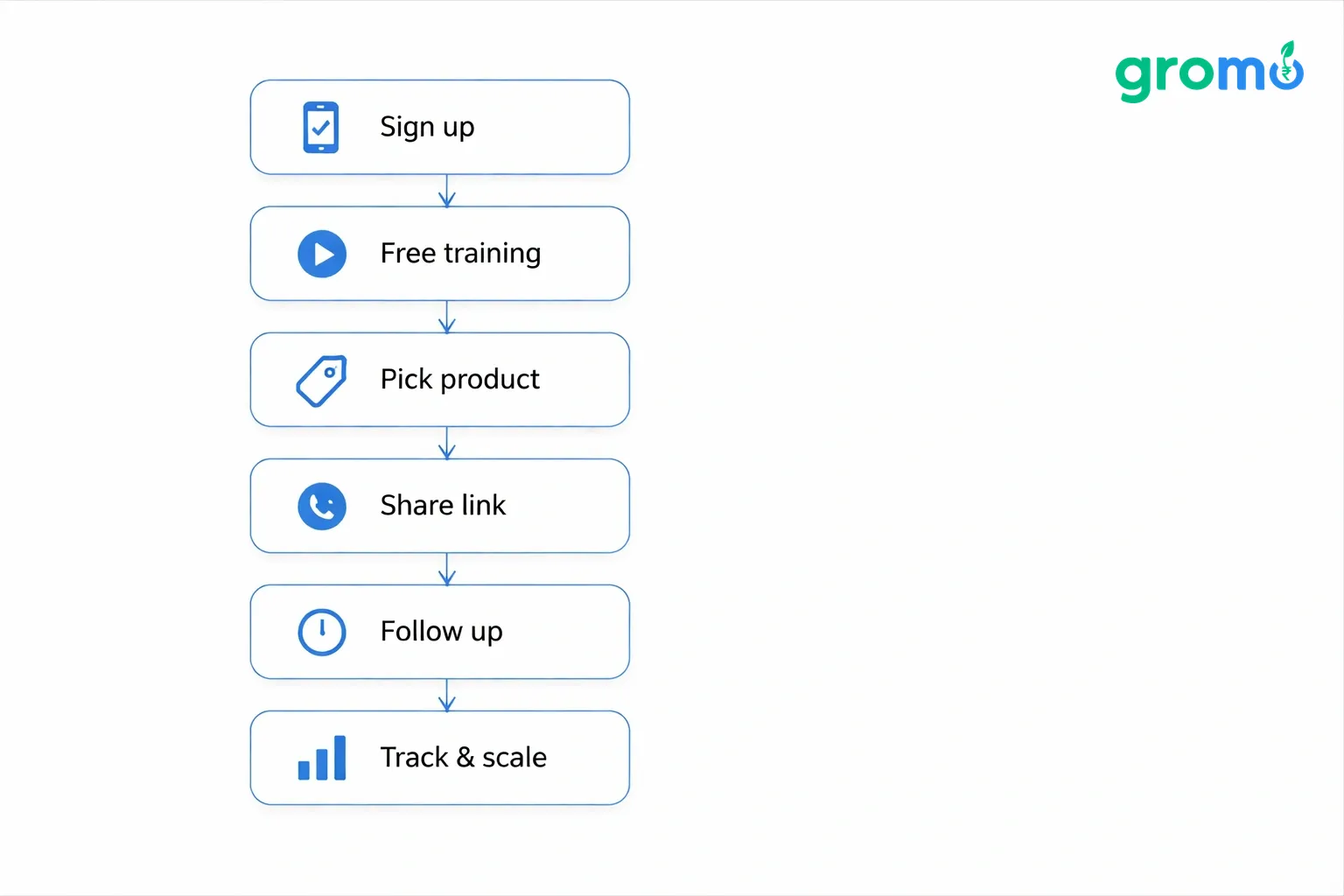

Download and sign up at app.gromo.co.in. Enter your mobile number, verify OTP, complete basic KYC (PAN, Aadhaar). The process takes 3 minutes. GroMo's interface is Hindi + English, designed for Tier 2/3 India.

Complete free training in the Academy tab. Watch 5-minute videos on how credit cards work, eligibility criteria for loans, and objection-handling scripts. Take the quiz to unlock certified-advisor status. This training is crucial it arms you with product knowledge and compliance guardrails (never promise guaranteed approvals, never ask for upfront fees from customers).

Choose high-payout products from the catalog. Start with Kotak 811 Super (₹800), IDFC FIRST Ashva Credit Card (₹5,000), or Hero Fincorp Personal Loan (₹1,500–3,500). These have high conversion rates because eligibility is broad and documentation is minimal. Avoid niche products (demat accounts for students, business loans for unregistered firms) until you understand customer pain points.

Share links via WhatsApp, SMS, social media. GroMo generates unique referral links for each product. Copy-paste the pre-written pitch ("Open Kotak 811 in 5 min, get ₹200 cashback + free debit card!") into your status or DM it to friends. Tag it with a call-to-action: "Reply 'interested' for link." Personalize messages don't spam generically.

Follow up within 24 hours. The app shows application status in real time. If someone clicks your link but doesn't complete KYC, nudge them: "Hey, saw you started the Kotak account takes just 2 more minutes, VKYC can be done on video call." Conversion rates jump from 10% to 40% with one follow-up.

Track payouts in the Wallet tab. Once the customer's account is opened (savings), card is dispatched (credit card), or loan is disbursed (personal loan), your commission hits your GroMo wallet. Withdraw to your bank account instantly no minimum threshold, no processing days.

Scale with referrals. Invite friends to become GroMo partners using your referral code. You earn ₹50–200 per recruit (depending on their activity), plus overriding commissions on their deals. Build a team of 20, and your monthly passive income can reach ₹10,000–30,000 even if you stop actively selling.

Hybrid strategy: Freelance + GroMo for maximum income

Combine both models if you're skilled enough for freelance work. Use freelance dollars ($500–1,000/month) as your primary income; layer GroMo commissions (₹15,000–30,000/month) as your safety net and savings fund. Freelance income is volatile client churn, project gaps, payment delays. GroMo provides steady, predictable cash flow to cover rent, groceries, and EMIs.

Allocate time efficiently. Dedicate mornings (9 AM–1 PM) to freelance client work; use evenings (6 PM–9 PM) for GroMo outreach WhatsApp broadcasts, social-media posts, follow-ups. Weekends are for team building: onboard new GroMo partners, conduct mini-webinars on your Facebook group, share success stories to motivate your network.

Leverage freelance networks for GroMo. Your freelance colleagues are salaried, creditworthy, digitally savvy perfect customers for premium credit cards (IDFC FIRST Ashva, SBI Tata Neu Infinity) and investment accounts (Upstox, 5paisa demat). A single WhatsApp group of 50 freelancers can yield 10–15 conversions monthly, earning you ₹30,000–50,000 without diluting your freelance focus.

Reinvest GroMo earnings into freelance upskilling. Use your first ₹20,000 GroMo payout to buy a Udemy course (advanced Figma, Python for data science, copywriting masterclass). Better skills → higher freelance rates → more dollars. GroMo becomes your self-funded education budget, creating a virtuous cycle of income growth.

Tax-optimize across both streams. Freelance income (foreign) and GroMo income (domestic) fall under different ITR sections. Claim Section 80C deductions (₹1.5 lakh/year) against GroMo earnings by investing in ELSS or PPF. Foreign income doesn't qualify for 80C, so you save more tax by structuring smartly. Consult a CA to maximize this arbitrage.

Common pitfalls and how to avoid them

Overpromising to customers kills trust. Never say "Your loan will definitely be approved" or "You'll get a ₹5 lakh credit limit." Banks decide based on credit scores, income proof, and internal policies. Your job is to help customers apply correctly complete documentation, accurate details, timely VKYC. Set expectations: "Eligibility depends on your profile; I'll guide you through the process."

Spamming WhatsApp groups gets you muted or banned. Instead of broadcasting links to 20 groups daily, identify 3–5 high-intent groups (alumni networks, housing-society chats, freelancer communities) and engage genuinely. Answer finance questions, share tips on credit scores, post success stories. When someone asks "How do I get a loan?", then share your GroMo link with context.

Ignoring compliance invites legal trouble. GroMo's training explicitly prohibits charging customers upfront fees, making job-placement promises, or misrepresenting product terms. If you violate these, your account gets blocked and payouts reversed. Follow the scripts, disclose fees clearly (e.g., Tide Business Account has ₹590 debit-card fee), and never pressure anyone to apply.

Neglecting follow-ups tanks conversion. 60% of customers click your link but don't complete KYC within 24 hours they get distracted, unsure about documents, or lazy. A simple "Hi [Name], need any help completing the Kotak account? I can walk you through VKYC on a call" doubles your close rate. Use GroMo's reminder feature to automate this.

Failing to build a team caps your income. Solo partners hit a ceiling at ₹30,000–50,000/month because there are only so many people in your immediate network. Recruiting 10–20 active sub-partners unlocks overriding commissions and scales you to ₹1 lakh+/month. Dedicate 20% of your time to team training, motivation, and support it's the difference between a side hustle and a sustainable business.

Comparing GroMo to other Indian earning models

GroMo vs. freelancing: Freelancing pays more per hour ($10–50/hour = ₹840–4,200/hour) but demands rare skills and competes globally. GroMo pays less per transaction (₹300–5,000) but requires only social skills and local networks. Freelancing scales linearly; GroMo scales exponentially via referrals. Freelancers earn ₹30,000–1 lakh/month after 1–2 years; GroMo partners hit ₹50,000–1 lakh in 6–9 months with consistent effort.

GroMo vs. ad-watching apps: Apps like Roz Dhan, Pocket Money, or TaskBucks pay ₹5–50/day for watching ads, filling surveys, or playing games. GroMo partners earn 20x more because financial-product commissions are ₹300–5,000 per conversion vs. ₹5 per ad. Ad apps waste time; GroMo builds a real business.

GroMo vs. traditional DSA (Direct Selling Agent): Bank DSAs earn similar commissions but require physical paperwork, branch visits, and months-long approval cycles. GroMo digitizes everything customers complete KYC on their phones, approvals happen in 24–48 hours, payouts are instant. DSAs also pay ₹10,000–50,000 upfront for tie-ups; GroMo is free.

GroMo vs. affiliate marketing: Amazon Associates or Flipkart Affiliate pay 1–10% of product value; you need high-traffic blogs or YouTube channels. GroMo pays fixed commissions (₹300–5,000) per conversion, independent of transaction value. A single Kotak 811 referral (₹800) beats 50 Amazon book sales (₹10 each). Affiliate marketing takes 12+ months to scale; GroMo delivers in weeks.

GroMo vs. reselling (Meesho, GlowRoad): Reselling earns ₹50–200 per sale, requires inventory management, shipping coordination, and return handling. GroMo is fully digital no inventory, no logistics. Margins are higher (₹300–5,000 vs. ₹50–200), and there's no capital blockage. Reselling suits product-savvy entrepreneurs; GroMo suits relationship-driven networkers.

Tax and legal considerations for GroMo earnings

GroMo income is business income under Section 44ADA (presumptive taxation for professionals) or Section 44AD (presumptive taxation for businesses). If your annual GroMo earnings are ≤₹50 lakh, declare 50% of receipts as profit and pay tax on that. Example: ₹6 lakh annual earnings → ₹3 lakh taxable profit → ₹15,600 tax (5% slab + 4% cess). No need for detailed bookkeeping.

If you earn >₹50 lakh annually, file ITR-3 with full P&L and balance sheet. GroMo's dashboard exports payout reports; download quarterly and share with your CA. Deduct business expenses mobile recharge, internet bills, travel for team meetings, promotional costs (WhatsApp broadcasts, Facebook ads). Net profit is taxable.

TDS (Tax Deducted at Source) applies if GroMo's parent company pays you >₹15,000 in a year under Section 194H (commission). GroMo auto-deducts 5% TDS and issues Form 16A. You claim this TDS as advance tax when filing your return. No double taxation just a timing issue.

GST registration is optional below ₹20 lakh annual turnover. Above ₹20 lakh, register for GST and charge 18% on your commissions. GroMo-classified services (business auxiliary services, SAC 998599) are taxable. File GSTR-3B monthly and GSTR-1 quarterly. Most partners stay below ₹20 lakh, so GST is irrelevant.

No FEMA reporting because GroMo earnings are domestic. Unlike freelance dollar income, you don't file LUT (Letter of Undertaking) or report to RBI. Simpler compliance = fewer errors and penalties.

Real-world success stories and earnings benchmarks

Rajesh from Jaipur, a college student, started GroMo in January 2026. He shared Kotak 811 and IDFC credit-card links in his hostel WhatsApp group. First month: 8 conversions, ₹5,200 earned. By March, he recruited 5 batchmates as sub-partners and earned ₹18,000 (own deals + overriding commissions). April: ₹32,000. May projection: ₹50,000. He now funds his semester fees from GroMo no parental support needed.

Priya, a housewife in Pune, wanted side income without leaving home. She downloaded GroMo in February 2026, completed training, and started pitching savings accounts to her kitty-party group. First month: ₹4,500 from 6 conversions. She then tapped into her husband's office colleagues (200+ employees) and closed 15 credit cards in March, earning ₹42,000. By May, she's averaging ₹60,000/month with a 10-person team under her.

Vikram, a freelance graphic designer in Bangalore, combined GroMo with his Fiverr gigs. Fiverr income: $800/month (₹67,000). GroMo income: ₹25,000/month from referrals in design communities. Total: ₹92,000/month. He uses GroMo cash for rent and EMIs, keeping freelance dollars for savings and investments. This hybrid model gives him financial stability even when client projects dry up.

Anjali from Lucknow, a BPO employee earning ₹20,000/month, doubled her income with GroMo. She dedicates 2 hours daily (8 PM–10 PM) to sharing loan and credit-card links in local Facebook groups. Monthly GroMo earnings: ₹22,000–28,000. Combined salary + GroMo: ₹42,000–48,000. She's now saving for a car down payment impossible on salary alone.

These aren't outliers. GroMo's leaderboard (visible in-app) shows 100+ partners earning >₹1 lakh/month, 5,000+ earning ₹30,000–1 lakh, and 50,000+ earning ₹5,000–30,000. Consistency, follow-up discipline, and team building separate top earners from casual users.

Practical tips to maximize GroMo income

Segment your audience. Salaried professionals (IT, banking, teaching) are ideal for premium credit cards and personal loans. Small-business owners need business loans and current accounts (Tide Business). Students want demat accounts and zero-balance savings accounts. Tailor your pitch: don't spam a ₹5 lakh loan link to a college group or a student account to a CEO.

Use video testimonials. Record 30-second WhatsApp status videos: "I helped Ramesh get a ₹3 lakh loan in 48 hours if you need funds, DM me." Social proof converts. People trust recommendations from real humans, not faceless links. Your face + success story = credibility.

Host mini-webinars. Create a Zoom room or Instagram Live: "How to improve your credit score in 30 days" or "Best credit cards for online shopping." Share GroMo links at the end. Educate first, sell second. 20-minute sessions build authority and generate 10–15 warm leads per session.

Leverage festivals and salary days. January (New Year resolutions), April (financial year-end), August (Independence Day sales), October (Diwali shopping) these are high-conversion periods. Push credit cards and personal loans hard during these months. Salary-day targeting (1st–7th of every month) also boosts loan approvals because affordability checks pass easily.

Gamify your team. If you've built a 10-person team, run monthly contests: "Whoever closes 20 deals wins ₹2,000 bonus from my earnings." Competition motivates dormant partners. Share leaderboard screenshots in your WhatsApp group. Peer pressure + rewards = higher activity.

Reinvest 20% of earnings into ads. Spend ₹5,000/month on Facebook or Instagram ads targeting your city. Promote high-ticket products (IDFC credit card, Hero Fincorp loan). Drive traffic to a simple Google Form → collect leads → follow up personally. Paid ads scale beyond your organic network and can 3x your conversions.

Why GroMo is the smarter path than dollar chasing

Chasing dollars from India is a mirage for 90% of people. Freelancing, remote jobs, and global affiliate marketing demand skills most Indians don't have native-level English, specialized tech knowledge, portfolio traction. Even if you acquire these, you compete with Filipinos, Pakistanis, Ukrainians who undercut you. Payment friction, tax complexity, and currency-conversion losses erode the dollar premium.

GroMo eliminates all barriers. No skill moat just social capital. No global competition you sell to your local network. No payment hassles instant rupee payouts. No tax mazes simple ITR-4 filing. And unlike freelancing, GroMo scales exponentially via referrals. Your 10-person team can earn you ₹30,000/month passively while you sleep or work another job.

The purchasing-power argument clinches it. $500 = ₹42,000 sounds great, but after PayPal fees, forex margins, and 30% tax, you net ₹25,000. A GroMo partner closing 8 deals (4 credit cards, 3 savings accounts, 1 loan) earns ₹28,000 in the same month with zero deductions, instant payouts, and no client drama. In real-take-home terms, GroMo matches or beats freelance dollars for average Indians.

Zero-investment business models are the future. As India digitizes and financial inclusion deepens, demand for credit cards, loans, and investment accounts will explode. GroMo positions you at the center of this boom earning commissions from a ₹50 lakh crore credit market without owning a bank or becoming a CA. It's the smartest wealth-creation lever for non-elite Indians in 2026.

Frequently Asked Questions

Q: Can I earn dollars from India?

A: Yes, through freelancing (Upwork, Fiverr), remote jobs, or global affiliate marketing. However, payment gateway fees (4–6%), forex margins (2–3%), FEMA compliance, and tax complexity make it challenging. Most Indians earn more in purchasing-power terms by focusing on rupee-based platforms like GroMo, which pay ₹300–5,000 per conversion instantly with zero currency-conversion hassles.

Q: How to earn 100 dollars per day?

A: $100/day = $3,000/month = ₹2.5 lakh/month. Achieving this requires either freelancing at $50–100/hour (4–6 billable hours daily), landing a remote full-time job ($60,000+ annual salary), or scaling affiliate/content businesses to 500,000+ monthly visitors. Entry barrier is high 2–3 years of skill-building and portfolio development. Alternatively, GroMo lets you earn ₹1 lakh+/month (= $1,200/month = $40/day) in 6–9 months via referrals and team-building, which is more accessible for most.

Q: How to earn ₹1000 daily in India?

A: ₹1,000/day = ₹30,000/month. On GroMo, close 6–8 financial-product deals monthly (mix of credit cards ₹1,500–5,000, savings accounts ₹300–800, loans ₹1,500–3,500). With consistent follow-ups and a 20–30% conversion rate from 30–40 leads, this is achievable in 2–3 months. Alternatively, combine a part-time job (₹15,000/month) with GroMo side income (₹15,000/month) to cross ₹30,000. Learn daily-earning strategies here.

Q: How can I get dollars in India?

A: Open a PayPal, Wise, or Payoneer account to receive international payments. Alternatively, use Stripe Atlas (for US LLC formation) or foreign bank accounts (HDFC's PayZapp Forex Card, ICICI's Money2India). However, receiving dollars doesn't mean keeping them you must convert to rupees for spending, incurring 3–5% total fees. For most use cases (earning online), focusing on rupee-based platforms like GroMo, Meesho, or YouTube India (INR payouts) is simpler and nets higher take-home income after costs.